Bill Gates

Auto Added by WPeMatico

Auto Added by WPeMatico

“The book itself is a curious artefact, not showy in its technology but complex and extremely efficient: a really neat little device, compact, often very pleasant to look at and handle, that can last decades, even centuries. It doesn’t have to be plugged in, activated, or performed by a machine; all it needs is light, a human eye, and a human mind. It is not one of a kind, and it is not ephemeral. It lasts. It is reliable. If a book told you something when you were 15, it will tell it to you again when you’re 50, though you may understand it so differently that it seems you’re reading a whole new book.”—Ursula K. Le Guin

Every year, Bill Gates goes off-grid, leaves friends and family behind, and spends two weeks holed up in a cabin reading books. His annual reading list rivals Oprah’s Book Club as a publishing kingmaker. Not to be outdone, Mark Zuckerberg shared a reading recommendation every two weeks for a year, dubbing 2015 his “Year of Books.” Susan Wojcicki, CEO of YouTube, joined the board of Room to Read when she realized how books like The Evolution of Calpurnia Tate were inspiring girls to pursue careers in science and technology. Many a biotech entrepreneur treasures a dog-eared copy of Daniel Suarez’s Change Agent, which extrapolates the future of CRISPR. Noah Yuval Harari’s sweeping account of world history, Sapiens, is de rigueur for Silicon Valley nightstands.

This obsession with literature isn’t limited to founders. Investors are just as avid bookworms. “Reading was my first love,” says AngelList’s Naval Ravikant. “There is always a book to capture the imagination.” Ravikant reads dozens of books at a time, dipping in and out of each one nonlinearly. When asked about his preternatural instincts, Lux Capital’s Josh Wolfe advised investors to “read voraciously and connect dots.” Foundry Group’s Brad Feld has reviewed 1,197 books on Goodreads and especially loves science fiction novels that “make the step function leaps in imagination that represent the coming dislocation from our current reality.”

This begs a fascinating question: Why do the people building the future spend so much of their scarcest resource — time — reading books?

Image by NiseriN via Getty Images. Reading time approximately 14 minutes.

Do innovators read in order to mine literature for ideas? The Kindle was built to the specs of a science fictional children’s storybook featured in Neal Stephenson’s novel The Diamond Age, in fact, the Kindle project team was originally codenamed “Fiona” after the novel’s protagonist. Jeff Bezos later hired Stephenson as the first employee at his space startup Blue Origin. But this literary prototyping is the exception that proves the rule. To understand the extent of the feedback loop between books and technology, it’s necessary to attack the subject from a less direct angle.

David Mitchell’s Cloud Atlas is full of indirect angles that all manage to reveal deeper truths. It’s a mind-bending novel that follows six different characters through an intricate web of interconnected stories spanning three centuries. The book is a feat of pure M.C. Escher-esque imagination, featuring a structure as creative and compelling as its content. Mitchell takes the reader on a journey ranging from the 19th century South Pacific to a far-future Korean corpocracy and challenges the reader to rethink the very idea of civilization along the way. “Power, time, gravity, love,” writes Mitchell. “The forces that really kick ass are all invisible.”

The technological incarnations of these invisible forces are precisely what Kevin Kelly seeks to catalog in The Inevitable. Kelly is an enthusiastic observer of the impact of technology on the human condition. He was a co-founder of Wired, and the insights explored in his book are deep, provocative, and wide-ranging. In his own words, “When answers become cheap, good questions become more difficult and therefore more valuable.” The Inevitable raises many important questions that will shape the next few decades, not least of which concern the impacts of AI:

“Over the past 60 years, as mechanical processes have replicated behaviors and talents we thought were unique to humans, we’ve had to change our minds about what sets us apart. As we invent more species of AI, we will be forced to surrender more of what is supposedly unique about humans. Each step of surrender—we are not the only mind that can play chess, fly a plane, make music, or invent a mathematical law—will be painful and sad. We’ll spend the next three decades—indeed, perhaps the next century—in a permanent identity crisis, continually asking ourselves what humans are good for. If we aren’t unique toolmakers, or artists, or moral ethicists, then what, if anything, makes us special? In the grandest irony of all, the greatest benefit of an everyday, utilitarian AI will not be increased productivity or an economics of abundance or a new way of doing science—although all those will happen. The greatest benefit of the arrival of artificial intelligence is that AIs will help define humanity. We need AIs to tell us who we are.”

It is precisely this kind of an AI-influenced world that Richard Powers describes so powerfully in his extraordinary novel The Overstory:

“Signals swarm through Mimi’s phone. Suppressed updates and smart alerts chime at her. Notifications to flick away. Viral memes and clickable comment wars, millions of unread posts demanding to be ranked. Everyone around her in the park is likewise busy, tapping and swiping, each with a universe in his palm. A massive, crowd-sourced urgency unfolds in Like-Land, and the learners, watching over these humans’ shoulders, noting each time a person clicks, begin to see what it might be: people, vanishing en masse into a replicated paradise.”

Taking this a step further, Virginia Heffernan points out in Magic and Loss that living in a digitally mediated reality impacts our inner lives at least as much as the world we inhabit:

“The Internet suggests immortality—comes just shy of promising it—with its magic. With its readability and persistence of data. With its suggestion of universal connectedness. With its disembodied imagines and sounds. And then, just as suddenly, it stirs grief: the deep feeling that digitization has cost us something very profound. That connectedness is illusory; that we’re all more alone than ever.”

And it is the questionable assumptions underlying such a future that Nick Harkaway enumerates in his existential speculative thriller Gnomon:

“Imagine how safe it would feel to know that no one could ever commit a crime of violence and go unnoticed, ever again. Imagine what it would mean to us to know—know for certain—that the plane or the bus we’re travelling on is properly maintained, that the teacher who looks after our children doesn’t have ugly secrets. All it would cost is our privacy, and to be honest who really cares about that? What secrets would you need to keep from a mathematical construct without a heart? From a card index? Why would it matter? And there couldn’t be any abuse of the system, because the system would be built not to allow it. It’s the pathway we’re taking now, that we’ve been on for a while.”

Machine learning pioneer, former President of Google China, and leading Chinese venture capitalist Kai-Fu Lee loves reading science fiction in this vein — books that extrapolate AI futures — like Hao Jingfang’s Hugo Award-winning Folding Beijing. Lee’s own book, AI Superpowers, provides a thought-provoking overview of the burgeoning feedback loop between machine learning and geopolitics. As AI becomes more and more powerful, it becomes an instrument of power, and this book outlines what that means for the 21st century world stage:

“Many techno-optimists and historians would argue that productivity gains from new technology almost always produce benefits throughout the economy, creating more jobs and prosperity than before. But not all inventions are created equal. Some changes replace one kind of labor (the calculator), and some disrupt a whole industry (the cotton gin). Then there are technological changes on a grander scale. These don’t merely affect one task or one industry but drive changes across hundreds of them. In the past three centuries, we’ve only really seen three such inventions: the steam engine, electrification, and information technology.”

So what’s different this time? Lee points out that “AI is inherently monopolistic: A company with more data and better algorithms will gain ever more users and data. This self-reinforcing cycle will lead to winner-take-all markets, with one company making massive profits while its rivals languish.” This tendency toward centralization has profound implications for the restructuring of world order:

“The AI revolution will be of the magnitude of the Industrial Revolution—but probably larger and definitely faster. Where the steam engine only took over physical labor, AI can perform both intellectual and physical labor. And where the Industrial Revolution took centuries to spread beyond Europe and the U.S., AI applications are already being adopted simultaneously all across the world.”

Cloud Atlas, The Inevitable, The Overstory, Gnomon, Folding Beijing, and AI Superpowers might appear to predict the future, but in fact they do something far more interesting and useful: reframe the present. They invite us to look at the world from new angles and through fresh eyes. And cultivating “beginner’s mind” is the problem for anyone hoping to build or bet on the future.

Powered by WPeMatico

Young founders who want to start companies while still in school have an increasing number of resources to tap into that exist just for them. Students that want to learn how to build companies can apply to an increasing number of fast-track programs that allow them to gain valuable early stage operating experience. The energy around student entrepreneurship today is incredible. I’ve been immersed in this community as an investor and adviser for some time now, and to say the least, I’m continually blown away by what the next generation of innovators are dreaming up (from Analytical Space’s global data relay service for satellites to Brooklinen’s reinvention of the luxury bed).

Bill Gates in 1973

First, let’s look at student founders and why they’re important. Student entrepreneurs have long been an important foundation of the startup ecosystem. Many students wrestle with how best to learn while in school —some students learn best through lectures, while more entrepreneurial students like author Julian Docks find it best to leave the classroom altogether and build a business instead.

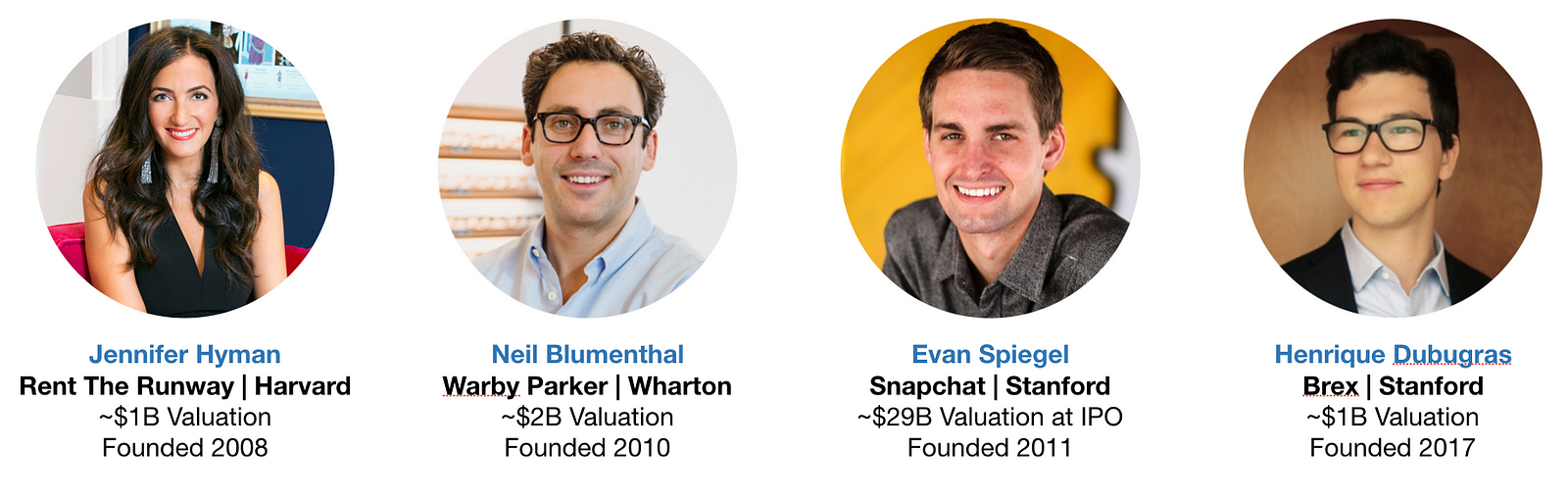

Indeed, some of our most iconic founders are Microsoft’s Bill Gates and Facebook’s Mark Zuckerberg, both student entrepreneurs who launched their startups at Harvard and then dropped out to build their companies into major tech giants. A sample of the current generation of marquee companies founded on college campuses include Snap at Stanford ($29B valuation at IPO), Warby Parker at Wharton (~$2B valuation), Rent The Runway at HBS (~$1B valuation), and Brex at Stanford (~$1B valuation).

Some of today’s most celebrated tech leaders built their first ventures while in school — even if some student startups fail, the critical first-time founder experience is an invaluable education in how to build great companies. Perhaps the best example of this that I could find is Drew Houston at Dropbox (~$9B valuation at IPO), who previously founded an edtech startup at MIT that, in his words, provided a: “great introduction to the wild world of starting companies.”

Student founders are everywhere, but the highest concentration of venture-backed student founders can be found at just 5 universities. Based on venture fund portfolio data from the last six years, Harvard, Stanford, MIT, UPenn, and UC Berkeley have produced the highest number of student-founded companies that went on to raise $1 million or more in seed capital. Some prospective students will even enroll in a university specifically for its reputation of churning out great entrepreneurs. This is not to say that great companies are not being built out of other universities, nor does it mean students can’t find resources outside a select number of schools. As you can see later in this essay, there are a number of new ways students all around the country can tap into the startup ecosystem. For further reading, PitchBook produces an excellent report each year that tracks where all entrepreneurs earned their undergraduate degrees.

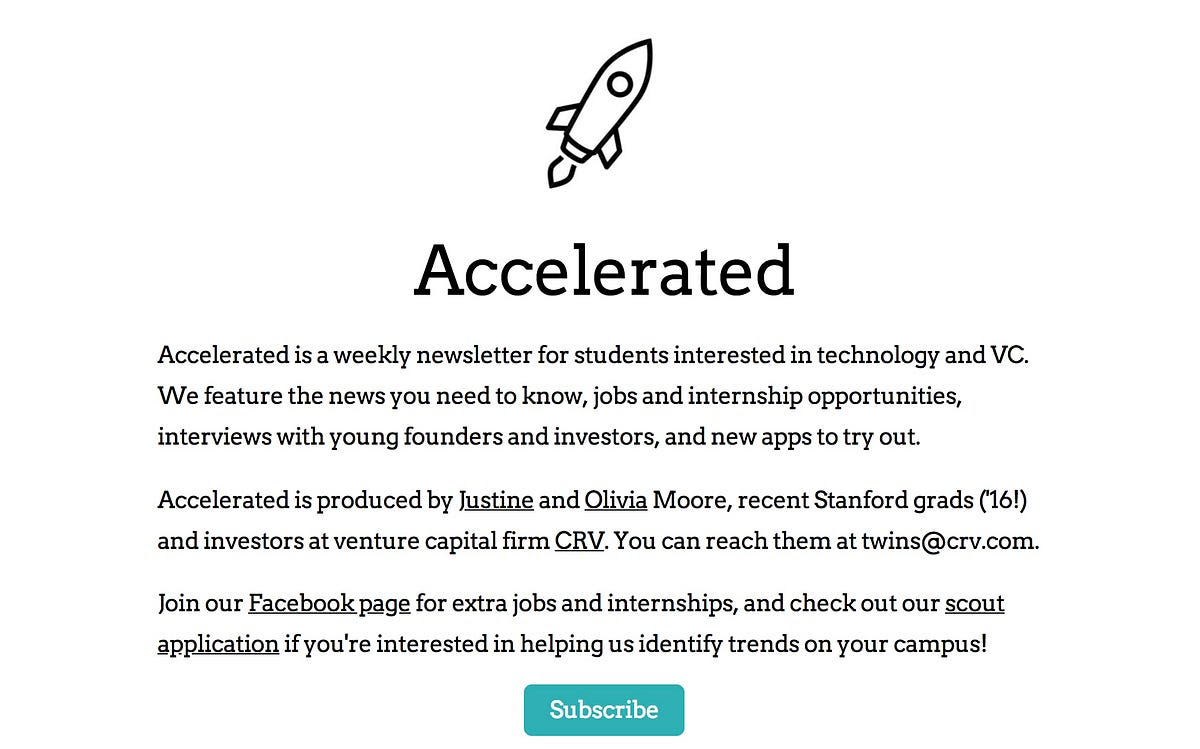

Student founders have a number of new media resources to turn to. New email newsletters focused on student entrepreneurship like Justine and Olivia Moore’s Accelerated and Kyle Robertson’s StartU offer new channels for young founders to reach large audiences. Justine and Olivia, the minds behind Accelerated, have a lot of street cred— they launched Stanford’s on-campus incubator Cardinal Ventures before landing as investors at CRV.

StartU goes above and beyond to be a resource to founders they profile by helping to connect them with investors (they’re active at 12 universities), and run a podcast hosted by their Editor-in-Chief Johnny Hammond that is top notch. My bet is that traditional media will point a larger spotlight at student entrepreneurship going forward.

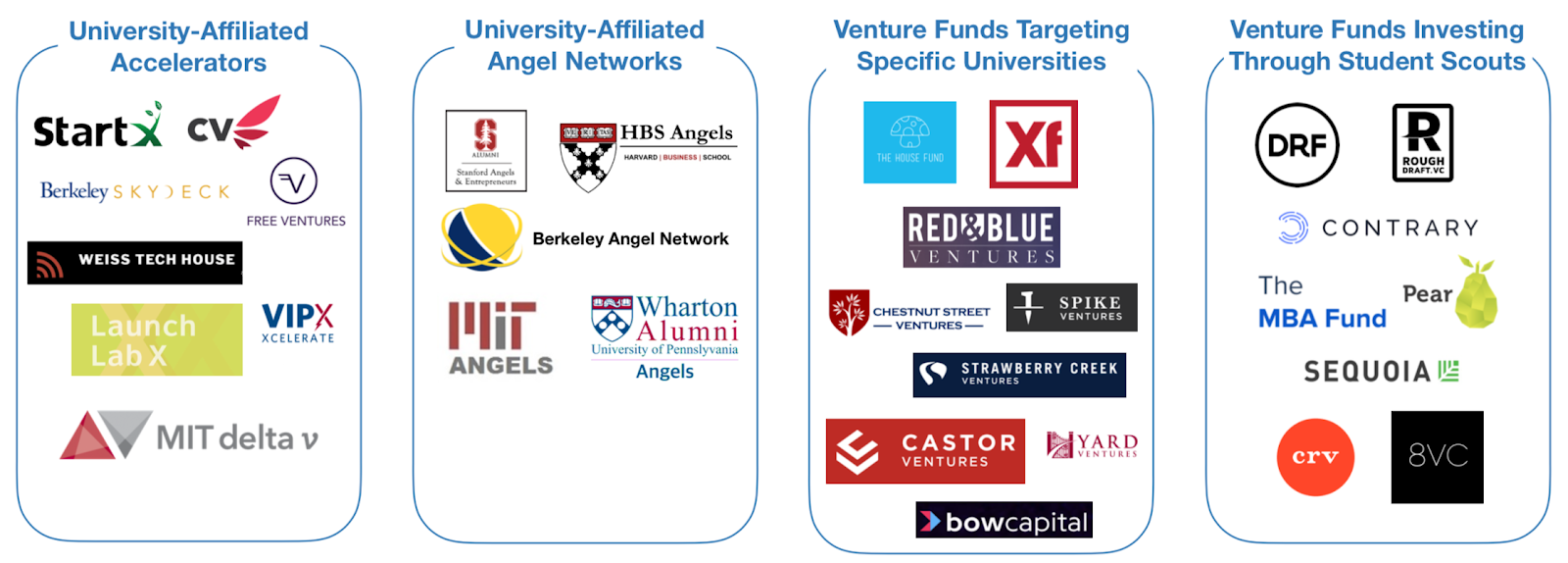

New pools of capital are also available that are specifically for student founders. There are four categories that I call special attention to:

While it is difficult to estimate exactly how much capital has been deployed by each, there is no denying that there has been an explosion in the number of programs that address the pre-seed phase. A sample of the programs available at the Top 5 universities listed above are in the graphic below — listing every resource at every university would be difficult as there are so many.

One alumni-centric fund to highlight is the Alumni Ventures Group, which pools LP capital from alumni at specific universities, then launches individual venture funds that invest in founders connected to those universities (e.g. students, alumni, professors, etc.). Through this model, they’ve deployed more than $200M per year! Another highlight has been student scout programs — which vary in the degree of autonomy and capital invested — but essentially empower students to identify and fund high-potential student-founded companies for their parent venture funds. On campuses with a large concentration of student founders, it is not uncommon to find student scouts from as many as 12 different venture funds actively sourcing deals (as is made clear from David Tao’s analysis at UC Berkeley).

Investment Team at Rough Draft Ventures

In my opinion, the two institutions that have the most expansive line of sight into the student entrepreneurship landscape are First Round’s Dorm Room Fund and General Catalyst’s Rough Draft Ventures. Since 2012, these two funds have operated a nationwide network of student scouts that have invested $20K — $25K checks into companies founded by student entrepreneurs at 40+ universities. “Scout” is a loose term and doesn’t do it justice — the student investors at these two funds are almost entirely autonomous, have built their own platform services to support portfolio companies, and have launched programs to incubate companies built by female founders and founders of color. Another student-run fund worth noting that has reach beyond a single region is Contrary Capital, which raised $2.2M last year. They do a particularly great job of reaching founders at a diverse set of schools — their network of student scouts are active at 45 universities and have spoken with 3,000 founders per year since getting started. Contrary is also testing out what they describe as a “YC for university-based founders”. In their first cohort, 100% of their companies raised a pre-seed round after Contrary’s demo day. Another even more recently launched organization is The MBA Fund, which caters to founders from the business schools at Harvard, Wharton, and Stanford. While super exciting, these two funds only launched very recently and manage portfolios that are not large enough for analysis just yet.

Over the last few months, I’ve collected and cross-referenced publicly available data from both Dorm Room Fund and Rough Draft Ventures to assess the state of student entrepreneurship in the United States. Companies were pulled from each fund’s portfolio page, then checked against Crunchbase for amount raised, accelerator participation, and other metrics. If you’d like to sift through the data yourself, feel free to ping me — my email can be found at the end of this article. To be clear, this does not represent the full scope of investment activity at either fund — many companies in the portfolios of both funds remain confidential and unlisted for good reasons (e.g. startups working in stealth). In fact, the In addition, data for early stage companies is notoriously variable in quality, even with Crunchbase. You should read these insights as directional only, given the debatable confidence interval. Still, the data is still interesting and give good indicators for the health of student entrepreneurship today.

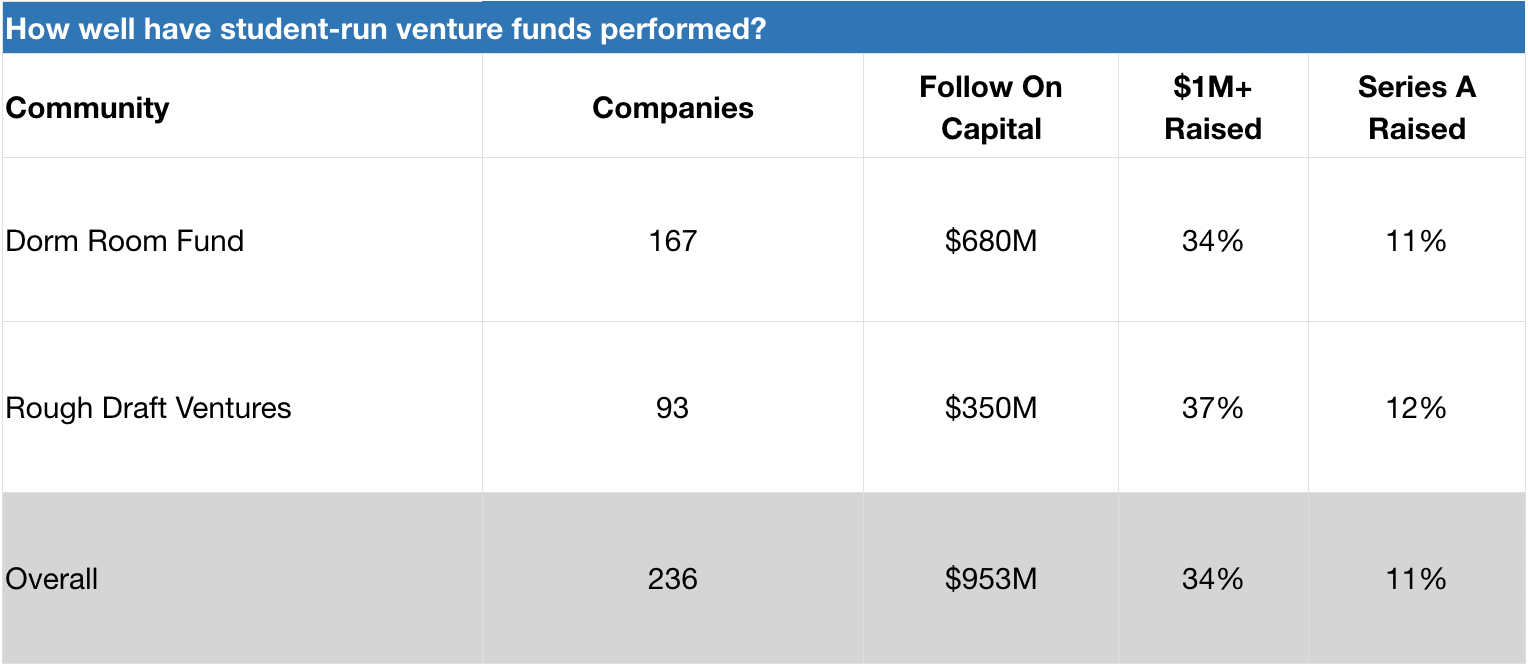

Dorm Room Fund and Rough Draft Ventures have invested in 230+ student-founded companies that have gone on to raise nearly $1 billion in follow on capital. These funds have invested in a diverse range of companies, from govtech (e.g. mark43, raised $77M+ and FiscalNote, raised $50M+) to space tech (e.g. Capella Space, raised ~$34M). Several portfolio companies have had successful exits, such as crypto startup Distributed Systems (acquired by Coinbase) and social networking startup tbh (acquired by Facebook). While it is too early to evaluate the success of these funds on a returns basis (both were launched just 6 years ago), we can get a sense of success by evaluating the rates by which portfolio companies raise additional capital. Taken together, 34% of DRF and RDV companies in our data set have raised $1 million or more in seed capital. For a rough comparison, CB Insights cites that 40% of YC companies and 48% of Techstars companies successfully raise follow on capital (defined as anything above $750K). Certainly within the ballpark!

Dorm Room Fund and Rough Draft Ventures companies in our data set have an 11–12% rate of survivorship to Series A. As a benchmark, a previous partner at Y Combinator shared that 20% of their accelerator companies raise Series A capital (YC declined to share the official figure, but it’s likely a stat that is increasing given their new Series A support programs. For further reading, check out YC’s reflection on what they’ve learned about helping their companies raise Series A funding). In any case, DRF and RDV’s numbers should be taken with a grain of salt, as the average age of their portfolio companies is very low and raising Series A rounds generally takes time. Ultimately, it is clear that DRF and RDV are active in the earlier (and riskier) phases of the startup journey.

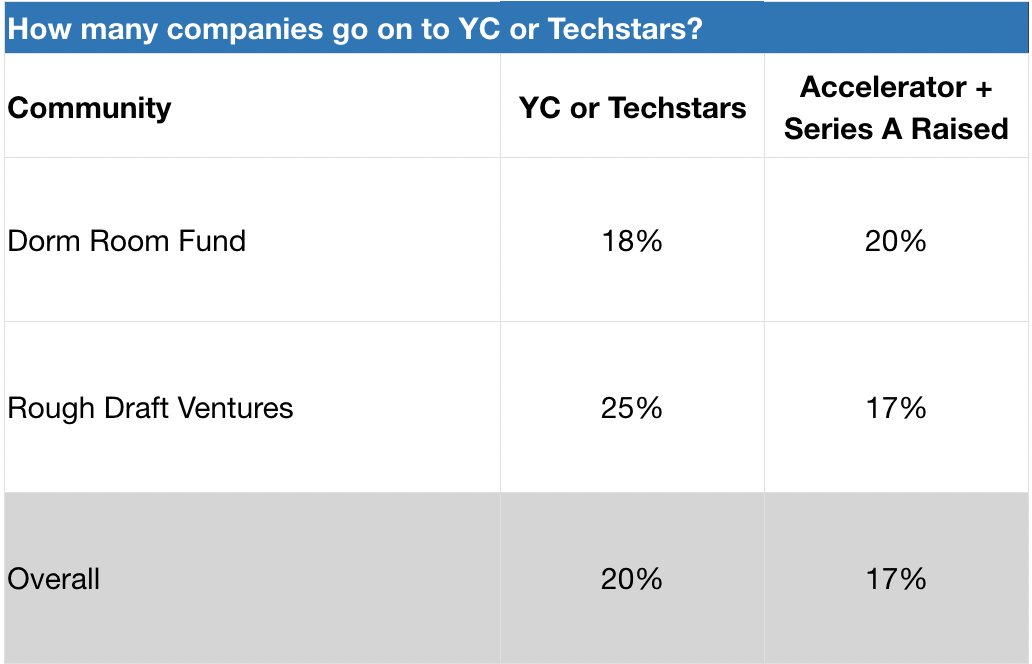

Dorm Room Fund and Rough Draft Ventures send 18–25% of their portfolio companies to Y Combinator or Techstars. Given YC’s 1.5% acceptance rate as reported in Fortune, this is quite significant! Internally, these two funds offer founders an opportunity to participate in mock interviews with YC and Techstars alumni, as well as tap into their communities for peer support (e.g. advice on pitch decks and application content). As a result, Dorm Room Fund and Rough Draft Ventures regularly send cohorts of founders to these prestigious accelerator programs. Based on our data set, 17–20% of DRF and RDV companies that attend one of these accelerators end up raising Series A venture financing.

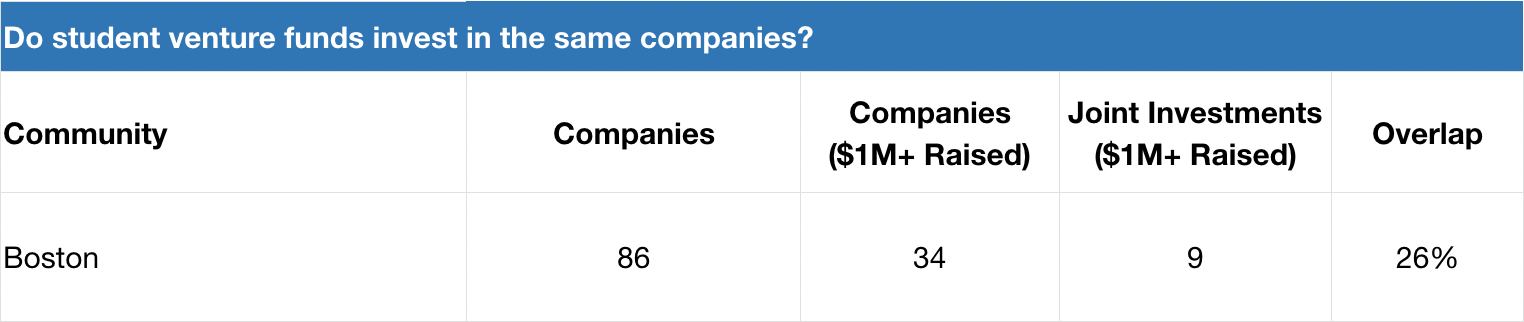

Dorm Room Fund and Rough Draft Ventures don’t invest in the same companies. When we take a deeper look at one specific ecosystem where these two funds have been equally active over the last several years — Boston — we actually see that the degree of investment overlap for companies that have raised $1M+ seed rounds sits at 26%. This suggests that these funds are either a) seeing different dealflow or b) have widely different investment decision-making.

Dorm Room Fund and Rough Draft Ventures should not just be measured by a returns-basis today, as it’s too early. I hypothesize that DRF and RDV are actually encouraging more entrepreneurial activity in the ecosystem (more students decide to start companies while in school) as well as improving long-term founder outcomes amongst students they touch (portfolio founders build bigger and more successful companies later in their careers). As more students start companies, there’s likely a positive feedback loop where there’s increasing peer pressure to start a company or lean on friends for founder support (e.g. feedback, advice, etc).Both of these subjects warrant additional study, but it’s likely too early to conduct these analyses today.

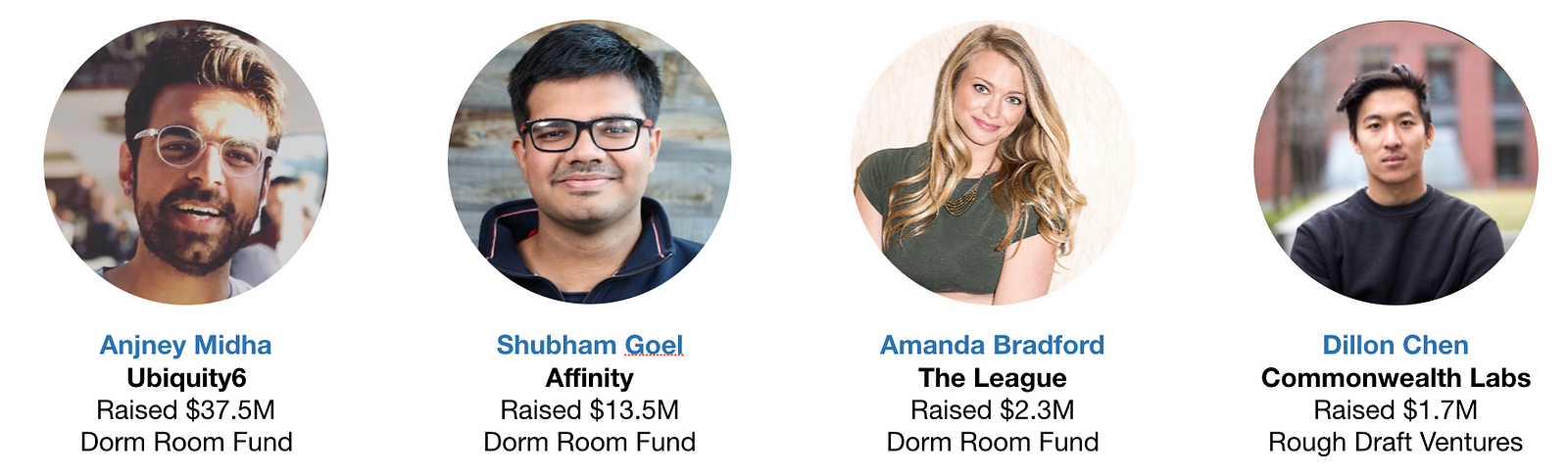

Dorm Room Fund and Rough Draft Ventures have impressive alumni that you will want to track. 1 in 4 alumni partners are founders, and 29% of these founder alumni have raised $1M+ seed rounds for their companies. These include Anjney Midha’s augmented reality startup Ubiquity6 (raised $37M+), Shubham Goel’s investor-focused CRM startup Affinity (raised $13M+), Bruno Faviero’s AI security software startup Synapse (raised $6M+), Amanda Bradford’s dating app The League (raised $2M+), and Dillon Chen’s blockchain startup Commonwealth Labs (raised $1.7M). It makes sense to me that alumni from these communities that decide to start companies have an advantage over their peers — they know what good companies look like and they can tap into powerful networks of young talent / experienced investors.

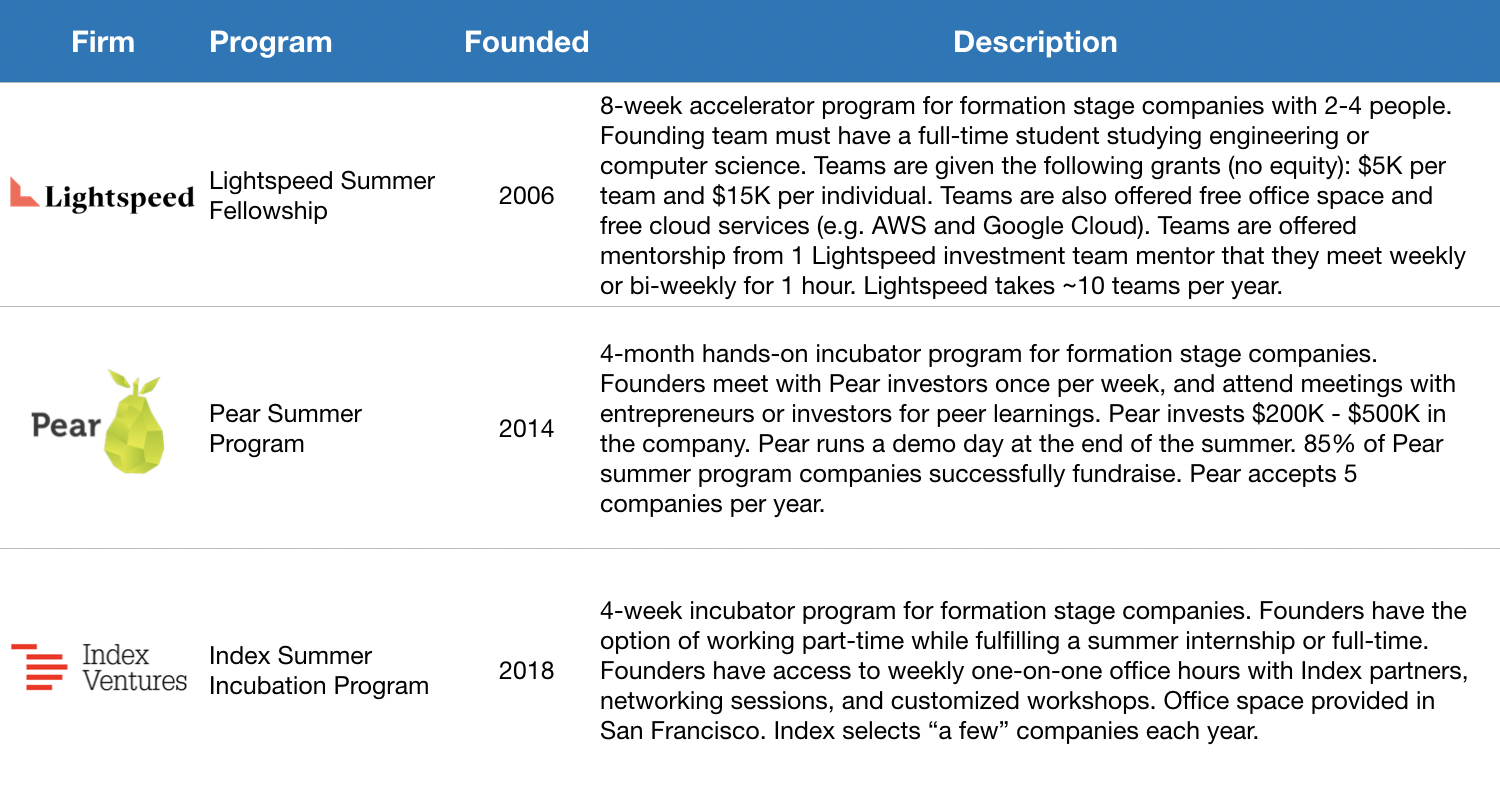

Beyond Dorm Room Fund and Rough Draft Ventures, some venture capital firms focus on incubation for student-founded startups. Credit should first be given to Lightspeed for producing the amazing Summer Fellows bootcamp experience for promising student founders — after all, Pinterest was built there! Jeremy Liew gives a good overview of the program through his sit-down interview with Afterbox’s Zack Banack. Based on a study they conducted last year, 40% of Lightspeed Summer Fellows alumni are currently active founders. Pear Ventures also has an impressive summer incubator program where 85% of its companies successfully complete a fundraise. Index Ventures is the latest to build an incubator program for student founders, and even accepts founders who want to work on an idea part-time while completing a summer internship.

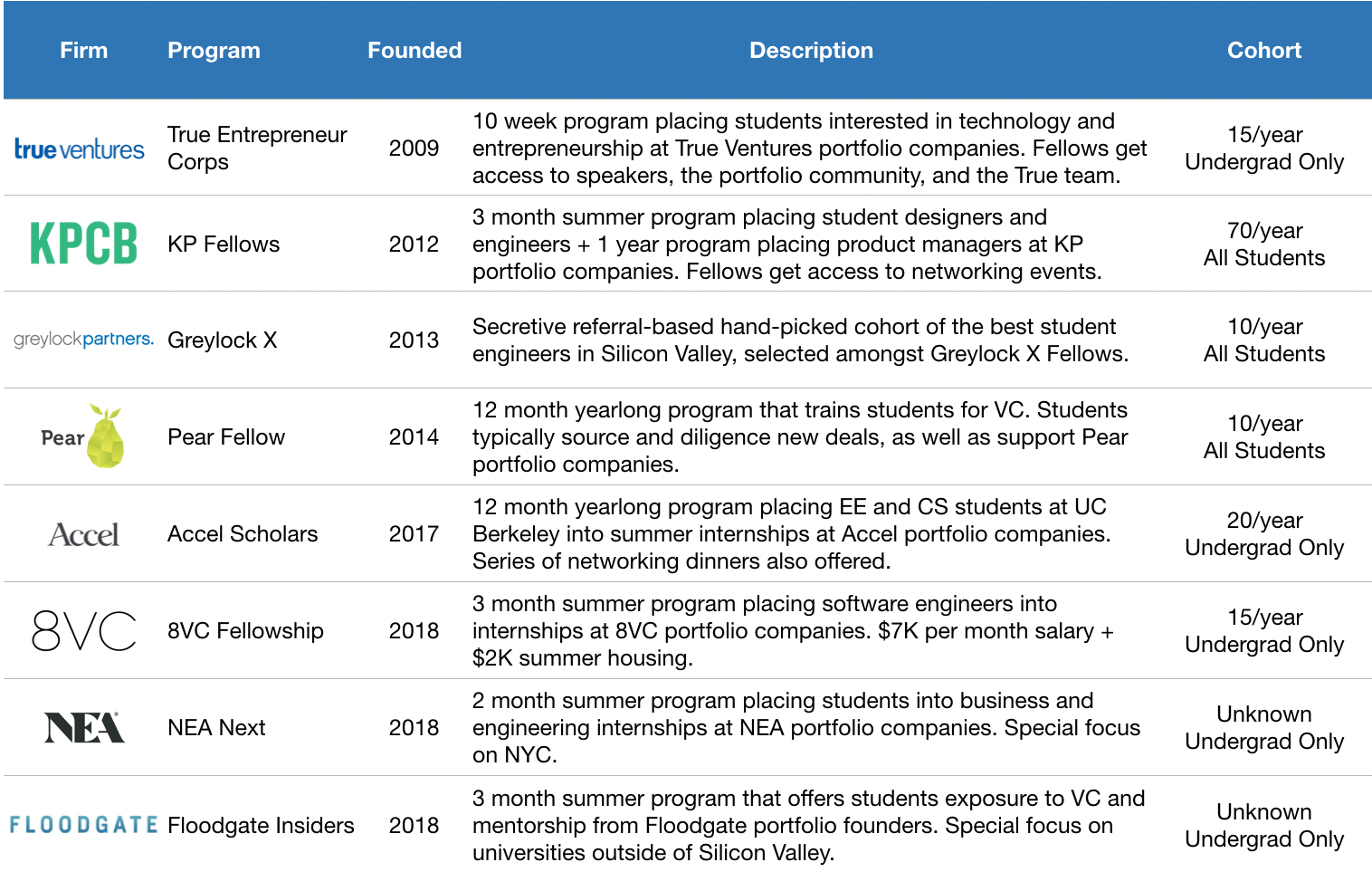

Let’s now look at students who want to join a startup before founding one. Venture funds have historically looked to tap students for talent, and are expanding the engagement lifecycle. The longest running programs include Kleiner Perkins’ class=”m_1196721721246259147gmail-markup–strong m_1196721721246259147gmail-markup–p-strong”> KP Fellows and True Ventures’ TEC Fellows, which focus on placing the next generation’s most promising product managers, engineers, and designers into the portfolio companies of their parent venture funds.

There’s also the secretive Greylock X, a referral-based hand-picked group of the best student engineers in Silicon Valley (among their impressive alumni are founders like Yasyf Mohamedali and Joe Kahn, the folks behind First Round-backed Karuna Health). As these programs have matured, these firms have recognized the long-run value of engaging the alumni of their programs.

More and more alumni are “coming back” to the parent funds as entrepreneurs, like KP Fellow Dylan Field of Figma (and is also hosting a KP Fellow, closing a full circle loop!). Based on their latest data, 10% of KP Fellows alumni are founders — that’s a lot given the fact that their community has grown to 500! This helps explain why Kleiner Perkins has created a structured path to receive $100K in seed funding to companies founded by KP Fellow alumni. It looks like venture funds are beginning to invest in student programs as part of their larger platform strategy, which can have a real impact over the long term (for further reading, see this analysis of platform strategy outcomes by USV’s Bethany Crystal).

KP Fellows in San Francisco

Venture funds are doubling down on student talent engagement — in just the last 18 months, 4 funds have launched student programs. It’s encouraging to see new funds follow in the footsteps of First Round, General Catalyst, Kleiner Perkins, Greylock, and Lightspeed. In 2017, Accel launched their Accel Scholars program to engage top talent at UC Berkeley and Stanford. In 2018, we saw 8VC Fellows, NEA Next, and Floodgate Insiders all launch, targeting elite universities outside of Silicon Valley. Y Combinator implemented Early Decision, which allows student founders to apply one batch early to help with academic scheduling. Most recently, at the start of 2019, First Round launched the Graduate Fund (staffed by Dorm Room Fund alumni) to invest in founders who are recent graduates or young alumni.

Given more time, I’d love to study the rates by which student founders start another company following investments from student scout funds, as well as whether or not they’re more successful in those ventures. In any case, this is an escalation in the number of venture funds that have started to get serious about engaging students — both for talent and dealflow.

Student entrepreneurship 2.0 is here. There are more structured paths to success for students interested in starting or joining a startup. Founders have more opportunities to garner press, seek advice, raise capital, and more. Venture funds are increasingly leveraging students to help improve the three F’s — finding, funding, and fixing. In my personal view, I believe it is becoming more and more important for venture funds to gain mindshare amongst the next generation of founders and operators early, while still in school.

I can’t wait to see what’s next for student entrepreneurship in 2019. If you’re interested in digging in deeper (I’m human — I’m sure I haven’t covered everything related to student entrepreneurship here) or learning more about how you can start or join a startup while still in school, shoot me a note at sxu@dormroomfund.com. A massive thanks to Phin Barnes, Rei Wang, Chauncey Hamilton, Peter Boyce, Natalie Bartlett, Denali Tietjen, Eric Tarczynski, Will Robbins, Jasmine Kriston, Alicia Lau, Johnny Hammond, Bruno Faviero, Athena Kan, Shohini Gupta, Alex Immerman, Albert Dong, Phillip Hua-Bon-Hoa, and Trevor Sookraj for your incredible encouragement, support, and insight during the writing of this essay.

Powered by WPeMatico

Carbon Engineering, a Canadian company developing technology to remove carbon dioxide from the atmosphere and process it for use in enhanced oil recovery or in the creation of new synthetic fuels, has locked in financing from two big industry backers — Chevron and Occidental Petroleum — to bring its products to market.

The undisclosed amount of capital Carbon Engineering raised from the investment arms of two of the world’s largest oil and gas companies — Oxy Low Carbon Ventures and Chevron Technology Ventures — will be used to commercialize its technology at a time when legislation in California and British Columbia are making low-carbon fuels more economically viable, according to a statement from the company’s chief executive, Steve Oldham. The company had already managed to nab Microsoft co-founder Bill Gates as an investor.

Gates is one of several big-name backers to be drawn to renewable energy technologies in the face of a steadily warming planet that’s rapidly approaching a tipping point of no return when it comes to global climate change. Together with a group of other multi-billionaires, including Marc Benioff, Jeff Bezos, Michael Bloomberg, Richard Branson, Jack Ma, Masayoshi Son and Meg Whitman, Gates launched a $1 billion fund called Breakthrough Energy Ventures last year to back companies that are developing things like new energy storage and water production technologies.

The Squamish, B.C.-based Carbon Engineering isn’t in the Breakthrough portfolio, but is one of several companies working on making economically viable a technology called “direct air capture” of carbon dioxide.

At the company’s pilot plant in Squamish, air gets hoovered up by giant fans into a processing facility where it is treated with potassium hydroxide, which captures and holds the carbon dioxide. Then more chemicals and heat are added to the mix to create millions of small white pellets — which contain higher concentrations of the carbon dioxide.

After that, the pellets are heated again to create a gas that is almost pure carbon dioxide. That gas can be either sequestered underground (a proposition with no economic benefit for Carbon Engineering at the moment) or converted back into fuels or chemicals, or used in enhanced oil recovery.

Carbon Engineering and competitors like ClimeWorks or Global Thermostat claim they can remove carbon dioxide from the atmosphere for roughly $100 per ton, or a bit less once they can get to scale. To make money though, they’ll need to refine that carbon dioxide into some sort of product — likely a fuel, which will return that carbon to the atmosphere.

Other companies tackling carbon capture, like Newlight Technologies and Opus12, convert the carbon into plastics or chemicals, while companies like CarbonCure aim to turn the captured carbon into a cement replacement.

While these products from carbon emissions are available, they’re not yet commercially viable at a significant scale. Oldham told National Public Radio that the fuel Carbon Engineering manufactures is roughly 20 percent more expensive than regular gasoline.

That’s why states like California are putting incentives in place to offset the added costs of using these low-carbon products.

Carbon Engineering has already spent $30 million to develop its process, while Climeworks raised $31 million last year to develop its own version of this carbon capture technology.

Not all climate watchers are convinced that these kinds of negative emission technologies are the answer. They argue that it’s less expensive to use renewable energy and other carbon-free energy sources than to take carbon dioxide out of the air.

At this point, though, emission reductions may not be enough. Given the dire reports coming out of the Trump administration and the Intergovernmental Panel on Climate Change, it’s going to take pretty much a combination of everything that humanity’s got to avoid a pretty catastrophic fate for a pretty large portion of the world’s population.

Even the companies that have been notorious for their contributions to the climate crisis that the world faces are waking up to the need for decarbonization (even if it’s an open question of whether they’re being dragged to the table or sitting down of their own free will).

Oxy Low Carbon Ventures is a good example. Reading the writing on the wall, the firm has invested not just in Carbon Engineering, but another company called NET Power, which purports to have developed a power plant with zero emissions.

“It is a very important time for the air capture field right now,” said Oldham in a statement. “We’re seeing leading jurisdictions, like California and British Columbia, creating markets for low carbon fuels and technologies like DAC, through effective climate policy. These efficient market-based regulations, and action from energy industry leaders like Occidental and Chevron, show the power of policy in driving innovation and achieving emissions reductions while delivering reliable and affordable energy.”

Powered by WPeMatico

Malta, the renewable energy storage project born in Alphabet’s moonshot factory X, is now on its own and flush with $26 million from a Series A funding round led by Breakthrough Energy Ventures .

Concord New Energy Group and Alfa Laval also invested in the round.

Project Malta launched last year in Alphabet’s X (formerly Google X) with an aim to build energy storage facilities that can support full-scale power grids. The independent company spun out of Alphabet is now called Malta Inc.

Malta Inc. has developed a system designed to keep power generated from renewable energy or fossil fuels in reserve for longer than lithium-ion batteries. The electro-thermal storage system first captures energy generated from wind, solar or fossil generators on the grid. The collected electricity drives a heat pump, which converts the electrical energy into thermal energy. The heat is stored in molten salt, while the cold is stored in a chilled antifreeze liquid. A heat engine is used to convert the energy back to electricity for the grid when it’s needed.

The system can store electricity for days or even weeks, Malta says.

Malta is going to use the funds to work with industry partners to turn the detailed designs developed and refined at X into industrial-grade machinery for its first pilot system.

BEV, the lead investor in Malta’s Series A round, was created in 2016 by the Breakthrough Energy Coalition, an investor group that includes Microsoft co-founder Bill Gates, John Doerr, chairman of venture firm Kleiner Perkins Caufield & Byers, Alibaba founder Jack Ma, Amazon founder and CEO Jeff Bezos, and SAP co-founder Hasso Plattner.

Powered by WPeMatico

In tech circles, it would be easy to assume that the world of high-impact charitable giving is a rich man’s game where deals are inked at exclusive black tie galas over fancy hors d’oeuvre. Both Mark Zuckerberg and Marc Benioff have donated to SF hospitals that now bear their names. Gordon Moore has given away $5B – including $600M to Caltech – which was the largest donation to a university at the time. And of course, Bill Gates has already donated $27B to every cause imaginable (and co-founded The Giving Pledge, a consortium of billionaires pledging to donate most of their net worth to charity by the end of their lifetime.)

For Bill, that means he has about $90B left to give.

For the average working American, this world of concierge giving is out of reach, both in check size, and the army of consultants, lawyers and PR strategists that come with it. It seems that in order to do good, you must first do well. Very well.

Bright Funds is looking to change that. Founded in 2012, this SF-based startup is looking to democratize concierge giving to every individual so they “can give with the same effectiveness as Bill and Melinda Gates.” They are doing to philanthropy what Vanguard and Wealthfront have done for asset management for retail investors.

In particular, they are looking to unlock dollars from the underutilized corporate benefit of matching funds for donations, which according to Bright Funds is offered by over 60% of medium to large enterprises, but only used by 13% of employees at these companies. The need for such a service is clear — these programs are cumbersome, transactional, and often offline. Make a donation, submit a receipt, and wait for it to churn through the bureaucratic machine of accounting and finance before matching funds show up weeks later.

Bright Funds is looking to make your company’s matching funds benefit as accessible and important to you as your free lunches or massages. Plus, Bright Funds charges companies per seat, along with a transaction fee to cover the cost of payment processing, sparing employees any expense.

It’s a model that is working. According to Bright Fund’s CEO Ty Walrod, Bright Funds customers see on average a 40% year-over-year increase in funds donated through the platform. More importantly, Bright Funds not only transforms an employee’s relationship to personal philanthropy, but also to the company they work for.

This model of bottoms-up giving is a welcome change from the big foundation model which has recently been rocked by scandal. The Silicon Valley Community Foundation was the go-to foundation for The Who’s Who of Silicon Valley elite. It rode the latest tech boom to become the largest community foundation in eleven short years with generous stock donations from donors like Mark Zuckerberg ($1.8 billion), GoPro’s Nicholas Woodman ($500 million), and WhatsApp co-founder Jan Koum ($566 million). Today, at $13.5 billion, it surpasses the 80+ year old Ford Foundation in endowment size.

However, earlier this year, their star fundraiser Mari Ellen Loijens (credited with raising $8.3B of the $13.5B) was accused of repeatedly bullying and sexually harassing coworkers, allegations that the Foundation had “known about for years” but failed to act upon. In 2017, a similar case occurred when USC’s star fundraiser David Carrera stepped down on charges of sexual harassment after leading the university’s historic $6 billion fundraising campaign.

While large foundations and endowments do important work, their structure relies too much on whale hunting for big checks, giving an inordinate amount of power to the hands of a small group of talented fund raisers.

This stands in contrast to Bright Funds’ ethos — to lead a grassroots movement in empowering individual employees to make their dollar of giving count.

Bright Funds is the latest iteration of a lineup of workplace giving platforms. MicroEdge and Cybergrants paved the way in the 80s and 90s by digitizing the giving experience, but was mainly on-premise, and lacked a focus on user experience. Benevity and YourCause arrived in 2007 to bring workplace giving to the cloud, but they were still not turnkey solutions that could be easily implemented.

Bright Funds started as a consumer platform, and has retained that heritage in its approach to product design, aiming to reduce friction for both employee and company adoption. This is why many of their first customers were midsized tech startups with limited resources and looking for a turnkey solution, including Eventbrite, Box, Github, and Contently . They are now finding their way upmarket into larger, more established enterprises like Cisco, VMWare, Campbell’s Soup Company, and Sunpower.

Bright Funds approach to product has brought a number of innovations to this space.

The first is the concept of a cause-focused “fund.” Similar to a mutual fund or ETF, these funds are portfolios of nonprofits curated by subject-matter experts tailored to a specific cause area (e.g. conservation, education, poverty, etc.). This solves one of the chief concerns of any donor — is my dollar being put to good use towards the causes I care about? Passionate about conservation? Invest with Jim Leape from the Stanford Woods Institute for the Environment, who brings over three decades of conservation experience in choosing the six nonprofits in Bright Fund’s conservation portfolio. This same expertise is available across a number of cause areas.

Additionally, funds can also be created by companies or employees. This has proven to be an important rallying point for emergency relief during natural disasters, where employees at companies can collectively assemble a list of nonprofits to donate to. In 2017, Cisco employees donated $1.8 million (including company matching) through Bright Funds to Hurricanes Harvey, Maria, and Irma as well as the central Mexico earthquakes, the current flooding in India and many more.

The second key feature of their product is the impact timeline, a central news feed to understand where your dollars are going across all your cause areas. This transforms giving from a black box transaction to an ongoing dialogue between you and your charities.

Lastly, Bright Funds wants to take away all the administrative burden that might come with giving and volunteering — everything from tracking your volunteer opportunities and hours, to one-click tax reporting across all your charitable donations. In short, no more shoeboxes of receipts to process through in April.

Although Bright Funds is focused on transforming the individual giving experience, it’s paying customer at the end of the day is the enterprise.

And although it is philanthropic in nature, Bright Funds is not exempt from the procurement gauntlet that every enterprise software startup faces — what’s in it for the customer? What impact does workplace giving and volunteering have on culture and the bottom line?

To this end, there is evidence to show that corporate social responsibility has a an impact on recruiting the next generation of workers. A study by Horizon Media found that 81% of millennials expect their companies to be good corporate citizens. A separate 2015 study found that 62% of millennials said they’d take a pay cut to work for a company that’s socially responsible.

Box, one of Bright Fund’s early customers, has seen this impact on recruiting firsthand (disclosure: Box is one of my former employers). Like most tech companies competing for talent in the Valley, Box used to give out lucrative bonuses for candidate referrals. They recently switched to giving out $500 in Bright Funds gift credit. Instead of seeing employee referrals dip, Box saw referrals “skyrocket,” according to Box.org Executive Director Bryan Breckenridge. This program has now become “one of the most cherished cultural traditions at Box,” he said.

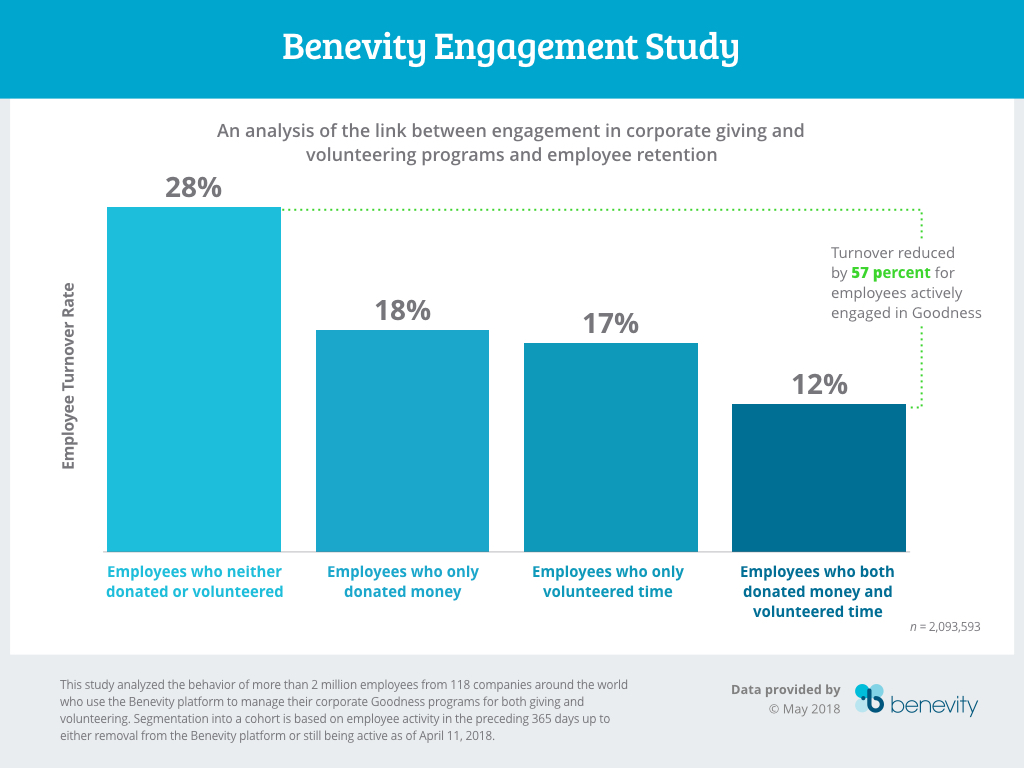

Additionally, like any corporate benefit, there should be metrics tied to employee retention. Benevity released a study of 2 million employees across 118 companies on their platform that showed a 57% reduction in turnover for employees engaged in corporate giving or volunteering efforts. VMware, one of Bright Fund’s customers, has seen an astonishing 82% of their 22,000 employees participate in their Citizen Philanthropy program of giving and volunteering, according to VMware Foundation Director Jessa Chin. Their full-time voluntary turnover rate (8%) is well below the software industry average of 13.2%.

Bright Funds still has a lot of work to do. CEO Walrod says that one of his top priorities is to expand the platform beyond US charities, finding ways to evaluate and incorporate international nonprofits.

They have also not given up their dream of becoming a truly consumer platform, perhaps one day competing in the world of donor-advised funds, which today is largely dominated by big names like Fidelity and Schwab who house over $85B of assets. In the short term, Walrod wants to make every Bright Funds account similar to a 401K account. It goes wherever you work, and is a lasting record of the causes you care about, and the time and resources you’ve invested in them.

Whether the impetus is altruism around giving or something more utilitarian like retention, companies are increasingly realizing that their employees represent a charitable force that can be harnessed for the greater good. Bright Funds has more work to do like any startup, but it is empowering the next set of donors who can give with the same effectiveness as Gates, and one day, at the same scale as him as well.

Powered by WPeMatico

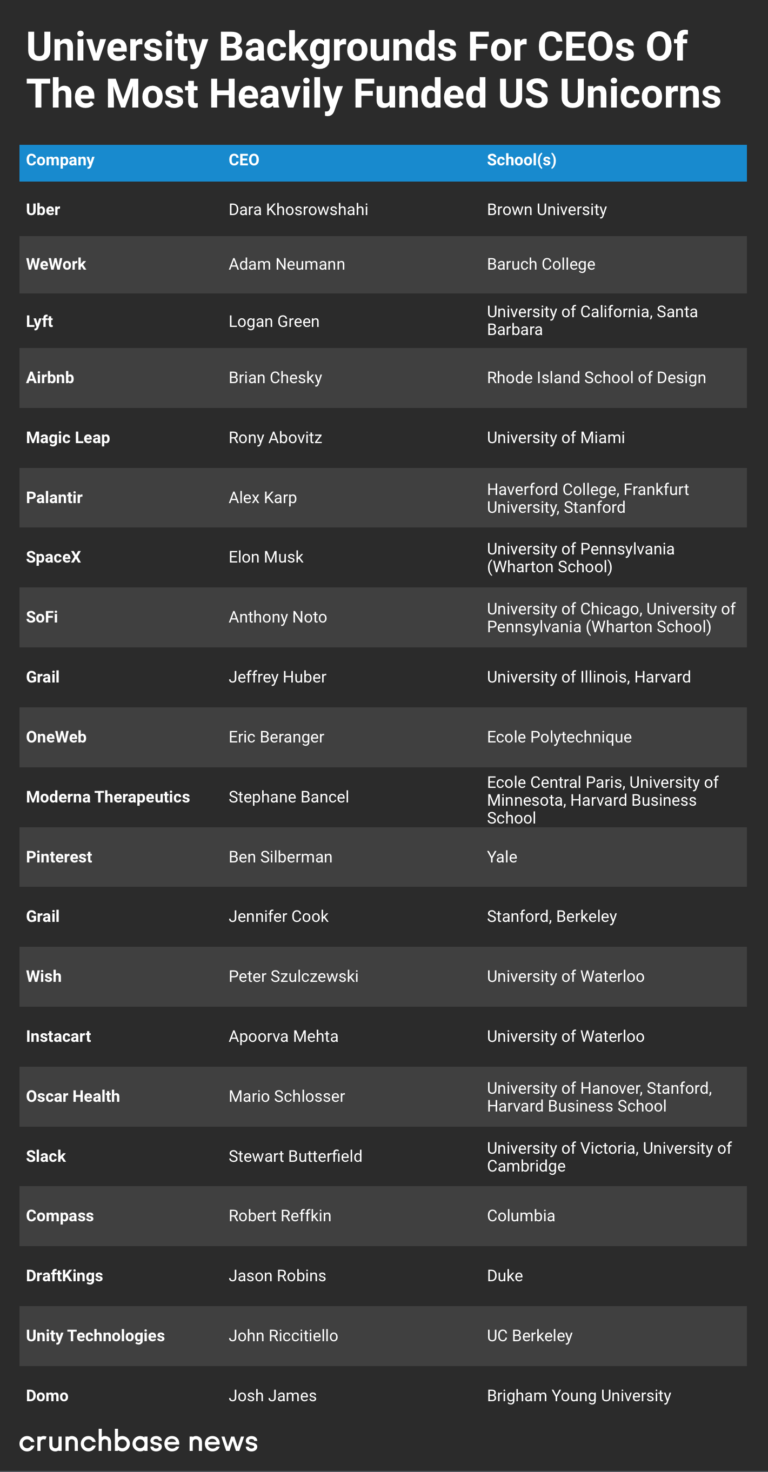

CEOs of funded startups tend to be a well-educated bunch, at least when it comes to university degrees.

Yes, it’s true college dropouts like Mark Zuckerberg and Bill Gates can still do well. But Crunchbase data shows that most startup chief executives have an advanced degree, commonly from a well-known and prestigious university.

Earlier this month, Crunchbase News looked at U.S. universities with strong track records for graduating future CEOs of funded companies. This unearthed some findings that, while interesting, were not especially surprising. Stanford and Harvard topped the list, and graduates of top-ranked business schools were particularly well-represented.

In this next installment of our CEO series, we narrowed the data set. Specifically, we looked at CEOs of U.S. companies funded in the past three years that have raised at least $100 million in total venture financing. Our intent was to see whether educational backgrounds of unicorn and near-unicorn leaders differ markedly from the broad startup CEO population.

Here’s the broad takeaway of our analysis: Most CEOs of well-funded startups do have degrees from prestigious universities, and there are a lot of Harvard and Stanford grads. However, chief executives of the companies in our current data set are, educationally speaking, a pretty diverse bunch with degrees from multiple continents and all regions of the U.S.

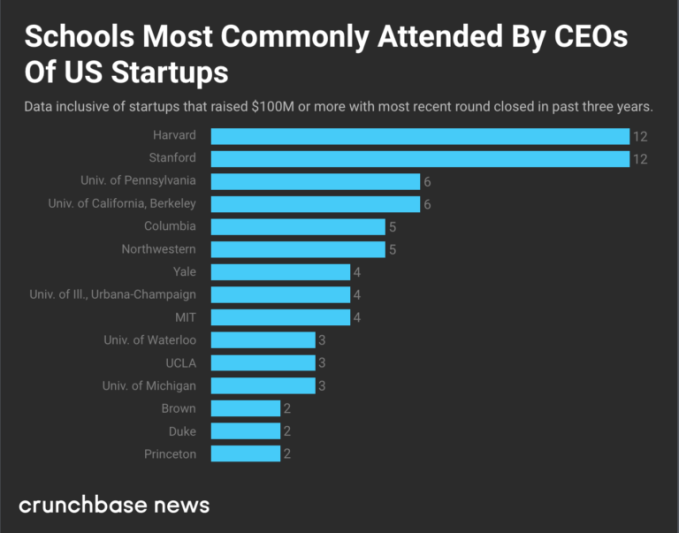

In total, our data set includes 193 private U.S. companies that raised $100 million or more and closed a VC round in the past three years. In the chart below, we look at the universities most commonly attended by their CEOs:1

The rankings aren’t hugely different from the broader population of funded U.S. startups. In that data set, we also found Harvard and Stanford vying for the top slots, followed mostly by Ivy League schools and major research universities.

For heavily funded startups, we also found a high proportion of business school degrees. All of the University of Pennsylvania alum on the list attended its Wharton School of Business. More than half of Harvard-affiliated grads attended its business school. MBAs were a popular credential among other schools on the list that offer the degree.

When it comes to the most heavily funded startups, the degree mix gets quirkier. That makes sense, given that we looked at just 20 companies.

In the chart below, we look at alumni affiliations for CEOs of these companies, all of which have raised hundreds of millions or billions in venture and growth financing:

One surprise finding from the U.S. startup data set was the prevalence of Canadian university grads. Three CEOs on the list are alums of the University of Waterloo . Others attended multiple well-known universities. The list also offers fresh proof that it’s not necessary to graduate from college to raise billions. WeWork CEO Adam Neumann just finished his degree last year, 15 years after he started. That didn’t stop the co-working giant from securing more than $7 billion in venture and growth financing.

Powered by WPeMatico

Product Hunt’s first employee Erik Torenberg is ready to fund fresh new startups, not just reveal them to the world. Today is the soft launch of Village Global, a seed and pre-seed early stage venture capital fund looking to connect entrepreneurs to cash as well as all-star mentors. Facebook’s Mark Zuckerberg, Amazon’s Jeff Bezos, LinkedIn’s Reid Hoffman,… Read More

Product Hunt’s first employee Erik Torenberg is ready to fund fresh new startups, not just reveal them to the world. Today is the soft launch of Village Global, a seed and pre-seed early stage venture capital fund looking to connect entrepreneurs to cash as well as all-star mentors. Facebook’s Mark Zuckerberg, Amazon’s Jeff Bezos, LinkedIn’s Reid Hoffman,… Read More

Powered by WPeMatico

LinkedIn co-founder Reid Hoffman announced today that he’s making a big bet on Change.org, the site for social justice petitions. Hoffman is leading a $30 million round, with other investors including big names like Bill Gates and Y Combinator president Sam Altman.

LinkedIn co-founder Reid Hoffman announced today that he’s making a big bet on Change.org, the site for social justice petitions. Hoffman is leading a $30 million round, with other investors including big names like Bill Gates and Y Combinator president Sam Altman.

“Change.org, the global hub for collective action, is a crucial democratizing force in this era of growing civic… Read More

Powered by WPeMatico

Bill Gates, Jeff Bezos, Vinod Khosla, Jack Ma, John Doerr and 15 other high-profile investors have formed a new venture firm, Breakthrough Energy Ventures, that will pour at least $1 billion into cleantech companies over the next 20 years. The firm’s goal, according to its own website, will be: “to provide everyone in the world with access to reliable, affordable power, food,… Read More

Bill Gates, Jeff Bezos, Vinod Khosla, Jack Ma, John Doerr and 15 other high-profile investors have formed a new venture firm, Breakthrough Energy Ventures, that will pour at least $1 billion into cleantech companies over the next 20 years. The firm’s goal, according to its own website, will be: “to provide everyone in the world with access to reliable, affordable power, food,… Read More

Powered by WPeMatico

With icons like Leonardo DiCaprio and Bill Gates using their powerful brands and personal convictions to turn the world’s focus toward the crisis of climate change and the long-lever arm of energy efficiency, it’s time for policy makers and practitioners to get serious about finding ways to take better care of our planet. Read More

With icons like Leonardo DiCaprio and Bill Gates using their powerful brands and personal convictions to turn the world’s focus toward the crisis of climate change and the long-lever arm of energy efficiency, it’s time for policy makers and practitioners to get serious about finding ways to take better care of our planet. Read More

Powered by WPeMatico