bigcommerce

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Despite some recent market volatility, the valuations that software companies have generally been able to command in recent quarters have been impressive. On Friday, we took a look into why that was the case, and where the valuations could be a bit more bubbly than others. Per a report written by few Battery Ventures investors, it stands to reason that the middle of the SaaS market could be where valuation inflation is at its peak.

Something to keep in mind if your startup’s growth rate is ticking lower. But today, instead of being an enormous bummer and making you worry, I have come with some historically notable data to show you how good modern software startups and their larger brethren have it today.

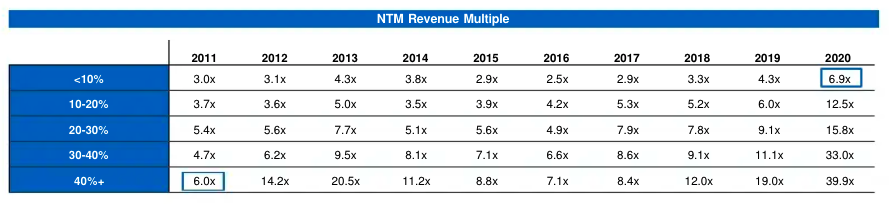

In case you are not 100% infatuated with tables, let me save you some time. In the upper right we can see that SaaS companies today that are growing at less than 10% yearly are trading for an average of 6.9x their next 12 months’ revenue.

Back in 2011, SaaS companies that were growing at 40% or more were trading at 6.0x their next 12 month’s revenue. Climate change, but for software valuations.

One more note from my chat with Battery. Its investor Brandon Gleklen riffed with The Exchange on the definition of ARR and its nuances in the modern market. As more SaaS companies swap traditional software-as-a-service pricing for its consumption-based equivalent, he declined to quibble on definitions of ARR, instead arguing that all that matters in software revenues is whether they are being retained and growing over the long term. This brings us to our next topic.

I’ve taken a number of earnings calls in the last few weeks with public software companies. One theme that’s come up time and again has been consumption pricing versus more traditional SaaS pricing. There is some data showing that consumption-priced software companies are trading at higher multiples than traditionally priced software companies, thanks to better-than-average retention numbers.

But there is more to the story than just that. Chatting with Fastly CEO Joshua Bixby after his company’s earnings report, we picked up an interesting and important market distinction between where consumption may be more attractive and where it may not be. Per Bixby, Fastly is seeing larger customers prefer consumption-based pricing because they can afford variability and prefer to have their bills tied more closely to revenue. Smaller customers, however, Bixby said, prefer SaaS billing because it has rock-solid predictability.

I brought the argument to Open View Partners Kyle Poyar, a venture denizen who has been writing on this topic for TechCrunch in recent weeks. He noted that in some cases the opposite can be true, that variably priced offerings can appeal to smaller companies because their developers can often test the product without making a large commitment.

So, perhaps we’re seeing the software market favoring SaaS pricing among smaller customers when they are certain of their need, and choosing consumption pricing when they want to experiment first. And larger companies, when their spend is tied to equivalent revenue changes, bias toward consumption pricing as well.

Evolution in SaaS pricing will be slow, and never complete. But folks really are thinking about it. Appian CEO Matt Calkins has a general pricing thesis that price should “hover” under value delivered. Asked about the consumption-versus-SaaS topic, he was a bit coy, but did note that he was not “entirely happy” with how pricing is executed today. He wants pricing that is a “better proxy for customer value,” though he declined to share much more.

If you aren’t thinking about this conversation and you run a startup, what’s up with that? More to come on this topic, including notes from an interview with the CEO of BigCommerce, who is betting on SaaS over the more consumption-driven Shopify.

Next Insurance bought another company this week. This time it was AP Intego, which will bring integration into various payroll providers for the digital-first SMB insurance provider. Next Insurance should be familiar because TechCrunch has written about its growth a few times. The company doubled its premium run rate to $200 million in 2020, for example.

The AP Intego deal brings $185.1 million of active premium to Next Insurance, which means that the neo-insurance provider has grown sharply thus far in 2021, even without counting its organic expansion. But while the Next Insurance deal and the impending Hippo SPAC are neat notes from a hot private sector, insurtech has shed some of its public-market heat.

Stocks of public neo-insurance companies like Root, Lemonade and MetroMile have lost quite a lot of value in recent weeks. So, the exit landscape for companies like Next and Hippo — yet-private insurtech startups with lots of capital backing their rapid premium growth — is changing for the worse.

Hippo decided it will debut via a SPAC. But I doubt that Next Insurance will pursue a rapid ramp to the public markets until things smooth out. Not that it needs to go public quickly; it raised a quarter billion back in September of last year.

What else? Sisense, a $100 million ARR club member, hired a new CFO. So we expect them to go public inside the next four or five quarters.

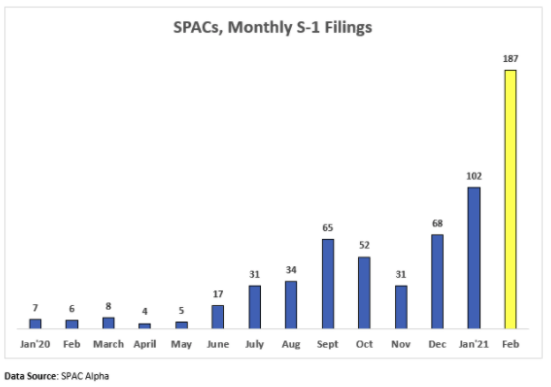

And the following chart, which is via Deena Shakir of Lux Capital, via Nasdaq, via SPAC Alpha:

Powered by WPeMatico

BigCommerce has partnered with Walmart to allow its customers to sell on the Bentonville, Arkansas-based retailer’s e-commerce marketplace, it announced this morning. Shares of Austin-based BigCommerce rose sharply in pre-market trading after the news, gaining around 10% before the bell.

Walmart, best-known for in-person shopping, has proven an e-commerce success story in recent years. For example, in its most recent quarter while Walmart as a whole grew 7.3%, its e-commerce sales advanced 69%.

BigCommerce has also reported strong growth in recent quarters, supported in part by partnerships similar to the one that it announced today. The e-commerce SaaS provider rolled out an integration with Wish last year, for example.

In a call concerning its earnings, which were announced before the Walmart news was announced, BigCommerce CEO Brent Bellm told TechCrunch that his company had been impressed with customer uptake of the Wish integration. Regarding the Walmart partnership, in a second interview Bellm told TechCrunch that it was overdue on the BigCommerce side; given the historical success of the Wish deal, it will be curious to dig into how many of the e-commerce platform’s customers opt to sell on Walmart, and how quickly they do so.

TechCrunch also spoke with Walmart exec Jeff Clementz about the arrangement. He stressed Walmart’s online customer monthly-actives — 120 million, per his company — and the breadth of their demand; BigCommerce customers selling on Walmart could expand its product diversity, helping the traditionally physical retailer possible continue its rapid growth.

The two companies are incentivizing adoption of the deal amongst BigCommerce customers by waiving certain fees for a month for retailers that sign up to sell on Walmart; Clementz described it as the first time that his company had offered a “new-seller discount.”

TechCrunch has had its eye on BigCommerce for some quarters now, thanks in part to its 2020 IPO. But the company is also interesting as its regular earnings results provide a lens into the world of e-commerce growth amongst independent digital retailers. Shopify, a chief BigCommerce rival, provides a similar view into the e-commerce world.

Shopify previously integrated with Walmart in the middle of 2020.

Looking ahead, it will be interesting to see if the Walmart partnership helps BigCommerce continue its improving revenue growth. The company is in a market share race with Shopify. But while BigCommerce’s rival has posted impressive growth from its integrated solutions, like its payments service, the Austin-based company stresses what it calls a more open model. Shopify charges many customers a percentage of their transaction volume for using a third-party payment solution over its own, for example, which Bellm described as a “tax” during an interview.

“Merchant Solutions” revenue at Shopify, which it generates “principally” from “payment processing fees from Shopify Payments,” grew 116% in 2020 to a little over $2 billion.

So with BigCommerce collecting a partnership with Walmart to match Shopify’s own, we’re seeing not merely two e-commerce platforms go toe-to-toe on providing their customers with as much market access as they can, but two different business philosophies compete. Akin to Microsoft Teams and Slack, it’s a competition to spectate.

Powered by WPeMatico

A startup called BlackCart is tackling one of the key challenges with online shopping: an inability to try on or test out the merchandise before making a purchase. That company, which has now closed on $8.8 million in Series A funding, has built a try-before-you-buy platform that integrates with e-commerce storefronts, allowing customers to ship items to their home for free and only pay if they choose to keep the item after a “try on” period has lapsed.

The new round of financing was led by Origin Ventures and Hyde Park Ventures Partners, and saw participation from Struck Capital, Citi Ventures, 500 Startups and several other angel investors, including Christian Sullivan of Republic Labs, Dean Bakes of M3 Ventures, Greg Rudin of Menlo Ventures, Jordan Nathan of Caraway Cookware and First National Bank CFO Nick Pirollo, among others.

The Toronto-based company last year had raised a $2 million seed.

Image Credits: BlackCart

BlackCart founder Donny Ouyang had previously founded online tutoring marketplace Rayku before joining a seed-stage VC fund, Caravan Ventures. But he was inspired to return to entrepreneurship, he says, after experiencing a personal problem with trying to order shoes online.

Realizing the opportunity for a “try before you buy” type of service, Ouyang first built BlackCart in 2017 as a business-to-consumer (B2C) platform that worked by way of a Chrome extension with some 50 different online merchants, largely in apparel.

This MVP of sorts proved there was consumer demand for something like this in online shopping.

Ouyang credits the earlier version of BlackCart with helping the team to understand what sort of products work best for this service.

“I think, in general, for try-before-you-buy, anything that’s moderate to higher price points, lower frequency of purchase, where the customer makes a considered purchase decision — those perform really well,” he says.

Two years later, Ouyang took BlackCart to 500 Startups in San Francisco, where he then pivoted the business to the B2B offering it is today.

Image Credits: BlackCart

The startup now provides a try-before-you-buy platform that integrates with online storefronts, including those from Shopify, Magento, WooCommerce, Big Commerce, SalesForce Commerce Cloud, WordPress and even custom storefronts. The system is designed to be turnkey for online retailers and takes around 48 hours to set up on Shopify and around a week on Magento, for example.

BlackCart has also developed its own proprietary technology around fraud detection, payments, returns and the overall user experience, which includes a button for retailers’ websites.

Because the online shoppers aren’t paying upfront for the merchandise they’re being shipped, BlackCart has to rely on an expanded array of behavioral signals and data in order to make a determination about whether the customer represents a fraud risk. As one example, if the customer had read a lot of helpdesk articles about fraud before placing their order, that could be flagged as a negative signal.

BlackCart also verifies the user’s phone number at checkout and matches it to telco and government data sets to see if their historical addresses match their shipping and billing addresses.

Image Credits: BlackCart

After the customer receives the item, they are able to keep it for a period of time (as designated by the retailer) before being charged. BlackCart covers any fraud as part of its value proposition to retailers.

BlackCart makes money by way of a rev share model, where it charges retailers a percentage of the sales where the customers have kept the products. This amount can vary based on a number of factors, like the fraud multiplier, average order value, the type of product and others. At the low end, it’s around 4% and around 10% on the high end, Ouyang says.

The company has also expanded beyond home try-on to include try-before-you-buy for electronics, jewelry, home goods and more. It can even ship out makeup samples for home try-on, as another option.

Once integrated on a website, BlackCart claims its merchants typically see conversion increases of 24%, average order values climb by 51% and bottom-line sales growth of 27%.

To date, the platform has been adopted by more than 50 medium-to-large retailers, as well as e-commerce startups, like luxury sneaker brand Koio, clothing startup Dia&Co, online mattress startup Helix Sleep and cookware startup Caraway, among others. It’s also under NDA now with a top-50 retailer it can’t yet name publicly, and has contracts signed with 13 others that are waiting to be onboarded.

Soon, BlackCart aims to offer a self-serve onboarding process, Ouyang notes.

“This would be later, end of Q2 or early Q3,” he says. “But I think for us, it will still be probably 80% self-serve, and then larger enterprises will want to be handheld.”

With the additional funding, BlackCart aims to shift to paying the merchant immediately for the items at checkout, then reconciling afterwards in order to be more efficient. This has been one of merchants’ biggest feature requests, as well.

Image Credits: BlackCart; team photo

The funding will also allow BlackCart to expand its remotely distributed 10-person team to around 50 by year-end, including engineers, product specialists, customer support staff and sales.

More broadly, it aims to quickly capitalize on the growth in the e-commerce market, driven by the COVID-19 pandemic.

“[We want to] take advantage of the favorable macroeconomic situation to scale as quickly as possible,” Ouyang explains. “We’re hoping to get to around $250 million in transactions through our platform by the end of 2021. And this would be driven by both engineering and sales hires, and just pushing it up,” he says.

Longer-term, Ouyang envisions adding more consumer-facing features to BlackCart’s platform, like on-demand returns where a courier comes to the house to pick up your return, for example.

“Our firm is excited to partner with BlackCart as it makes try-before-you-buy the standard in online shopping,” said Prashant Shukla of Origin Ventures, who now sits on BlackCart’s board, as result of the new financing. “Its underwriting technology provides merchants with peace of mind, and its best-in-class consumer experience delivers significant sales and conversion lifts. Digital Native generations expect to be able to shop online exactly as they would in a retail store, and BlackCart is the only company providing this experience,” he adds.

Powered by WPeMatico

Revolution, the Washington, D.C.-based investment firm founded by AOL cofounder CEO Steve Case and former AOL senior exec Ted Leonsis, is raising $500 million for its fourth fund, shows a new SEC filing.

Asked about the effort earlier today, the firm declined to comment.

This new fund was was expected. It has been more than four years since Revolution announced its third growth fund, a vehicle that closed with $525 million in capital commitments. That’s a longer time between funds than we’re seeing more broadly across the venture industry, where teams have tended to raise new funds every two years roughly, but Revolution’s pacing could tie to its mission. The firm tends to invest primarily in what it long ago dubbed “rise of the rest” cities, where the cost of living and talent is less extreme and where checks go a lot further as a result.

The outfit is also investing out of more than one fund at a time. In recent years, it formed a seed practice and has since raised two Rise of the Rest seed funds, the most recent of which closed last year with $150 million in capital commitments.

Presumably, the firm’s investors have further taken note of some recent exits for Revolution. Earlier this year, its Boston-based portfolio company DraftKings closed on a three-way merger and debuted on the Nasdaq. Meanwhile, BigCommerce, an Austin-based SaaS startup helping companies build, manage and market online stores, went public via a traditional IPO in early August and currently boasts a market cap of $4.2 billion. (Revolution provided the capital for the company’s Series C round in 2013 and continued to invest in subsequent rounds.)

Others of Revolution’s notable investments include Orchard, a tech platform that helps users sell their current home while simultaneously purchasing their next one and whose $69 million Series C round was led by Revolution in September; TemperPack, a maker of thermal liners meant to address the plastic waste that raised $31 million in Series C funding this past summer, including follow-on funding from Revolution; and sweetgreen, the fast-casual restaurant chain that has endured some ups and downs owing to the pandemic but that closed on $150 million in funding a year ago and which first received backing from Revolution back in 2013.

Last month, we talked at some length with Case, including about his involvement in the creation of Section 230 Section 230 of the Communications Decency Act of 1996, which helped create today’s internet giants.

We also talked at the time about whether COVID-19 will cause Silicon Valley to finally lose its gravitational pull. Said Case at the time, in comments not published previously:

“Obviously the jury is out. I think a lot of people who decided to leave Silicon Valley to shelter someplace else, most of those will end up returning. I don’t think you’ll see a mass exodus from the city, whether that be Silicon Valley or New York or Boston, which some have predicted.

I do think some of the people who decided to leave at least temporarily will decide to stay, and most of them will end up still working for their current company, in part because some of the tech companies like Facebook and Square and many others have have made it easier to work remotely. But some, once they get settled in another place, and their family is settled, will likely will decide to do something different [and] I think it could be a helpful catalyst in terms of these rise-of-the-rest cities that were showing some signs of momentum. This could be an accelerant.”

We had also talked with Case about data that suggests that women and other founders who are not in the networking flow of traditional venture firms are getting left behind as deals are being struck over Zoom. He’d also seen the data and was surprised by it. As he told us:

Yeah, that’s a concern. And it’s a concern about place. It’s also a concerned about people. If you just look at the the NVCA data, last year, 75% of venture capital went to just three states and more than 90% of venture capital went to men and less than 10% to women, even though women represent half our population. And last year, even though Black Americans are about 14% of the population, Black founders got less than 1% of venture capital. So if you just look at the data, it does matter where you live, it does matter what you look like, it does matter the kind of school you went to.

I would have thought that because of the pandemic and because suddenly, Zoom meetings for pitches were becoming increasingly commonplace . . .that that would open up the aperture for most venture capitalists. They would be more willing to take meetings with people in other places, and also be willing to get to reach out to some of the diverse communities that they haven’t traditionally have invested in.

Some of that has happened, for sure. We have seen more interest among coastal investors in opportunities in these in these rise-of-the-rest cities. I think the challenge more broadly, when you go beyond place toward people is what you hear from more of these venture capitalists. They say, ‘Yes, we understand that it’s a problem we need to be help solve. It’s also an opportunity we can potentially seize, because some of these entrepreneurs are going to build some really valuable companies. But we don’t really have the networks. We tend to be mostly situated where we live and have worked or went to school and also where we’ve previously made investments. So we just don’t have the networks in the middle of a country. We don’t have networks with Black founders,’ and so forth.

So that’s an area that we’re really focusing on now: how do we extend the networks. I do think most VCs realize they should be part of the solution, and not part of the problem.

Case mentioned during our call — ahead of the U.S. presidential election — his longstanding friendship with now President-elect Joseph Biden. Case isn’t the only one at Revolution with ties to Biden, however. Ron Klain, an executive vice president at Revolution, previously served as Biden’s chief of staff when he was vice president and, as the world learned last week, Klain is again heading into politics after being chosen to serve as the White House chief of staff beginning in January.

Powered by WPeMatico

Software valuations are bonkers, which means it’s a great time to go public. Asana, Monday.com, Wrike and every other gosh darn software company that is putting it off, pay attention. Heck, even service-y Palantir could excel in this market.

Let me explain.

Over the past few weeks, TechCrunch has tracked the filing, first pricing, rejiggered pricing range, and, today, the first day of trading for BigCommerce, a Texas-based e-commerce company. You can think of it as a comp with Shopify to a degree.

Image Credits: IMGFlip (opens in a new window)

In the wake of the Canadian phenom’s blockbuster earnings report, BigCommerce boosted its IPO range. Yesterday the company did itself one better, pricing $1 per share above that raised range, selling 9,019,565 shares at $24 per share, of which 6,850,000 came from BigCommerce itself.

Before some additions, there are now 65,843,546 shares of BigCommerce in the world, giving the company an IPO valuation of around $1.58 billion.

Given that the company’s Q2 expected revenue range is “between $35.5 million and $35.8 million,” the company sported a run-rate multiple of 11.1x to 11x, depending on where its final revenue tally comes in. That felt somewhat reasonable, if perhaps a smidgen light.

Then the company opened at $68 per share today, currently trading for $82 per share. Hello, 1999 and other insane times. BigCommerce is now worth, using some rough math, around $5.4 billion, giving it a run-rate multiple of around 38x, using the midpoint of its Q2 revenue range.

Powered by WPeMatico

As expected, BigCommerce has filed to go public. The Austin, Texas, based e-commerce company raised over $200 million while private. The company’s IPO filing lists a $100 million placeholder figure for its IPO raise, giving us directional indication that this IPO will be in the lower, and not upper, nine-figure range.

BigCommerce, similar to public market darling Shopify, provides e-commerce services to merchants. Given how enamored public investors are with its Canadian rival, the timing of BigCommerce’s debut is utterly unsurprising and is prima facie intelligent.

Of course, we’ll know more when it prices. Today, however, the timing appears fortuitous.

BigCommerce is a SaaS business, meaning that it sells a digital service for a recurring payment. For more on how it derives revenue from customers, head here. For our purposes what matters is that public investors will classify it along with a very popular — today’s trading notwithstanding — market segment.

Starting with broad strokes, here’s how the company performed in 2019 compared to 2018, and Q1 2020 in contrast to Q1 2019:

BigCommerce didn’t grow too quickly in 2019, but its Q1 2020 expansion pace is much better. BigCommerce will file an S-1/A with more information in Q2 2020, we expect; it can’t go public without sharing more about its recent financial performance.

If the company’s revenue growth acceleration continues in the most recent period — bearing in mind that e-commerce as a segment has proven attractive to many businesses during the COVID-19 pandemic — BigCommerce’s IPO timing would appear even more intelligent than it did at first blush. Investors love growth acceleration.

Moving from revenue growth to revenue quality, BigCommerce’s Q1 2020 gross margins came in at 77.5%, a solid SaaS result. In Q1 2019 its gross margin was 76.8%, a slightly worse figure. Still, improving gross margins are popular as they indicate that future cash flows will grow at a faster clip than revenues, all else held equal.

In 2018 BigCommerce lost $38.9 million on a GAAP basis. Its net loss expanded modestly to $42.6 million in 2020, a larger dollar figure in gross terms, but a slimmer percent of its yearly top line. You can read those results however you’d like. In Q1 2020, however, things got better, as the company’s GAAP net loss fell to $4 million from its year-ago Q1 result of $10.5 million.

The BigCommerce big commerce business is growing more slowly than I had anticipated, but its overall operational health is better than I expected.

A few other notes, before we tear deeper into its S-1 filing tomorrow morning. BigCommerce’s adjusted EBITDA, a metric that gives a distorted, partial view of a company’s profitability, improved along similar lines to its net income, falling from -$9.2 million in Q1 2019 to -$5.7 million in Q1 2020.

The company’s cash flow is, akin to its adjusted EBITDA, worse than its net loss figures would have you guess. BigCommerce’s operating activities consumed $10 million in Q1 2020, an improvement from its Q1 2019 operating cash burn of $11.1 million.

The company is further in debt than many SaaS companies, but not so far as to be a problem. BigCommerce’s long-term debt, net of its current portion, was just over $69 million at the end of Q1 2020. It’s not a nice figure, per se, but it is one small enough that a good IPO haul could sharply reduce while still providing good amounts of working capital for the business.

Investors listed in its IPO document include Revolution, General Catalyst, GGV Capital, and SoftBank.

Powered by WPeMatico

Earlier today we took a look at two companies that have filed to go public, nCino and GoHealth. The pair join Lemonade in a march toward the public markets.

But those three firms are hardly alone. We know that DoorDash filed privately earlier this year (it also raised a pile of cash lately, so its IPO may not be in a hurry), and Postmates filed privately last year.

Even more, there are a number of companies whose IPOs we anticipate in short order. So, what follows is our incredibly scientific survey of impending IPOs, starting with those closest to the gate. This list is focused on companies that were at one point venture-backed startups, even if they have become behemoths in the intervening years.

We’ll start with companies that have filed and are moving toward debuts in the next few weeks:

And, next, companies that have filed privately but are still hanging back:

And here are companies that are making the sort of noise that one might make before finally going public:

All of the above is a jam, and I am stoked to dig through the S-1 trenches with you.

Powered by WPeMatico

Chris Fry, the man who waged war against the Fail Whale as Twitter’s former senior vice president of engineering, has joined Bigcommerce’s board of advisors. The e-commerce startup, which has offices in San Francisco, Austin, and Sydney, Australia, says that Fry will work closely with its product and development teams as its focuses on international expansion. Last month,… Read More

Chris Fry, the man who waged war against the Fail Whale as Twitter’s former senior vice president of engineering, has joined Bigcommerce’s board of advisors. The e-commerce startup, which has offices in San Francisco, Austin, and Sydney, Australia, says that Fry will work closely with its product and development teams as its focuses on international expansion. Last month,… Read More

Powered by WPeMatico