Bedrock Capital

Auto Added by WPeMatico

Auto Added by WPeMatico

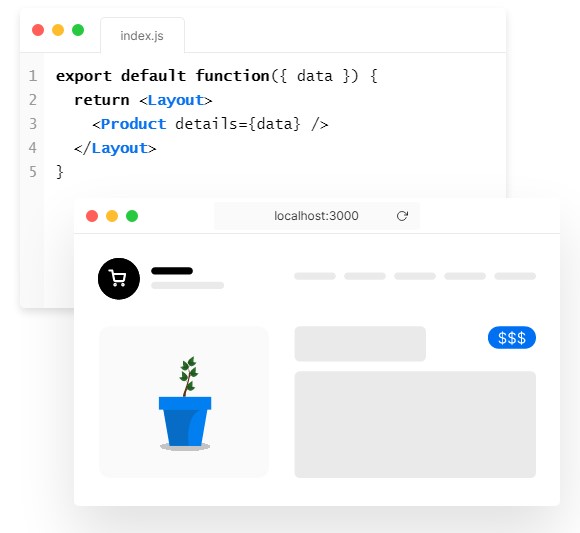

Vercel, the company behind the popular open-source Next.js React framework, today announced that it has raised a $102 million Series C funding round led by Bedrock Capital. Existing investors Accel, CRV, Geodesic Capital, Greenoaks Capital and GV also participated in this round, together with new investors 8VC, Flex Capital, GGV, Latacora, Salesforce Ventures and Tiger Global. In total, the company has now raised $163 million and its current valuation is $1.1 billion.

As Vercel notes, the company saw strong growth in recent months, with traffic to all sites and apps on its network doubling since October 2020. The number of sites among the world’s largest 10,000 websites that use Next.js grew 50% in the same time frame, too.

Image Credits: Vercel

Given the open-source nature of the Next.js framework, not all of these users are obviously Vercel customers, but its current paying customers include the likes of Carhartt, Github, IBM, McDonald’s and Uber.

“For us, it all starts with a front-end developer,” Vercel CEO Guillermo Rauch told me. “Our goal is to create and empower those developers — and their teams — to create delightful, immersive web experiences for their customers.”

With Vercel, Rauch and his team took the Next.js framework and then built a serverless platform that specifically caters to this framework and allows developers to focus on building their front ends without having to worry about scaling and performance.

Older solutions, Rauch argues, were built in isolation from the cloud platforms and serverless technologies, leaving it up to the developers to deploy and scale their solutions. And while some potential users may also be content with using a headless content management system, Rauch argues that increasingly, developers need to be able to build solutions that can go deeper than the off-the-shelf solutions that many businesses use today.

Rauch also noted that developers really like Vercel’s ability to generate a preview URL for a site’s front end every time a developer edits the code. “So instead of just spending all your time in code review, we’re shifting the equation to spending your time reviewing or experiencing your front end. That makes the experience a lot more collaborative,” he said. “So now, designers, marketers, IT, CEOs […] can now come together in this collaboration of building a front end and say, ‘that shade of blue is not the right shade of blue.’”

“Vercel is leading a market transition through which we are seeing the majority of value-add in web and cloud application development being delivered at the front end, closest to the user, where true experiences are made and enjoyed,” said Geoff Lewis, founder and managing partner at Bedrock. “We are extremely enthusiastic to work closely with Guillermo and the peerless team he has assembled to drive this revolution forward and are very pleased to have been able to co-lead this round.”

Powered by WPeMatico

SoleSavy, a community built around buying hot sneakers and related items that are increasingly hard to acquire at retail, raised $2 million in a round that closed late last year. SoleSavy is a group of communities that is currently mostly hosted on Slack.

SoleSavy’s co-founders Dejan Pralica and Justin Dusanj founded the company in 2018 as a paid community for collectors and enthusiasts seeking pairs that were getting snapped up by bots or resellers. Pralica previously co-founded Kicks Deals, a sneaker shipping site focused on less than retail pricing and Dusanj is the former director of Operations at New Age Sports, a Nike retailer.

SoleSavy’s $2 million party raise includes investment from Panache Ventures, Jason Calacanis’ LAUNCH, Turner Novak, Ben Narasin, Morning Brew’s Alex Lieberman and Austin Rief, Tiny Capital, Wesley Pentz (yes, Diplo), Matthew Hauri aka Yung Gravy, Ryan Holmes, Roham Gharegozlou and Bedrock Capital.

SoleSavy has built an engaged community (several communities, really) around the ebb and flow of the sneakerhead consumer universe (SCU). I just coined that, by the way, please make it a thing. The SCU is an interesting place filled with fascinating characters and behaviors. Every once in a while it pokes its head into the mainstream, whether via a documentary, a hot shoe release or a strong-arm robbery attempt. In 2021, I believe that we will see more of this world breaking out of its box into the larger consumer consciousness.

The trends that are leading us to this place are varied, but some of them have been front and center during the pandemic, as a decade’s worth of consumer behavioral change has occurred in the space of a few months. You only have to look at how hard it was to get a PS5 or Xbox One X or a GPU for the holiday season, and how many services, Twitter accounts and monitor groups rose up to try to help people do that to see what the future of shopping looks like.

I joked about not being able to buy butter without a bot, but it’s not far from the truth — nearly every category of goods has had its own shortages over the last year. But the mother of all limited goods category for decades now has been sneakers.

Every release is hotly anticipated and eagerly purchased by people looking for the latest shoe. The massive increase in interest in the sneaker as the marquee desirable item and the unwillingness of the biggest manufacturers to lose the hype halo has led to each drop being harder to get than the last. Second-market startups like StockX and GOAT have sprung up to facilitate those who don’t mind paying 30%-200% premiums on each release.

The solution for many lies in the countless “cook groups” that help buyers anticipate demand and stock for each drop and plan to purchase them on release date.

SoleSavy’s function is ostensibly to do just that: help regular enthusiasts to strategize and execute the release-day cop. But beyond that, Pralica says that the group has come to be about the community of people around those shoes more than the purchase itself.

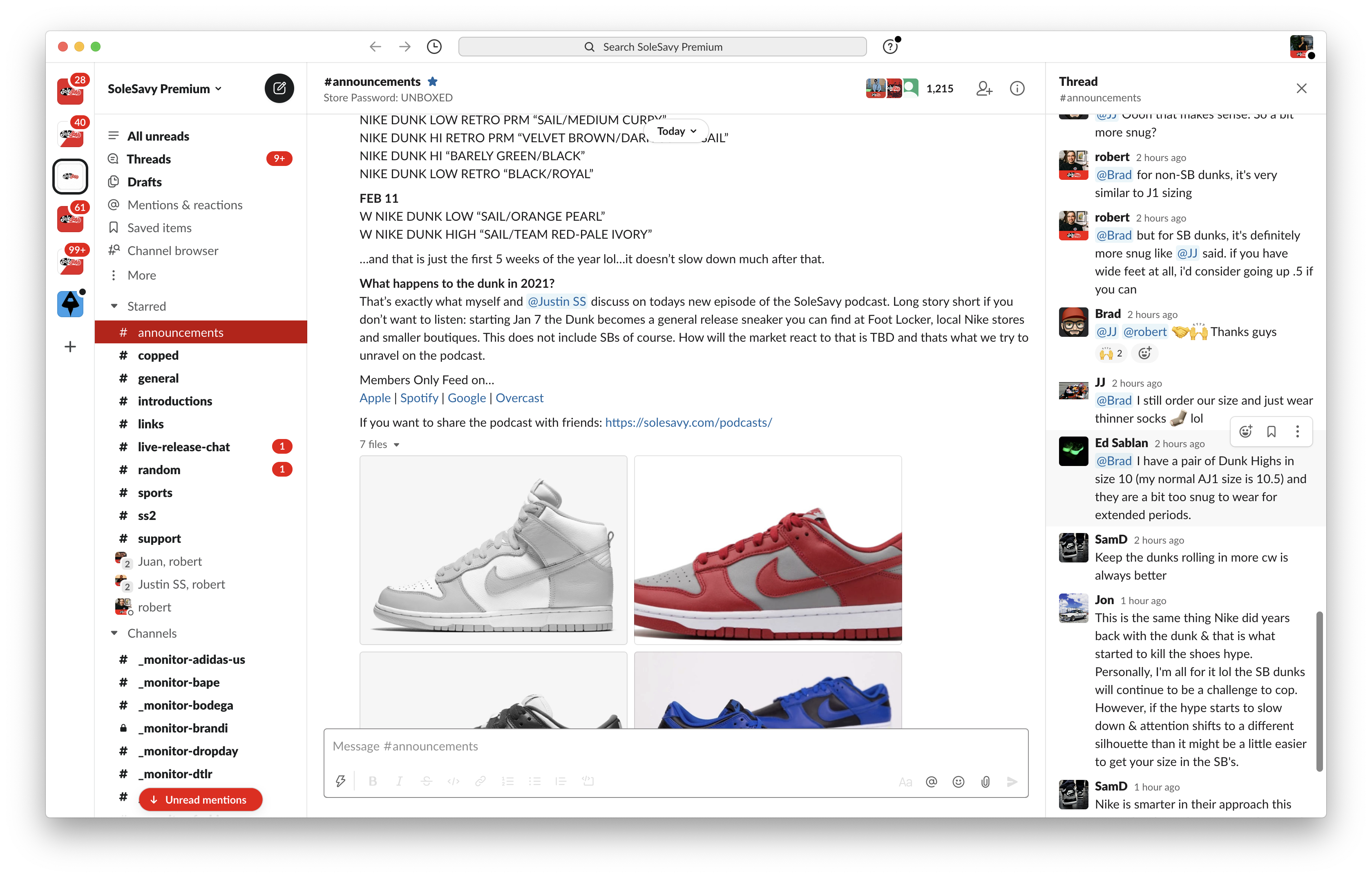

Image Credits: SoleSavy

SoleSavy is at its heart a Slack group (a series of groups actually that act as cohorts, leading people through the tiers of community that the team has built) with rooms that help people to understand what’s happening in sneakers, get the releases and commiserate around the culture. Pralica says that they’ve built that community out slowly (the waitlist for the group grows by 400 people per day) in order to maintain a positive atmosphere and to properly onboard new people to the group. They also have an app that drives push notifications and a podcast.

That positive community vibe is what Pralica says is SoleSavy’s long-term focus and differentiating factor that keeps the 4,000 members across the U.S. and Canada interacting with the group on a nearly daily basis.

I’ve been in a dozen or so different groups focused on buying large quantities of each release to re-sell over the years and many of them are, at best, rowdy and at worst toxic. That’s an environment that SoleSavy wanted to stay away from, says Pralica. Instead, SoleSavy tries to court those who want to buy and wear the shoes, trade them and yes, maybe even resell personal pairs eventually to obtain and wear another grail.

Though cook groups have been the “core” of the Discord and Slack-based communities in the sneaker world, other iterations have been booming too. Entrepreneurial communities based in the same hustle principles like Tyler Blake’s In This Economy and fanbase-focused groups around popular streamers top the Disboard. And bets on social token outfits like Zora are also focused on community as the glue that holds together a user base.

Community is the future of all commerce, whether you’re looking for a specific product (see the huge PS5 monitors) or want to steep yourself in a particular universe of product interest (the SCU). The trends that I’ve been seeing all point to 2021 being the year that community-driven purchasing breaks out of the underbelly of fandom and becomes officially “a thing.”

Image Credits: SoleSavy

SoleSavy has been experimenting with a variety of ways to keep the community knit going, including live chats, get-togethers and even a handsome custom community-designed Jordan 1. These efforts have driven the previously bootstrapped company to some impressive early numbers. Pralica says that SoleSavy is currently profitable, with $1.5 million ARR on $33 monthly subscriptions plus affiliate revenue and that their DAUs are at 90% — an engagement number that would make any retailer salivate.

Though the funding closed (very) late last year I thought that this would be a great kick-off story for the year ahead. Though SoleSavy seems to have a really compelling story and a great growth curve, I think they’re at the tip of a very large trend, one that we will see continue to build throughout the year.

Powered by WPeMatico

Big news today the world of IT startups targeting businesses. Rippling, the startup founded by Parker Conrad to take on the ambitious challenge of building a platform to manage all aspects of employee data, from payroll and benefits through to device management, has closed $145 million in funding — a monster Series B that catapults the company to a valuation of $1.35 billion.

Parker Conrad, the CEO who co-founded the company with Prasanna Sankar (the CTO), said in an interview that the plan will be to use the money to continue its own in-house product development (that is, bringing more tools into the Rippling mix organically, not by way of acquisition) but also to have it just in case, given everything else going on at the moment.

“We will double down on R&D but to be honest we’re trying not to change the formula too much,” Conrad said. “We want to have that discipline. This fundraising was opportunistic amid the larger macroeconomic risk at the moment. I was working at startups in 2008-2009 and the funding markets are strong right now, all things considered, and so we wanted to make sure we had the stockpile we needed in case things went bad.”

This latest round included Greenoaks Capital, Coatue Management and Bedrock Capital, as well as existing investors including Kleiner Perkins, Initialized Capital and Y Combinator. Founders Fund partner Napoleon Ta will join Rippling’s board of directors. Founders Fund had also backed Zenefits when Parker was at the helm, and from what we understand, this round was oversubscribed — also a big feat in the current market, working against a lot of factors, including a wobbling economy.

It is a big leap for the company: it was just a little over a year ago that it raised a Series A of $45 million at a valuation of $270 million.

This latest round is notable for a few reasons.

First is the business itself. HR and employee management software are two major areas of IT that have faced a lot of fragmentation over the years, with many businesses opting for a cocktail of services covering disparate areas like employee onboarding, payroll, benefits, device management, app provisioning and permissions and more. That’s been even more the case among smaller organizations in the 2-1,000 employee range that Rippling targets.

Rippling is approaching that bigger challenge as one that can be tackled by a single platform — the theory being that managing HR employee data is essentially part and parcel of good management of IT data permissions and device provision. This funding is a signal of how both investors and customers are buying into Rippling and its approach, even if right now the majority of customers don’t onboard with the full suite of services. (Some 75% are usually signing up with HR products, Conrad noted.)

“We like to think of ourselves as a Salesforce for employee data,” Conrad said, “and by that, we think that employee data is more than just HR. We want to manage access to all of your third-party business apps, your computer and other devices. It’s when you combine all that that you can manage employees well.”

The company is gradually adding more tools. Most recently, it’s been launching new tools to help with job costing, helping companies track where employees are spending time when working on different projects, a tool critical for IT, accounting and other companies where employees work across a number of clients. Other new tools include SMS communications for “desk-less” workers and more accounting integrations.

Second is the founder. You might recall that Conrad was ousted from his previous company, Zenefits (taking on a related, but smaller, challenge in payroll and benefits), over a controversy linked to compliance issues and also misleading investors. But if Zenefits was finished with Conrad, Conrad was not finished with Zenefits — or at least the problem it was tackling. This funding is a testament to how investors are putting a big bet on Conrad himself, who says that a lot of what he has been building at Rippling was what he would have done at Zenefits if he’d stayed there.

“Once you’re lucky, twice you’re good,” said Mamoon Hamid, a partner at Kleiner Perkins, in a separate statement. “Parker is a true product visionary, and he and his team are solving an enormous pain point for businesses everywhere. We’re thrilled to continue partnering with Rippling as demand for their platform dramatically increases in this era of remote work.”

“Rippling is not just a superior payroll company, but something much broader: they’ve built the system of record for all employee data, creating an entirely new software category. Rippling’s massive market opportunity is to streamline the employee life cycle, from software to payroll to benefits, and fundamentally improve the way businesses hire and manage their employees,” said Ta in a statement.

Third is the context in which this round is coming. We’re in the midst of an economic downturn caused in part by a global health pandemic, and that’s leading to a lot of companies curtailing budgets, reducing headcount and potentially shutting down altogether. Ironically, that force is also propelling companies like Rippling full steam ahead.

Its SaaS model — priced at a flat $8 per person per month — not only fits with how many businesses are being run at the moment (primarily remotely), but Rippling’s purpose is specifically geared to helping businesses both onboard and offboard employees more efficiently, the kind of software that companies need to have in place to fit how they are working right now.

Updated with commentary from an interview with Conrad.

Powered by WPeMatico

Sex, despite being one of the most fundamental human experiences, is still one of those businesses that some advertisers reject, banks are hesitant to financially support and some investors don’t want to fund.

Given how sex is such a huge part of our lives, it’s no surprise founders are looking to capitalize on the space. But the idea of pleasure versus function, plus the stigma still associated with all-things sex, is at the root of the barriers some startup founders face.

Just last month, Samsung was forced to apologize to sextech startup Lioness after it wrongfully asked the company to take down its booth at an event it was co-hosting. Lioness is a smart vibrator that aims to improve orgasms through biofeedback data.

Sextech companies that relate to the ability to reproduce or, the ability to not reproduce, don’t always face the same problems when it comes to everything from social acceptance to advertising to raising venture funding. It seems to come down to the distinction between pleasure and function, stigma and the patriarchy.

This is where the trajectories for sextech startups can diverge. Some startups have raised hundreds of millions from traditional investors in Silicon Valley while others have struggled to raise any funding at all. As one startup founder tells me, “Sand Hill Road was a big no.”

Powered by WPeMatico

A new wave of female-led businesses wants to help women get off.

Dipsea, an app-based platform for short-form erotic audio stories, is the latest to grab funding from venture capital investors. The female-founded, San Francisco-headquartered startup, which officially launched in December, has raised $5.5 million in a round led by Bedrock Capital and Thrive Capital. The funding comes amid a notable explosion in interest and investment in audio content consumption and creation, as well as an uptick in AirPod sales, easily removable wireless earbuds that encourage listeners to enjoy snackable audio like Dipsea’s erotica.

In addition to Dipsea’s seed financing, podcasting platform WaitWhat secured a $4.3 million round this month. Days earlier, Himalaya nabbed $100 million to scale its podcast distribution tool and a pair of podcast startups, Gimlet and Anchor, sold to Spotify in a nine-figure deal.

Meanwhile, as the audio content space booms, more attention is being paid to female entrepreneurs eyeing venture capital. Enter Dipsea, whose founders say the business captures the zeitgeist of female empowerment.

Dipsea’s subscription-based app, available for $8.99 per month or $48 per year, offers short audio stories meant to turn women on. The app’s library, which is poised to expand with the new cash, includes narrative sexy stories and non-narrative guided audio pieces. The stories are designed to be listened to at any time, with the company’s examples including solo in bed, while getting ready for a date or to help turn off boss brain on the way home from work. The subscription business model made me wince at first, but auditory erotica doesn’t exactly lend itself to an advertising business model, after all, and once I listened to a few of Dipsea’s short stories, I understood that the service is something many women would pay for.

Since the onset of internet porn, there’s been a gaping hole in content crafted specifically for women. Most women use “mental framing” to get turned on, meaning they imagine scenarios, often with detailed story-lines and characters to stimulate themselves, per a study by OMGYes and The Kinsey Institute. Dipsea’s sensorial audio storytelling sets the mood and sparks the listener’s imagination.

“Audio is amazing because it’s imaginative; it requires you to paint a picture in your brain that’s very stimulating and it’s super intimate and very personal,” Dipsea co-founder and chief executive officer Gina Gutierrez told TechCrunch.

The brand and design strategist started Dipsea alongside chief technical officer Faye Keegan, a former product manager at Neighborly. Gutierrez said she came up with the idea while meditating with Headspace, a wellness app.

The founders have prioritized diversity of perspective, working with freelance writers of different backgrounds on various episodes, as well as consensuality, ensuring a form of verbal consent is worked into storylines. They recently hired their first staff writer.

“To me the future of entertainment is sensory,” Gutierrez said. “This felt like it could be a medium for women that hadn’t been harnessed or attempted before.”

Powered by WPeMatico

Local newspapers may be shuttering and people may be consuming most news on social media, but don’t tell Alex Mather that a subscription news publication can’t grow like a unicorn startup. His 2-year-old sports publisher The Athletic has gained over 100,000 paid subscribers (60 percent under age 34) and has a 90 percent retention rate.

Having already raised $30 million in its short life, the company announced a new $40 million Series C yesterday, led by Founders Fund and Bedrock Capital. It reportedly values The Athletic around $200 million.

I interviewed Alex Mather (The Athletic’s CEO) and Eric Stomberg (partner at Bedrock Capital) to understand what’s behind the breakout success, and why they think this publishing startup can scale to become a multi-billion dollar company.

EP: Bedrock makes concentrated, contrarian bets. Explain how The Athletic fits that.

ES: I first met Alex and Adam in 2016 during Y Combinator. The popular view then, as it remains now, was that people just aren’t willing to pay for content online and that to win in media you have to put out a high volume of free articles on social.

The Athletic took the opposite approach. It’s a narrative violation. Everything is part of a paid subscription, with the belief that instead of writers needing to post 3-4 pieces per day, they should focus on deeper stories that add value to paid subscribers over time. That worldview resonated with us. If you can create content at scale that people are willing to pay for, that’s a powerful economic engine.

There’s so much sports coverage already out there, by professionals and amateurs alike, so why are people willing to pay for The Athletic?

AM: While there appears to be an abundance of content, most of it is aggregated, shallow content for a broad audience. We produce fewer stories and target a diehard fan. Our subscribers consistently tell us that no one else produces the same depth on a daily basis.

How did you determine the $60/year price point?

AM: We think of $60/year ($5/month) as less than the average NBA ticket. It’s a meaningful price but not prohibitive, especially when we do discounts in the first year. Like all subscription companies, whether we like it or not, we have to consider how our pricing stacks up against Netflix. For $10/month, you can subscribe to Netflix which is spending $8 billion per year in content.

Is The Athletic profitable?

AM: We expand by launching in local markets. We are in 47 thus far. The operational focus is on building a local team and becoming profitable in each local market. I can tell you that most markets are profitable in the first year — currently all of our markets over one year old are profitable and most of those over 6 months old are profitable.

(Photo by Thearon W. Henderson/Getty Images)

Explain your growth strategy in terms of coverage: Which sports did you start with and at which level (local versus national)?

AM: Direct-to-consumer businesses have to really work to earn their subscribers’ hard-earned money. We have to obsess over where we can be different. In the beginning, that was with hockey and baseball, because those have been de-prioritized by the bigger players. That shifted as we gained more subscribers: we needed to become comprehensive. We hired folks to cover the NBA, to cover the NFL, to cover soccer.

Do subscribers usually come just for one local sport or for the broader bundle?

AM: We’ve built a powerful bundle. A local newspaper has local politics, local restaurants, and then local sports. We have just the sports, but add a national perspective and a nationwide bundle. Most of our subscribers are “super bundlers,” meaning they subscribe to content from multiple cities plus at least one national product and usually a college product that’s not local. We provide all that for significantly less than competitors.

Eric — as a VC looking for multi-billion-dollar exits, how are you analyzing the potential scale of a subscription publication like this? Even most people who are bullish on subscriptions believe it’s a choice of going for a niche audience and staying small.

ES: There are two things we look for in a subscription business: retention and a positive flywheel.

Retention. In any subscription business, the key question is: can they maintain their subscribers over time? Most of them don’t. Spotify does, Netflix does, and The Athletic does as well. The Athletic is off the charts, which sets it up for scale. You want to see deep engagement over a very, very long period of time — years.

A positive flywheel. The more you build your subscriber base, the more you build your revenue base. That allows you to get better content, to hire unique writers, to build greater depth. In doing so, you attract people who weren’t ready to subscribe in the early days but now you have writers they follow and content they want. Technology is important here too: as you build a bigger platform with more content, serving the right content at the right time to each user is a key advantage. When this flywheel is working it’s actually quite hard to put a ceiling on the business.

Most publishers did a so-called “pivot to video” over the last couple of years. You’re anchored in writing. Why not more video at the start?

AM: We’re obsessed with the consumer and all our research in the beginning said that people still like to read books and articles. Advertising with text may not be as good as with video, which may be why so many other companies “pivoted to video,” but we think the written word is still the best way to convey certain types of stories. It’s straightforward, it doesn’t require headphones.

There’s an incredible amount of talent out there that can produce these stories and that has been cast aside by many entities. We saw it as an opportunity to give them great jobs and bring value to our subscribers. That has paid off for us.

What are your plans for video or other content formats in the future?

AM: We raised this Series C with audio and video in mind. We can tell even more stories when we add in audio and video possibilities. Our goal is to serve the subscriber: some love to read, some love to listen, others prefer to watch. We look up to things like The Ringer, Andre the Giant on HBO, VICE News, Gimlet, and The Daily by The New York Times all as incredible storytelling, and we ask ourselves “how can we do sports versions of those?”

Why focus on hiring experienced, full-time writers rather than a stable of contributors or curating from the vast pool of content by fans? Lots of amateurs pay close attention to sports.

AM: What’s really important to us is a growth mentality — that by Day 100 on our team a writer is thinking very differently. We’re providing lots of data, lots of feedback. We invest in great people who will figure this out with us over time. Also, scaling so quickly from 0 to 300 editorial staff was possible because we recruited experienced talent who know what to do already.

We do have about 400 contributors as well. These are folks who may be lawyers or accountants but are passionate about the teams they cover. We are a way for them to reach a premium audience. We can pay them really well and give them world-class editors formerly with Sports Illustrated and ESPN.

How are you acquiring your subscribers?

AM: When we expand into a new market, we gain new subscribers by hiring writers who have a following already and by word of mouth from existing subscribers. Then like any direct-to-consumer brand, we are acquiring subscribers through Google, Facebook and Twitter.

You financially incentivize your writers based on them acquiring new subscribers through their articles or by promoting The Athletic with their followers online. That is very uncommon in publishing. Explain that strategy.

AM: It ties back to our focus on building for the long term and investing in talent that will grow with us. We like to assign incentives that give us the best chance of building a sustainable business and we think about compensation in that way. We give our team equity in the company and for many, we tie a portion of their comp to the performance of their team, sport, city. It’s a great way to share in the responsibility and success of the business.

At the bottom of articles, you ask readers to rate each story as “Meh,” “Solid,” or “Awesome.” I wish every publisher did this. How do you use this data? How do a writer’s scores impact them?

AM: It’s about feedback loops. Our writers gauge feedback when they share on Twitter. This is another data point. It helps paint a more complete picture. NPS alone isn’t enough of course though. We look at whether articles drive new subscribers, drive deep engagement, drive comments, etc. We don’t use pageviews, but we certainly use metrics. Usually, this results in a writer producing very different work on Day 100 than they were on Day 0.

Explain the interaction between subscribers. It’s not unique to have a comments section: there are bad comments sections, good comments sections and comments sections that go unused. At a tactical level, how do you think about building community?

AM: My co-founder and I met at Strava, the social network for endurance athletes. I ran the product team and we were obsessed with community. We see an incredible connection between community engagement and subscriber retention. The question that drives us is how can we connect users in an authentic way, how can we connect users to our staff in an authentic way, how can we connect users to athletes in an authentic way. We’re doing a lot of experimentation here. We have a distinct opportunity because of our paywall: most of the comments on The Athletic are saying substantive things.

Powered by WPeMatico