Banking

Auto Added by WPeMatico

Auto Added by WPeMatico

Latin America (LATAM) is home to one of the fastest-growing mobile markets in the world. In 2018, there were 326 million mobile internet users in the region, and that figure is anticipated to increase to over 422 million users by 2025. Part of the reason for such exponential growth is that mobile is the main tool for internet access in Latin America, providing a portable way for people living in rural areas to get online. The social media boom and rise in messaging platforms in recent years have also spurred demand for optimized mobile services.

As mobile penetration continues in LATAM, it is facilitating innovative apps that promote opportunities for social mobility, financial control, access to overseas markets and societal development. And while a difference in maturity levels and local regulations dictates the mobile landscape for individual countries, there are visible trends throughout the region.

These trends are both reactions to LATAM’s unique mobile conditions and broader international influences, so can be telling of future mobile user expectations and behaviors. By recognizing and assimilating these trends, new mobile apps and services can disrupt the market in a more meaningful way.

Here are the current and upcoming trends of mobile growth across Latin America:

Approximately 70% of Latin America’s population is unbanked or underbanked, meaning there is a huge opportunity to improve financial access. One emerging solution is digital wallets, which work via top-ups and don’t require a bank account with a physical company or branch to set up. Digital wallets, therefore, bypass the mistrust that many Latin Americans have around official banking institutions.

COVID-19 has certainly contributed to the heightened demand for mobile wallets in LATAM. As a predominantly cash-driven location, concerns about handling paper money have been confirmed as new studies reveal that the virus can survive on physical currency for 28 days. In turn, masses of citizens and consumers have begun looking for safer alternatives to cash. In Mexico, digital wallets are thought to occupy a 27.7% share of the business-to-consumer e-commerce payments market by 2021, while Argentina has also been showing high in-store use of digital wallets during the pandemic.

Over in Venezuela, AirTM’s digital wallet has been processing funds promised by interim President Guaidó to essential workers. The company has been instrumental in delivering the money to healthcare staff after the Maduro regime blocked the provider operating in the country. Beyond financial aid, digital wallets in Venezuela and other countries with high inflation rates mean locals don’t have to carry large amounts of bills and coins with them.

Powered by WPeMatico

The economic impact of the COVID-19 pandemic adversely affected the financial outlook for millions of people, and continues to cause significant fiscal distress to millions more, but such challenging times have also wrought a more resilient and resourceful financial system.

With the ingenuity of crowdfunding, considered to be one of the last decade’s greatest “success stories,” and such desperate times calling for bold new ways to finance a wide variety of COVID-19 relief efforts, we are now seeing an excellent opportunity for banks and other financial institutions to partner with crowdfunding platforms and campaigns, bolstering their efforts and impact.

Before considering how financial institutions can assist with crowdfunding campaigns, we must first look at the diverse array of impressive results from this financing option during the pandemic. As people choose between paying the rent or buying groceries, and countless other despairing circumstances, we must look to some of the more inventive ways businesses, entrepreneurs and people in general are using crowdfunding to provide the COVID-19 relief that cash-strapped consumers with maxed-out or poor credit do not have access to or the government has not provided.

Some great examples of COVID-19 crowdfunding at its best include the following:

The possibilities presented by crowdfunding in this age of the coronavirus are endless, and financial institutions can certainly lend their assistance. Here is how.

Crowdfunding is a substantial and ever-so relevant means of financing all sorts of businesses, people and products. Denying its substantive contribution to the economy, especially in digital finance during this pandemic, is akin to wearing a monocle when you actually need glasses for both of your eyes. Do not be shortsighted on this. Crowdfunding is here to stay. In fact, countless crowdfunding businesses and platforms continue to make major moves within the markets globally. For example, Parpera from Australia, in coordination with the equity-crowdfunding platforms, hopes to rival the likes of GoFundMe, Kickstarter and Indiegogo.

This might seem contrary to the original purpose of these campaigns, but the right amount of seed-cash infusions to campaigns that are aligned with your goals as a company is a win-win for both you and the entrepreneurs or causes, especially now in such desperate times of need.

This means that small businesses and medium-sized businesses within your institution’s community could use your help. Consider investing in crowdfunding campaigns similar to the ones mentioned earlier. Better yet, bridge the gaps between financial institutions and crowdfunding platforms and campaigns so that smaller businesses get the opportunities they need to survive through these difficult times.

Last month, the United Nations Development Program released a report proclaiming that digital finance is now allowing people from all over the world to customize and personalize their money-management experiences such that their financial needs have the potential to be more readily and sufficiently met. Financial institutions willing to work as a partner with crowdfunding platforms and campaigns will further these goals and set society up for a more robust rebound from any possible detrimental effects of the COVID-19 recession.

Other countries are already beginning to figure out better ways to regulate the crowdfunding financing industry, such as the recent updates to the European Union’s handling of crowdfunding regulations, set to take effect this fall. Well-established financial institutions can lend their support in defining the policies and standard operating procedures for crowdfunding even during such a chaotic time as the COVID-19 pandemic. Doing so will ensure fair and equitable financing for all, at least, in theory.

While originally born out of either philanthropy or early-adopting innovation, depending on the situation, person or product, crowdfunding has become an increasingly reliable means of providing COVID-19 economic relief when other organizations, including the government and some banks, cannot provide sufficient assistance. Financial institutions must lend their vast expertise, knowledge and resources to these worthy causes; after all, we are all in this together.

Powered by WPeMatico

It’s only been a few months since Lili announced its $10 million seed round, and it’s already raised more funding — namely, a $15 million Series A.

The startup, founded by CEO Lilac Bar David and CTO Liran Zelkha, is creating a bank account and associated products designed for freelancers, with features like early access to direct deposit payments and the ability to set aside a percentage of income for taxes.

The account (and associated Visa debit card) is free of overdraft fees or minimum balance requirements; Bar David said the company only makes money from card processing fees.

She also said that the platform has seen rapid growth this year, with transactions up 700% since the beginning of the pandemic and nearly 100,000 accounts opened since the launch in 2019.

Bar David suggested that the economic turmoil caused by COVID-19 has prompted (or forced) more skilled workers — such as programmers and digital marketers — to turn to freelancing. Meanwhile, she’s also seen “a big shift from part-time freelance to full-time freelance.”

Lili CEO Lilac Bar David

Bar David predicted that the recent growth of the freelance economy won’t simply disappear once the pandemic is over, because workers are discovering the benefits of freelancing.

“If you have a 9-to-5 job, you’re dependent on one employer,” she said. “If something happens you’re out of a job … If you’ve got a diversified customer base, you’re not dependent on just one source of income.”

In recent months, Lili has added new features like automatically generated quarterly income and expense reports, a digital debit card (which customers can use before the physical card arrives in the mail) and the ability to send and receive money via Google Pay (Lili already supported Cash App and Venmo) .

Bar David said the startup decided to raise more funding to expand its engineering team and further accelerate its growth. Apparently she was preparing for a traditional Series A fundraising process (albeit one that was conducted in the middle of a pandemic), but “our current investors were so tremendously impressed by the product-market fit and the growth” that they were willing to fund almost all of the new round.

So the Series A was led by previous investor Group 11, with participation from Foundation Capital, AltaIR Capital, Primary Venture Partners and Torch Capital — along with new backer Zeev Ventures.

“As the global workforce evolves at a rapid pace, we are excited to lead another round of funding to help Lili capitalize on unprecedented demand and offer an entirely new solution to help freelancers seamlessly save time and money,” said Group 11’s Dovi Frances in a statement.

Powered by WPeMatico

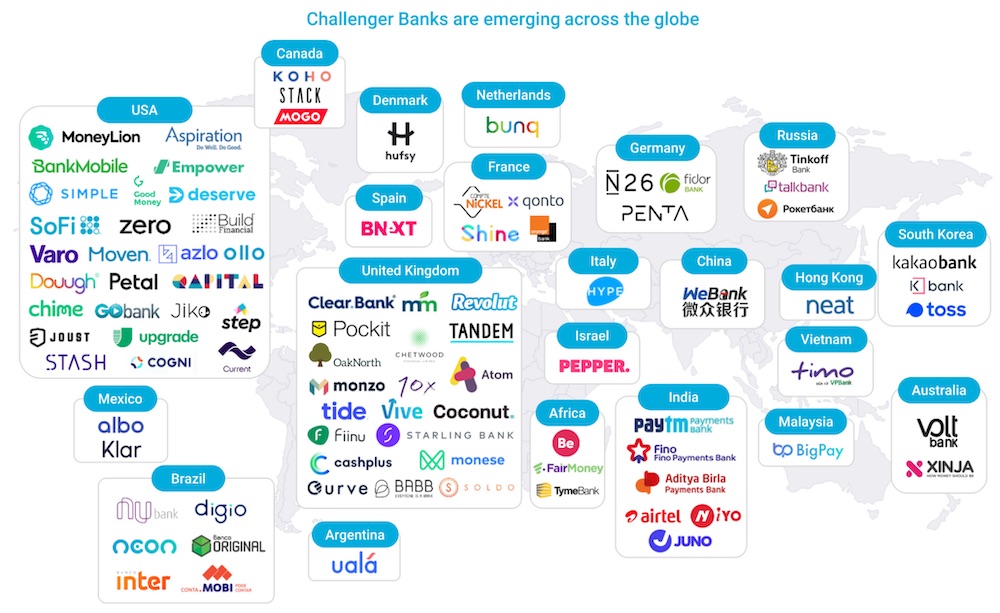

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

Plum, the London and Athens-based fintech that offers a “smart” money management app to help you improve your “financial resilience,” has raised a further $10 million in funding as it gears up for European expansion.

The new round is led by Japan’s Global Brain and the European Bank for Reconstruction and Development, which has participated in previous Plum funding rounds.

In addition, the company has received further funding from early backer VentureFriends, matched by the U.K. taxpayer via the U.K. government’s Future Fund scheme. Plum has raised $19.3 million in total since being founded by Victor Trokoudes (an early TransferWise employee) and Alex Michael in 2016.

Launched in the U.K. the following year, Plum is one of a number of fintech startups that is vying to become a user’s financial hub or control centre, in a way that goes far beyond the first generation of personal finance manager apps and bank account aggregators.

You link the app to your bank account and gain access to a range of functionality, including savings, investments and analysis of your utility bills to help you make better purchasing decisions. Like similar apps, Plum’s “artificial intelligence” also deems what you can afford to save by analysing your bank transactions. It then puts money away each month in the form of round-ups and/or regular savings.

You can open an ISA investment account and invest based on themes, such as only in “ethical companies” or technology. Another related feature is “Splitter,” which, as the name suggests, lets you split your automatic savings between Plum savings pots and investments, selecting the percentage amounts to go into each pot, from 0-100%.

In a call with Trokoudes, he talked me through a few recent Plum updates that he says bring it much closer to fulfilling its financial control centre mission and being a candidate to replace your individual banking apps.

Crucially, you can now link all of your accounts to Plum, whereas previously Plum only let you access a single linked bank account. This gives you “full visibility” of your saving, spending and investments all in a single app.

On the roadmap is also the ability to make payments via Open Banking — and Trokoudes doesn’t rule out a Plum card in the future as a complementary feature with additional benefits, not a core offering, unlike numerous competitors.

More immediately, Plum is launching interest for savers who use Plum to set money aside but don’t want to invest any or all of it. Paid users are being offered an interest rate of 0.6% for instant access savings and 0.75% for 95 days’ notice. Plum users on its free tier can earn 0.35% interest.

Trokoudes explained that there’s also the option to split a percentage of the money put aside automatically, allocating deposits between the new interest-bearing account and Plum-powered investments.

Meanwhile, armed with fresh capital, Plum plans to launch in Spain and France by the end of 2020. The company claims 1 million registered users in the U.K., and now employs more than 60 people split across London, U.K. and Athens, Greece. Trokoudes tells me it will scale up further to 80 employees by the end of 2020 and is aiming for 5 million users across Europe by the end of 2021.

Adds Naoki Kamimaeda, partner and Europe office representative at Global Brain Corporation: “More users have started using fintech apps and personal financial management apps across the globe, to be more efficient and be better off. Among these fintech apps, Plum has a very unique position and very bold ambition to be a partner of individuals to save more money and manage their financial life in an easier and more effective manner.”

Powered by WPeMatico

Zopa, the 15-year-old peer-to-peer lending company, is announcing that it has been awarded its full U.K. bank licence, as it gears up to launch a fixed-term savings account, followed by a credit card.

Dubbed “Zopa Bank,” the new challenger bank will sit alongside its existing peer-to-peer lending business, under Zopa Group, creating what the veteran fintech previously described as the first hybrid peer-to-peer and digital bank offering.

Zopa had provisionally acquired a U.K. bank license in December 2018 “with restrictions,” the first major milestone in the licensing process. The full license, which required Zopa to raise a further £140 million late last year in a round led by IAG Capital in order to meet capital required to become a bank, means it can now launch more widely.

“The Zopa Fixed Term Savings Account offers a competitive rate over 1-5 years at a time when rates are at a historic low,” says the upstart bank. “The account can be opened in as little as 7 minutes online and is protected by the Financial Services Compensation Scheme (FSCS) up to £85,000.”

Next, Zopa says it plans to introduce a credit card in the coming months, which will include “innovative new features designed to put customers in control of their borrowing.”

“The card will address the needs of customers who have had to put up with poor service and unclear pricing from their existing card providers. These new products will sit alongside Zopa’s existing offering of personal and auto loans and investment products,” says Zopa Bank.

Whether or not a new challenger bank, even one with Zopa’s established brand, can cut through the noise this late in the race remains to be seen. The challenger bank space in the U.K. is crowded, to say the least, including burgeoning household names like Monzo and Starling, and to a lesser extent, Tandem, which on the surface looks to be Zopa’s most direct non-legacy competitor.

Powered by WPeMatico

It may have entered the game later than other leading regions such as Europe and North America, but Latin America’s fintech industry is dynamic and growing fast. The sector was recently given a valuation of more than $150 billion and continues to expand year-on-year.

And while the longer-term impact of COVID-19 on the sector is yet to be determined, there’s no doubt that the demand for certain fintech solutions is on the rise. As smaller financial institutions across the region are under pressure to digitize, many are calling on fintechs to help them along this journey. In addition, a number of SMEs are seeking out digital loan services to help them get through the crisis.

The sector’s speedy expansion has meant that regulators in LatAm are under increasing pressure to enact legislation that addresses the murky waters of fintech activity, providing confidence to consumers and investors alike. However, regulation across the region must be careful to not quash innovation, while startups must figure out how to be agile in an environment which is becoming increasingly regulated. Let’s take a closer look at what impact regulation has had so far in LatAm, and what needs to happen to strike a balance between sector growth and public trust.

Mexico is currently leading the way when it comes to fintech regulation in LatAm, thanks to its comprehensive 2018 fintech Law. The law covers most fintech activities, including crowdfunding, virtual wallet, transactions carried out with cryptocurrencies and open banking. In addition, Mexico has certain financial laws that regulate financial entities in their execution of transactions using fintech. The law also provides a regulatory sandbox for both licensed and non-licensed companies.

Brazil is the furthest ahead after Mexico, as it individually legislates crowdfunding and peer-to-peer lending, while a special congressional commission is working on a broader legislative strategy. Brazil’s Central Bank also endeavors to make open banking legislation effective by the third quarter of 2020, which will pave the way for a thriving open banking ecosystem.

Powered by WPeMatico

Small and medium businesses and sole-traders account for the vast majority of businesses globally, 99.9% of all enterprises in the U.K. alone. And while the existence of millions of separate companies, with their individual demands, speaks of a fragmented market, together they still represent a lot of opportunity. Today, a U.K. fintech startup looking to capitalise on that is announcing a round of growth funding to enter Europe after onboarding 20,000 customers in its home country.

ANNA, a mobile-first banking, tax accounting and financial service assistant aimed at small and medium businesses and freelancers, has closed a $21 million round of investment from a single investor, the ABHH Group, the sometimes controversial owner of Alfa Bank in Russia, the Amsterdam Trade Bank in the Netherlands and other businesses.

The investment is a strategic one: ANNA will be using the funding to expand for the first time outside of the U.K. into Europe, and CEO Eduard Panteleev said that effort will be built on Amsterdam Trade Bank’s rails. He confirmed that the investment values ANNA at $110 million, and the founders keep control of 40% of the company in the deal.

The fundraising started before COVID-19 really picked up speed, but its chilling effect on the economy has also had a direct impact on the very businesses that ANNA targets as customers: some have seen drastic reductions in commercial activity, and some have shuttered their businesses altogether.

Despite this, the situation hasn’t changed measurably for ANNA, Panteleev said.

“COVID-19 hasn’t impacted us so far. We are designed as a digital business, and so working from home was a completely normal shift for us to make,” he said, but added that when it comes to the customers, “Yes, we have seen that our customers’ incoming payments are quite affected, with 15-30% decrease in the volume of customer payments.” The firm belief that ANNA and investors have, however, is that business will bounce back, and ANNA wants to make sure it’s in a strong position when it does.

ANNA is an acronym for “Absolutely No Nonsense Admin,” and that explains the gist of what it aims to do: it provides an all-in-one service for smaller enterprises that lets them run a business account to make and receive payments, along with software for invoicing, accounting and managing taxes that is run through a chat interface to assist you and automate some of the functions (like invoice tracking). ANNA also offers additional services, such as connecting you to a live accountant during tax season.

ANNA is part of a wave of fintech startups that have cropped up in the last several years specifically targeting SMEs .

It used to be the case that SMEs and freelancers were drastically underserved in the world of financial services: their business, even collectively, is not as lucrative as accounts from larger enterprises, and therefore there was little innovation or attention paid to how to improve their experience or offerings, and so whatever traditional banks had to offer was what they got.

All that changed with the rise of “fintech” as a salient category: ever-smarter smartphones and app usage are now ubiquitous, broadband is inexpensive and also widespread, cloud and other technology has turbo charged what people can do on their devices and people are just more digitally savvy. And many startups have taken advantage of all that to develop fintech services catering to SMEs, which also has meant competition from the likes of Monzo, Revolut, Tide and now even offerings from high-street banks like NatWest.

Panteleev believes ANNA’s product stands separate from these. “We offer more of a financial assistant to users, rather than just moving their money, and it’s also a different business case, because we look at what a user needs more holistically,” he said. Pricing is also a little different: businesses with monthly income of less than $500 can use ANNA for free. It then goes up on a sliding scale to a maximum of £19.90 per month, for those with monthly income between £20,000 and £500,000.

Panteleev — who co-founded the company with Andrey Pachay, Boris Dyakonov, Daljit Singh, Nikita Filippov and Slava Akulov — is a repeat entrepreneur, having founded two other banking startups in Russia with Dyakonov that are still going: Knopka (Russian for button) and Totchka (Russian for dot). These are older and more established: Totchka for example has some 500,000 users, but Panteleev has said there are no plans to try to bring ANNA into the Russian market, nor take these other companies international.

For ABHH, the attraction of investing in this particular startup was probably two-fold. The businesses have Russian DNA in common, making for potentially a better cultural fit, but also it is yet another example of a legacy, large bank tapping into a smaller and more fleet-of-foot startup to address a market sector that the bigger company might be more challenged to do alone.

“I’m looking forward to embarking on this exciting journey together,” said Alan Vaksman, member of the supervisory board at Amsterdam Trade Bank and future chairman of ANNA, in a statement. “At this moment most SMEs find themselves in a challenging situation; however, once the pandemic comes to an end, there will be a very clear realisation that neither corporates nor family businesses can afford to run most operational processes manually. Tech services and platforms, like ANNA, are in for some dynamic times ahead.”

Powered by WPeMatico

The economic effects of COVID-19 could delay Africa’s next big IPO — that of Nigerian fintech unicorn Interswitch.

If so, it wouldn’t be the first time the Lagos-based payments company’s plans for going public were postponed; the tech world has been anticipating Interswitch’s stock market debut since 2016.

For the continent’s innovation ecosystem, there’s a lot riding on the digital finance company’s IPO. After e-commerce venture Jumia, it would become only the second listing of a VC-backed African tech company on a major exchange. And Interswitch’s stock market debut — when it occurs — could bring more investor attention and less controversy to the region’s startup scene.

TechCrunch reached out to Interswitch on the window for listing, but the company declined to comment. The tech firm’s path from startup to IPO aspirant traces back to the vision of founder Mitchell Elegbe, a Nigerian electrical engineering graduate whose entire career has pretty much been Interswitch.

Africa’s tech scene is still fairly young, but it does have a timeline with several definitive points. An early one would be the success of mobile money in East Africa, with the launch of Safaricom’s M-Pesa in 2007. Another is the notable wave of VC-backed startups and founders that launched around 2010.

Interswitch CEO Mitchell Elegbe (Photo Credits: Interswitch)

With Interswtich, Elegbe pre-dated both by a number of years, founding his fintech company back in 2002 to connect Nigeria’s largely disconnected banking system. The firm became a pioneer of the infrastructure to digitize Nigeria’s economy.

Interswitch created the first electronic switch whereby Nigerian financial institutions could communicate and thereby operate ATMs and point of sales operations. The company now provides much of the rails for Nigeria’s online banking system.

Powered by WPeMatico

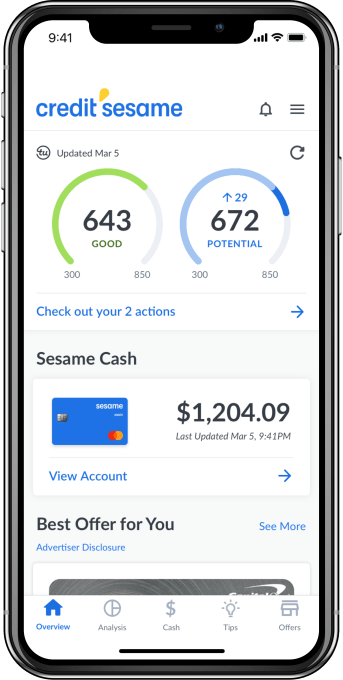

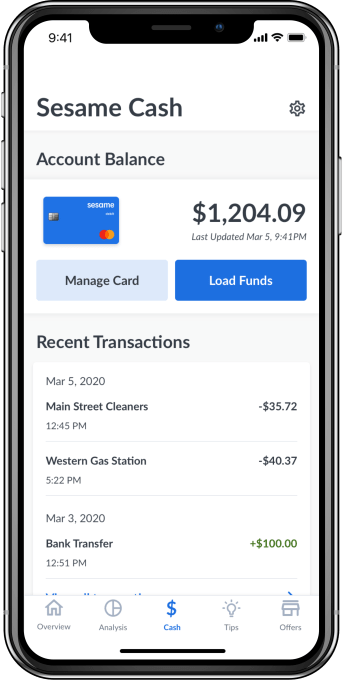

Credit Sesame is getting into digital banking. The credit and loans company, first launched at TechCrunch Disrupt in 2010, has since grown to 15 million registered users and, in 2016, achieved profitability. To date, its focus has been on helping consumers achieve financial health by taking steps to consolidate debt and raise their credit score. Now, it’s expanding to include digital banking, but with the goal of using its better understanding of its banking customers’ finances to better personalize its credit improvement recommendations.

The new service, Sesame Cash, has many features found in other challenger banking apps, like a general lack of fees, real-time notifications, an early payday option, free access to a sizable ATM network, in-app debit card management and more. Specifically, Credit Sesame says it won’t charge monthly fees or overdraft fees, and it provides free access to more than 55,000 ATMs and a no-fee debit card from Mastercard.

However, the banking app also serves a secondary purpose beyond its plan to take on traditional banks. Because the company has insights into users’ finances and repayment abilities, it will be able to offer personalized recommendations, including those for relevant credit products from its hundreds of financial institution partners.

However, the banking app also serves a secondary purpose beyond its plan to take on traditional banks. Because the company has insights into users’ finances and repayment abilities, it will be able to offer personalized recommendations, including those for relevant credit products from its hundreds of financial institution partners.

Other features also differentiate Sesame Cash from rival challenger banks, including built-in access to view your daily credit score and a system that rewards consumers with cash incentives — up to $100 per month — for credit score improvements. The banking app includes $1 million in credit and identity theft protection, as well.

In the months following its launch, the company is planning to introduce a smart bill pay service that manages cash to improve credit and lower interest rates on credit balances, plus an auto-savings feature that works by rounding up transactions, a rewards program for everyday purchases and other smart budgeting tools.

“Through the use of advanced machine learning and AI, we’ve helped millions of consumers improve and manage their credit. However, we identified the disconnect between consumers’ cash and credit—how much cash you have, and how and when you use your cash has an impact on your credit health,” said Adrian Nazari, Credit Sesame Founder and CEO, in a statement. “With Sesame Cash, we are now bridging that gap and unlocking a whole new set of benefits and capabilities in a new product category. This underscores our mission and commitment to innovation and financial inclusion, and the importance we place in working with partners who share the same ethos,” he added.

Credit Sesame today caters to consumers interested in bettering their credit. The company says 61% of its members see credit score improvements within their first six months, and 50% see scores improve by more than 10 points during that time. Indeed, 20% see their score improve by more than 50 points during the first six months.

But one challenge Credit Sesame faces is that after consumers reach their goals, credit-wise, they may become less engaged with the Credit Sesame platform. The new banking app changes that, by allowing the company to maintain a relationship with customers over time.

But one challenge Credit Sesame faces is that after consumers reach their goals, credit-wise, they may become less engaged with the Credit Sesame platform. The new banking app changes that, by allowing the company to maintain a relationship with customers over time.

Credit Sesame is a smaller version of Credit Karma, which was recently acquired by Intuit for $7 billion. Since then, it has been rumored to be another potential acquisition target for Intuit, if it didn’t proceed to go public. The banking service would make Credit Sesame more attractive to a potential acquirer, if that’s the case, as it would offer something Credit Karma did not.

The company says Sesame Cash bank accounts are held with Community Federal Savings Bank, Member FDIC.

The banking service will initially be made available to existing customers, before becoming available to the general public. The Credit Sesame mobile app is a free download for iPhone and Android.

Powered by WPeMatico