Banking

Auto Added by WPeMatico

Auto Added by WPeMatico

Business, now more than ever before, is going digital, and today a startup that’s building a vertically integrated solution to meet business banking needs is announcing a big round of funding to tap into the opportunity. Airwallex — which provides business banking services directly to businesses themselves as well as via a set of APIs that power other companies’ fintech products — has raised $200 million, a Series E round of funding that values the Australian startup at $4 billion.

Lone Pine Capital is leading the round, with new backers G Squared and Vetamer Capital Management, and previous backers 1835i Ventures (formerly ANZi), DST Global, Salesforce Ventures and Sequoia Capital China also participating.

The funding brings the total raised by Airwallex — which has head offices in Hong Kong and Melbourne, Australia — to $700 million, including a $100 million injection that closed out its Series D just six months ago.

Airwallex will be using the funding both to continue investing in its product and technology as well as to continue its geographical expansion and to focus on some larger business targets. The company has started to make some headway into Europe and the U.K. and that will be one big focus, along with the U.S.

The quick succession of funding and rising valuation underscore Airwallex’s traction to date around what CEO and co-founder Jack Zhang describes as a vertically integrated strategy.

That involves two parts. First, Airwallex has built all the infrastructure for the business banking services that it provides directly to businesses with a focus on small and medium enterprise customers. Second, it has packaged up that infrastructure into a set of APIs that a variety of other companies use to provide financial services directly to their customers without needing to build those services themselves — the so-called “embedded finance” approach.

“We want to own the whole ecosystem,” Zhang said to me. “We want to be like the Apple of business finance.”

That seems to be working out so far for Airwallex. Revenues were up almost 150% for the first half of 2021 compared to a year before, with the company processing more than US$20 billion for a global client portfolio that has quadrupled in size. In addition to tens of thousands of SMEs, it also, via APIs, powers financial services for other companies like GOAT, Papaya Global and Stake.

Airwallex got its start like many of the strongest startups do: It was built to solve a problem that the founders encountered themselves. In the case of Airwallex, Zhang tells me he had actually been working on a previous startup idea. He wanted to build the “Blue Bottle Coffee” of Asia Pacific out of Australia, and it involved buying and importing a lot of different materials, packaging and, of course, coffee from all around the world.

“We found that making payments as a small business was slow and expensive,” he said, since it involved banks in different countries and different banking systems, manual efforts to transfer money between them and many days to clear the payments. “But that was also my background — payments and trading — and so I decided that it was a much more fascinating problem for me to work on and resolve.”

Eventually one of his co-founders in the coffee effort came along, with the four co-founders of Airwallex ultimately including Zhang, along with Xijing Dai, Lucy Liu and Max Li.

It was 2014, and Airwallex got attention from VCs early on in part for being in the right place at the right time. A wave of startups building financial services for SMBs were definitely gaining ground in North America and Europe, filling a long-neglected hole in the technology universe, but there was almost nothing of the sort in the Asia Pacific region, and in those earlier days solutions were highly regionalized.

From there it was a no-brainer that starting with cross-border payments, the first thing Airwallex tackled, would soon grow into a wider suite of banking services involving payments and other cross-border banking services.

“In the last six years, we’ve built more than 50 bank integrations and now offer payments across 95 countries, payments through a partner network,” he added, with 43 of those offering real-time transactions. From that, it moved on to bank accounts and “other primitive stuff” with card issuance and more, he said, eventually building an end-to-end payment stack.

Airwallex has tens of thousands of customers using its financial services directly, and they make up about 40% of its revenues today. The rest is the interesting turn the company decided to take to expand its business.

Airwallex had built all of its technology from the ground up itself, and it found that — given the wave of new companies looking for more ways to engage customers and become their one-stop shop — there was an opportunity to package that tech up in a set of APIs and sell that on to a different set of customers, those who also provided services for small businesses. That part of the business now accounts for 60% of Airwallex’s business, Zhang said, and is growing faster in terms of revenues. (The SMB business is growing faster in terms of customers, he said.)

A lot of embedded finance startups that base their business around building tech to power other businesses tend to stay at arm’s length from offering financial services directly to consumers. The explanation I have heard is that they do not wish to compete against their customers. Zhang said that Airwallex takes a different approach, by being selective about the customers they partner with, so that the financial services they offer would not be in direct competition with those of its customers. The GOAT marketplace for sneakers, or Papaya Global’s HR platform are classic examples of this.

However, as Airwallex continues to grow, you can’t help but wonder whether one of those partners might like to gobble up all of Airwallex and take on some of that service provision role itself. In that context, it’s very interesting to see Salesforce Ventures returning to invest even more in the company in this round, given how widely the company has expanded from its early roots in software for salespeople into a massive platform providing a huge range of cloud services to help people run their businesses.

For now, it’s been the combination of its unique roots in Asia Pacific, plus its vertical approach of building its tech from the ground up, plus its retail acumen that has impressed investors and may well see Airwallex stay independent and grow for some time to come.

“Airwallex has a clear competitive advantage in the digital payments market,” said David Craver, MD at Lone Pine Capital, in a statement. “Its unique Asia-Pacific roots, coupled with its innovative infrastructure, products and services, speak volumes about the business’ global growth opportunities and its impressive expansion in the competitive payment providers space. We are excited to invest in Airwallex at this dynamic time, and look forward to helping drive the company’s expansion and success worldwide.”

Updated to note that the coffee business was in Australia, not Hong Kong.

Powered by WPeMatico

SellersFunding secured $166.5 million in a combination of Series A equity funding and a credit facility to continue developing its technology and payments platforms for e-commerce businesses.

Northzone led the round and was joined by Endeavor Catalyst and Fasanara. SellersFunding CEO Ricardo Pero did not disclose the funding breakdown, but did say the company previously raised two seed rounds for a total of $40 million in equity and more than $100 million in credit facilities, including one that the company was expanding to $200 million.

SellersFunding, with offices in Florida, New York and London, created a digital platform that delivers financial tools and resources to streamline global commerce for thousands of marketplaces, including working capital, cross-border cash management, tax solutions and business valuation.

Pero got the idea for the company after spending 20 years in the financial industry. He left JP Morgan in 2016 with a drive to start his own company. He was consulting for a friend selling on Amazon who asked him to help make sense of Amazon’s fees and to review the next year’s budget because the friend was struggling to keep up with growth.

“I helped him address the fees issue, but when I went to talk to traditional lenders, I found that they have no clue about e-commerce and the needs of SMEs,” he said.

In addition to being a lending source for businesses selling on these marketplaces, SellersFunding leverages sales data provided by the marketplaces and e-commerce platforms to create sales and cash flow estimates based on the credit limits given to clients so that owners can better understand the fees they are paying and make more informed decisions.

He founded the company in 2017, and today has over 30,000 registered users and is approaching $10 billion in sales volume that is feeding data into SellersFunding’s daily models. The company makes money as both a lender and on fees it charges for payments collected by its customers. Merchants can collect money from marketplaces and pay their suppliers in local or foreign currency.

SellersFunding has consistently grown 300% year over year, Pero said. As such, he intends to use the new funding to scale globally, expand the team, create a marketing budget and look for two small acquisitions in the U.S. and Europe.

The company will continue to invest on the payments side and to promote cross-border payments.

“When I look at the payments landscape, companies are competing on pricing and I don’t think we will ever have a focus there, but instead will compete on customer experience,” Pero added. “Our core business will always be lending and our core investments will be payments and technology, but then we will extend to other services that our clients want.”

With an eye on expanding internationally, it fit to bring on Northzone as a partner, he added. The venture firm is based in Europe and was of a similar vision for thinking globally.

Jeppe Zink, general partner at Northzone, said via email that Pero and his team “are the most experienced in this category” and are building a category leader that is “more experienced and understanding of the lending side than its competitors.”

“We have seen this massive rise in e-shopping, most of the new ones coming from marketplaces like Amazon and Shopify, and if you look at the sellers, thousands are small businesses sourcing their goods which means that they are very important customers,” Zink added. “Normal banks like Barclay can’t check credit. SellersFinding is helping small businesses get this credit, and rightly so. In the same way we thought neobanks won with accounts created when it comes to delivering credit and banking products, they are nowhere to be found yet.”

Powered by WPeMatico

A Canadian startup called Nuula that is aiming to build a super app to provide a range of financial services to small and medium businesses has closed $120 million of funding, money that it will use to fuel the launch of its app and first product, a line of credit for its users.

The money is coming in the form of $20 million in equity from Edison Partners, and a $100 million credit facility from funds managed by the Credit Group of Ares Management Corporation.

The Nuula app has been in a limited beta since June of this year. The plan is to open it up to general availability soon, while also gradually bringing in more services, some built directly by Nuula itself but many others following an embedded finance strategy: business banking, for example, will be a service provided by a third party and integrated closely into the Nuula app to be launched early in 2022. Alongside that, the startup will also be making liberal use of APIs to bring in other white-label services, such as B2B and customer-focused payment services, starting first in the U.S. and then expanding to Canada and the U.K. before expanding further into countries across Europe.

Current products include cash flow forecasting, personal and business credit score monitoring, and customer sentiment tracking; and monitoring of other critical metrics including financial, payments and e-commerce data are all on the roadmap.

“We’re building tools to work in a complementary fashion in the app,” CEO Mark Ruddock said in an interview. “Today, businesses can project if they are likely to run out of money, and monitor their credit scores. We keep an eye on customers and what they are saying in real time. We think it’s necessary to surface for SMBs the metrics that they might have needed to get from multiple apps, all in one place.”

Nuula was originally a side-project at BFS, a company that focused on small business lending, where the company started to look at the idea of how to better leverage data to build out a wider set of services addressing the same segment of the market. BFS grew to be a substantial business in its own right (and it had raised its own money to that end, to the tune of $184 million from Edison and Honeywell). Over time, it became apparent to management that the data aspect, and this concept of a super app, would be key to how to grow the business, and so it pivoted and rebranded earlier this year, launching the beta of the app after that.

Nuula’s ambitions fall within a bigger trend in the market. Small and medium enterprises have shaped up to be a huge business opportunity in the world of fintech in the last several years. Long ignored in favor of building solutions either for the giant consumer market, or the lucrative large enterprise sector, SMBs have proven that they want and are willing to invest in better and newer technology to run their businesses, and that’s leading to a rush of startups and bigger tech companies bringing services to the market to cater to that.

Super apps are also a big area of interest in the world of fintech, although up to now a lot of what we’ve heard about in that area has been aimed at consumers — just the kind of innovation rut that Nuula is trying to get moving.

“Despite the growth in services addressing the SMB sector, overall it still lacks innovation compared to consumer or enterprise services,” Ruddock said. “We thought there was some opportunity to bring new thinking to the space. We see this as the app that SMBs will want to use everyday, because we’ll provide useful tools, insights and capital to power their businesses.”

Nuula’s priority to build the data services that connect all of this together is very much in keeping with how a lot of neobanks are also developing services and investing in what they see as their unique selling point. The theory goes like this: banking services are, at the end of the day, the same everywhere you go, and therefore commoditized, and so the more unique value-added for companies will come from innovating with more interesting algorithms and other data-based insights and analytics to give more power to their users to make the best use of what they have at their disposal.

It will not be alone in addressing that market. Others building fintech for SMBs include Selina, ANNA, Amex’s Kabbage (an early mover in using big data to help loan money to SMBs and build other financial services for them), Novo, Atom Bank, Xepelin and Liberis, biggies like Stripe, Square and PayPal, and many others.

The credit product that Nuula has built so far is a taster of how it hopes to be a useful tool for SMBs, not just another place to get money or manage it. It’s not a direct loaning service, but rather something that is closely linked to monitoring a customers’ incomings and outgoings and only prompts a credit line (which directly links into the users’ account, wherever it is) when it appears that it might be needed.

“Innovations in financial technology have largely democratized who can become the next big player in small business finance,” added Gary Golding, General Partner, Edison Partners. “By combining critical financial performance tools and insights into a single interface, Nuula represents a new class of financial services technology for small business, and we are excited by the potential of the firm.”

“We are excited to be working with Nuula as they build a unique financial services resource for small businesses and entrepreneurs,” said Jeffrey Kramer, Partner and Head of ABS in the Alternative Credit strategy of the Ares Credit Group, in a statement. “The evolution of financial technology continues to open opportunities for innovation and the emergence of new industry participants. We look forward to seeing Nuula’s experienced team of technologists, data scientists and financial service veterans bring a new generation of small business financial services solutions to market.”

Powered by WPeMatico

Oh, how the tables have turned.

It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry.

It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry.

But lately, fintech upstarts are the ones doing the acquiring. Over just the last year or so, we’ve seen:

So what’s going on here? Why are fintechs now acquiring legacy financial services businesses, instead of the other way around?

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Lower, an Ohio-based home finance platform, announced today it has raised $100 million in a Series A funding round led by Accel.

This round is notable for a number of reasons. First off, it’s a large Series A even by today’s standards. The financing also marks the previously bootstrapped Lower’s first external round of funding in its seven-year history. Lower is also something that is kind of rare these days in the startup world: profitable. Silicon Valley-based Accel has a history of backing profitable, bootstrapped companies, having also led large Series A rounds for the likes of 1Password, Atlassian, Qualtrics, Webflow, Tenable and Galileo (which went on to be acquired by SoFi).

In fact, Galileo founder Clay Wilkes introduced the VC firm to Dan Snyder, Lower’s founder and CEO. The two companies have a few things in common besides being profitable: they were both bootstrapped for years before taking institutional capital and both have headquarters outside of Silicon Valley.

“We were immediately intrigued because Ohio-based Lower echoes both of these themes,” said Accel partner John Locke, who led the firm’s investment in Lower and is taking a seat on the company’s board as part of the investment. “Like Galileo, Lower will be one of the most successful bootstrapped fintech companies globally. The combination of a company built in a nontraditional region across the globe and a bootstrapped company reminds us of [other] companies we have partnered with for a large Series A.”

There were other unnamed participants in the round, but Accel provided the “majority” of the investment, according to Lower.

Snyder co-founded Lower in 2014 with the goal of making the home-buying process simpler for consumers. The company launched with Homeside, its retail brand that Snyder describes as “a tech-leveraged retail mortgage bank” that works with realtors and builders, among others.

In 2018, the company launched the website for Lower, its direct-to-consumer digital lending brand with the mission of making its platform a one-stop shop where consumers can go online to save for a home, obtain or refinance a mortgage and get insurance through its marketplace. This year, it launched the Lower mobile app with a savings account.

Sitting (L to R): Co-founders Dan Snyder, Grayson Hanes

Standing (L to R): Co-founders Mike Baynes, Chris Miller

Not pictured: Robert Tyson; Image credit: Lower

Over the years, Lower has funded billions of dollars in loans and notched an impressive $300 million in revenue in 2020 after doubling revenue every year, according to Snyder.

“Our history is maybe a little atypical of fintech companies today,” he told TechCrunch. “We’ve had a view going back to the start of the company that we wanted to run it profitably. That’s been one of our pillars, so that’s what we’ve done. Also, we all grew up in the mortgage industry, so we saw firsthand the size of the market, but also how broken it was, so we wanted to change it.”

In launching the direct-to-consumer digital lending brand, the company was working to make the homebuying process more “digital, transparent and easier for consumers to access,” Snyder said.

At the same time, the company didn’t want to lose the human touch.

“We tried to design the app flow in a way where you can get as far along as you can in the application but if you want, at any point in time, to talk or chat with someone, we’re available,” Snyder added.

Image Credits: Lower

Lower’s typical customer is the millennial and now Gen Z who’s aspiring to own their first home, according to Snyder.

“They might be thinking, ‘OK, I might be living in an apartment now, but in the next few years I’m going to meet someone and/or have a child and I want to unlock the investment that is a home,’” he told TechCrunch. “And we’ll help them on that journey.”

Lower’s recently launched new app offers a deposit account it’s dubbed “HomeFund.” The interest-bearing, FDIC-insured deposit account offers a 0.75% Annual Percentage Yield and is designed to help consumers save for a home with a “dollar-for-dollar match in rewards” up to the first $1,000 saved, Snyder said.

Lower works with more than 35 major insurance carriers nationally, including Nationwide, Liberty Mutual and Allstate. It has more than 1,600 employees, about half of which are based in Lower’s home state. That’s up from about 650 employees in June of 2020.

Looking ahead, the company plans to add more services and has an “aggressive roadmap” for adding new features to its platform. Today, for example, Lower sells primarily to Fannie Mae and Freddie Mac. And while it services the majority of its loans, like many large lenders, it uses a subservicer. That will change, however, in early 2022, when Lower intends to launch its own native servicing platform.

And while the company intends to continue to run profitably, Snyder said he and his co-founders “think the time is now to gain share.”

“We want to become a global brand, raise money and gain market share,” he added. “We’re going to continue to double down on product and build out our capabilities. We are the best-kept secret in fintech and plan to change that with smart branding, advertising and sponsorships.”

And last but not least, Lower is eyeing the public markets as part of its longer-term roadmap.

“Ultimately, we know we can build a great public company,” Snyder told TechCrunch. “We’re of the scale to be a public company right now, but we’re going to keep our heads down and we’re going to keep building for the next few years and then I think we can be in a spot to be a strong public business.”

Accel’s Locke points out that in the U.S., mortgage and home finance are among the largest financial service markets, and they have primarily been handled by large banks.

“For most consumers, getting a mortgage through these banks continues to be an overly complex, slow-moving process,” Locke told TechCrunch. “We believe by providing consumers a great mobile experience, Lower will gain share from incumbent banks, in the same way that companies like Monzo have in banking or Venmo in payments or Trade Republic and Robinhood in stock trading.”

Powered by WPeMatico

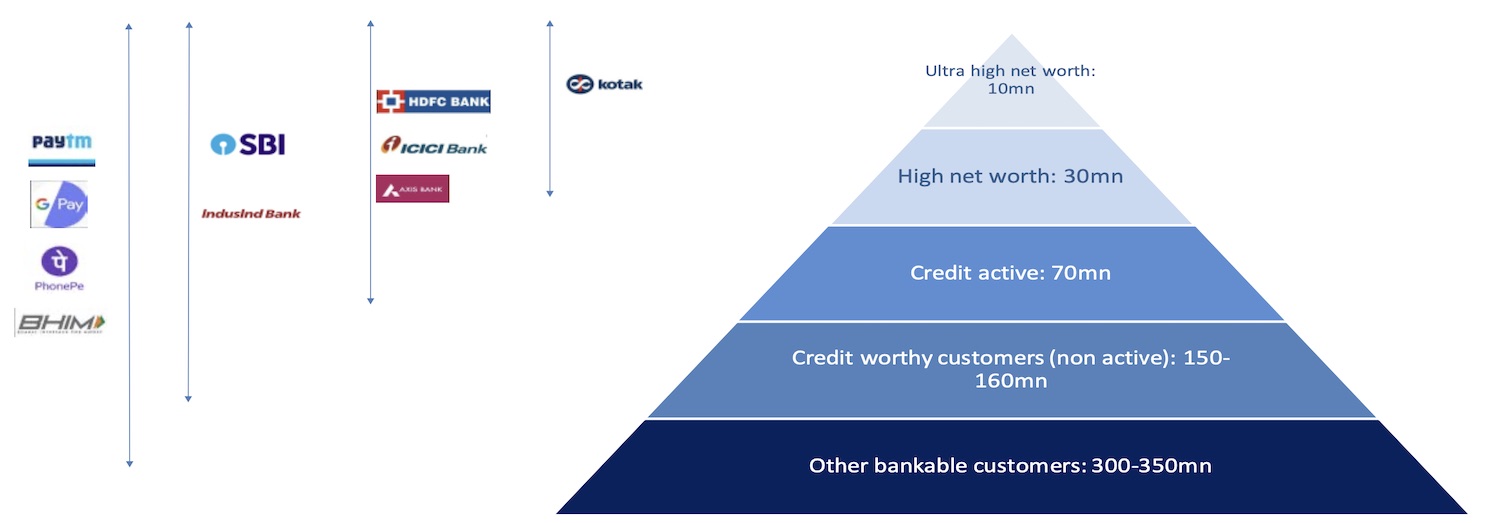

For most people in India, having to engage with banks doesn’t instill a sense of joy. Banks in the South Asian market are notorious for making unannounced spam calls to upsell customers loans and credit cards, even when they have been explicitly asked not to do so.

Moreover, when a customer does reach out to a bank with a query, it can take forever to get the job done. Take ICICI Bank, India’s third largest bank and until recently my only banking partner for over six years, for an example.

It is now in its third month in figuring out who exactly in its relationship with Amazon is supposed to re-issue me a credit card. I have moved on with my life, and it looks like they did, too, likely before they even looked at my query.

Small and medium-sized businesses aren’t a big fan of banks, either. If you operate an early-stage startup, it’s anyone’s guess if you will ever be able to convince a bank to issue you a corporate account. So of course, startups — Razorpay and Open — took it upon themselves to fix this experience.

For consumers, too, in recent years, scores of startups have arrived on the scene to improve this banking experience. Whether you are a teenager, or just out of college, or a working professional, or don’t have a credit score, there are firms that can get you a credit card and loan.

But even these services have a ceiling limit of some sort. And customers aren’t loyal to any startup.

“A customer’s relationship is always with the entity where they park their savings deposit,” said Jitendra Gupta, a high-profile entrepreneur who has spent a decade in the fintech world. Since these customers are not parking their money with fintech, “the startups have been unable to disrupt the bank. That’s the hard reality.”

So what’s the alternative? Gupta, who co-founded CitrusPay (sold to Naspers’ PayU) and served as managing director of PayU, has been thinking about these challenges for more than two years.

“If you really want to change the banking industry, you cannot operate from the side. You have to fight from the centre, where they deposit their money. It’s a very time-consuming process and requires a lot of initial capital and experience with banks,” he told TechCrunch in an interview.

After more than a year and a half of raising about $24 million — from Sequoia Capital India, 3one4 Capital, Amrish Rau, Kunal Shah, Kunal Bahl, Tanglin Venture Partners, Rainmatter and others — Gupta is ready to launch what he believes will address a lot of the issues individuals face with their banks.

His new startup, called Jupiter, wants to bring “delight” to the banking experience, and it will launch in India on Thursday.

“We believe that a bank account should be a smart account, where it gives you insight, shares personalized tips and guides you through attaining some financial discipline,” he said.

A snapshot of the reach of banks and fintech startups in India. Data: CIBIL, Statista, BofA Global Research. Image: BofA

To be sure, Jupiter, too, will offer loans and other financial services to customers. But instead of making irrelevant calls to customers, it will assess which of its customers are running short on money and give the option to take a credit line from its app itself, he said. “The upsell doesn’t need to happen by way of spam. It needs to happen by way of contextualization and personalization.”

“Jupiter has been built in a deep integration with the underlying bank, allowing the consumer to have a frictionless experience for all their banking needs,” said Amrish Rau, chief executive of Pine Labs, co-founder of CitrusPay and longtime friend of Gupta.

The startup, which employs 115 people, has developed a number of products for customers joining on day one. The products include the ability to buy now and pay later on UPI, a feature first offered in the market by Jupiter, and a mutual fund portfolio analyzer. A debit card, in-app chat with a customer service agent, expense categorisation, finding the right card, determining the existing health insurance coverage, and more are ready to ship, the startup said.

Jupiter is currently working on providing zero mark-up on forex transactions, and frictionless two-factor authentication. The startup has published a public Trello page where it has outlined the features it is working on and when it expects to ship them, as well as features suggested by its beta-testing customers. “I want to establish full transparency in what we are working on to build trust with customers,” said Gupta.

Jupiter will have its own customer relationship team that will engage with the startup’s users. The startup, which last month opened a waiting list for customers to sign up, had amassed more than 25,000 applications as of two weeks ago.

Even Jupiter, which one day wishes to disrupt the banking sector, currently has to partner with banks. Its partners are Federal Bank and Axis Bank.

I asked Gupta about the excitement his investors see in Jupiter. “Everyone believes, as you see with fintech giants such as Nubank globally, that we will become a full bank,” he said.

But for the time being, Gupta said he is not looking to partner with more banks. “I don’t want Jupiter to attract customers because they want to bank with Federal or Axis. I want them to come to Jupiter because they want to bank with Jupiter,” he said.

In the next 12 months, the startup hopes to serve more than 1 million customers.

Powered by WPeMatico

Small businesses have traditionally been underserved when it comes to IT — they are too big and have too many requirements that can’t be met by consumer products, yet are much too small to afford, implement or thoroughly need apps and other IT build for larger enterprises. But when it comes to neobanks, it feels like there is no shortage of options for the SMB market, nor venture funding being invested to help them grow.

In the latest development, Novo, a neobank that has built a service targeting small businesses, has closed a round of $40.7 million, a Series A that it will be using to continue growing its business, and its platform.

The funding is being led by Valar Ventures with Crosslink Capital, Rainfall Ventures, Red Sea Ventures and BoxGroup all participating. The startup is not disclosing valuation, but Novo — originally founded in New York in 2018 but now based out of Miami — has racked up 100,000 SMB customers — which it defines as businesses that make between $25,000 and $100,000 in annualized revenues — and has seen $1 billion in lifetime transactions, with growth accelerating in the last couple of years.

There are a wide variety of options for small businesses these days when it comes to going for a banking solution. They include staying with traditional banks (which are starting to add an increasing number of services and perks to retain small business customers), as well as a variety of fintechs — other neobanks, like Novo — that are building banking and related financial tools to cater to startups and other small businesses.

Just doing a quick search, some of the others targeting the sector include Rho, NorthOne, Lili, Mercury, Brex, Hatch, Anna, Tide, Viva Wallet, Open and many more (and you could argue also players like Amazon, offering other money management and spending tools similar to what neobanks are providing). Some of these are not in the U.S., and some are geared more at startups, or freelancers, but taken together they speak to the opportunity and also the attention that it is getting from the tech industry right now.

As CEO and co-founder Michael Rangel — who hails from Miami — described it to me, one of the key differentiators with Novo is that it’s approaching SMB banking from the point of view of running a small business. By this, he means that typically SMBs are already using a lot of other finance software — on average seven apps per business — to manage their books, payments and other matters, and so Novo has made it easier by way of a “drag and drop” dashboard where an SMB can integrate and view activity across all of those apps in one place. There are “dozens” of integrations currently, he said, and more are being added.

This is the first step, he said. The plan is to build more technology so that the activity between different apps can also be monitored, and potentially automated

“We’re able to see this is your balance and what you should expect,” he said. “The next frontier is to marry the incoming with outgoing. We’re using the funding to build that, and it’s on the roadmap in the next six months.”

Novo has yet to bring cash advances or other lending products into its platform, although those too are on the roadmap, but it is also listening to its customers and watching what they want to do on the platform — another reason why it’s clever to make it easy to for those customers to integrate other services into Novo: not only does that solve a pain point for the customer, but it becomes a pretty clear indicator of what customers are doing, and how you could better cater to that.

Listening to the customers is in itself becoming a happy challenge, it seems. Novo launched quietly enough — between 2018 and the end of 2019, it had picked up only 5,000 accounts. But all that changed during 2020 and the COVID-19 pandemic, which Rangel describes as “just hockey stick growth. We grew like crazy.”

The reason, he said, is a classic example of why incumbent banks have to catch up with the times. Everyone was locked down at home, and suddenly a lot of people who were either furloughed or laid off were “spinning up businesses,” he said, and that led to many of them needing to open bank accounts. But those who tried to do this with high-street banks were met with a pretty significant barrier: you had to go into the bank in person to authenticate yourself, but either the banks were closed, or people didn’t want to travel to them. That paved the way for Novo (and others) to cater to them.

Its customer numbers shot up to 24,000 in the year.

Then other market forces have also helped it. You might recall that banking app Simple was shut down by BBVA ahead of its merger with PNC; but at the same time, it also shut down Azlo, it’s small business banking service. That led to a significant number of users migrating to other services, and Novo got a huge windfall out of that, too.

In the last six months, Novo grew four-fold, and Rangel attributed a lot of that to ex-Azloans looking for a new home.

The fact that there are so many SMB banking providers out there might mean competition, but it also means fragmentation, and so if a startup emerges that seems to be catching on, it’s going to catch something else, too: the eye of investors.

“The ability of the Novo team to grow the company rapidly during a year where businesses have faced unprecedented challenges is impressive,” said Andrew McCormack, founding partner at Valar Ventures, the firm co-founded by Peter Thiel, another big figure in fintech. “Novo tripled its small business customer base in the first half of 2021! Their custom infrastructure and banking platform put them in prime position to expand their services at an even faster pace as we come out of the health crisis. All of us at Valar Ventures are excited to join this team.”

Powered by WPeMatico

Brazil is a country riven with economic contradictions. It has one of the largest and most profitable banking industries in Latin America, and is among the world’s most developed financial markets. Financial transactions that would take days to process in the United States through ACH happen instantaneously in Brazil. This sophistication, however, masks a backward state of affairs plagued by appalling customer service, exorbitant fees and lack of banking access for many.

The country’s financial system is volatile and often leaves its citizens with few or no alternatives. According to an HBS case study, “in December 2018 the interest rate in Brazil for corporate loans was 52.3%, for consumer loans it was 120.0% and for credit card indebtedness it was 272.42%.” Those rates are many multiples higher compared to figures in neighboring countries.

Brazil’s banking system is a massive market, and one ill-served by incumbents. If someone could thread the needle of product development, strategy and political horse trading required to build a bank in a country where it is nearly impossible for foreigners to own or invest in a bank, it would be one of the great startup and economic success stories of this century.

Nubank is on its way to realizing that objective. Its story is one of unmitigated success, even by the standards of our EC-1 series on high-flying companies and their hard-learned lessons. Just last week, this Brazilian credit card and banking fintech raised a $750 million round led by Berkshire Hathaway at a $30 billion valuation, becoming one of the most valuable startups in the world. It has 40 million users across Brazil, as well as Mexico and Colombia.

Yet, it’s a startup with a CEO and co-founder who isn’t Brazilian, didn’t speak the local language of Portuguese, hadn’t started a company before, and didn’t really know a lot about banking to begin with. This is a story of how raw execution, a “faster, faster” mentality and a fanaticism for making customer experience as enjoyable as a trip to Disney World can completely change the history of an industry — and country — forever.

Our lead writer for this EC-1 is Marcella McCarthy. McCarthy, who spent significant time in Brazil growing up and is trilingual in English, Spanish and Portuguese, has been covering the LatAm and Miami ecosystems for TechCrunch with an eye to the disruption underway in these interconnected regions. The lead editor for this package was Danny Crichton, the assistant editor was Ram Iyer, the copy editor was Richard Dal Porto, and illustrations were drawn by Nigel Sussman.

Nubank had no say in the content of this analysis and did not get advance access to it. McCarthy has no financial ties to Nubank or other conflicts of interest to disclose.

The Nubank EC-1 comprises four main articles numbering 9,200 words and a reading time of 37 minutes. Here’s what’s in the bank:

We’re always iterating on the EC-1 format. If you have questions, comments or ideas, please send an email to TechCrunch Managing Editor Danny Crichton at danny@techcrunch.com.

Powered by WPeMatico

For most startups, the hardest early challenge is identifying a market and a product to serve it. That wasn’t the case for Nubank CEO David Velez, who understood the massive potential for success if he could break into Latin America’s most valuable economy with even a moderately modern banking offering.

Instead, the challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

Nubank knew its market and geography, and through tenacious fundraising, inventive marketing and product development, and a series of contrarian hires, Velez and his team stripped bare the morass of Brazilian banking to build one of the world’s great fintech companies.

The challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

In the first part of this EC-1, I’ll look at how Velez brought his skills and experience to bear on this market, how Nubank was founded in 2013, and how the team brought a Californian rather than Brazilian vibe to their first office on — no joke — California Street, in a neighborhood called Brooklin in the city of São Paulo.

The idea of being his own boss was ingrained in Velez from his earliest days in Colombia, where he grew up in an entrepreneurial family, with a father who owned a button factory. “I heard from my dad over and over again that you need to start your own company,” Velez said.

But years would pass and Velez still had no idea what he wanted to do. To “kill time,” and also to surround himself with entrepreneurial energy, Velez attended Stanford University — partially financed by the sale of some livestock — and then worked as an analyst at Goldman Sachs and Morgan Stanley before switching to venture capital at General Atlantic and Sequoia.

Powered by WPeMatico