Bank

Auto Added by WPeMatico

Auto Added by WPeMatico

With $90 million in deposits and $18.25 million in new financing, HMBradley is making moves as the Los Angeles-based entrant into the challenger bank competition.

LA is home to a growing community of financial services startups, and HMBradley is quickly taking its place among the leaders with a novel twist on the banking business.

Unlike most banking startups that woo customers with easy credit and savvy online user interfaces, HMBradley is pitching a better savings account.

The company offers up to 3% interest on its savings accounts, much higher than most banks these days, and it’s that pitch that has won over consumers and investors alike, according to the company’s co-founder and chief executive, Zach Bruhnke.

With climbing numbers on the back of limited marketing, Bruhnke said raising the company’s latest round of financing was a breeze.

“They knew after the first call that they wanted to do it,” Brunke said of the negotiations with the venture capital firm Acrew, a venture firm whose previous exposure to fintech companies included backing the challenger bank phenomenon which is Chime . “It was a very different kind of fundraise for us. Our seed round was a terrible, treacherous 16-month fundraise,” Brunke said.

For Acrew’s part, the company actually had to call Chime’s founder to ensure that the company was okay with the venture firm backing another entrant into the banking business. Once the approval was granted, Brunke said the deal was smooth sailing.

Acrew, Chime and HMBradley’s founders see enough daylight between the two business models that investing in one wouldn’t be a conflict of interest with the other. And there’s plenty of space for new entrants in the banking business, Bruhnke said. “It’s a very, very large industry as a whole,” he said.

As the company grows its deposits, Bruhnke said there will be several ways it can leverage its capital. That includes commercial lending on the back end of HMBradley’s deposits and other financial services offerings to grow its base.

For now, it’s been wooing consumers with one-click credit applications and the high interest rates it offers to its various tiers of savers.

“When customers hit that 3% tier they get really excited,” Bruhnke said. “If you’re saving money and you’re not saving to HMBradley then you’re losing money.”

The money that HMBradley raised will be used to continue rolling out its new credit product and hiring staff. It already poached the former director of engineering at Capital One, Ben Coffman, and fintech thought leader Saira Rahman, the company said.

In October, the company said, deposits doubled month-over-month and transaction volume has grown to over $110 million since it launched in April.

Since launching the company’s cash back credit card in July, HMBradley has been able to pitch customers on 3% cash back for its highest tier of savers — giving them the option to earn 3.5% on their deposits.

The deposit and lending capabilities the company offers are possible because of its partnership with the California-based Hatch Bank, the company said.

Powered by WPeMatico

Cryptocurrency exchange Coinbase is adding a new way to withdraw funds from your Coinbase account. If you’ve added a compatible debit card to your account, you can transfer USD, EUR or GBP to your bank account nearly instantly.

There are some drawbacks, and the main one is that you’ll pay a lot of fees. In the U.S., Coinbase deducts 1.5% from the transaction, or a minimum $0.55 if it’s a small transaction. In the U.K. and Europe, you pay 2% in fees or a minimum fee of £0.45/€0.52, respectively.

You also need to have a compatible card. Not all debit cards support incoming transfers. You need to have a Visa card that supports Visa Fast Funds. In the U.S., you can also use a Mastercard card with Mastercard Send.

It’s hard to know whether your bank or card issuer support those features. The best way to figure it out is probably by adding your card to Coinbase and seeing what Coinbase says.

Coinbase isn’t removing other withdrawal methods. For instance, if you’re looking for a cheaper way to withdraw your funds in Europe, a SEPA bank transfer costs €0.15 per transfer. And Coinbase supports instant SEPA transfers if your bank has enabled that.

The company also lets you link your PayPal account with your Coinbase account. Your funds should hit your PayPal account within a few seconds, and there are no fees on Coinbase’s side.

As you can see, there are many ways to move money from your bank account to your Coinbase account. Some of them are slower than others, some of them are more expensive than others. Crypto-to-crypto transactions are a bit simpler by comparison, as you only need your recipient’s wallet address to send tokens.

Image Credits: Coinbase

Powered by WPeMatico

Lana, a new startup based in Madrid, is looking to be the next big thing in Latin American fintech.

Founded by serial entrepreneur Pablo Muniz, whose last business was backed by one of Spain’s largest financial services institutions, BBVA, Lana is looking to be the all-in-one financial services provider for Latin America’s gig economy workers.

Muniz’s last company, Denizen, was designed to provide expats in foreign and domestic markets with the financial services they would need as they began their new lives in a different country. While the target customer for Lana may not be the same middle to upper-middle-class international traveler that he had previously hoped to serve, the challenges gig economy workers face in Latin America are much the same.

Muniz actually had two revelations from his work at Denizen. The first — he would never try to launch a fintech company in conjunction with a big bank. And the second was that fintechs or neobanks that focus on a very niche segment will be successful — so long as they can find the right niche.

The biggest niche that Muniz saw that was underserved was actually in the gig economy space in Latin America. “I knew several people who worked at gig economy companies and I knew that their businesses were booming and the industry was growing,” he said. “[But] I was concerned about the inequalities.”

Workers in gig economy marketplaces in Latin America often don’t have bank accounts and are paid through the apps on which they list their services in siloed wallets that are exclusive to that particular app. What Lana is hoping to do is become the wallet of wallets for all of the different companies on which laborers list their services. Frequently, drivers will work for Uber or Cabify and deliver food for Rappi. Those workers have wallets for each service.

(Photo by Cris Faga/Pacific Press/LightRocket via Getty Images)

Lana wants to unify all of those disparate wallets into a single account that would operate like a payment account. These accounts can be opened at local merchant shops and, once opened, workers will have access to a debit card that they can use at other locations.

The Lana service also has a bill pay feature that it’s rolling out to users, in the first evolution of the product into a marketplace for financial services that would appeal to gig workers, Muniz said.

“We want to become that account in which they receive funds,” he said. “We are still iterating the value proposition to gig economy companies.”

Working with companies like Cabify, and other, undisclosed companies, Lana has plans to roll out in Mexico, Chile, Peru and, eventually, Colombia and Argentina.

Eventually, Lana hopes to move beyond basic banking services like deposits and payments and into credit services. Already hundreds of customers are using the company’s service through the distribution partnership with Cabify, which ran the initial pilot to determine the viability of the company’s offering.

“The idea of creating Lana was initially tested as an internal project at Cabify,” Muniz wrote in an email. “Soon Cabify and some potential investors saw that Lana could have a greater impact as an independent company, being able to serve gig economy workers from any industry and decided to start over a new entrepreneurial project.”

Through those connections with Cabify, Lana was able to bring in other investors like the Silicon Valley-based investment firm Base 10.

“One of the things we’ve been interested in is in inclusion generally and in fintech specifically,” said Adeyemi Ajao, the firm’s co-founder. “We had gotten very close to investing in a couple of fintech companies in Latin America and that is because the opportunity is huge. There are several million people going from unbanked to banked in the region.”

Along with a few other investors, Base 10 put in $12.5 million to finance Lana as it looks to expand. It’s a market that has few real competitors. Nubank, Latin America’s biggest fintech company, is offering credit services across the continent, but most of their end users already have an established financial history.

“Most of their end users are not unbanked,” said Ajao. “With Lana it is truly gig workers… They can start by being a wallet of wallets and then give customers products that help them finance their cars or their scooters.”

The ultimate idea is to get workers paid faster and provide a window into their financial history that can give them more opportunities at other gig economy companies, said Ajao. “The vision would be that someone can plug in their financial information for services. If they’re working for Rappi and have never been an Uber driver and they want to be an Uber driver, Lana can use their financial history with Rappi to offer a loan on a car,” he said.

That financial history is completely inaccessible to a traditional bank, and those established financial services don’t care about the history built in wallets that they can’t control or track. “Today if you’ve been a gig worker and you go to a bank, that’s worth nothing,” said Ajao.

Powered by WPeMatico

DeHaat, an online platform that offers full-stack agricultural services to farmers, has raised $12 million as it looks to scale its network across India.

The Series A financial round for the eight-year-old Patna and Gurgaon-based startup was led by Sequoia Capital India. Dutch entrepreneurial development bank FMO, and existing investors Omnivore and AgFunder, also participated in the round. The startup, which began to seek funding from external investors last year, has raised $16 million to date and $3 million in venture debt.

DeHaat (which means village in Hindi) eases the burden on farmers by bringing together brands, institutional financers and buyers on one platform, explained Shashank Kumar, co-founder and chief executive of the startup, in an interview with TechCrunch.

The platform helps farmers secure thousands of agri-input products, including seeds and fertilizers, and receive tailored advisory on the crop they should sow in a season. “We have built a comprehensive database of crop tests to offer advice to farmers,” he said.

DeHaat, which employs 242 people, also helps them connect with 200 institutional partners to provide farmers with working capital, and when the season is over, helps them sell their yields to bulk buyers such as Reliance Fresh, food delivery startup Zomato and business-to-business e-commerce giant Udaan.

DeHaat today operates in 20 regional hubs in the eastern part of India — states such as Bihar, Uttar Pradesh, and Jharkhand — and serves more than 210,000 farmers, said Kumar.

Shashank Kumar, Amrendra Singh, Adarsh Srivastav and Shyam Sundar Singh co-founded DeHaat in 2012

The startup has developed a network of hundreds of micro-entrepreneurs in rural areas that distribute agri-input goods to farmers from their regional hubs and then bring back the output to the same hub.

“We have an app in local languages and a helpline desk that farmers, many of whom don’t own a smartphone, use to reach out to us and explain their pain points and needs,” he said.

DeHaat does not charge any fee for its advisory, but takes a cut whenever farmers use its platform to buy agri-inputs or sell their crop yields.

The startup will use the fresh capital to extend its network to 2,000 rural retail centres, on-board more micro-entrepreneurs for last-mile delivery and reach 1 million farmers by June of next year, said Kumar. DeHaat is also working on automating its supply chain and developing more sophisticated data analytics, he said.

At stake is India’s agriculture market that is worth $350 billion and serves nearly 100 million small and independent farmers, said Abhishek Mohan, VP at Sequoia Capital India, the VC fund that writes more checks than anyone else in the country.

“This industry is on the brink of a massive transformation thanks to ease of regulation, farmers getting organized and increasing penetration of smartphones. DeHaat is leveraging these trends to build the next-gen product in agricultural supply chain,” said Mohan in a statement.

“The tipping point that led to Sequoia India’s decision to partner with them was the field visit, where the farmers expressed how proud they were to be associated with a platform they felt truly worked in their favour. This impact and deep brand loyalty stems from the leadership team’s razor-sharp focus, deep empathy and fine execution,” he added.

Powered by WPeMatico

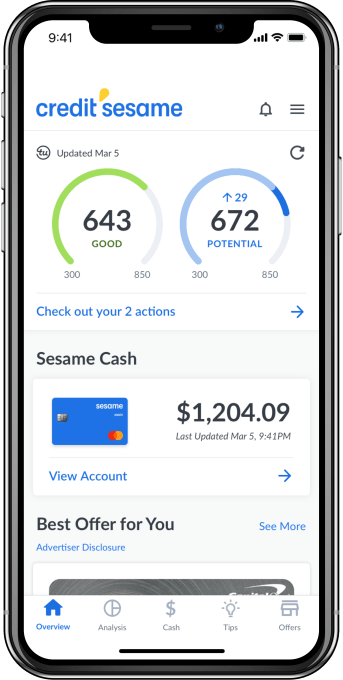

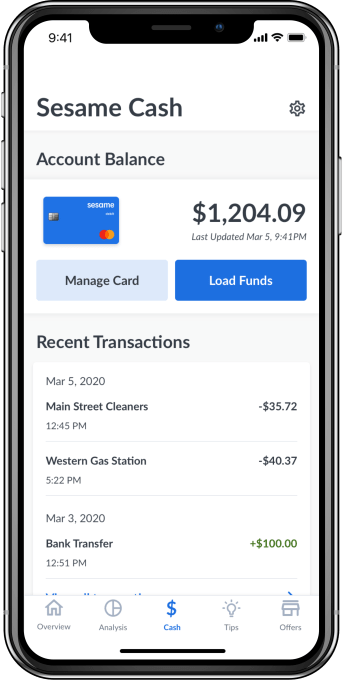

Credit Sesame is getting into digital banking. The credit and loans company, first launched at TechCrunch Disrupt in 2010, has since grown to 15 million registered users and, in 2016, achieved profitability. To date, its focus has been on helping consumers achieve financial health by taking steps to consolidate debt and raise their credit score. Now, it’s expanding to include digital banking, but with the goal of using its better understanding of its banking customers’ finances to better personalize its credit improvement recommendations.

The new service, Sesame Cash, has many features found in other challenger banking apps, like a general lack of fees, real-time notifications, an early payday option, free access to a sizable ATM network, in-app debit card management and more. Specifically, Credit Sesame says it won’t charge monthly fees or overdraft fees, and it provides free access to more than 55,000 ATMs and a no-fee debit card from Mastercard.

However, the banking app also serves a secondary purpose beyond its plan to take on traditional banks. Because the company has insights into users’ finances and repayment abilities, it will be able to offer personalized recommendations, including those for relevant credit products from its hundreds of financial institution partners.

However, the banking app also serves a secondary purpose beyond its plan to take on traditional banks. Because the company has insights into users’ finances and repayment abilities, it will be able to offer personalized recommendations, including those for relevant credit products from its hundreds of financial institution partners.

Other features also differentiate Sesame Cash from rival challenger banks, including built-in access to view your daily credit score and a system that rewards consumers with cash incentives — up to $100 per month — for credit score improvements. The banking app includes $1 million in credit and identity theft protection, as well.

In the months following its launch, the company is planning to introduce a smart bill pay service that manages cash to improve credit and lower interest rates on credit balances, plus an auto-savings feature that works by rounding up transactions, a rewards program for everyday purchases and other smart budgeting tools.

“Through the use of advanced machine learning and AI, we’ve helped millions of consumers improve and manage their credit. However, we identified the disconnect between consumers’ cash and credit—how much cash you have, and how and when you use your cash has an impact on your credit health,” said Adrian Nazari, Credit Sesame Founder and CEO, in a statement. “With Sesame Cash, we are now bridging that gap and unlocking a whole new set of benefits and capabilities in a new product category. This underscores our mission and commitment to innovation and financial inclusion, and the importance we place in working with partners who share the same ethos,” he added.

Credit Sesame today caters to consumers interested in bettering their credit. The company says 61% of its members see credit score improvements within their first six months, and 50% see scores improve by more than 10 points during that time. Indeed, 20% see their score improve by more than 50 points during the first six months.

But one challenge Credit Sesame faces is that after consumers reach their goals, credit-wise, they may become less engaged with the Credit Sesame platform. The new banking app changes that, by allowing the company to maintain a relationship with customers over time.

But one challenge Credit Sesame faces is that after consumers reach their goals, credit-wise, they may become less engaged with the Credit Sesame platform. The new banking app changes that, by allowing the company to maintain a relationship with customers over time.

Credit Sesame is a smaller version of Credit Karma, which was recently acquired by Intuit for $7 billion. Since then, it has been rumored to be another potential acquisition target for Intuit, if it didn’t proceed to go public. The banking service would make Credit Sesame more attractive to a potential acquirer, if that’s the case, as it would offer something Credit Karma did not.

The company says Sesame Cash bank accounts are held with Community Federal Savings Bank, Member FDIC.

The banking service will initially be made available to existing customers, before becoming available to the general public. The Credit Sesame mobile app is a free download for iPhone and Android.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

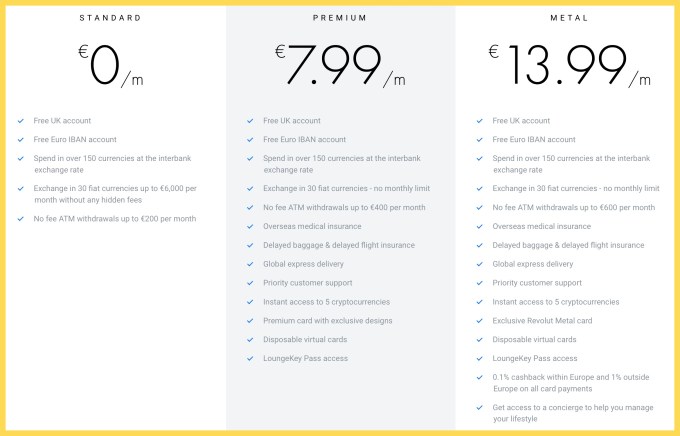

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Although the 2008 global financial crisis sparked the fintech movement, in Latin America, the rise of ecommerce was responsible for the first wave of fintech startups.

Because digital payments were key to enabling the growth of ecommerce, investors funded companies like Braspag, PagSeguro, PayU, Mercado Pago and Moip in the early 2000s to take advantage of this opportunity.

Payment is still the most relevant segment, with successful cases like Stone and PagSeguro, but after the financial crisis, we started to see the rise of financial technology in lending and neobanking, generating impressive cases like Nubank, Neon, Creditas, Credijusto and Ualá.

As the ecosystem evolves and expands, let’s take a closer look at emerging trends in Latin America that might give us a hint about where to expect its next fintech unicorns.

Latin America has seen explosive growth in ride-hailing and food delivery platforms such as Uber, Didi, Rappi and iFood, creating a totally new market opportunity — many gig economy workers can’t access basic financial services such as bank accounts, personal loans and insurance. Even those who have access often struggle with financial products that that don’t suit their needs because they were designed for full-time workers.

Spotting this opportunity, Uber Money launched at Money 2020, focusing on providing drivers with financial services. As 50% of the population in Latin America is unbanked where Uber has more than 1 million drivers, the region is definitely a ripe market. Cabify is going even farther by spinning off Lana, its company that provides financial services, so it can expand its market beyond Cabify drivers to include other gig economy professionals.

Although established players in this sector have a clear advantage, they aren’t the only ones looking to explore this opportunity; Brazilian YC alumni Zippi is offering personal loans to ride-hailing drivers based on their driving earnings. As the gig economy tends to keep growing in the region, I believe we will start to see more solutions for those professionals.

As the banking world has been shaken by fintechs, insurance companies are growing aware that high regulatory barriers won’t protect their industry from disruption.

Insurance penetration in Latin America has been historically low compared to developed markets — 3.1%, compared to 8% — but the insurance market is growing well and tends to close this gap. Adding this to bad services and complex products that insurances provide, insurtech has an immense opportunity to grow.

Because purchasing insurance is historically a complicated and painful experience, the first insurtechs in the region focused on providing a better experience by digitizing the process and using online channels to acquire customers. Those insurtechs worked together with the insurance companies and operating as online broker, but now, we’re starting to see startups providing new insurance products, as well as traditional insurances in different models.

Some are partnering with insurance companies while others are competing directly with them; Think Seg and Miituo partnered with larger players to provide a pay-as-you-go model for car insurance, while Mango Life and Kakau are offering a better purchasing experience. On the other end, Crabi and Pier are rethinking the insurance model from the ground up.

As insurtechs emerge as a potential threat, incumbents are more willing to work with startups that can improve their services to enable them to compete on better grounds, which is exactly what companies such as Bdeo, Lisa, and HelloZum are doing.

Although penetrating the insurance industry is more complicated than other financial services due to high regulatory demands and steep initial operating costs, insurtechs fueled by VC investment will without any doubt try to do it. And, if we’ve learned anything from other fintech segments, it’s that entrepreneurs will find ways to overcome initial challenges.

Powered by WPeMatico

Brex, a Silicon Valley fintech darling, has lofty plans to battle big banks —and Stripe.

Code-named “Gemini,” Brex today announced a new product designed to replace and improve the functionality of traditional bank accounts. Brex Cash, as it will be known publicly, is a business cash management account integrated with the Brex Card, a corporate card for startups launched in 2018.

Brex tells us they’ve built the core banking infrastructure from scratch, allowing the company to forgo third-party processing fees and provide a much-needed tech infusion to antiquated banking systems. In partnership with Boston’s Radius Bank, Brex Cash will allow customers to send payments quickly and easily with no transaction fees attached. Rather, Brex plans to reward its users for making or receiving payments using Brex Cash with points redeemable for cash back, travel and air miles. Customers will also receive 1.6% yield on deposits.

It’s not a bank, but in practice, it can replace a bank, says Brex co-founder and co-chief executive officer Henrique Dubugras .

“Our idea is that new businesses —the new Y Combinator companies —we hope a big percent of them never open a bank account,” Dubugras tells TechCrunch.

Brex now has many similarities to a bank. What differentiates it is its lack of physical branches — it’s exclusively digital — and it’s insurance. Traditional banks are insured by the Federal Deposit Insurance Corporation (FDIC), which protects up to $250,000 per depositor. Brex Cash users are protected by the Securities Investor Protection Corporation (SIPC), a nonprofit agency overseen by the U.S. Securities and Exchange Commission that protects up to $500,000 and specializes in protecting customers of brokerage firms from the loss of cash and securities.

We think we’ve won a lot of credibility. Before, who was going to give their money to a random-ass startup called Brex? -Brex co-CEO Henrique Dubugras

Additionally, Brex invests its customers’ money in a money market mutual fund of U.S. treasury bonds. “If Brex goes out of business, customers’ money will be safe,” the company writes in a press statement. “The only scenario where money could be lost is if the U.S. government defaults.”

Brex Cash user interface

“It’s not that we are inventing this — this model exists with Fidelity,” says Dubugras. “Fidelity isn’t necessarily a bank — we are bringing that concept to businesses to give lower fees, better interest rates, better experiences and more security.”

Brex, a graduate of the winter 2017 Y Combinator cohort, has quickly become a Silicon Valley success story for the ages. The rapid adoption of its startup credit card, which doesn’t require a personal guarantee, and its ability to issue cards instantly and provide higher limits than other options on the market has attracted thousands of customers and venture capitalists. The business, led by a pair of young Brazilian repeat entrepreneurs, including Dubugras and co-CEO Pedro Franceschi, has collected more than $300 million in equity funding, including a $100 million C-2 financing that valued the company at $2.6 billion earlier this year.

“There will always be customers that are skeptical, but I think by starting out with a card, we built a lot of trust,” Dubugras said. “It was us giving them money instead of them giving us money. A few years in … We think we’ve won a lot of credibility. Before, who was going to give their money to a random-ass startup called Brex?”

In the weeks ahead of TechCrunch Disrupt San Francisco, where Dubugras announced Brex Cash on Wednesday, the CEO told TechCrunch that Brex had no immediate fundraising plans and that they were “waiting for the right time” to raise again. As for what’s next, he said the company is discussing the launch of a debit card and plans to add another 100 employees in the next year, bringing the Brex headcount to 400.

The Brex news follows the launch of Stripe Capital, a new offering from payments behemoth Stripe that will make instant loan offers to customers on its platform, and the announcement of the Stripe Corporate Card. Akin to Brex, Stripe will issue a no-fee, no interest rate credit card intended for Stripe customers. Brex and Stripe, two Y Combinator grads, will go head-to-head in a battle for customers, particularly YC grads looking for friendly financial tools.

Immediately following Stripe’s announcements, the business announced a $250 million funding at a $35 billion valuation. Brex may be following a similar playbook, announcing a major product on the heels of a large capital infusion.

Brex Cash represents a new era for the company. Though the product may be costly for Brex, it opens the business up to thousands more potential customers. Now, any startup, regardless of funding, can create a Brex account to store cash, explains Dubugras, and all companies using Brex Cash will be immediately issued a Brex corporate credit card.

“If you’re starting out, if you don’t have funding yet, you can still receive your payments using Brex,” Dubugras said. “That’s a super big deal for us.”

Brex Cash was built under product lead Ritik Malhotra, who joined the team as part of an acquisition of his startup, Elph. Brex poached the company, which was focused on blockchain infrastructure, right out of YC for an undisclosed amount. In retrospect, the deal looks much more like an acqui-hire of Malhotra, who had the digital payments infrastructure acumen necessary to complete this project.

“It’s an easy way to move money, which is the lifeblood of a business,” Malhotra tells TechCrunch of the new product.

Brex Cash is itself not a cash cow for Brex; rather, the startup makes money on purchases made on its corporate card, in which it charges the merchant, not the customer. This model is particularly beneficial when its customers are spending a lot of money, growing quickly and raising capital. In a downturn, however, this model isn’t as attractive.

Brex seems unconcerned with the possibility of an impending recession. Brex writes that even in downturns, entrepreneurs will start companies and attempt to raise money. The Brex Cash product, regardless of the economy, will help Brex better underwrite Brex Cards, as it gives them better access to a customer’s financial health.

In a battle against Stripe, Brex is at a disadvantage. At only two years old, the company may have garnered a lot of credibility in a short time but it doesn’t have the decade of experience building fintech products that Stripe has and, more importantly, it doesn’t have 10 years of customer loyalty.

Powered by WPeMatico

Two years after the Los Angeles-based fintech startup Dave launched with a suite of money management tools to save consumers from overdraft fees, the company is now worth $1 billion thanks to a nascent banking practice that had investors lining up.

The company used its overdraft protection service and money management display to shift customers’ focus away from the total balance that their account would show by giving them a sense of how much was actually left in their accounts once debits were included in their statements.

“What was cool about our financial management product was that we were trying to use Dave as a replacement for their current bank,” says Jason Wilk, Dave’s co-founder and chief executive.

Dave now counts over 4 million users for its financial management app and has roughly 800,000 people on the waiting list to use its banking services, Wilk says.

The company has taken a methodical approach to opening its doors as a digital bank, in part because it wants to have the necessary support infrastructure in place to service the demand that Wilk expects to see for its service.

“It’s one thing to help people with budgeting. It’s another to actually manage their money,” says Wilk.

")

Dave will use the $50 million raised from Norwest to significantly expand its product and engineering team within the next 12 months, in order to double down on the core business and ensure the success of the banking product.

“We can prove that Dave can be helpful by showing how we can help you manage your current account, and then Dave banking is the marketing lever from there,” says Wilk.

For now, customers need to have the financial management app installed to be able to access the company’s banking service.

Dave charges $1 per month for access to its financial management tools and that also gives customers the ability to use a cushion of between $50 to $75 to avoid being hit with overdraft fees from their current bank account. Dave asks for a tip every time a customer uses that cushion to cover expenses — something that Wilk says is still cheaper than having to worry about overdraft fees.

And, to add a bit of environmental spin, for every tip that Dave receives, the company plants a tree. “We plant millions and millions of trees,” says Wilk.

The company is FDIC insured through a partner bank, the Memphis-based Evolve Bank and Trust, which acts as a backstop for the company’s financial management activities.

“We already had a relationship with them for some payment processing stuff,” says Wilk. “We liked the team and liked the terms and went with them.”

Terms between financial services firms can vary, and, Wilk says, Evolve Bank was willing to give the company a good deal on splitting the interchange fee, which is a big source of revenue for upstart banks.

It’s possible that Dave could have received a bigger check at a potentially higher valuation, but Wilk says the startup is trying to stay lean.

“The company is growing so quickly, we didn’t want to get too diluted on this round,” he says. “We think the company is quite a bit more valuable than [$1 billion]. You don’t want to raise too much money too quickly if you really think the valuation is going to climb… Since we signed the term sheet the company has already grown another 40%.”

It was only four months ago that Dave was announcing a $110 million credit financing with Victory Park Capital and the launch of its banking product.

Dave’s products and services have a few advantages for customers that are just getting started on the path to financial security. The company monitors everyday monthly payments and reports them to credit agencies to improve customers’ credit ratings. The company also provides up to $100, interest-free, overdraft protection.

“Banks have failed their customers by building products that put their own interests ahead of the humans who use them. People don’t need predatory fees, they need tools that actually solve their challenges around credit building, finding work and getting access to their own money to cover immediate expenses. Dave is the banking product that works with its customers, not against them,” said Wilk, in a June statement announcing the funding and banking product launch.

While Dave is getting some hefty firepower and a generous valuation from Norwest, it’s also operating in a market where its core services that were a point of differentiation are quickly becoming table stakes.

Earlier in September, the new startup banking company Chime announced that it had hit 5 million banking customers and was offering its own overdraft protection service.

The San Francisco-based bank has also raised a lot more capital for a potential piggy bank to raid if it needs to acquire or spend on engineering talent to build out new products and services. Earlier this year, the company announced a $200 million round and said it had hit roughly 3 million customers. Clearly Chime is adding new banking customers at a torrid pace.

And they’re facing global competition as well. N26, the European startup bank with a $3.6 billion valuation and hundreds of millions in financing launched in the U.S. a few months ago as well.

The company sees a global opportunity to create new digital banking services in a world where large amounts of capital and an elite set of consumers move easily between international markets.

“We have an opportunity that we build a bank that has more than 50 million users around the globe. Today, we only have 3.5 million users but we’re accelerating,” said N26 chief executive, Valentin Self, in an interview with TechCrunch. “From a country perspective, we have agreed already that we go to Brazil. There’s no plan after Brazil yet. Now let’s focus on the U.S., then on Brazil, then next year we’ll find out what’s the feedback from these two markets.”

Powered by WPeMatico

Axis is selling its first product, the Axis Gear, on Amazon and direct from its own website, but that’s a relatively recent development for the four-year-old company. The idea for Gear, which is a $249.00 ($179.00 as of this writing thanks to a sale) aftermarket conversion gadget to turn almost any cord-pull blinds into automated smart blinds, actually came to co-founder and CEO Trung Pham in 2014, but development didn’t begin until early the next year, and the maxim that “hardware is hard” once again proved more than valid.

Pham, whose background is actually in business but who always had a penchant for tech and gadgets, originally set out to scratch his own itch and arrived upon the idea for his company as a result. He was actually in the market for smart blinds when he moved into his first condo in Toronto, but after all the budget got eaten up on essentials like a couch, a bed and a TV, there wasn’t much left in the bank for luxuries like smart shades — especially after he actually found out how much they cost.

“Even though I was a techie, and I wanted automated shades, I couldn’t afford it,” Pham told me in an interview. “I went to the designer and got quoted for some really nice Hunter Douglas. And they quoted me just over $1,000 a window with the motorization option. So I opted just for manual shades. A couple of months later, when it’s really hot and sunny, I’m just really noticing the heat so I go back to the designer and ask him ‘Hey can I actually get my shades motorized now, I have a little bit more money, I just want to do my living room.’ And that’s when I learned that once you have your shades installed, you actually can’t motorize them, you have to replace them with brand new shades.”

With his finance background, Pham saw an opportunity in the market that was ignored by the big legacy players, and potentially relatively easy to address with tech that wasn’t all that difficult to develop, including a relatively simple motor and the kind of wireless connectivity that’s much more readily available thanks to the smartphone component supply chain. And the market demand was there, Pham says — especially with younger homeowners spending more on their property purchases (or just renting) and having less to spare on expensive upgrades like motorized shades.

The Axis solution is relatively affordable (though its regular asking price of $249 per unit can add up, depending on how many windows you’re looking to retrofit) and also doesn’t require you to replace your entire existing shades or blinds, so long as you have the type with which the Gear is compatible (which includes quite a lot of commonly available shades). There are a couple of power options, including an AC adapter for a regular outlet, or a solar bar with back-up from AA batteries in case there’s no outlet handy.

The Axis solution is relatively affordable (though its regular asking price of $249 per unit can add up, depending on how many windows you’re looking to retrofit) and also doesn’t require you to replace your entire existing shades or blinds, so long as you have the type with which the Gear is compatible (which includes quite a lot of commonly available shades). There are a couple of power options, including an AC adapter for a regular outlet, or a solar bar with back-up from AA batteries in case there’s no outlet handy.

Pham explained how in early investor meetings, he would cite Dyson as an inspiration, because that company took something that was standard and considered central to their very staid industry and just removed it altogether — specifically referring to their bagless design. He sees Axis as taking a similar approach in the smart blind market, which has too much to gain from maintaining its status quo to tackle Axis’ approach to the market. Plus, Pham notes, Axis has six patents filed and three granted for its specific technical approach.

“We want to own the idea of smart shades to the end consumer,” he told me. “And that’s where the focus really is. It’s a big opportunity, because you’re not just buying one doorbell or one thermostat – you’re buying multiple units. We have customers that buy one or two right away, come back and buy more, and we have customers that buy 20 right away. So our ability to sell volume to each household is very beneficial for us as a business.”

Which isn’t to say Axis isn’t interested in larger-scale commercial deployment — Pham says that there are “a lot of [commercial] players and hotels testing it,” and notes that they also “did a project in the U.S. with one of the largest developers in the country.” So far, however, the company is laser-focused on its consumer product and looking at commercial opportunities as they come inbound, with plans to tackle the harder work of building a proper commercial sales team. But it could afford Axis a lot of future opportunity, especially because their product can help building managers get compliant with measures like the Americans with Disabilities Act to outfit properties with the requisite amount of units featuring motorized shades.

To date, Axis has been funded entirely via angel investors, along with family and friends, and through a crowdfunding project on Indiegogo, which secured its first orders. Pham says revenue and sales, along with year-over-year growth, have all been strong so far, and that they’ve managed to ship “quite a few units so far” — though he declined to share specifics. The startup is about to close a small bridge round and then will be looking to pin down its Series A funding as it looks to expand its product line — with a focus on greater window coverings style compatibility as top priority.

Powered by WPeMatico