AWS

Auto Added by WPeMatico

Auto Added by WPeMatico

I’ve met hundreds of founders over the years, and most, particularly early-stage founders, share one common go-to-market gripe: Pricing.

For enterprise software, traditional pricing methods like per-seat models are often easier to figure out for products that are hyperspecific, especially those used by people in essentially the same way, such as Zoom or Slack. However, it’s a different ballgame for startups that offer services or products that are more complex.

Most startups struggle with a per-seat model because their products, unlike Zoom and Slack, are used in a litany of ways. Salesforce, for example, employs regular seat licenses and admin licenses — customers can opt for lower pricing for solutions that have low-usage parts — while other products are priced based on negotiation as part of annual renewals.

You may have a strong champion in a CIO you’re selling to or a very friendly person handling procurement, but it won’t matter if the pricing can’t be easily explained and understood. Complicated or unclear pricing adds more friction.

Early pricing discussions should center around the buyer’s perspective and the value the product creates for them. It’s important for founders to think about the output and the outcome, and a number they can reasonably defend to customers moving forward. Of course, self-evaluation is hard, especially when you’re asking someone else to pay you for something you’ve created.

This process will take time, so here are three tips to smoothen the ride.

Pricing is not a fixed exercise. The enterprise software business involves a lot of intangible aspects, and a software product’s perceived value, quality, and user experience can be highly variable.

The pricing journey is long and, despite what some founders might think, jumping headfirst into customer acquisition isn’t the first stop. Instead, step one is making sure you have a fully fledged product.

If you’re a late-seed or Series A company, you’re focused on landing those first 10-20 customers and racking up some wins to showcase in your investor and board deck. But when you grow your organization to the point where the CEO isn’t the only person selling, you’ll want to have your go-to-market position figured out.

Many startups fall into the trap of thinking: “We need to figure out what pricing looks like, so let’s ask 50 hypothetical customers how much they would pay for a solution like ours.” I don’t agree with this approach, because the product hasn’t been finalized yet. You haven’t figured out product-market fit or product messaging and you want to spend a lot of time and energy on pricing? Sure, revenue is important, but you should focus on finding the path to accruing revenue versus finding a strict pricing model.

Powered by WPeMatico

Organizations are swimming in data these days, and so solutions to help manage and use that data in more efficient ways will continue to see a lot of attention and business. In the latest development, SingleStore — which provides a platform to enterprises to help them integrate, monitor and query their data as a single entity, regardless of whether that data is stored in multiple repositories — is announcing another $80 million in funding, money that it will be using to continue investing in its platform, hiring more talent and overall business expansion. Sources close to the company tell us that the company’s valuation has grown to $940 million.

The round, a Series F, is being led by Insight Partners, with new investor Hewlett Packard Enterprise, and previous backers Khosla Ventures, Dell Technologies Capital, Rev IV, Glynn Capital and GV (formerly Google Ventures) also participating. The startup has to date raised $264 million, including most recently an $80 million Series E last December, just on the heels of rebranding from MemSQL.

The fact that there are three major strategic investors in this Series F — HPE, Dell and Google — may say something about the traction that SingleStore is seeing, but so too do its numbers: 300%+ increase in new customer acquisition for its cloud service and 150%+ year-over-year growth in cloud.

Raj Verma, SingleStore’s CEO, said in an interview that its cloud revenues have grown by 150% year over year and now account for some 40% of all revenues (up from 10% a year ago). New customer numbers, meanwhile, have grown by over 300%.

“The flywheel is now turning around,” Verma said. “We didn’t need this money. We’ve barely touched our Series E. But I think there has been a general sentiment among our board and management that we are now ready for the prime time. We think SingleStore is one of the best-kept secrets in the database market. Now we want to aggressively be an option for people looking for a platform for intensive data applications or if they want to consolidate databases to one from three, five or seven repositories. We are where the world is going: real-time insights.”

With database management and the need for more efficient and cost-effective tools to manage that becoming an ever-growing priority — one that definitely got a fillip in the last 18 months with COVID-19 pushing people into more remote working environments. That means SingleStore is not without competitors, with others in the same space, including Amazon, Microsoft, Snowflake, PostgreSQL, MySQL, Redis and more. Others like Firebolt are tackling the challenges of handing large, disparate data repositories from another angle. (Some of these, I should point out, are also partners: SingleStore works with data stored on AWS, Microsoft Azure, Google Cloud Platform and Red Hat, and Verma describes those who do compute work as “not database companies; they are using their database capabilities for consumption for cloud compute.”)

But the company has carved a place for itself with enterprises and has thousands now on its books, including GE, IEX Cloud, Go Guardian, Palo Alto Networks, EOG Resources and SiriusXM + Pandora.

“SingleStore’s first-of-a-kind cloud database is unmatched in speed, scale, and simplicity by anything in the market,” said Lonne Jaffe, managing director at Insight Partners, in a statement. “SingleStore’s differentiated technology allows customers to unify real-time transactions and analytics in a single database.” Vinod Khosla from Khosla Ventures added that “SingleStore is able to reduce data sprawl, run anywhere, and run faster with a single database, replacing legacy databases with the modern cloud.”

Powered by WPeMatico

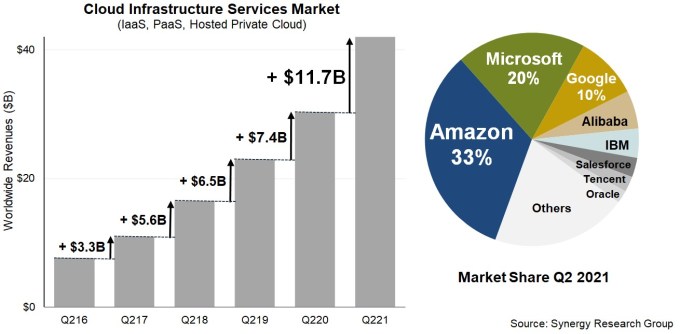

It’s often said in baseball that a prospect has a high ceiling, reflecting the tremendous potential of a young player with plenty of room to get better. The same could be said for the cloud infrastructure market, which just keeps growing, with little sign of slowing down any time soon. The market hit $42 billion in total revenue with all major vendors reporting, up $2 billion from Q1.

Synergy Research reports that the revenue grew at a speedy 39% clip, the fourth consecutive quarter that it has increased. AWS led the way per usual, but Microsoft continued growing at a rapid pace and Google also kept the momentum going.

AWS continues to defy market logic, actually increasing growth by 5% over the previous quarter at 37%, an amazing feat for a company with the market maturity of AWS. That accounted for $14.81 billion in revenue for Amazon’s cloud division, putting it close to a $60 billion run rate, good for a market leading 33% share. While that share has remained fairly steady for a number of years, the revenue continues to grow as the market pie grows ever larger.

Microsoft grew even faster at 51%, and while Microsoft cloud infrastructure data isn’t always easy to nail down, with 20% of market share according to Synergy Research, that puts it at $8.4 billion as it continues to push upward with revenue up from $7.8 billion last quarter.

Google too continued its slow and steady progress under the leadership of Thomas Kurian, leading the growth numbers with a 54% increase in cloud revenue in Q2 on revenue of $4.2 billion, good for 10% market share, the first time Google Cloud has reached double figures in Synergy’s quarterly tracking data. That’s up from $3.5 billion last quarter.

Image Credits: Synergy Research

After the Big 3, Alibaba held steady over Q1 at 6% (but will only report this week), with IBM falling a point from Q1 to 4% as Big Blue continues to struggle in pure infrastructure as it makes the transition to more of a hybrid cloud management player.

John Dinsdale, chief analyst at Synergy, says that the Big 3 are spending big to help fuel this growth. “Amazon, Microsoft and Google in aggregate are typically investing over $25 billion in capex per quarter, much of which is going towards building and equipping their fleet of over 340 hyperscale data centers,” he said in a statement.

Meanwhile, Canalys had similar numbers, but saw the overall market slightly higher at $47 billion. Their market share broke down to Amazon with 31%, Microsoft with 22% and Google with 8% of that total number.

Canalys analyst Blake Murray says that part of the reason companies are shifting workloads to the cloud is to help achieve environmental sustainability goals as the cloud vendors are working toward using more renewable energy to run their massive data centers.

“The best practices and technology utilized by these companies will filter to the rest of the industry, while customers will increasingly use cloud services to relieve some of their environmental responsibilities and meet sustainability goals,” Murray said in a statement.

Regardless of whether companies are moving to the cloud to get out of the data center business or because they hope to piggyback on the sustainability efforts of the Big 3, companies are continuing a steady march to the cloud. With some estimates of worldwide cloud usage at around 25%, the potential for continued growth remains strong, especially with many markets still untapped outside the U.S.

That bodes well for the Big 3 and for other smaller operators who can find a way to tap into slices of market share that add up to big revenue. “There remains a wealth of opportunity for smaller, more focused cloud providers, but it can be hard to look away from the eye-popping numbers coming out of the Big 3,” Dinsdale said.

In fact, it’s hard to see the ceiling for these companies any time in the foreseeable future.

Powered by WPeMatico

Most database startups avoid building relational databases, since that market is dominated by a few goliaths. Oracle, MySQL and Microsoft SQL Server have embedded themselves into the technical fabric of large- and medium-size companies going back decades. These established companies have a lot of market share and a lot of money to quash the competition.

So rather than trying to compete in the relational database market, over the past decade, many database startups focused on alternative architectures such as document-centric databases (like MongoDB), key-value stores (like Redis) and graph databases (like Neo4J). But Cockroach Labs went against conventional wisdom with CockroachDB: It intentionally competed in the relational database market with its relational database product.

While it did face an uphill battle to penetrate the market, Cockroach Labs saw a surprising benefit: It didn’t have to invent a market. All it needed to do was grab a share of a market that also happened to be growing rapidly.

Cockroach Labs has a bright future, compelling technology, a lot of money in the bank and has an experienced, technically astute executive team.

In previous parts of this EC-1, I looked at the origins of CockroachDB, presented an in-depth technical description of its product as well as an analysis of the company’s developer relations and cloud service, CockroachCloud. In this final installment, we’ll look at the future of the company, the competitive landscape within the relational database market, its ability to retain talent as it looks toward a potential IPO or acquisition, and the risks it faces.

CockroachDB’s success is not guaranteed. It has to overcome significant hurdles to secure a profitable place for itself among a set of well-established database technologies that are owned by companies with very deep pockets.

It’s not impossible, though. We’ll first look at MongoDB as an example of how a company can break through the barriers for database startups competing with incumbents.

Dev Ittycheria, MongoDB CEO, rings the Nasdaq Stock Market Opening Bell. Image Credits: Nasdaq, Inc

MongoDB is a good example of the risks that come with trying to invent a new database market. The company started out as a purely document-centric database at a time when that approach was the exception rather than the rule.

Web developers like document-centric databases because they address a number of common use cases in their work. For example, a document-centric database works well for storing comments to a blog post or a customer’s entire order history and profile.

Powered by WPeMatico

On a recent episode of Extra Crunch Live, Retail Zipline founder Melissa Wong and Emergence Capital investor Lotti Siniscalco joined Managing Editor Jordan Crook to walk attendees through Zipline’s Series A deck.

Interestingly, the conversation revealed that Wong declined an invitation to do a virtual pitch and insisted on an in-person meeting.

“She was one of the few or maybe the only CEO who ever stood up to pitch the entire team,” said Siniscalco.

“She pointed to the screen projected behind her to help us stay on the most relevant piece of information. The way she did it really made us stay with her. Like, we couldn’t break eye contact.”

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Beyond Wong’s pitch technique, this post also examines some of the key “customer love” metrics that helped Zipline win the day, such as CAC, churn rates and net promoter score.

“In retrospect, I really underestimated the competitive advantage of coming from the industry,” said Wong. “But it resulted in the numbers in our deck, because I know what customers want, what they want to buy next, how to keep them happy and I was able to be way more capital-efficient.”

Read our recap with highlights from their conversation, or click though to watch a video with their entire chat.

Thanks very much for reading Extra Crunch this week!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

Global venture capital reached $156 billion in Q2 2021, a YOY increase of 157%. A record number of unicorns found their feet during the same period and valuations rose across the board, report Anna Heim and Alex Wilhelm in today’s edition of The Exchange.

Even if round counts didn’t set all-time highs, “the general vibe of Q2 venture capital data was clear: It’s a great time for startups looking to raise capital.”

Anna and Alex are interviewing VCs in different regions to find out why they’re feeling so generous and optimistic. Today, they started with the following U.S.-based investors:

Image Credits: AzmanJaka (opens in a new window) / Getty Images

The construction industry might seem like a sector wanting innovation, Safe Site Check In CEO and founder David Ward writes in a guest column, but there are unique challenges that make construction firms slow to adapt to new technology.

From the way construction projects are funded to complicated local regulations, there’s no one-size-fits-all solution for the construction industry’s tech problems.

Construction tech might be appealing to investors, Ward writes, but it must be “easy to use, easy to deploy or access while on a job site, and improve productivity almost immediately.”

Image Credits: AP Photo/Isaac Brekken/John Locher

Now that he’s stepping away from AWS and taking over for Jeff Bezos, what are the biggest challenges facing incoming Amazon CEO Andy Jassy?

Enterprise reporter Ron Miller reached out to three analysts to get their take:

Amazon is listed second in the Fortune 500, but it’s not all sunshine and roses — maintaining growth, unionization, and the potential for antitrust regulation at home and abroad are just a few of his responsibilities.

“I think the biggest to-do is to just continue that momentum that the company has had for the last several years,” Kodali says. “He has to make sure that they don’t lose that. If he does that, I mean, he will win.”

Image Credits: Peter Dazeley (opens in a new window) / Getty Images

Publishing an API isn’t enough for any startup: Once it’s released, the hard work of cultivating a developer base begins.

Postman’s head of developer relations, Joyce Lin, wrote a guest post for Extra Crunch based on the findings of a study aimed at increasing adoption of APIs that utilize a public workspace.

Lin found that the most important metric for a public API is time to first call (TTFC). It makes sense — faster TTFC allows developers to begin using new tools quickly. As a result, “legitimately streamlining TTFC results in a larger market potential of better-educated users for the later stages of your developer journey,” writes Lin.

This post isn’t just for the developers in our audience: TTFC is a metric that product and growth teams should also keep top of mind, they suggest.

“Even if your market is defined as a limited subset of the developer community, any enhancements you make to TTFC equate to a larger available market.”

Image Credits: olli0815/iStock

Couchbase and Kaltura offered new filings Monday, with NoSQL provider Couchbase setting an initial price range for its IPO and Kaltura resurrecting its public offering with a fresh price range and new financial information.

“Both bits of news should help us get a handle on how the Q3 2021 IPO cycle is shaping up at the start,” Alex Wilhelm writes.

Image Credits: PM Images (opens in a new window)/ Getty Images

Mark Spera, the head of growth marketing at Minted, offers SEO tips to help smaller sites stand out.

He writes in a guest column that Google’s algorithm “errs on the side of caution,” which leads the search engine to favor larger, more established websites.

“The cards aren’t in your favor, so you need to be even more strategic than the big guys,” he writes. “This means executing on some cutting-edge hacks to increase your SEO throughput and capitalize on some of the arbitrage still left in organic search. I call these five tactics ‘advanced-ish,’ because none of them are complicated, but all of them are supremely important for search marketers in 2021.”

Powered by WPeMatico

It’s not easy following a larger-than-life founder and CEO of an iconic company, but that’s what former AWS CEO Andy Jassy faces this week as he takes over for Jeff Bezos, who moves into the executive chairman role. Jassy must deal with myriad challenges as he becomes the head honcho at the No. 2 company on the Fortune 500.

How he handles these challenges will define his tenure at the helm of the online retail giant. We asked several analysts to identify the top problems he will have to address in his new role.

Handling that transition smoothly and showing investors and the rest of the world that it’s business as usual at Amazon is going to be a big priority for Jassy, said Robin Ody, an analyst at Canalys. He said it’s not unlike what Satya Nadella faced when he took over as CEO at Microsoft in 2014.

Handling the transition smoothly and showing investors and the rest of the world that it’s business as usual at Amazon is going to be a big priority for Jassy.

“The biggest task is that you’re following Jeff Bezos, so his overarching issue is going to be stability and continuity. … The eyes of the world are on that succession. So managing that I think is the overall issue and would be for anyone in the same position,” Ody said.

Forrester analyst Sucharita Kodali said Jassy’s biggest job is just to keep the revenue train rolling. “I think the biggest to-do is to just continue that momentum that the company has had for the last several years. He has to make sure that they don’t lose that. If he does that, I mean, he will win,” she said.

As an online retailer, the company has thrived during COVID, generating $386 billion in revenue in 2020, up more than $100 billion over the prior year. As Jassy takes over and things return to something closer to normal, will he be able to keep the revenue pedal to the metal?

Powered by WPeMatico

When the Pentagon killed the JEDI cloud program yesterday, it was the end of a long and bitter road for a project that never seemed to have a chance. The question is why it didn’t work out in the end, and ultimately I think you can blame the DoD’s stubborn adherence to a single vendor requirement, a condition that never made sense to anyone, even the vendor that ostensibly won the deal.

In March 2018, the Pentagon announced a mega $10 billion, decade-long cloud contract to build the next generation of cloud infrastructure for the Department of Defense. It was dubbed JEDI, which aside from the Star Wars reference, was short for Joint Enterprise Defense Infrastructure.

The idea was a 10-year contract with a single vendor that started with an initial two-year option. If all was going well, a five-year option would kick in and finally a three-year option would close things out with earnings of $1 billion a year.

While the total value of the contract had it been completed was quite large, a billion a year for companies the size of Amazon, Oracle or Microsoft is not a ton of money in the scheme of things. It was more about the prestige of winning such a high-profile contract and what it would mean for sales bragging rights. After all, if you passed muster with the DoD, you could probably handle just about anyone’s sensitive data, right?

Regardless, the idea of a single-vendor contract went against conventional wisdom that the cloud gives you the option of working with the best-in-class vendors. Microsoft, the eventual winner of the ill-fated deal acknowledged that the single vendor approach was flawed in an interview in April 2018:

Leigh Madden, who heads up Microsoft’s defense effort, says he believes Microsoft can win such a contract, but it isn’t necessarily the best approach for the DoD. “If the DoD goes with a single award path, we are in it to win, but having said that, it’s counter to what we are seeing across the globe where 80% of customers are adopting a multicloud solution,” Madden told TechCrunch.

Perhaps it was doomed from the start because of that. Yet even before the requirements were fully known there were complaints that it would favor Amazon, the market share leader in the cloud infrastructure market. Oracle was particularly vocal, taking its complaints directly to the former president before the RFP was even published. It would later file a complaint with the Government Accountability Office and file a couple of lawsuits alleging that the entire process was unfair and designed to favor Amazon. It lost every time — and of course, Amazon wasn’t ultimately the winner.

While there was a lot of drama along the way, in April 2019 the Pentagon named two finalists, and it was probably not too surprising that they were the two cloud infrastructure market leaders: Microsoft and Amazon. Game on.

The former president interjected himself directly in the process in August that year, when he ordered the Defense Secretary to review the matter over concerns that the process favored Amazon, a complaint which to that point had been refuted several times over by the DoD, the Government Accountability Office and the courts. To further complicate matters, a book by former defense secretary Jim Mattis claimed the president told him to “screw Amazon out of the $10 billion contract.” His goal appeared to be to get back at Bezos, who also owns the Washington Post newspaper.

In spite of all these claims that the process favored Amazon, when the winner was finally announced in October 2019, late on a Friday afternoon no less, the winner was not in fact Amazon. Instead, Microsoft won the deal, or at least it seemed that way. It wouldn’t be long before Amazon would dispute the decision in court.

By the time AWS re:Invent hit a couple of months after the announcement, former AWS CEO Andy Jassy was already pushing the idea that the president had unduly influenced the process.

“I think that we ended up with a situation where there was political interference. When you have a sitting president, who has shared openly his disdain for a company, and the leader of that company, it makes it really difficult for government agencies, including the DoD, to make objective decisions without fear of reprisal,” Jassy said at that time.

Then came the litigation. In November the company indicated it would be challenging the decision to choose Microsoft charging that it was was driven by politics and not technical merit. In January 2020, Amazon filed a request with the court that the project should stop until the legal challenges were settled. In February, a federal judge agreed with Amazon and stopped the project. It would never restart.

In April the DoD completed its own internal investigation of the contract procurement process and found no wrongdoing. As I wrote at the time:

While controversy has dogged the $10-billion, decade-long JEDI contract since its earliest days, a report by the DoD’s inspector general’s office concluded today that, while there were some funky bits and potential conflicts, overall the contract procurement process was fair and legal and the president did not unduly influence the process in spite of public comments.

Last September the DoD completed a review of the selection process and it once again concluded that Microsoft was the winner, but it didn’t really matter as the litigation was still in motion and the project remained stalled.

The legal wrangling continued into this year, and yesterday the Pentagon finally pulled the plug on the project once and for all, saying it was time to move on as times have changed since 2018 when it announced its vision for JEDI.

The DoD finally came to the conclusion that a single-vendor approach wasn’t the best way to go, and not because it could never get the project off the ground, but because it makes more sense from a technology and business perspective to work with multiple vendors and not get locked into any particular one.

“JEDI was developed at a time when the Department’s needs were different and both the CSPs’ (cloud service providers) technology and our cloud conversancy was less mature. In light of new initiatives like JADC2 (the Pentagon’s initiative to build a network of connected sensors) and AI and Data Acceleration (ADA), the evolution of the cloud ecosystem within DoD, and changes in user requirements to leverage multiple cloud environments to execute mission, our landscape has advanced and a new way ahead is warranted to achieve dominance in both traditional and nontraditional warfighting domains,” said John Sherman, acting DoD chief information officer in a statement.

In other words, the DoD would benefit more from adopting a multicloud, multivendor approach like pretty much the rest of the world. That said, the department also indicated it would limit the vendor selection to Microsoft and Amazon.

“The Department intends to seek proposals from a limited number of sources, namely the Microsoft Corporation (Microsoft) and Amazon Web Services (AWS), as available market research indicates that these two vendors are the only Cloud Service Providers (CSPs) capable of meeting the Department’s requirements,” the department said in a statement.

That’s not going to sit well with Google, Oracle or IBM, but the department further indicated it would continue to monitor the market to see if other CSPs had the chops to handle their requirements in the future.

In the end, the single vendor requirement contributed greatly to an overly competitive and politically charged atmosphere that resulted in the project never coming to fruition. Now the DoD has to play technology catch-up, having lost three years to the histrionics of the entire JEDI procurement process and that could be the most lamentable part of this long, sordid technology tale.

Powered by WPeMatico

Jeff Bussgang, a co-founder and general partner at Flybridge Capital, recently wrote an Extra Crunch guest post that argued it is time for a refresh when it comes to the technology adoption life cycle and the chasm. His argument went as follows:

Now, I agree with Jeff that we are seeing remarkable growth in technology adoption at levels that would have astonished investors from prior decades. In particular, I agree with him when he says:

The pandemic helped accelerate a global appreciation that digital innovation was no longer a luxury but a necessity. As such, companies could no longer wait around for new innovations to cross the chasm. Instead, everyone had to embrace change or be exposed to an existential competitive disadvantage.

But this is crossing the chasm! Pragmatic customers are being forced to adopt because they are under duress. It is not that they buy into the vision of software eating the world. It is because their very own lunches are being eaten. The pandemic created a flotilla of chasm-crossings because it unleashed a very real set of existential threats.

The key here is to understand the difference between two buying decision processes, one governed by visionaries and technology enthusiasts (the early adopters and innovators), the other by pragmatists (the early majority).

The key here is to understand the difference between two buying decision processes, one governed by visionaries and technology enthusiasts (the early adopters and innovators), the other by pragmatists (the early majority). The early group makes their decisions based on their own analyses. They do not look to others for corroborative support. Pragmatists do. Indeed, word-of-mouth endorsements are by far the most impactful input not only about what to buy and when but also from whom.

Powered by WPeMatico

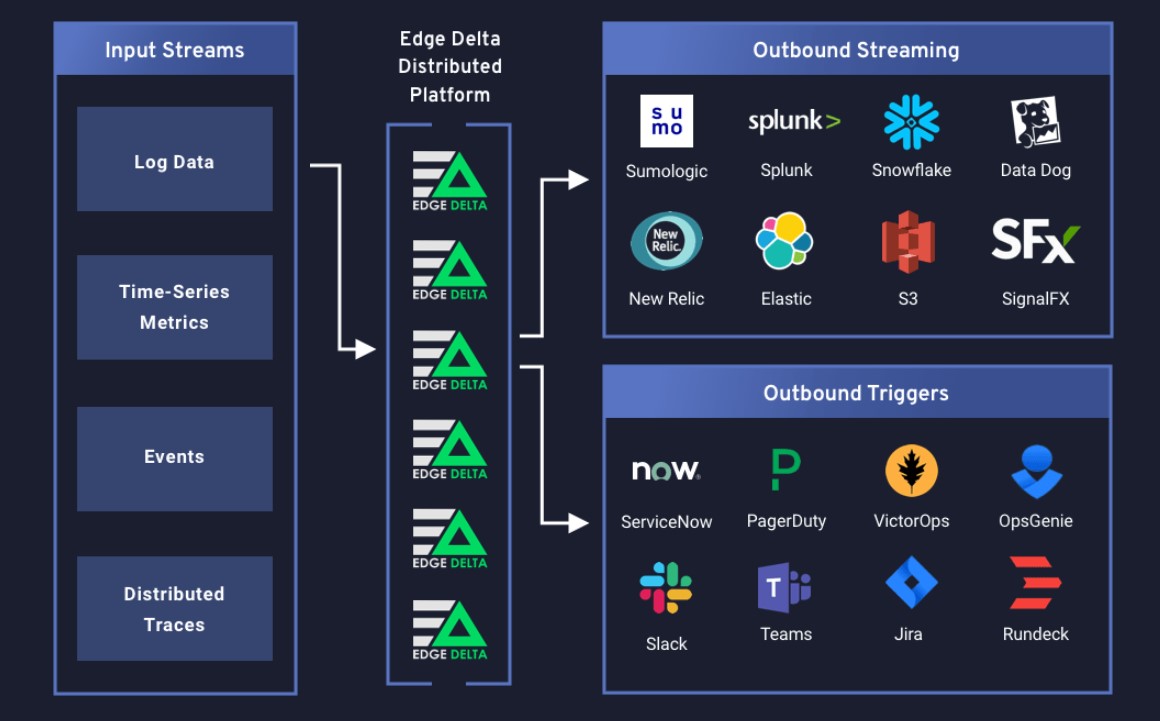

Seattle-based Edge Delta, a startup that is building a modern distributed monitoring stack that is competing directly with industry heavyweights like Splunk, New Relic and Datadog, today announced that it has raised a $15 million Series A funding round led by Menlo Ventures and Tim Tully, the former CTO of Splunk. Previous investors MaC Venture Capital and Amity Ventures also participated in this round, which brings the company’s total funding to date to $18 million.

“Our thesis is that there’s no way that enterprises today can continue to analyze all their data in real time,” said Edge Delta co-founder and CEO Ozan Unlu, who has worked in the observability space for about 15 years already (including at Microsoft and Sumo Logic). “The way that it was traditionally done with these primitive, centralized models — there’s just too much data. It worked 10 years ago, but gigabytes turned into terabytes and now terabytes are turning into petabytes. That whole model is breaking down.”

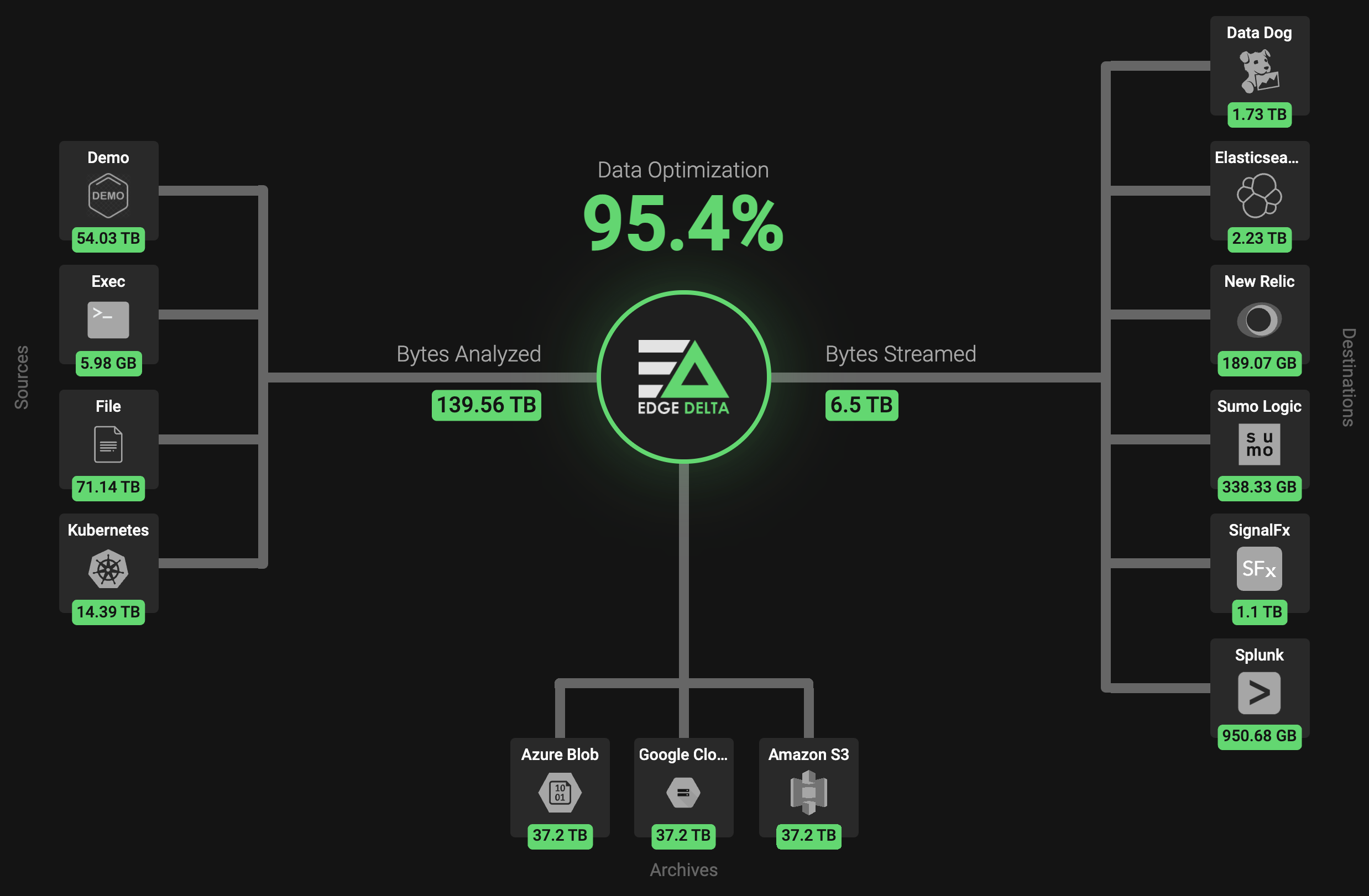

Image Credits: Edge Delta

He acknowledges that traditional big data warehousing works quite well for business intelligence and analytics use cases. But that’s not real-time and also involves moving a lot of data from where it’s generated to a centralized warehouse. The promise of Edge Delta is that it can offer all of the capabilities of this centralized model by allowing enterprises to start to analyze their logs, metrics, traces and other telemetry right at the source. This, in turn, also allows them to get visibility into all of the data that’s generated there, instead of many of today’s systems, which only provide insights into a small slice of this information.

While competing services tend to have agents that run on a customer’s machine, but typically only compress the data, encrypt it and then send it on to its final destination, Edge Delta’s agent starts analyzing the data right at the local level. With that, if you want to, for example, graph error rates from your Kubernetes cluster, you wouldn’t have to gather all of this data and send it off to your data warehouse where it has to be indexed before it can be analyzed and graphed.

With Edge Delta, you could instead have every single node draw its own graph, which Edge Delta can then combine later on. With this, Edge Delta argues, its agent is able to offer significant performance benefits, often by orders of magnitude. This also allows businesses to run their machine learning models at the edge, as well.

Image Credits: Edge Delta

“What I saw before I was leaving Splunk was that people were sort of being choosy about where they put workloads for a variety of reasons, including cost control,” said Menlo Ventures’ Tim Tully, who joined the firm only a couple of months ago. “So this idea that you can move some of the compute down to the edge and lower latency and do machine learning at the edge in a distributed way was incredibly fascinating to me.”

Edge Delta is able to offer a significantly cheaper service, in large part because it doesn’t have to run a lot of compute and manage huge storage pools itself since a lot of that is handled at the edge. And while the customers obviously still incur some overhead to provision this compute power, it’s still significantly less than what they would be paying for a comparable service. The company argues that it typically sees about a 90 percent improvement in total cost of ownership compared to traditional centralized services.

Image Credits: Edge Delta

Edge Delta charges based on volume and it is not shy to compare its prices with Splunk’s and does so right on its pricing calculator. Indeed, in talking to Tully and Unlu, Splunk was clearly on everybody’s mind.

“There’s kind of this concept of unbundling of Splunk,” Unlu said. “You have Snowflake and the data warehouse solutions coming in from one side, and they’re saying, ‘hey, if you don’t care about real time, go use us.’ And then we’re the other half of the equation, which is: actually there’s a lot of real-time operational use cases and this model is actually better for those massive stream processing datasets that you required to analyze in real time.”

But despite this competition, Edge Delta can still integrate with Splunk and similar services. Users can still take their data, ingest it through Edge Delta and then pass it on to the likes of Sumo Logic, Splunk, AWS’s S3 and other solutions.

Image Credits: Edge Delta

“If you follow the trajectory of Splunk, we had this whole idea of building this business around IoT and Splunk at the Edge — and we never really quite got there,” Tully said. “I think what we’re winding up seeing collectively is the edge actually means something a little bit different. […] The advances in distributed computing and sophistication of hardware at the edge allows these types of problems to be solved at a lower cost and lower latency.”

The Edge Delta team plans to use the new funding to expand its team and support all of the new customers that have shown interest in the product. For that, it is building out its go-to-market and marketing teams, as well as its customer success and support teams.

Powered by WPeMatico

Salesforce and AWS represent the two most successful cloud companies in their respective categories. Over the last few years the two cloud giants have had an evolving partnership. Today they announced plans for a new set of integration capabilities to make it easier to share data and build applications that cross the two platforms.

Patrick Stokes, EVP and GM for Platform at Salesforce, points out that the companies have worked together in the past to provide features like secure sharing between the two services, but they were hearing from customers that they wanted to take it further and today’s announcement is the first step towards making that happen.

“[The initial phases of the partnership] have really been massively successful. We’re learning a lot from each other and from our mutual customers about the types of things that they want to try to accomplish, both within the Salesforce portfolio of products, as well as all the Amazon products, so that the two solutions complement each other really nicely. And customers are asking us for more, and so we’re excited to enter into this next phase of our partnership,” Stokes explained.

He added, “The goal really is to unify our platforms, so bring [together] all the power of the Amazon services with all of the power of the of the Salesforce platform.” These capabilities could be the next step in accomplishing that.

This involves a couple of new features the companies are working on to help developers on both the platform and application side of the equation. For starters that includes enabling developers to virtualize Amazon data inside Salesforce without having to do all the coding to make that happen manually.

“More specifically, we’re going to virtualize Amazon data within the Salesforce platform, so whether you’re working with an S3 bucket, Amazon RDS or whatever it is we’re going to make it so that that the data is virtualized and just appears just like it’s native data on the Salesforce platform,” he said.

Similarly, developers building applications on Amazon will be able to access Salesforce data and have it appear natively in Amazon. This involves providing connectors between the two systems to make the data flow smoothly without a lot of coding to make that happen.

The companies are also announcing event sharing capabilities, which makes it easier for both Amazon and Salesforce customers to build microservices-based applications that cross both platforms.

“You can build microservices-oriented architecture that spans the services of Salesforce and Amazon platforms, again without having to write any code. To do that, [we’re developing] out of the box connectors so you can click and drag the events that you want.”

The companies are also announcing plans to make it easier from an identity and access management perspective to access the platforms with a guided setup. Finally, the companies are working on applications to build Amazon Chime communications tooling into Service Cloud and other Salesforce services to build things like virtual call centers using AWS machine learning technology.

Amazon VP of Global Marketing Rachel Thorton says that having the two cloud giants work together in this way should make it easier for developers to create solutions that span the two platforms. “I just think it unlocks such possibilities for developers, and the faster and more innovative developers can be, it just unlocks opportunities for businesses, and creates better customer experiences,” Thornton said.

It’s worth noting that Salesforce also has extensive partnerships with other cloud providers including Microsoft Azure and Google Cloud Platform.

As is typically the case with Salesforce announcements, while all of these capabilities are being announced today, they are still in the development stage and won’t go into beta testing until later this year with GA expected sometime next year. The companies are expected to release more details about the partnership at Dreamforce and re:Invent, their respective customer conferences later this year.

Powered by WPeMatico