automotive

Auto Added by WPeMatico

Auto Added by WPeMatico

Wall Street darling Tesla is holding on to its recent gains today on the back of a bullish analyst report, despite some weakness in tech shares.

Tesla has seen its value skyrocket in recent quarters, rising from a 52-week low share price of $211 to $1,548.81 today. That figure, however, is low in the eyes of some. Enter Piper Sandler.

The Piper analyst report, which was first released late Monday, gives Tesla a new price target of $2,322, up from the group’s prior price target of a little over $900 per share. The stock still has room to run, some believe, perhaps explaining some of the mania that related companies have seen in recent weeks, including fellow electric car manufacturers Nikola, Nio and others.

It was enough to prompt a “wow” from Tesla CEO Elon Musk via a tweet Monday evening.

Wow

— Elon Musk (@elonmusk) July 14, 2020

The Piper report cites two key factors for its new Tesla price target: The company’s edge in manufacturing and resulting unit volume, and the possibility that software will allow the company to eventually generate operating margins in the mid-20s.

On the manufacturing front, Piper increased its 2020 delivery estimates based on Tesla’s recent second-quarter numbers. The firm believes Tesla can hit its original 2020 delivery guidance of 500,000 units, which it notes is impressive, given factory closures due to COVID-19.

Piper suggested Tesla can scale rapidly in the coming years. The constraint isn’t customer demand, but instead capacity, the analyst suggested. Of course, building out production capacity is no small and cheap feat. Still, with customer demand wide open, Piper sees big revenue gains moving forward.

The latter argument feels more speculative. A 25% operating margin implies that the automotive company’s gross margins would need to be far higher, a seeming stretch for a company that sells molded metal and plastic in a competitive market.

The basis of Piper’s argument centers on Tesla’s software, specifically its FSD, or “full self-driving” feature, an $8,000 add-on that provides advanced driver assistance over its standard Autopilot system.

Let us provide some quick backstory so that everyone understands: Today, Tesla vehicles come standard with Autopilot, an advanced driver assistance system that offers a combination of adaptive cruise control and lane steering. Tesla once charged for this feature as well, but made it standard in April 2019.

The more robust and higher-functioning version of Autopilot is called full self-driving. FSD includes the parking feature Summon as well as Navigate on Autopilot, an active guidance system that navigates a car from a highway on-ramp to off-ramp, including interchanges and making lane changes. The system now recognizes and responds to traffic lights, as well.

Still, Tesla vehicles are not self-driving cars. The system requires a human driver to remain engaged at all times.

Piper believes the FSD price will continue to rise, driving up margins. The firm predicted the cost of FSD could rise as high as $40,000.

“Thanks to the high-margin nature of the FSD package, we think that by the 2030s, Tesla could conceivably be selling vehicles at cost — or even below cost — while still achieving higher operating margins,” Piper wrote.

There is a very material catch to all of this. Tesla is able to recognize FSD revenue on its balance sheet as it rolls out more features. In other words, Tesla has to keep improving the product to be able to capture that entire line item.

In the first-quarter earnings call, Tesla CFO Zachary Kirkhorn explained that the company takes “roughly half” of the FSD as revenue. The other half of it goes into deferred revenue.

“Our deferred revenue balance is continuing to grow,” he said at the time. “It’s a little bit over $600 million. And so as we release features with time, at the end of every quarter, we take a look at what features have been released, associated value and then we can release that from the deferred revenue into our financials for that quarter. And then cars going forward, once the feature is released, we can recognize that revenue.”

For Tesla shareholders, institutional and retail alike, Piper’s report is welcome. Now Tesla has to live up to raised expectations. The company reports earnings on July 22. TechCrunch will be tuned in.

Powered by WPeMatico

Electric vehicle startup Fisker Inc. said Wednesday it has raised $50 million, much needed capital that will go toward funding the next phase of engineering work on the company’s all-electric luxury SUV.

The startup is aiming to launch the Fisker Ocean SUV in 2022.

The Series C funding round was led by Moore Strategic Ventures LLC, the private investment vehicle of Louis M. Bacon, the billionaire hedge fund manager.

“Since we first showed the car at CES earlier this year, reaction from customers and investors has been extremely positive,” Fisker Inc. Chairman and CEO Henrik Fisker said in a statement. “We are radically challenging the conventional industry thinking around developing and selling cars and this capital will allow us to execute our planned timeline to start producing vehicles in 2022.”

The company is also beefing up its executive lineup to help push the project along. Fisker said it has hired Burkhard Huhnke as its CTO. Huhnke was the former vice president of e-mobility for Volkswagen America and vice president of automotive at chipmaker Synopses.

As CTO, Huhnke will spread his time between the company’s R&D work in Los Angeles and its new Fisker Innovation Lab in Silicon Valley.

Building a car company isn’t easy. Just ask Fisker. The well-known automotive designer, who was behind the Aston Martin V8 Vantage, Aston Martin DB9 and BMW Z8 among others, launched a startup called Fisker Automotive that aimed to produce a luxury plug-in hybrid electric vehicles. The flagship vehicle, the Fisker Karma, debuted at the 2008 North American International Auto Show, and first deliveries were in 2011. But the company ran into numerous challenges and production was suspended in November 2012 and ended in bankruptcy a year later.

China’s Wanxiang Group purchased what was left of Fisker in 2014 and launched a new company called Karma Automotive . On a side note: Karma, which has had its own financial struggles, also announced Wednesday it had raised $100 million.

This time around, Fisker is focused on an SUV. The Fisker Ocean, which was officially revealed in January at CES 2020, starts at $37,499 before applying any federal income tax credit or state incentives.

Powered by WPeMatico

Karma Automotive has raised a $100 million lifeline from outside investors, as reported by Bloomberg, with the struggling electric vehicle maker’s fortunes likely buoyed by the current market optimism on other EV companies, including Tesla. Karma is the reincarnated version of Fisker Automotive, which previously faced bankruptcy before being acquired by Wanxiang Group in 2014.

Karma Automotive has made more progress than Fisker ever did, including actually delivering around 500 of its inaugural Revero electric sport sedan in 2019. The company will be continuing to sell the Revero, which retails starting at around $140,000, and will also be looking to add a high-horsepower GTE version, as well as a supercar for an even higher-tier customer.

The automaker also says that it’s in discussions with a partner for a commercial delivery truck, which it intends to develop in prototype form by year’s end. There are a number of different companies pursuing delivery vans for use by courier companies, including UPS and FedEx, and the increase in e-commerce spending presents an opportunity for multiple players to succeed in this category, even as there is a rush on in terms of entrants.

Karma will also seek to leverage and extend the benefits of its fresh investment by shopping around its EV platform to other automakers and OEMs, the company says, and also will eventually expand beyond pure EVs to hybrid fuel vehicles. In short, it sounds like Karma is willing to try just about everything and anything to chart a path toward profitability, but time will tell if that’s intelligent opportunism, or scattershot desperation.

Powered by WPeMatico

TuSimple, the self-driving truck startup backed by Sina, Nvidia, UPS and Tier 1 supplier Mando Corporation, is headed back into the marketplace in search of new capital from investors. The company has hired investment bank Morgan Stanley to help it raise $250 million, according to multiple sources familiar with the effort.

Morgan Stanley recently sent potential investors an informational packet, viewed by TechCrunch, that provides a snapshot of the company and an overview of its business model, as well as a pitch on why the company is poised to succeed — all standard fare for companies seeking investors.

TuSimple declined to comment.

The search for new capital comes as TuSimple pushes to ramp up amid an increasingly crowded pool of potential rivals.

TuSimple is a unique animal in the niche category of self-driving trucks. It was founded in 2015 at a time when most of the attention and capital in the autonomous vehicle industry was focused on passenger cars, and more specifically robotaxis.

Autonomous trucking existed in relative obscurity until high-profile engineers from Google launched Otto, a self-driving truck startup that was quickly acquired by Uber in August 2016. Startups Embark and the now defunct Starsky Robotics also launched in 2016. Meanwhile, TuSimple quietly scaled. In late 2017, TuSimple raised $55 million with plans to use those funds to scale up testing to two full truck fleets in China and the U.S. By 2018, TuSimple started testing on public roads, beginning with a 120-mile highway stretch between Tucson and Phoenix in Arizona and another segment in Shanghai.

Others have emerged in the past two years, including Ike and Kodiak Robotics. Even Waymo is pursuing self-driving trucks. Waymo has talked about trucks since at least 2017, but its self-driving trucks division began noticeably ramping up operations after April 2019, when it hired more than a dozen engineers and the former CEO of failed consumer robotics startup Anki Robotics. More recently, Amazon-backed Aurora has stepped into trucks.

TuSimple stands out for a number of reasons. It has managed to raise $298 million with a valuation of more than $1 billion, putting it into unicorn status. It has a large workforce and well-known partners like UPS. It also has R&D centers and testing operations in China and the United States. TuSimple’s research and development occurs in Beijing and San Diego. It has test centers in Shanghai and Tucson, Arizona.

Its ties to, and operations in China can be viewed as a benefit or a potential risk due to the current tensions with the U.S. Some of TuSimple’s earliest investors are from China, as well as its founding team. Sina, operator of China’s biggest microblogging site Weibo, is one of TuSimple’s earliest investors. Composite Capital, a Hong Kong-based investment firm and previous investor, is also an investor.

In recent years, the company has worked to diversify its investor base, bringing in established North American players. UPS, which is a customer, took a minority stake in TuSimple in 2019. The company announced it added about $120 million to a Series D funding round led by Sina. The round included new participants, such as CDH Investments, Lavender Capital and Tier 1 supplier Mando Corporation.

TuSimple has continued to scale its operations. As of March 2020, the company was making about 20 autonomous trips between Arizona and Texas each week with a fleet of more than 40 autonomous trucks. All of the trucks have a human safety operator behind the wheel.

Powered by WPeMatico

Teleoperators who remotely monitor and control autonomous vehicles rely on high-performance connectivity to transfer 4K video, multiple audio streams and other data. Even a skosh of latency, jitter or packet loss could spell disaster for a teleoperator intervening to help an autonomous sidewalk delivery bot or even a robotaxi.

One Israeli startup, which spun out of video transmission technology company LiveU, has developed a connectivity platform aimed at ending unpredictable network behavior. Now, after a year as an independent company, DriveU.auto is coming out of stealth with $4 million in new funding.

The funding round was led by RAD group co-founder Zohar Zisapel and included participation from Two Lanterns Venture Partners, Yigal Jacoby, Kaedan Capital and other private investors. Francisco Partners is an existing shareholder. Alon Podhurst, who was vice president of sales at Israeli startup Cognata, has joined DriveU.auto as CEO.

The connectivity platform is designed specifically for teleoperations, a burgeoning technology used to support a variety of autonomous vehicle applications, including robotaxis, self-driving trucks and delivery drones.

DriveU.auto uses what it calls cellular bonding technology, 4K video encoding and advanced algorithms to adapt to changes on a network. Podhurst explained that the company’s “secret sauce” is how it fuses dynamic encoding and cellular network bonding to enable the level of connectivity needed for demanding AV use cases.

The platform provides the missing link for AV companies that want to deploy autonomous vehicles without a human safety driver, Podhurst told TechCrunch. It works in the two major use cases of teleoperations. Teleoperations can be used for direct driving, in which a remote human operator controls the autonomous vehicle. That operator can also use a teleoperations system for remote assistance such as providing high-level driving commands.

DriveU.auto started as a unit within LiveU. It was initially part of LiveU’s CTO office. Although it spun out as an independent company late last year and is now a standalone company, some of its shareholders also have stakes in LiveU.

DriveU.auto has demonstrated its platform with AV developers and Tier 1 suppliers on public roads in Europe, Israel, Japan and the United States, according to Prodhurst. The investment followed engagement with several customers that helped confirm market demand for its technology.

DriveU.auto isn’t sharing customer names. However, Podhurst was able to share that its product is being tested by companies developing delivery and robotaxi platforms, autonomous trucking technology as well as a Tier 1 supplier. DriveU.auto also has a long-term proof of concept agreement with another Tier 1 supplier.

Powered by WPeMatico

In another up for technology shares, software companies saw their values reach new heights today.

The day’s trading comes after a sell-off last week eased some of technology companies’ rebounds from their COVID-19 lows; stocks in tech companies have more than made up for their early-year declines in mid-2020, with the Nasdaq reaching 10,000 points before giving up some ground.

Today the Nasdaq Composite index rose 0.15% to 9,910.53 points, just a few bips short of its all-time highs. A thematic tech index focused on fintech also saw their values recover to a mote under previous highs. The S&P 500 fell 0.36% to close at $3,113.41 and the Dow Jones Industrial Average Index decreased 0.65% to $26,119.13.

But software companies, tech’s highest fliers, set new records as measured by the Bessemer cloud index. According to the Financial Times, the software-and-cloud tracking index has seen gains of more than 45% during the last year, a sharp advance during a year of economic uncertainty and occasional stock market carnage.

Looking around more broadly, tech shares with a bit more of a value flavor — GAAP profitability, regular dividends, etc. — performed well, with Apple setting new record highs as well. The smartphone giant and services shop is worth more than $1.5 trillion, underscoring how attractive stable-tech has proved in 2020. On the same theme, Microsoft is a few points from all-time highs, and is worth around $1.48 trillion.

But while software’s growth has proved attractive, as has the stability of megacorp tech shops, less certain bets have also proved attractive. Nikola, an electric vehicle company that went public recently in a reverse debut, is still worth around $26 billion despite having no reported revenue. On a similar theme, Tesla shares are up from around $225 a year ago to over $993 today, a gain of 340% or so. In Q1 2020 the company posted 38% year-over-year growth.

$420 per share feels like a long time ago.

Speaking of transportation, Uber and Lyft had separate announcements Wednesday that should have primed the ol’ investor pump. Instead, shares of both companies bopped from flat to slightly down throughout the day.

Uber announced Wednesday that it will manage an on-demand service for Marin County in the San Francisco Bay area, marking the company’s broader push to Software as a Service and public transit.

Transportation Authority of Marin (TAM) will pay Uber a subscription fee to use its management software to facilitate requesting, matching and tracking of its high-occupancy vehicle fleet, starting with a service that operates along the Highway 101 corridor. Marin Transit trips will show up in the Uber app and let users book and even share rides.

This fundamental piece of news should have appealed to investors. Today they responded with a resounding “meh,” even though it represents the first steps into generating a new stream of revenue.

Uber shares closed down 0.60% to $33.29.

Meanwhile, rival Lyft pledged Wednesday that every car, truck and SUV on its platform will be all electric or powered by another zero-emission technology by 2030, a commitment that will require the company to coax drivers to shift away from gas-powered vehicles.

The target, which Lyft plans to pursue with help from the Environmental Defense Fund, will stretch across multiple programs. It will include the company’s autonomous vehicles, the Express Drive rental car partner program for rideshare drivers, consumer rental cars for riders and personal cars that drivers use on the Lyft app.

Perhaps investors understand that even with a decade-long timeline, the target could be difficult to meet.

Lyft shares closed at $35.32, down 3.79%.

TechCrunch has slowed its public market coverage as tech equities have returned to a more stable period; that they have made back lost ground has been worth noting, but lower volatility has lowered the market’s newsworthiness. Still, from time-to-time when new all-time highs are hit, it’s worth putting our toes back into the water. And on days when different blocs of public tech set records, we can’t help but make a public note.

Tech and tech-ish stocks: still in fashion.

Powered by WPeMatico

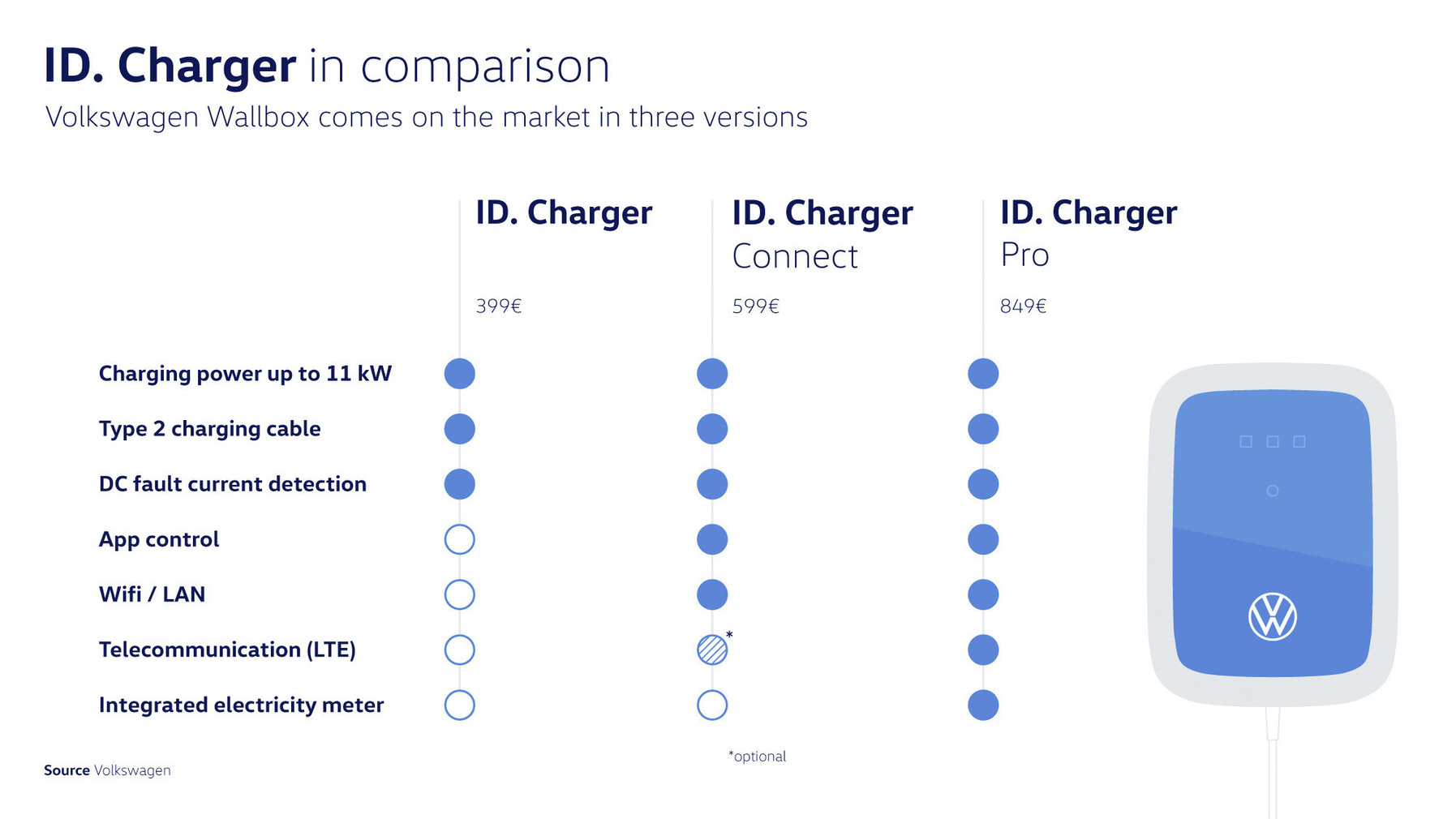

Volkswagen has started to sell a home-charging device as the automaker prepares to bring its new ID family of electric vehicles to market.

The ID.3 is the first electric vehicle under the ID label and will only be sold in Europe. Customers who made reservations for the launch edition, known as ID.3 1st, will be able to order their vehicle starting June 17. Volkswagen said this week that the deliveries for the ID.3 1st will begin in September.

And that means that, at least for now, the home-charging device known as Wallbox will only be available for sale in eight countries in Europe. Volkswagen is making three versions of the Wallbox that will range in price between €399 and €849 ($448 to $953). Those prices don’t include the cost of installation.

All of the versions will have a charging capacity of up to 11 kilowatts, permanently mounted Type 2 charging cable and integrated DC residual current protection. For now, just the base model is available, according to VW.

The two premium models, the ID. Charger Connect and ID. Charger Pro, will be available later this year. These models come with additional software that allows for the kind of interaction and analytics that Tesla owners are more familiar with. The ID. Charger Connect will allow customers to link their smartphone to control charging processes. The ID. Charger Pro has that connectivity feature plus an integrated electricity meter designed for commercial uses. The integrated meter can be used to bill electricity costs for company car drivers, according to VW.

Image Credits: Volkswagen

The ID.3 is the first model in the company’s new all-electric ID brand and the beginning of its ambitious plan to sell 1 million electric vehicles annually by 2025. The ID.3 will only be sold in Europe. Other models under the ID brand will be sold in North America.

Powered by WPeMatico

Yesterday evening, Vroom, a digital used car retailer, priced its IPO at $22 per share, a figure that was a full $7 above the low end of its first proposed IPO price range. The venture-backed firm first proposed a $15 to $17 per-share IPO price range, which it later raised to $18 to $20 per share.

Pricing at $22 per share meant that there was strong demand for the company’s equity during its IPO process. Pricing strength doesn’t guarantee performance as a public company, but it does provide a proxy for investor interest.

TechCrunch has covered a few IPOs lately, noting along the way that some recent offerings have featured heavy financial backing and incredibly slim margins. Not profit margins, mind, those don’t exist for the firms we’re talking about — we’re discussing gross margins, the most basic element of corporate profitability.

Gross margins are part of why software companies are so valuable. Their incredibly strong gross margins make their revenues, and therefore their operations, attractive to investors; higher gross margins mean more money left over to cover expenses and redistribute to shareholders via dividends and buybacks. Lower gross margin businesses, in contrast, have less money once they are done paying for revenue costs, making it harder for those companies to cover operating costs, let alone give away leftover funds to their owners.

So it has been to our surprise that Kingsoft Cloud, Vroom, and, soon, Lemonade are seeing such strong responses. It’s perhaps even more surprising that these companies managed to raise as much private capital as they did in their youth, despite not sporting gross margins that track with what we expect from venture-backed, tech and tech-ish companies.

With markets at all-time highs — and thus comparable valuations contentedly stretched — it’s probably a great time to take low-margin, growth-y companies public. But that doesn’t mean the situation makes perfect financial sense.

Powered by WPeMatico

Audi fired Daniel Abt from its Formula E racing team after learning he had a professional sim driver race for him during a virtual competition called the “Race at Home Challenge” held over the weekend.

The automaker said in a statement via Formula E that Abt had been suspended from Audi Sport “with immediate effect.” However, it appears the consequences are more serious and final. Abt said in a video message published Tuesday on YouTube that Audi had dropped him from the team.

“Today I was informed in a conversation with Audi that our ways will split from now on,” Abt said, according to a translation of the video message. “We won’t be racing together in Formula E anymore and the cooperation has ended. It is a pain which I have never felt in this way in my life.”

The 14-minute video was meant to explain the incident that occurred May 23 during the virtual competition, Abt said. He claims that it was all meant as a joke, which he intended to publicize after the race.

Abt tapped 18-year-old pro sim driver Lorenz Hoerzing to take his spot in the fifth round of Formula E’s online sim racing series. Unlike the real Formula E race series, this was meant to entertain fans and raise funds for UNICEF.

Hoerzing came in third in the race. Questions were raised almost immediately following the virtual event when Abt didn’t appear on the post-race interview.

Abt explained, via translation of the video, the plan.

“We had a conversation and the idea came up that it would be a funny move if a sim racer basically drove for me, to show the other, real drivers, what he is capable of and use the chance to drive against them,” Abt said. “We wanted to document it and create a funny story for the fans with it.”

Abt later added that it was never his intention to “get a result and keep quiet about it later on just to make me look better.”

Abt has also been fined €10,000, which will be sent to the charity.

You can watch the entire statement here.

Powered by WPeMatico

Even though it’s a vast sector in the midst of transformation, manufacturing is often overlooked by early-stage investors. We surveyed top VCs in the industry to gather their perspectives on the challenges and opportunities facing manufacturing.

Traditionally, manufacturing companies are capital-intensive and can be slow to implement new technology and processes. The investors in the survey below acknowledge the long-standing barriers facing founders in this space, yet they see large opportunities where startups can challenge incumbents.

These investors noted that the pandemic is bringing overnight change in the manufacturing world; old rules are being rewritten in the face of worker safety, remote work and the need for increased automation. According to Eclipse Ventures founder Lior Susan, “COVID-19 has exposed the systemic vulnerabilities inherent to manufacturing and supply chain and, as such, significant opportunities for innovation. The market was lukewarm for a long time — it’s time to turn up the heat.”

What trends are you most excited about in manufacturing from an investing perspective?

Digital solutions that offer manufacturers greater agility and resilience will become major areas of focus for investors. For example, manufacturers still reliant on manual assembly were unable to build products when factories closed due to the coronavirus lockdown. While nothing would have kept production at 100%, the ability to quickly pivot and engage software-defined processes would have allowed manufacturing lines to continue building with a skeleton crew (especially important for any facility required to implement social distancing). Such systems have remote monitoring capabilities and computer vision systems to flag defeats in real-time and halt production if necessary.

Powered by WPeMatico