autodesk

Auto Added by WPeMatico

Auto Added by WPeMatico

Every founder dreams of building a substantial company. For those who make it through the myriad challenges, it typically results in an exit. If it’s through an acquisition, that can mean cashing in your equity, paying back investors and rewarding long-time employees, but it also usually results in a loss of power and a substantially reduced role.

Some founders hang around for a while before leaving after an agreed-upon time period, while others depart right away because there is simply no role left for them. However it plays out, being acquired can be an emotional shock: The company you spent years building is no longer under your control,

We spoke to a couple of startup founders who went through this experience to learn what the acquisition process was like, and how it feels to give up something after pouring your heart and soul into building it.

There has to be some impetus to think about selling: Perhaps you’ve reached a point where growth stalls, or where you need to raise a substantial amount of cash to take you to the next level.

For Tracy Young, co-founder and former CEO at PlanGrid, the forcing event was reaching a point where she needed to raise funds to continue.

After growing a company that helped digitize building plans into a $100 million business, Young ended up selling it to Autodesk for $875 million in 2018. It was a substantial exit, but Young said it was more of a practical matter because the path to further growth was going to be an arduous one.

“When we got the offer from Autodesk, literally we would have had to execute flawlessly and the world had to stay good for the next three years for us to have the same outcome,” she said at a panel on exiting at TechCrunch Disrupt last week.

“As CEO, [my] job is to choose the best path forward for all stakeholders of the company — for our investors, for our team members, for our customers — and that was the path we chose.”

For Rami Essaid, who founded bot mitigation platform Distil Networks in 2011, slowing growth encouraged him to consider an exit. The company had reached around $25 million run rate, but a lack of momentum meant that shifting to a broader product portfolio would have been too heavy a lift.

Powered by WPeMatico

How and when should startup founders think about the “exit”? It’s the perennial question in tech entrepreneurialism, but the hows and whens are questions to which there are a multitude of answers. For one thing, new founders often forget that the terms of the exit may not eventually be entirely in their control. There’s the board to think of, the strategic direction of the company, the first-in investors, the last-in. You name it. We’ll be chatting about this at Disrupt 2020.

Exits normally happen in only one of two ways: Either the startup gets acquired for enough money to give the investors a return or it grows big enough to list on the public markets. And it just so happens we have two perfect founders who will be able to unpack their own journeys on those two roads.

When Cloudflare went public last year it certainly wasn’t the end of its 10-year journey, and nor was it PlanGrid’s when it was acquired by Autodesk in 2018.

Cloudflare’s Michelle Zatlyn saw every nook and cranny of the company’s journey toward its IPO, which received a warm reception, even if there were a few bumps along the road leading up to it. What comes after an IPO and how do you even get there in the first place? Zatlyn will be laying it all out for us.

PlanGrid’s journey to acquisition by Autodesk was equally fascinating, and Tracy Young — who, as CEO and co-founder, shepherded the company to an $875 million exit — will be able to give us insight into what it’s like to dance with a potential acquirer, go through that (often fraught) process and come out the other side.

We’re excited to host this conversation at Disrupt 2020 and expect it to fill up quickly. Grab your pass before this Friday to save up to $300 on this session and more.

Powered by WPeMatico

Data management company Datastax, one of the largest contributors to the Apache Cassandra project, today announced that it has acquired The Last Pickle (and no, I don’t know what’s up with that name either), a New Zealand-based Cassandra consulting and services firm that’s behind a number of popular open-source tools for the distributed NoSQL database.

As Datastax Chief Strategy Officer Sam Ramji, who you may remember from his recent tenure at Apigee, the Cloud Foundry Foundation, Google and Autodesk, told me, The Last Pickle is one of the premier Apache Cassandra consulting and services companies. The team there has been building Cassandra-based open source solutions for the likes of Spotify, T Mobile and AT&T since it was founded back in 2012. And while The Last Pickle is based in New Zealand, the company has engineers all over the world that do the heavy lifting and help these companies successfully implement the Cassandra database technology.

It’s worth mentioning that Last Pickle CEO Aaron Morton first discovered Cassandra when he worked for WETA Digital on the special effects for Avatar, where the team used Cassandra to allow the VFX artists to store their data.

“There’s two parts to what they do,” Ramji explained. “One is the very visible consulting, which has led them to become world experts in the operation of Cassandra. So as we automate Cassandra and as we improve the operability of the project with enterprises, their embodied wisdom about how to operate and scale Apache Cassandra is as good as it gets — the best in the world.” And The Last Pickle’s experience in building systems with tens of thousands of nodes — and the challenges that its customers face — is something Datastax can then offer to its customers as well.

And Datastax, of course, also plans to productize The Last Pickle’s open-source tools like the automated repair tool Reaper and the Medusa backup and restore system.

As both Ramji and Datastax VP of Engineering Josh McKenzie stressed, Cassandra has seen a lot of commercial development in recent years, with the likes of AWS now offering a managed Cassandra service, for example, but there wasn’t all that much hype around the project anymore. But they argue that’s a good thing. Now that it is over ten years old, Cassandra has been battle-hardened. For the last ten years, Ramji argues, the industry tried to figure out what the de factor standard for scale-out computing should be. By 2019, it became clear that Kubernetes was the answer to that.

“This next decade is about what is the de facto standard for scale-out data? We think that’s got certain affordances, certain structural needs and we think that the decades that Cassandra has spent getting harden puts it in a position to be data for that wave.”

McKenzie also noted that Cassandra provides users with a number of built-in features like support for mutiple data centers and geo-replication, rolling updates and live scaling, as well as wide support across programming languages, give it a number of advantages over competing databases.

“It’s easy to forget how much Cassandra gives you for free just based on its architecture,” he said. “Losing the power in an entire datacenter, upgrading the version of the database, hardware failing every day? No problem. The cluster is 100 percent always still up and available. The tooling and expertise of The Last Pickle really help bring all this distributed and resilient power into the hands of the masses.”

The two companies did not disclose the price of the acquisition.

Powered by WPeMatico

Brick & Mortar Ventures, a young, San Francisco-based venture firm that’s focused on startups innovating in or around architecture, engineering, construction and facilities management, has closed with $97.2 million in capital commitments.

The fund is one in a sea of debut funds that have swung open their doors in recent years, though it’s also interesting for numerous reasons, beginning with its founder, Darren Bechtel, who knows a thing or two about the building industry. He’s a scion of the family that built the 120-year-old, privately held company Bechtel into one of the largest construction and engineering firms in the world. In fact, his brother, Brendan, who was named CEO in 2016, represents the fifth generation of Bechtels to lead the company. (Their sister, Katherine, is a project controls manager with the powerhouse outfit.)

Brick & Mortar’s investors are just as notable. They aren’t the typical pension funds and university endowments that many VCs try hard to lock down. Instead, they comprise a long list of companies that are part of the “construction value chain” and so have an interest in the latest and greatest developments in their respective industries. Among the firm’s backers, for example, is the special materials maker Ardex; the software giant Autodesk; the building materials company CEMEX; Ferguson Ventures, which is the venture arm of a huge U.S distributor of plumbing supplies; FMI, a management consulting company to the engineering and construction industry; Obayashi, a major Japanese construction company; Sidewalk Labs, which is Alphabet’s urban innovation organization; and United Rentals, one of the world’s largest equipment rental companies.

Brick & Mortar isn’t the first venture firm to focus on the so-called built world. Other firms that focus largely, if not exclusively, around the same themes include Fifth Wall Ventures, Navitas Capital, Corigin Ventures, Camber Creek, MetaProp, Starwood Capital and Tamarisc Ventures.

In fact, Darren Bechtel has ties to and is an individual investor in Fifth Wall, an LA-based firm that stormed onto the scene in 2017 with an equally impressive, and very different, roster of limited partners in the real estate industry, from which it has already amassed more than $700 million in capital commitments across two funds.

As Bechtel told us on a call late last week, he was going to go into business with Fifth Wall’s founders initially, but they wanted to raise a lot of money, and Bechtel was thinking more conservatively — for a reason. “I’d done five deals on AngelList with [Fifth Wall co-founder] Brendan [Wallace] and we’d started putting together a pitch deck, and as we were thinking through ideal fund structure and size, Brendan said $500 million and I said $50 million,” says Bechtel.

Wallace was thinking big, says Bechtel, because “hospitality already had some massive players — Airbnb, WeWork. It was a far more mature landscape, and Brendan thought that if we were going to own a category, we needed the capital to secure a leadership position in the right deals.”

Bechtel thinks Wallace was right, too. He says he just came to realize that construction tech — which is what really interested him — was in its own league, and it was in its infancy. Though the construction software company PlanGrid took off like gangbusters — Bechtel wrote the largest check during the company’s seed round — it wasn’t so long ago that “there were great, billion-dollar ideas being formed but the rounds were small and the valuations were small,” says Bechtel. Because the “investment community didn’t understand what it was looking at, I had concerns about our ability to generate returns if we had too large a fund.”

In the end, the friends and former Stanford MBA classmates decided to split their respective focus on real estate and hospitality (Fifth Wall) and the actual construction of buildings (Brick & Mortar), and things seem to have gone well since. As Fifth Wall has gained traction, so too has Brick & Mortar, which is now a couple of years in the making. Indeed, though Bechtel is announcing the close of Brick & Mortar’s first fund today, he already works with two principals and two associates, and they’ve collectively sourced and funded 16 startups to date with capital they’ve been raising from investors along the way.

One of those checks went to Fieldwire, a maker of field management software for construction teams. They’ve also backed Serious Labs, which trains workers how to use heavy equipment and tools via virtual reality software, and Curbio, a real estate technology startup that orchestrates turnkey renovations for home sellers, then gets paid back once the home is sold.

Brick & Mortar even has an exit already, having helped fund the construction software platform BuildingConnected, which sold last December to Autodesk. (Bechtel’s earlier investment in PlanGrid, which also sold to Autodesk last year, was a personal investment, one of roughly 40 he made before setting out to create a traditional venture firm.)

As for whether Brick & Mortar ever hunts for companies that Bechtel — the firm founded by Darren’s great-great-grandfather — might like to acquire or otherwise partner with, Darren is quick to note that the firm is not an investor in his venture fund or any or its portfolio companies, and he doesn’t have his finger on the pulse of what’s happening there.

“I don’t work at Bechtel or pretend to know what their intentions are, though my brother is CEO, so you could say I know a guy there.”

More, he notes, he doesn’t think it would make sense to fund a company that “a user would want to acquire. If one user buys [a startup’s tools] because they want exclusivity, they’re limiting the exit value of that company.” To underscore his point, he notes that “Bechtel does around $30 billion a year, but the construction market is an $11 trillion market.” In the end, he says, it’s “better to have a preferred relationship. Maybe you get the next year’s model released early; maybe you get custom colors.” But if you’ve developed a winning product, you want to make it accessible to everyone. “You benefit the most by having a technology adopted by the whole industry.”

Above, the Brick & Mortar Ventures team. From left to right: Austin Yount, senior associate; Alice Leung, associate; Curtis Rodgers, principal; Darren Bechtel, general partner; and Kaustubh Pandya, principal.

Powered by WPeMatico

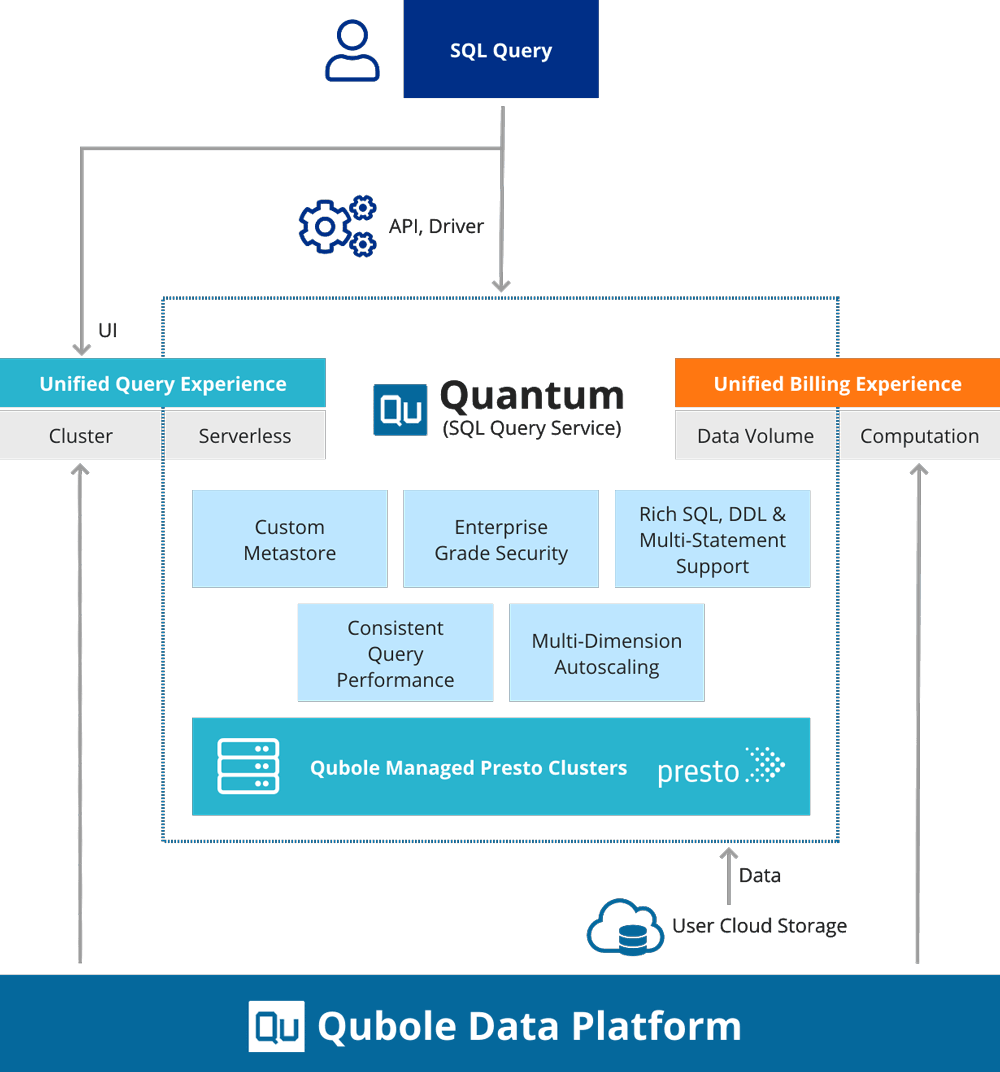

Qubole, the data platform founded by Apache Hive creator and former head of Facebook’s Data Infrastructure team Ashish Thusoo, today announced the launch of Quantum, its first serverless offering.

Qubole may not necessarily be a household name, but its customers include the likes of Autodesk, Comcast, Lyft, Nextdoor and Zillow . For these users, Qubole has long offered a self-service platform that allowed their data scientists and engineers to build their AI, machine learning and analytics workflows on the public cloud of their choice. The platform sits on top of open-source technologies like Apache Spark, Presto and Kafka, for example.

Typically, enterprises have to provision a considerable amount of resources to give these platforms the resources they need. These resources often go unused and the infrastructure can quickly become complex.

Qubole already abstracts most of this away, offering what is essentially a serverless platform. With Quantum, however, it is going a step further by launching a high-performance serverless SQL engine that allows users to query petabytes of data with nothing else but ANSI-SQL, giving them the choice between using a Presto cluster or a serverless SQL engine to run their queries, for example.

The data can be stored on AWS and users won’t have to set up a second data lake or move their data to another platform to use the SQL engine. Quantum automatically scales up or down as needed, of course, and users can still work with the same metastore for their data, no matter whether they choose the clustered or serverless option. Indeed, Quantum is essentially just another SQL engine without Qubole’s overall suite of engines.

Typically, Qubole charges enterprises by compute minutes. When using Quantum, the company uses the same metric, but enterprises pay for the execution time of the query. “So instead of the Qubole compute units being associated with the number of minutes the cluster was up and running, it is associated with the Qubole compute units consumed by that particular query or that particular workload, which is even more fine-grained,” Thusoo explained. “This works really well when you have to do interactive workloads.”

Thusoo notes that Quantum is targeted at analysts who often need to perform interactive queries on data stored in object stores. Qubole integrates with services like Tableau and Looker (which Google is now in the process of acquiring). “They suddenly get access to very elastic compute capacity, but they are able to come through a very familiar user interface,” Thusoo noted.

Powered by WPeMatico

Autodesk announced plans to acquire PlanGrid for $875 million today. The San Francisco startup helped move blueprints from paper to the iPad when it launched in 2011.

This digitization of construction fits with Autodesk’s vision of digitizing design in general, and CEO Andrew Anagnost certainly recognized the transformational potential of the company he was buying. “There is a huge opportunity to streamline all aspects of construction through digitization and automation. The acquisition of PlanGrid will accelerate our efforts to improve construction workflows for every stakeholder in the construction process,” he said in a statement.

The company, which is a 2012 graduate of Y Combinator, raised just $69 million, so this appears to be a healthy exit for the them. PlanGrid took what was a paper-intensive task and shifted it to digital, taking a world of hand-written mark-ups and sticky notes onto the fledgling iPad.

In an interview with CEO and co-founder Tracy Young in 2015 at TechCrunch Disrupt in San Francisco, she said the industry was ripe for change. “The heart of construction is just a lot of construction blueprints information. It’s all tracked on paper right now and they’re constantly, constantly changing,” Young said at the time.

Those manual changes often resulted in errors she said, and that was costly for the contractors. As an engineer working for a construction company, who was at one time responsible for making the paper copies, she recognized that the process could be improved by moving it into the digital realm.

PlanGrid CEO Tracy Young onstage at TechCrunch Disrupt San Francisco in 2015

Her idea, which was kind of radical in 2011 when she started the company, was to move all that paper to the cloud and display it on an iPad. It’s important to remember that the enterprise was not rushing to the cloud in 2011, and most people considered the iPad at the time to be a consumer device, so what she and her co-founders were attempting was a true kind of industry transformation.

Young sees joining Autodesk as a way to continue building on that early vision. “PlanGrid has excelled at building beautiful, simple field collaboration software, while Autodesk has focused on connecting design to construction. Together, we can drive greater productivity and predictability on the jobsite,” she said in a statement.

PlanGrid currently has 400 employees, 12,000 customers and 120,000 paid users, and has been used on over a million construction projects worldwide, according to data provided by the companies. They believe that under Autodesk’s umbrella and combined with their existing product set, they can provide a complete construction solution and grow the business faster than PlanGrid could have on its own — pretty much the standard argument in an acquisition like this.

PlanGrid was efficient with the money it took. In fact the last raise was $40 million almost exactly three years ago. The deal is expected to close at the end of January pending the normal regulatory approval process.

Powered by WPeMatico

Many entrepreneurs assume that an invention carries intrinsic value, but that assumption is a fallacy.

Here, the examples of the 19th and 20th century inventors Thomas Edison and Nikola Tesla are instructive. Even as aspiring entrepreneurs and inventors lionize Edison for his myriad inventions and business acumen, they conveniently fail to recognize Tesla, despite having far greater contributions to how we generate, move and harness power. Edison is the exception, with the legendary penniless Tesla as the norm.

Universities are the epicenter of pure innovation research. But the reality is that academic research is supported by tax dollars. The zero-sum game of attracting government funding is mastered by selling two concepts: Technical merit, and broader impact toward benefiting society as a whole. These concepts are usually at odds with building a company, which succeeds only by generating and maintaining competitive advantage through barriers to entry.

In rare cases, the transition from intellectual merit to barrier to entry is successful. In most cases, the technology, though cool, doesn’t give a fledgling company the competitive advantage it needs to exist among incumbents and inevitable copycats. Academics, having emphasized technical merit and broader impact to attract support for their research, often fail to solve for competitive advantage, thereby creating great technology in search of a business application.

Of course there are exceptions: Time and time again, whether it’s driven by hype or perceived existential threat, big incumbents will be quick to buy companies purely for technology. Cruise/GM (autonomous cars), DeepMind/Google (AI) and Nervana/Intel (AI chips). But as we move from 0-1 to 1-N in a given field, success is determined by winning talent over winning technology. Technology becomes less interesting; the onus is on the startup to build a real business.

If a startup chooses to take venture capital, it not only needs to build a real business, but one that will be valued in the billions. The question becomes how a startup can create a durable, attractive business, with a transient, short-lived technological advantage.

Most investors understand this stark reality. Unfortunately, while dabbling in technologies which appeared like magic to them during the cleantech boom, many investors were lured back into the innovation fallacy, believing that pure technological advancement would equal value creation. Many of them re-learned this lesson the hard way. As frontier technologies are attracting broader attention, I believe many are falling back into the innovation trap.

So what should aspiring frontier inventors solve for as they seek to invest capital to translate pure discovery to building billion-dollar companies? How can the technology be cast into an unfair advantage that will yield big margins and growth that underpin billion-dollar businesses?

Talent productivity: In this age of automation, human talent is scarce, and there is incredible value attributed to retaining and maximizing human creativity. Leading companies seek to gain an advantage by attracting the very best talent. If your technology can help you make more scarce talent more productive, or help your customers become more productive, then you are creating an unfair advantage internally, while establishing yourself as the de facto product for your customers.

Great companies such as Tesla and Google have built tools for their own scarce talent, and build products their customers, in their own ways, can’t do without. Microsoft mastered this with its Office products in the 1990s through innovation and acquisition, Autodesk with its creativity tools, and Amazon with its AWS Suite. Supercharging talent yields one of the most valuable sources of competitive advantage: switchover cost. When teams are empowered with tools they love, they will loathe the notion of migrating to shiny new objects, and stick to what helps them achieve their maximum potential.

Marketing and distribution efficiency: Companies are worth the markets they serve. They are valued for their audience and reach. Even if their products in of themselves don’t unlock the entire value of the market they serve, they will be valued for their potential to, at some point in the future, be able to sell to the customers that have been tee’d up with their brands. AOL leveraged cheap CD-ROMs and the postal system to get families online, and on email.

Dollar Shave Club leveraged social media and an otherwise abandoned demographic to lock down a sales channel that was ultimately valued at a billion dollars. The inventions in these examples were in how efficiently these companies built and accessed markets, which ultimately made them incredibly valuable.

Network effects: Its power has ultimately led to its abuse in startup fundraising pitches. LinkedIn, Facebook, Twitter and Instagram generate their network effects through internet and Mobile. Most marketplace companies need to undergo the arduous, expensive process of attracting vendors and customers. Uber identified macro trends (e.g. urban living) and leveraged technology (GPS in cheap smartphones) to yield massive growth in building up supply (drivers) and demand (riders).

Our portfolio company Zoox will benefit from every car benefiting from edge cases every vehicle encounters: akin to the driving population immediately learning from special situations any individual driver encounters. Startups should think about how their inventions can enable network effects where none existed, so that they are able to achieve massive scale and barriers by the time competitors inevitably get access to the same technology.

Offering an end-to-end solution: There isn’t intrinsic value in a piece of technology; it’s offering a complete solution that delivers on an unmet need deep-pocketed customers are begging for. Does your invention, when coupled to a few other products, yield a solution that’s worth far more than the sum of its parts? For example, are you selling a chip, along with design environments, sample neural network frameworks and data sets, that will empower your customers to deliver magical products? Or, in contrast, does it make more sense to offer standard chips, licensing software or tag data?

If the answer is to offer components of the solution, then prepare to enter a commodity, margin-eroding, race-to-the-bottom business. The former, “vertical” approach is characteristic of more nascent technologies, such as operating robots-taxis, quantum computing and launching small payloads into space. As the technology matures and becomes more modular, vendors can sell standard components into standard supply chains, but face the pressure of commoditization.

A simple example is personal computers, where Intel and Microsoft attracted outsized margins while other vendors of disk drives, motherboards, printers and memory faced crushing downward pricing pressure. As technology matures, the earlier vertical players must differentiate with their brands, reach to customers and differentiated product, while leveraging what’s likely going to be an endless number of vendors providing technology into their supply chains.

A magical new technology does not go far beyond the resumes of the founding team.

What gets me excited is how the team will leverage the innovation, and attract more amazing people to establish a dominant position in a market that doesn’t yet exist. Is this team and technology the kernel of a virtuous cycle that will punch above its weight to attract more money, more talent and be recognized for more than it’s product?

Powered by WPeMatico

Dropbox announced a couple of products today to make it easier for Autodesk users to access and share large design files. The products include an integrated desktop app for opening and saving Autodesk files stored in Dropbox and an app for viewing design files without the need for owning Autodesk. These products are long overdue given that Dropbox’s Ross Piper, who is head of ecosystem… Read More

Dropbox announced a couple of products today to make it easier for Autodesk users to access and share large design files. The products include an integrated desktop app for opening and saving Autodesk files stored in Dropbox and an app for viewing design files without the need for owning Autodesk. These products are long overdue given that Dropbox’s Ross Piper, who is head of ecosystem… Read More

Powered by WPeMatico

Imagine a world where manufacturing is no longer geographically mandated, when you can print custom parts in minutes, and anyone can build anything. That’s the world Amar Hanspal, Autodesk’s SVP or Product, wants to live in. I talked to Hanspal while he was at a future of manufacturing conference and we talked about all of the pitfalls of future manufacturing, the improvements… Read More

Imagine a world where manufacturing is no longer geographically mandated, when you can print custom parts in minutes, and anyone can build anything. That’s the world Amar Hanspal, Autodesk’s SVP or Product, wants to live in. I talked to Hanspal while he was at a future of manufacturing conference and we talked about all of the pitfalls of future manufacturing, the improvements… Read More

Powered by WPeMatico

When you think of Autodesk, you probably think of desktop software and traditional manufacturing, but the company is trying hard to change that perception, and today it announced the first three investments from its $100 million Forge Fund, which includes a 3D robotics drone company, an on-demand machine shop service and a platform for building smart connected Internet of Things devices… Read More

When you think of Autodesk, you probably think of desktop software and traditional manufacturing, but the company is trying hard to change that perception, and today it announced the first three investments from its $100 million Forge Fund, which includes a 3D robotics drone company, an on-demand machine shop service and a platform for building smart connected Internet of Things devices… Read More

Powered by WPeMatico