auto insurance

Auto Added by WPeMatico

Auto Added by WPeMatico

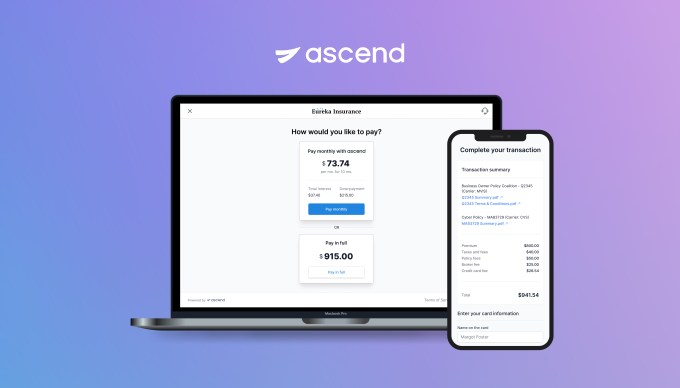

Ascend on Wednesday announced a $5.5 million seed round to further its insurance payments platform that combines financing, collections and payables.

First Round Capital led the round and was joined by Susa Ventures, FirstMark Capital, Box Group and a group of angel investors, including Coalition CEO Joshua Motta, Newfront Insurance executives Spike Lipkin and Gordon Wintrob, Vouch Insurance CEO Sam Hodges, Layr Insurance CEO Phillip Naples, Anzen Insurance CEO Max Bruner, Counterpart Insurance CEO Tanner Hackett, former Bunker Insurance CEO Chad Nitschke, SageSure executive Paul VanderMarck, Instacart co-founders Max Mullen and Brandon Leonardo and Houseparty co-founder Ben Rubin.

This is the first funding for the company that is live in 20 states. It developed payments APIs to automate end-to-end insurance payments and to offer a buy now, pay later financing option for distribution of commissions and carrier payables, something co-founder and co-CEO Andrew Wynn, said was rather unique to commercial insurance.

Wynn started the company in January 2021 with his co-founder Praveen Chekuri after working together at Instacart. They originally started Sheltr, which connected customers with trained maintenance professionals and was acquired by Hippo in 2019. While working with insurance companies they recognized how fast the insurance industry was modernizing, yet insurance sellers still struggled with customer experiences due to outdated payments processes. They started Ascend to solve that payments pain point.

The insurance industry is largely still operating on pen-and-paper — some 600 million paper checks are processed each year, Wynn said. He referred to insurance as a “spaghetti web of money movement” where payments can take up to 100 days to get to the insurance carrier from the customer as it makes its way through intermediaries. In addition, one of the only ways insurance companies can make a profit is by taking those hundreds of millions of dollars in payments and investing it.

Home and auto insurance can be broken up into payments, but the commercial side is not as customer friendly, Wynn said. Insurance is often paid in one lump sum annually, though, paying tens of thousands of dollars in one payment is not something every business customer can manage. Ascend is offering point-of-sale financing to enable insurance brokers to break up those commercial payments into monthly installments.

“Insurance carriers continue to focus on annual payments because they don’t have a choice,” he added. “They want all of their money up front so they can invest it. Our platform not only reduces the friction with payments by enabling customers to pay how they want to pay, but also helps carriers sell more insurance.”

Ascend app

Startups like Ascend aiming to disrupt the insurance industry are also attracting venture capital, with recent examples including Vouch and Marshmallow, which raised close to $100 million, while Insurify raised $100 million.

Wynn sees other companies doing verticalized payment software for other industries, like healthcare insurance, which he says is a “good sign for where the market is going.” This is where Wynn believes Ascend is competing, though some incumbents are offering premium financing, but not in the digital way Ascend is.

He intends to deploy the new funds into product development, go-to-market initiatives and new hires for its locations in New York and Palo Alto. He said the raise attracted a group of angel investors in the industry, who were looking for a product like this to help them sell more insurance versus building it from scratch.

Having only been around eight months, it is a bit early for Ascend to have some growth to discuss, but Wynn said the company signed its first customer in July and six more in the past month. The customers are big digital insurance brokerages and represent, together, $2.5 billion in premiums. He also expects to get licensed to operate as a full payment in processors in all states so the company can be in all 50 states by the end of the year.

The ultimate goal of the company is not to replace brokers, but to offer them the technology to be more efficient with their operations, Wynn said.

“Brokers are here to stay,” he added. “What will happen is that brokers who are tech-enabled will be able to serve customers nationally and run their business, collect payments, finance premiums and reduce backend operation friction.”

Bill Trenchard, partner at First Round Capital, met Wynn while he was still with Sheltr. He believes insurtech and fintech are following a similar story arc where disruptive companies are going to market with lower friction and better products and, being digital-first, are able to meet customers where they are.

By moving digital payments over to insurance, Ascend and others will lead the market, which is so big that there will be many opportunities for companies to be successful. The global commercial insurance market was valued at $692.33 billion in 2020, and expected to top $1 trillion by 2028.

Like other firms, First Round looks for team, product and market when it evaluates a potential investment and Trenchard said Ascend checked off those boxes. Not only did he like how quickly the team was moving to create momentum around themselves in terms of securing early pilots with customers, but also getting well known digital-first companies on board.

“The magic is in how to automate the underwriting, how to create a data moat and be a first mover — if you can do all three, that is great,” Trenchard said. “Instant approvals and using data to do a better job than others is a key advantage and is going to change how insurance is bought and sold.”

Powered by WPeMatico

Here in the U.S. the concept of using a driver’s data to decide the cost of auto insurance premiums is not a new one.

But in markets like Brazil, the idea is still considered relatively novel. A new startup called Justos claims it will be the first Brazilian insurer to use drivers’ data to reward those who drive safely by offering “fairer” prices.

And now Justos has raised about $2.8 million in a seed round led by Kaszek, one of the largest and most active VC firms in Latin America. Big Bets also participated in the round, along with the CEOs of seven unicorns, including Assaf Wand, CEO and co-founder of Hippo Insurance; David Vélez, founder and CEO of Nubank; Carlos Garcia, founder and CEO of Kavak; Sergio Furio, founder and CEO of Creditas; Patrick Sigrist, founder of iFood and Fritz Lanman, CEO of ClassPass. (There’s a seventh CEO who wishes to remain anonymous). Senior executives from Robinhood, Stripe, Wise, Carta and Capital One also put money in the round.

Serial entrepreneurs Dhaval Chadha, Jorge Soto Moreno and Antonio Molins co-founded Justos, having most recently worked at various Silicon Valley-based companies including ClassPass, Netflix and Airbnb.

“While we have been friends for a while, it was a coincidence that all three of us were thinking about building something new in Latin America,” Chadha said. “We spent two months studying possible paths, talking to people and investors in the United States, Brazil and Mexico, until we came up with the idea of creating an insurance company that can modernize the sector, starting with auto insurance.”

Ultimately, the trio decided that the auto insurance market would be an ideal sector considering that in Brazil, an estimated more than 70% of cars are not insured.

The process to get insurance in the country, by any accounts, is a slow one. It takes up to 72 hours to receive initial coverage and two weeks to receive the final insurance policy. Insurers also take their time in resolving claims related to car damages and loss due to accidents, the entrepreneurs say. They also charge that pricing is often not fair or transparent.

Justos aims to improve the whole auto insurance process in Brazil by measuring the way people drive to help price their insurance policies. Similar to Root here in the U.S., Justos intends to collect users’ data through their mobile phones so that it can “more accurately and assertively price different types of risk.” This way, the startup claims it can offer plans that are up to 30% cheaper than traditional plans, and grant discounts each month, according to the driving patterns of the previous month of each customer.

“We measure how safely people drive using the sensors on their cell phones,” Chadha said. “This allows us to offer cheaper insurance to users who drive well, thereby reducing biases that are inherent in the pricing models used by traditional insurance companies.”

Justos also plans to use artificial intelligence and computerized vision to analyze and process claims more quickly and machine learning for image analysis and to create bots that help accelerate claims processing.

“We are building a design-driven, mobile first and customer experience that aims to revolutionize insurance in Brazil, similar to what Nubank did with banking,” Chadha told TechCrunch. “We will be eliminating any hidden fees, a lot of the small text and insurance-specific jargon that is very confusing for customers.”

Justos will offer its product directly to its customers as well as through distribution channels like banks and brokers.

“By going direct to consumer, we are able to acquire users cheaper than our competitors and give back the savings to our users in the form of cheaper prices,” Chadha said.

Customers will be able to buy insurance through Justos’ app, website or even WhatsApp. For now, the company is only adding potential customers to a waitlist but plans to begin selling policies later this year..

During the pandemic, the auto insurance sector in Brazil declined by 1%, according to Chadha, who believes that indicates “there is latent demand raring to go once things open up again.”

Justos has a social good component as well. Justos intends to cap its profits and give any leftover revenue back to nonprofit organizations.

The company also has an ambitious goal: to help make insurance become universally accessible around the world and the roads safer in general.

“People will face everyday risks with a greater sense of safety and adventure. Road accidents will reduce drastically as a result of incentives for safer driving, and the streets will be safer,” Chadha said. “People, rather than profits, will become the focus of the insurance industry.”

Justos plans to use its new capital to set up operations, such as forming partnerships with reinsurers and an insurance company for fronting, since it is starting as an MGA (managing general agent).

It’s also working on building out its products such as apps, its back end and internal operations tools, as well as designing all its processes for underwriting, claims and finance. Justos’ data science team is also building out its own pricing model.

The startup will be focused on Brazil, with plans to eventually expand within Latin America, then Iberia and Asia.

Kaszek’s Andy Young said his firm was impressed by the team’s previous experience and passion for what they’re building.

“It’s a huge space, ripe for innovation and this is the type of team that can take it to the next level,” Young told TechCrunch. “The team has taken an approach to building an insurance platform that blends being consumer-centric and data-driven to produce something that is not only cheaper and rewards safety but as the brand implies in Portuguese, is fairer.”

Powered by WPeMatico

Caura, the U.K. startup that wants to take the hassle out of car ownership, is launching car insurance — unveiling its insurtech ambitions.

Dubbed “Caura Protect,” the new insurance product claims to reduce the cost and time taken to insure a car, building on the app’s existing car management features.

Launched earlier this year by Sai Lakshmi, who previously co-founded medication management service Echo, Caura is a mobile app designed to manage all of the vehicle-related admin that car owners endure.

Drivers are on-boarded by entering their vehicle registration number and can manage parking, tolls, MOT, road tax, congestion charges and now insurance — a “one-stop shop” app in a similar vein to Echo. The idea is that Caura minimises car ownership admin and helps to mitigate associated penalty fines.

Caura is FCA approved to undergo various insurance activities and enables drivers to compare insurers and manage their policy within the app. The startup also says it has redesigned the signup and verification process to significantly reduce the time needed to find the best insurance policy.

“Caura instantly verifies users against official sources like the DVLA, simplifying the experience, and reducing the risk of insurance fraud,” says the company.

The idea is to offer a much more user-friendly insurance search and buying process than is typical of price comparison websites that ask for a multiple-page questionnaire to be filled out before sending you — the “prospect” — to the insurer to complete your purchase. Instead, Caura claims that users can research options, select a quote, pay and be covered to drive in around a minute (if you navigate the app really fast, I’m assuming).

The insurance cover itself is provided by six of the leading U.K. insurers, including Aviva and Markerstudy. In early 2021, Caura users will be able to pay for insurance in monthly installments.

Asked why no one seems to have made shopping around for car insurance quite so straightforward, Lakshmi tells TechCrunch: “Startups in insurtech have been so busy finding niches that they’ve forgotten to innovate for the mainstream consumer”.

Powered by WPeMatico

I have struggled for years about whether or not to write a piece like this.

Speaking out about racism goes against every lesson I have learned since I was the only Black kid in my first-grade class in the Boston suburbs:

Save candid conversations about race for Black people. You’re being a victim. People will think you’re whining or making excuses. They’re not interested. Don’t make white people feel uncomfortable.

In a professional environment, speaking up could be career suicide. But now is not the time to be silent.

The startup I founded, Indenseo, is a data and analytics software insurtech company that provides automated underwriting services, software and analytics services to the insurance industry.

Despite strong customer relationships and support from angel investors, we didn’t complete building solutions and moving the company forward until we stopped taking unproductive pitch meetings with VCs. Some of my [white] colleagues who attended those meetings characterized these encounters as disrespectful and dismissive, but for me, they were par for the course.

I was raised by a single mother in West Medford, Massachusetts, and worked my way through Harvard, located about five miles away. Before starting Indenseo, I worked for @Road, a fleet management telematics company that was acquired by Trimble, a company that says it transforms “the way the world works by delivering products and services that connect the physical and digital worlds.” There, I led a team that pioneered the sale of telematics data, which started with using data for traffic predictions and expanded to other markets, including insurance.

At Trimble, I saw the difficulty legacy insurance carriers faced when they tried to incorporate new types of data into their underwriting and business processes; I started Indenseo to solve this problem by combining deep insurance industry experience with the nimbleness of a startup.

I knew fundraising would be a challenge: Commercial auto insurance has been unprofitable for years, and industry executives would be naturally skeptical that my solution would make it better. As my insurance industry friends said, “you sure picked a hard problem to solve.”

Even as a first-time founder, I did not anticipate how difficult it would be to raise venture funding, but the experience offered some insights into why so few Black entrepreneurs are funded by VCs.

Insurance is not the most mainstream venture category, though in recent years many insurtech companies have received funding. And VCs are not accustomed to seeing Black founders in this space. The overall scarcity of Black founders suggests that they’re not used to seeing many of us, period.

The odds of winning a venture round are low for everyone, but Black founders have a better chance playing pro sports than they do landing venture investments.

The odds of winning a venture round are low for everyone, but Black founders have a better chance playing pro sports than they do landing venture investments.

According to a Harvard study, between 1990 and 2016, just 0.4% of the entrepreneurs who received funding were Black. That’s 188 Black entrepreneurs, versus 34,000 white entrepreneurs in total, or about seven per year. In 2016, nine Black NFL quarterbacks started at least one game during the season. Should anyone wonder why ambitious young Black men pursue sports careers?

I got the meetings and pitched Indenseo to investors in Silicon Valley, New York City, Chicago and Boston. I expected that my experience, my best-in-class team, the compelling Indeseo proposition, market fit, and the financial and advisory backing of notable insurance executives would land the dollars, despite the odds. I was wrong.

One recurring phenomenon we frequently encountered were dismissive and disrespectful investors (in the words of a white colleague). When I had one disappointing meeting after another, people in my multiracial network — many with extensive fundraising experience — told me it didn’t make sense. I’d resisted getting distracted by race as a factor, but white colleagues were saying that something wasn’t adding up.

As Toni Morrison said, “The very serious function of racism is distraction. It keeps you from doing your work.” My own lived experience is that it’s an added factor that Black entrepreneurs have to manage.

I followed advice given to many Black founders: take a white colleague to your pitch meeting. I brought colleagues who had done a lot of fundraising themselves; some of these meetings were with their contacts. I tried this strategy dozens of times, and my colleagues were repeatedly shocked at the treatment we received.

I assumed most investors were jerks in pitch meetings, but they told me the level of disrespect and dismissiveness I received was not typical.

But if I lose my temper, I’d likely be labeled as just another angry Black man.

I did let my frustration show once when I directed a VC’s attention to the milestones we’d met and industry support we had gathered.

“What does it take for us to get a check from you?” I asked. His response: There is nothing you can say or do to get me to invest, but if you get another VC to lead the round, call me.

In another conversation with a VC, I pointed out the lack of diversity in both the ranks of investors and the entrepreneurs they choose to fund. He replied that Silicon Valley has produced the greatest accumulation of wealth in human history in the last 25 years. Why do we need to change anything?

GW Chew is a friend and a Black founder who was also having difficulty getting VC funding for his vegan meat company, Something Better Foods. He approached investors to raise funds to meet the fast expanding demand for his products. Talk about traction.

A white investor told Chew that if the founder/CEO were white, the company would have raised millions already. My friend told me he’s no longer talking to VCs and is raising funds from alternative sources.

Then there are the grifters. I don’t think Black founders are the only ones whose ideas get stolen after pitch meetings, but it happened to me.

We pitched a VC firm that had a consultant with an insurance background on their team to help evaluate the Indenseo opportunity. VCs don’t sign NDAs, but we did sign one with the consultant, who said Black founders can’t get companies funded but white founders can. (Yes, he said it.)

He later tried to ingratiate himself by saying he was considering investing too. Instead, he founded a company that copied our ideas. (So much for our NDA.)

Eventually, he told me, “I like your team. Call me when the wheels fall off.” When he announced his new company, we saw that he was backed by the VC who brought him into our meeting. He has since gone on to raise more than $40 million.

So why didn’t I sue him for violating the NDA? I consulted with some of our angel investors and they said we would be better off fighting them in the marketplace, given our limited time and resources. It wasn’t the first time our ideas were stolen.

When another company we pitched appropriated some of our ideas, my contact there informed his executives that they’d signed an NDA with Indenseo. Their reply: Indenseo doesn’t have the money to sue us. But they weren’t domain experts and we had left out much about our plans: They announced their launch in The Wall Street Journal, but as I expected, they failed.

Am I calling VCs racists? I don’t know what’s in their hearts, but I do know what’s in their numbers. Dealing with unconscious bias is difficult because as a Black entrepreneur trying to build a company, you know it exists and you have to figure out a way to manage around it. But it’s a subtle problem.

I don’t think VCs wake up in the morning and consciously decide not to invest in Black entrepreneurs or businesses intentionally choose not to buy from companies founded by Black entrepreneurs. But, the results of who receives investment and who doesn’t are quantifiable: few VC funds have Black employees or invest in companies started by Black founders.

I have never pitched at a VC firm that had a Black person in the room. And the pipeline excuse doesn’t work. There are Black people with technical degrees who aren’t hired at VC firms and white VC investment partners who earned liberal arts degrees.

Sure, there are funds started by Black VCs, but they encounter unconscious bias too when raising money. While more Black VCs with more capital is a crucial element of addressing underrepresentation, does that mean VC firms that aren’t founded by Black investors don’t have to change anything?

Deciding to stop the time-consuming VC pitch process and go in another direction to fund and develop the company was quite liberating. Moving forward, we’re free to manage our startup without wondering how VCs will view our decisions in the future when we seek funding.

We raised money from angel investors (including the former CEO of one of the world’s leading analytics software companies and his wife). In addition to money, it expanded our knowledge and it improved our products. Another lesson learned: Angel investors may be more helpful to your company than VCs.

The ultimate judgment on Indenseo’s products and team will be rendered by customers, partners and domain experts. The insurance industry has unique metrics that determine a company’s profitability. If you’re selling analytics software and services, either your solution is helping improve those metrics or it isn’t. The insurance industry is validating our market fit and survival skills.

I was able to build Indenseo without VCs because the insurance industry operates differently from VCs. One of the keys to success in the insurance industry is developing trust. Insurance isn’t a tangible product. It offers the promise that when a customer pays its premiums the insurance company will be able to support them when they file a claim. Without trust, a company can’t succeed in the industry.

There is a process to get insurance industry trust, and many senior executives in the industry are reluctant to invest the time in startups that’s necessary for them to get that trust. That’s because they aren’t convinced the startup will persevere to get through the process of getting that trust. We are able to get time with those executives because they trust our team and they don’t doubt that it’s worth their time to talk to Indenseo. They know we won’t fold when times are difficult.

A change I’ve seen since I started Indenseo that works in our favor is insurers don’t rely on VCs to act as a de facto screen for which insurtechs have the best teams and solutions. That’s because they don’t have confidence in investors’ judgments about insurtech companies.

Another lesson I’ve learned from my experiences: Don’t let VCs be the gatekeepers of your success. There are other funding sources, such as angel investors, corporate strategic investors, crowdfunding and more. There is funding outside the United States. Don’t overlook international investors: There is wealth in African countries. I found a way of funding the company that works for Indenseo.

We’ve developed Indenseo with angel investors and sweat equity. The key to our success is the amazing team, our advisory board and using capital efficiently. They remind me that you’re not the only one with an emotional investment in this company. When I started this company the only people in the insurance industry I knew were the people I had interacted with when I worked at Trimble.

Most of the people on our advisory board and team with insurance industry backgrounds are people I’ve met since I started Indenseo. It takes time to build those relationships. Because of them there is no corner of the commercial property casualty insurance industry we can’t access. The head of insurtech at a global reinsurance company told me that ours is the best balanced team of any insurtech company they’ve seen.

We are in the early stages of showing our flagship product, and it isn’t available for general release yet. Our VP of Engineering is telling me about a new concern: that we don’t take on too many customers too quickly.

Powered by WPeMatico

Root Insurance, an Ohio-based car insurance startup with a tech twist, said Wednesday it has raised $100 million in a Series D funding round led by Tiger Global Management, pushing the company’s valuation to $1 billion.

Redpoint Ventures, Ribbit Capital and Scale Venture Partners all participated as follow-on investors in this latest round.

The car insurance company, founded in 2015, plans to use the funds to expand into existing markets and make inroads into new states, as well as hire more employees such as engineers, actuaries, claims and customer service to support increased scale.

Root provides car insurance to drivers. Not exactly a new concept. But it establishes the premium customers based on their driving along with other factors. Drivers download the app and take a test drive that typically lasts two or three weeks. Then Root provides a quote that rewards good driving behavior and allows customers to switch their insurance policy. Customers can purchase and manage their policy through the mobile phone Root app.

Root says its approach allows good drivers to save more than 50 percent on their policies compared to traditional insurance carriers.

The company uses AI algorithms to adjust risk and sometimes provide discounts. For example, a vehicle with an advanced driver assistance system that it deems improves safety might receive further discounts.

“Root Insurance is leading digital innovation in U.S. auto insurance,” Lee Fixel, a partner at Tiger Global Management said in a statement. “This industry is ripe for change, and we are excited to invest in a team that has the expertise, vision, and momentum to deliver real results. We look forward to growing our partnership with Root and helping them expand their footprint across the United States.”

The company has grown from its home market of Ohio into 20 other states in the past two years. The company plans to expand to all 50 states and Washington, D.C., by the end of 2019.

Drive Capital and Silicon Valley Bank are also investors in the company.

Powered by WPeMatico

Alexander Timm has been working in the insurance industry since he was 14. While that’s strange enough, what’s even weirder is that Timm really loves the work. He’s so enamored of the business that he’s founded his own insurance company, Root Insurance, to remake the process of applying for — and insuring — drivers. There’s a lot happening in the… Read More

Alexander Timm has been working in the insurance industry since he was 14. While that’s strange enough, what’s even weirder is that Timm really loves the work. He’s so enamored of the business that he’s founded his own insurance company, Root Insurance, to remake the process of applying for — and insuring — drivers. There’s a lot happening in the… Read More

Powered by WPeMatico

A Chicago-based startup called Snapsheet has raised a Series C round of $20 million to make life easier for people who have been through a car crash.

A Chicago-based startup called Snapsheet has raised a Series C round of $20 million to make life easier for people who have been through a car crash.

The company’s cloud-based software is used by auto insurance providers to guide users through a photo- and information-gathering process on the scene of an accident. It is basically white labeled as a mobile app for each auto insurance… Read More

Powered by WPeMatico