atrium

Auto Added by WPeMatico

Auto Added by WPeMatico

Even in a non-hell year, running a successful startup is a tremendous lift. After the events of 2020, however, no doubt many already lean businesses are hanging on by the skin of their teeth. For every company that saw increased interest in their offerings during the pandemic, there were several that simply couldn’t make it through the finish line.

We’ve put this list together for several years now. It’s not a fun task, but it seems worthwhile to commemorate the startups that have closed up shop over the past 12 months. (Some of them were acquired by larger companies before shutting down, but all of them began their life as startups, and it still felt worthwhile to mark the end of their stories.) It also offers an opportunity to examine those issues from a bit of distance to see if there are any broader takeaways for the community at large.

This year’s list is among the most diverse we’ve done, ranging from standard smaller-name closures to big blockbuster crashes like Quibi and Essential . For some, the pandemic was the final nail in the coffin, but in many cases, cracks in business models were already starting to surface well before COVID-19 ground the global economy to a screeching halt.

Total Raised: $75 million

Atrium, a 100-person legal tech startup founded by Justin Kan, shut down in March after failing to find an efficient way to replace the arduous systems of law firms. The startup even returned some of its $75.5 million in funding to its investors, including Andreessen Horowitz.

The shutdown comes after the platform had pivoted just months earlier, laying off in-house lawyers and turning into a clearer SaaS play. Ultimately, Atrium’s failure shows how difficult and unprofitable it could be to disrupt a traditional and complicated system.

The closure came just three years after it launched with the goal to build software for startups to navigate fundraising, hiring, acquisition deals and collaboration with their legal team.

Total Raised: $330 million

Image Credits: Darrell Etherington

Big plans, big names and a boatload of money should have been enough to buy Essential a lengthy runway. Sure, Essential was entering a mature and oversaturated market, but the Playground-backed startup was doing so with $330 million in funding, a team of top industry executives and some genuinely innovative ideas.

When I spoke to the company at launch, an executive outlined a 10-year plan to become a major player in both the mobile and smart home categories. Ultimately, the company was able to eke out just under three years of life after coming out of stealth. And while it did give the world a promising handset, its connected home hub never arrived.

Timing, broader marketing issues and troubling allegations of sexual misconduct were all contributing factors that stopped Essential’s big plans dead in their tracks.

Total Raised: $11.4 million

Image Credits: HubHaus

HubHaus, founded by Shruti Merchant, was a long-term housing rental platform rooted in the belief that adult dormitories would take off. The startup targeted working professionals in cities, and raised only around $11 million in known venture capital. When it came to raising a Series B, Merchant says the company struggled to close and lost investor interest due to WeWork’s failed IPO.

After then pivoting to a self-funded company, HubHaus was just finding footing when the coronavirus pandemic arrived in the United States, drastically hurting the rental market (as shown by Airbnb’s public struggles, as well). The housing company eventually decided to close down in September, leaving landlords, members and vendors in limbo and bringing on a fresh sweep of critique and controversy.

Affordable housing continues to be an issue in the Bay Area, and HubHaus’s departure from the scene underscores this truth.

Total Raised: $55 million

Image Credits: Hipmunk

Hipmunk, founded by Adam J. Goldstein and Reddit co-founder Steve Huffman, was one of the first travel aggregation platforms on the market. The company put together information on flights, hotels and car rental all into one place so consumers could compare and contrast prices with ease.

The focus was enough for the platform to get acquired by Concur, but now after four years, the travel startup shut down. Notably, the travel startup’s closure wasn’t necessarily tied to the coronavirus pandemic. The site officially went dark on January 23, months before lockdowns came to the United States.

Total Raised: $51.4 million

Photo: Thomas Barwick/Getty Images

IfOnly had created a marketplaces of exclusive events — such as “goat yoga” — a business that faced obvious challenges during the pandemic. The startup was actually acquired by one of its investors, Mastercard, late last year, but the acquisition wasn’t announced until IfOnly revealed over the summer that it was shutting down.

Mastercard also said IfOnly’s team and technology are still part of its Priceless experience marketplace: “The IfOnly platform will continue to help advance our Priceless strategy and our combined team will be even better positioned and equipped to deliver exclusive experiences for cardholders globally.”

Mixer/Beam Interactive (2014-2020)

Total Raised: $520,000

Image Credits: Microsoft

Microsoft shut down its Twitch competitor Mixer this year, handing off its partnerships to Facebook Gaming. The service had its roots in the software giant’s acquisition of Beam Interactive shortly after the startup won TechCrunch’s Startup Battlefield in 2016.

Before giving up, Microsoft made some big investments in Mixer’s success, most notably signing streaming superstars Ninja and Shroud to exclusive deals. (They became free agents after the shutdown.) However, Microsoft’s gaming chief Phil Spencer said the company suffered from starting out “pretty far behind” the biggest players in the streaming market.

Total Raised: $10.2 million

Image Credits: The Outline

Despite a busy year of innovation and venture for news media platforms, The Outline, which branded itself as “the next generation version of the New Yorker” was shut down. The media site was started by Josh Topolsky and had an explicit focus on serving millennials with a digital-first news media brand.

The shutdown was part of a broader layoffs at Bustle Digital Group, which acquired the publication in 2019. Pre-acquisition, The Outline had already scaled back its editorial staff and refocused on freelance articles. (Input — a tech site that Topolsky founded for BDG — continues to publish.)

Periscope went out with more of a whimper than a bang. The startup was acquired by Twitter before it had even launched a product. With Meerkat bursting on the scene that year at SXSW, Twitter went on the offensive, buying the startup to build out its own live video offering.

Periscope’s run was decent as far as these things go, and its technology will live on as part of Twitter’s video offerings, even after the app is officially discontinued next March. But in the end, Periscope was a shell of its former self. In fact, this is a rare instance where the pandemic may have actually delayed its shutdown.

The company notes, “We probably would have made this decision sooner if it weren’t for all of the projects we reprioritized due to the events of 2020.”

Total Raised: $15.1 million

Image Credits: PicoBrew

The company made beer-brewing machines that used coffee pod-style PicoPaks, then expanded into other categories like coffee and tea, but never quite attracted enough customers to make the business viable. It sold its assets earlier this year to PB Funding Group — a group of lenders recruited by then-CEO Bill Mitchell in 2018 to keep it afloat.

It’s possible that PicoBrew will live on in some form, as PB Funding Group says it’s seeking buyers for the company’s patents and other intellectual property, and that it will keep the website running in the short term so that the machines don’t stop working.

Total Raised: $1.75 billion

Quibi CEO Meg Whitman speaks about the short-form video streaming service for mobile Quibi during a keynote address January 8, 2020 at the 2020 Consumer Electronics Show (CES) in Las Vegas, Nevada. (Photo by ROBYN BECK/AFP via Getty Images)

More so than any tech company in recent memory (with the possible exception of Theranos), Quibi’s existence feels like a fever dream. $1.75 billion in funding later and what do we have to show for it? “Fierce Queens,” a nature documentary about female animals. The HGTV-style program, “Murder House Flip.” And, of course, “The Shape of Pasta.” A show about pasta.

Early reports of the service’s demise seemed premature — if only because there was seemingly no way a company could burn through that much capital that quickly. By late-October, however, it was over. “All that is left now is to offer a profound apology for disappointing you and, ultimately, for letting you down,” founders Jeffrey Katzenberg and Meg Whitman wrote in an open letter.

Sometimes startup failures are bad timing. Sometimes it’s just plain bad luck. With Quibi, the diagnoses of what went wrong can be summed up in one word: everything.

Total Raised: $15 million

Image Credits: Rubica

Rubica spun out of security company Concentric Advisors with the aim of offering tools that were more advanced than antivirus software, while still remaining accessible to individuals and small businesses. CEO and co-founder Frances Dewing said that when customers cut back on spending during the pandemic, the company tried to shift its focus to larger enterprise, but it failed to convince investors there was a business there.

“We were all really surprised given how relevant and needed this is right now,” she said. “Investors didn’t agree with that or see it in the same way.”

Total Raised: $104 million

Businessman’s hands with calculator and cost at the office and Financial data analyzing counting on wood desk. Image Credits: Sarinya Pinngam/EyeEm / Getty Images

ScaleFactor was a startup claiming to offer artificial intelligence tools that could replace accountants for small businesses; it blamed the pandemic for cutting its revenue in half and forcing the company to shut down. However, former employees and customers told Forbes a different story — that ScaleFactor actually relied on human accountants (including an outsourced team in the Philippines) to do the work.

While it’s hardly unprecedented for a startup to fudge the truth about their level of automation versus human labor, this reportedly resulted in error-filled accounting for ScaleFactor clients. (Responding to a fact-checking email, former CEO Kurt Rathmann said the email was “filled with numerous factual inaccuracies and misrepresentation” and declined to comment further.)

Total Raised: $20 million

Self-driving trucks startup Starksy Robotics began with this first, and problematic truck. Image Credits: Starsky Robotics

“In 2019, our truck became the first fully-unmanned truck to drive on a live highway,” Starsky Robotics co-founder and CEO Stefan Seltz-Axmacher wrote in a Medium post in March. “And in 2020, we’re shutting down.” After five years and $20 million in funding, the autonomous trucking company shut its doors that month. It wasn’t for lack of ambition or demand — it seems safe to assume there’s still a bright future for self-driving trucks.

Ultimately, however, Starsky won’t be along for that ride — a fact Seltz-Axmacher blames largely on timing. A crowded market is certainly at play, as well, with countless companies currently pushing to bring autonomous technology to the road.

Total Raised: $10 million

Image Credits: Bryce Durbin

Founded in 2018 by ex-Googlers, Stockwell AI shut down after being unable to find business for its in-building smart vending machines that stocked everything from condoms to La Croix. The company blamed the “current landscape” (also known as the global pandemic we are experiencing) for its closure.

Stockwell AI, formerly known as Bodega, was well-funded and well-known, with more than $45 million in funding from investors that included NEA, GV, DCM Ventures, Forerunner, First Round and Homebrew. Still, even venture capital couldn’t make vending machines work well enough.

Total Raised: $2.5 million

Image Credits: Trover

Another travel-focused startup bites the dust as the coronavirus limits the chance to safely explore the world (let alone your neighborhood). Trover, a photo-sharing hub for travelers acquired by Expedia, shut down in August. The startup was founded by Rich Barton and Jason Karas and was meant to connect people travelling to the same places. The startup had quite the life: it began out of the remains of TravelPost, a travel review site, and got scooped up by its parent company when it only had $2.5 million in funding. Unfortunately, its nine-year journey is over for now.

Powered by WPeMatico

Justin Kan and Robin Chan have each been angel investing for more than a decade. They’re starting a new fund together now, though, to stay involved as cofounders of more startups.

Goat Capital is a hybrid incubator versus a pure seed investment firm, Chan explains. It will be writing checks ranging between roughly half a million and $3 million dollars, and it is only planning to raise $40 million — so the checks will be selective.

The offering is that “you’re going to be working with Justin and Robin,” he says, as a direct collaboration to help your company succeed. With $25 million closed already from themselves and several family offices, the fund has begun investing globally with particular interests in digital health, ecommerce, digital entertainment and gaming, robotics and climate change.

The goal is not just about being the Greatest Of All Time, Kan adds. In a startup, you “climb high heights and eat shit to get there. That tenacity is what we want.”

It’s a nod to their own successes and struggles as founders over the years, and what they have seen as investors and advisors to a wide range of companies around the world (Twitter, Xiaomi, Bird, Uber, Square, Ginkgo Bioworks, Scale.ai, Cruise, Razorpay, Xendit, Equipment Share, Wave, Teachable, Semantic Machines, Rippling, Built Robotics, etc.)

Kan was a cofounder of Justin.tv, which became Twitch as well as Socialcam. He later had an on-demand company called Exec and previously a calendar app called Kiko, both of which sold for small amounts. Most recently, he took a big shot at the traditional legal industry with Atrium, a law firm and legal software startup that raised big rounds of funding before shuttering earlier this year.

His prototype for Goat is Alto Pharmacy, a booming digital health unicorn today that the founders started in his living room.

“We do think founders should be treated like athletes, going for gold really hard… the Olympic metaphor,” Kan qualifies about the name. “That means grinding for years — and having to rest, too. I’m very passionate about mental health and wellness as part of the journey.” (More on that here.)

Chan, meanwhile, sold his gaming startup in China to Zynga a decade ago, then helped lead a failed attempt to buy Blackberry before founding Operator, a well-funded ecommerce company that closed a few years ago. During the pandemic, he helped create Operation Masks, a nonprofit that has been providing PPE across the US. He’s also an ongoing advisor to Sleeper, Bird, Expa and Flipboard.

The focus will be fully global now. Chan explains that even though you’re seeing more challenges to building a truly global company these days, there’s more space for local startups to win big.

“There’s the US internet, the China internet, the India internet, the EU internet — in some ways it makes those markets more valuable to win, like traditional media. Broadcast and cable are highly geographic but the franchise value becomes higher because of the regulatory moat.”

Chan, on that note, met Kan back when he was a director at [current TechCrunch owner] Verizon Wireless, when Justin.tv was trying to negotiate for free data. When I asked if they had worked out a deal during a phone interview, Kan said “you [expletive] didn’t.”

But it did lead to other co-investments later on, including Ramp, Workstream and others, and now this fund.

Today, Kan says that the focus on teams will be as flexible as the times. “When we started, the internet was America,” he says. “If you weren’t there, you weren’t a company. It’s been a complete reversal of that. Now teams are international, talent is international, more and more companies are building remote first — although you’d seen that before given the costs of the Bay. We have an entirely remote company in North Carolina, Grammarly in Europe… it’s more and more the norm. Smart founders are going anywhere to find talent.

For the two partners, this new fund will be about staying connected to that certain startup feeling that is elusive for anyone trying to build something great.

“There’s nothing more magical than being in the first step of a special company,” Chan says. “That glimpse of the future. We wouldn’t get the same feeling at the growth stage versus working with small teams or a single founder. I think we have the instinct.”

Powered by WPeMatico

Justin Kan’s hybrid legal software and law firm startup Atrium is shutting down today after failing to figure out how to deliver better efficiency than a traditional law firm, the CEO tells TechCrunch exclusively. The startup has now laid off all its employees, which totaled just over 100. It will return some of its $75.5 million in funding to investors, including Series B lead Andreessen Horowitz. The separate Atrium law firm will continue to operate.

“I’m really grateful to the customers and the team members who came along with me and our investors. It’s unfortunate that this wasn’t the outcome that we wanted but we’re thankful to everyone that came with us on the journey” said Kan. He’d previously founded Justin.tv which pivoted to become Twitch and later sold to Amazon for $970 million. “We decided to call it and wind down the startup operations. There will be some capital returned to investors post wind-down” Kan told me.

Atrium had attempted a pivot back in January, laying off its in-house lawyers to become a more pure software startup with better margins. Some of its lawyers formed a separate standalone legal firm and took on former Atrium clients. But Kan tells me that it was tough to regain momentum coming out of that change, which some Atrium customers tell me felt chaotic and left them unsure of their legal representation.

More layoffs quietly ensued as divisions connected to those lawyers were eliminated. But trying to build software for third-party lawyers, many of which have entrenched processes and older leadership, proved difficult. The streamlined workflows may not have seemed worth the thrash of adopting new technology.

“If you look at our original business model with the veritcalized law firm, a lot of these companies that have this kind of full stack model are not going to survive” Kan explained. “A lot of these companies, Atrium included, did not figure out how to make a dent in operational efficiency.”

Founded in 2017, Atrium built software for startups to navigate fundraising, hiring, acquisition deals, and collaboration with their legal team. Atrium also offered in-house lawyers that could provide counsel and best practices in these matters. The idea was that the collaboration software would make its lawyers more efficient than a traditional law firm so they could get work done faster, translating to savings for clients and Atrium.

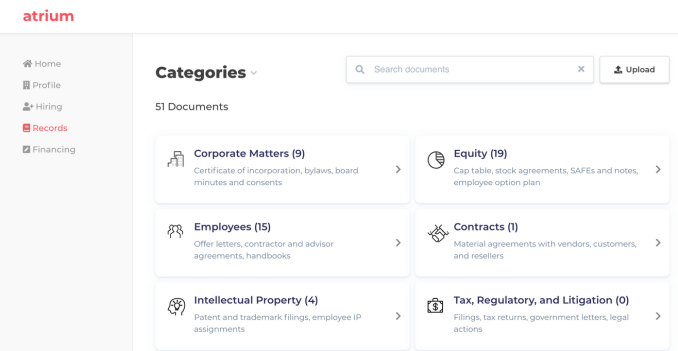

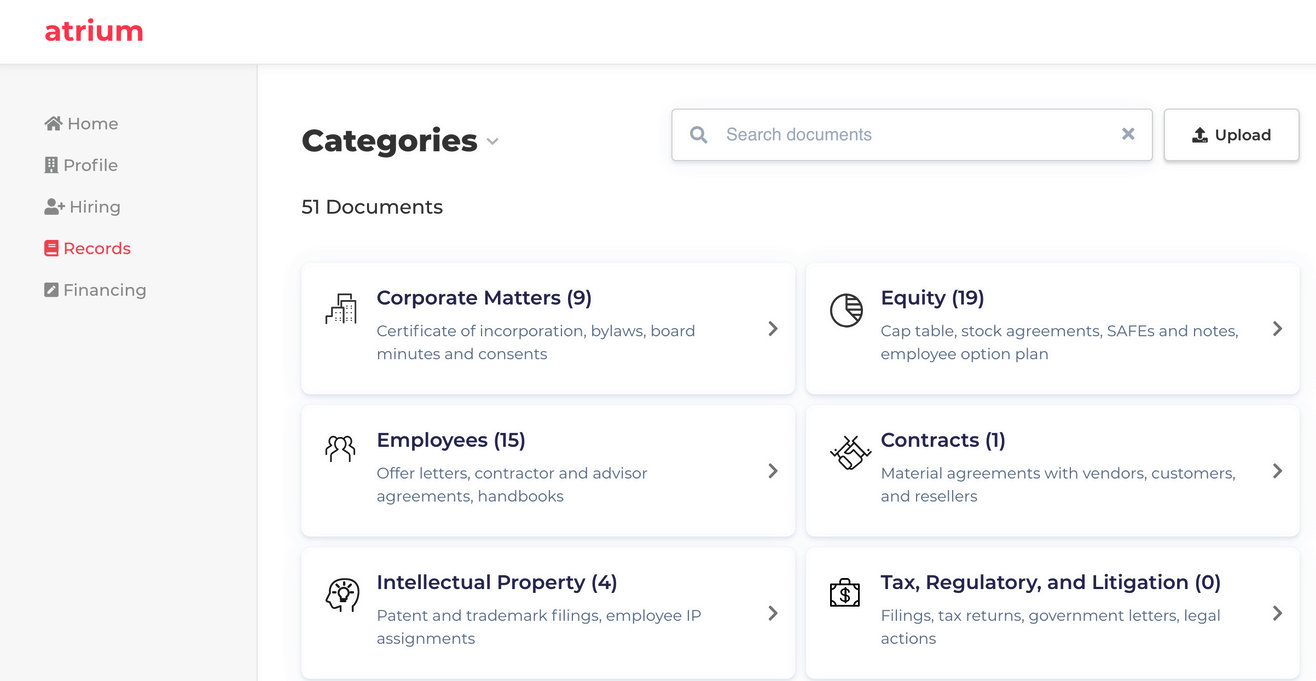

Atrium’s software included Records, a Dropbox-esque system for keeping track of legal documents, and Hiring, which instantly generated employment offer letters based on details punched into a form while keeping track of signatures. The startup hoped it could prevent clients and lawyers from wasting time digging through email chains or missing a sign-off that could put them in legal jeopardy.

The company tried to generate client leads by hosting fundraising workshops for startups, starring Kan and his stories from growing Twitch. A charismatic leader with a near-billion dollar exit under his belt, investors and founders alike were quick to buy into Kan’s vision and advice. Startups saw Atrium as an ally with industry expertise that could help them avoid dirty term sheets or botched hires.

But keeping a large squad of lawyers on staff proved costly. Atrium priced packages of its software and legal assistance under subscriptions, with momentous deals like acquisitions incurring add-on fees. The model relied less on milking clients with steep hourly rates measured down to six-minute increments like most law firms.

Yet eliminating the busy work for lawyers through its software didn’t materialize into bountiful profits. The pivot saught to create a professional services network where Atrium could route clients to attorneys. The layoffs had shaken faith in the startup as clients demanded stability lest they be caught without counsel at a tough time

Rather than trudge on, Kan decided to fold the company. The standalone Atrium law firm will continue to operate under partners Michel Narganes and Matthew Melville, but the startup developing legal software is done.

Atrium’s implosion could send ripples through the legaltech scene, and push other entrepreneurs to start with a more focused software-only approach.

Powered by WPeMatico

I am a chaplain trying to understand the tech world, and to me, that means I need to understand people like Justin Kan.

Who, after all, most “represents tech?” There are the obvious answers: secular deities like Bill Gates, Elon Musk or the late Steve Jobs. Or there are the often-marginalized figures on whom I’ve often preferred to focus in writing this column: the immigrant women of color who built the industry’s physical infrastructure; social workers and feminist philosophers who study how tech really works on a subconscious level, and how to fix it; or the next generation of leaders who represent the future of tech even as they worry about the inequalities they themselves embody.

But you can’t understand what has come to be the power and mystique of tech without also understanding the minds of its enigmatic founders. Justin Kan is a serial entrepreneur and founder who, whether you appreciate his public voice or not, certainly stands out as one of the most interesting examples of that classic Silicon Valley archetype: a tech entrepreneur ostensibly doing much more than just selling technology.

Kan famously started his business career not long after he graduated from Yale in 2005 by creating Justin.tv, a tech platform from which he broadcast his own life 24/7. Fifteen years later, Kan’s original idea seems quaint, given the level of self-promotion and oversharing that’s become commonplace. And yet, as he was arguably the first person to turn surveillance capitalism into not only overt performance art but also a noteworthy career in startups and venture capital, one can’t help but take the idea of Justin Kan seriously, at the very least as a harbinger of what is to come.

Powered by WPeMatico

The increase in activity in the pre-IPO secondary market means that founders, early employees, and investors are receiving liquidity much sooner in a company’s lifecycle than ever before. For most startups and privately-held companies, liquidity is often an issue for stockholders, as no market exists for selling shares and/or transfer restrictions can prevent their sale. Secondary stock transactions, however, are a way to work around this problem.

Here’s a quick look at how they work and what to keep in mind, especially if you’re going through the process for the first time. (If you’re not familiar, secondaries are transactions in which an existing stockholder sells their stock for cash to third parties or back to the company itself before the company undergoes an exit; traditionally, an exit refers to an M&A or an IPO.)

Offering secondary transactions to founders is a tool VCs have been using to win deals. For example, if a VC promises that the founders will receive $1,000,000 in cash through a secondary sale from a $15,000,000 venture financing round, the founders will likely prefer that VC’s term sheet to a term sheet from a VC that does not offer that deal.

Powered by WPeMatico

Law firms have little incentive to build or buy software that will save their lawyers time because they often bill clients by the hour. Tasks like tracking down legal documents, extracting key information and drawing up hiring offers or funding term sheets add up to make lawyers expensive, even if they’re constantly repeating mindless busy work.

That’s why legal startup Atrium is so exciting — even though it’s developing tech that might seem boring on the surface. After raising $75 million from Andreessen Horowitz and General Catalyst while growing to 400 clients, today Atrium is announcing its first customer-facing products.

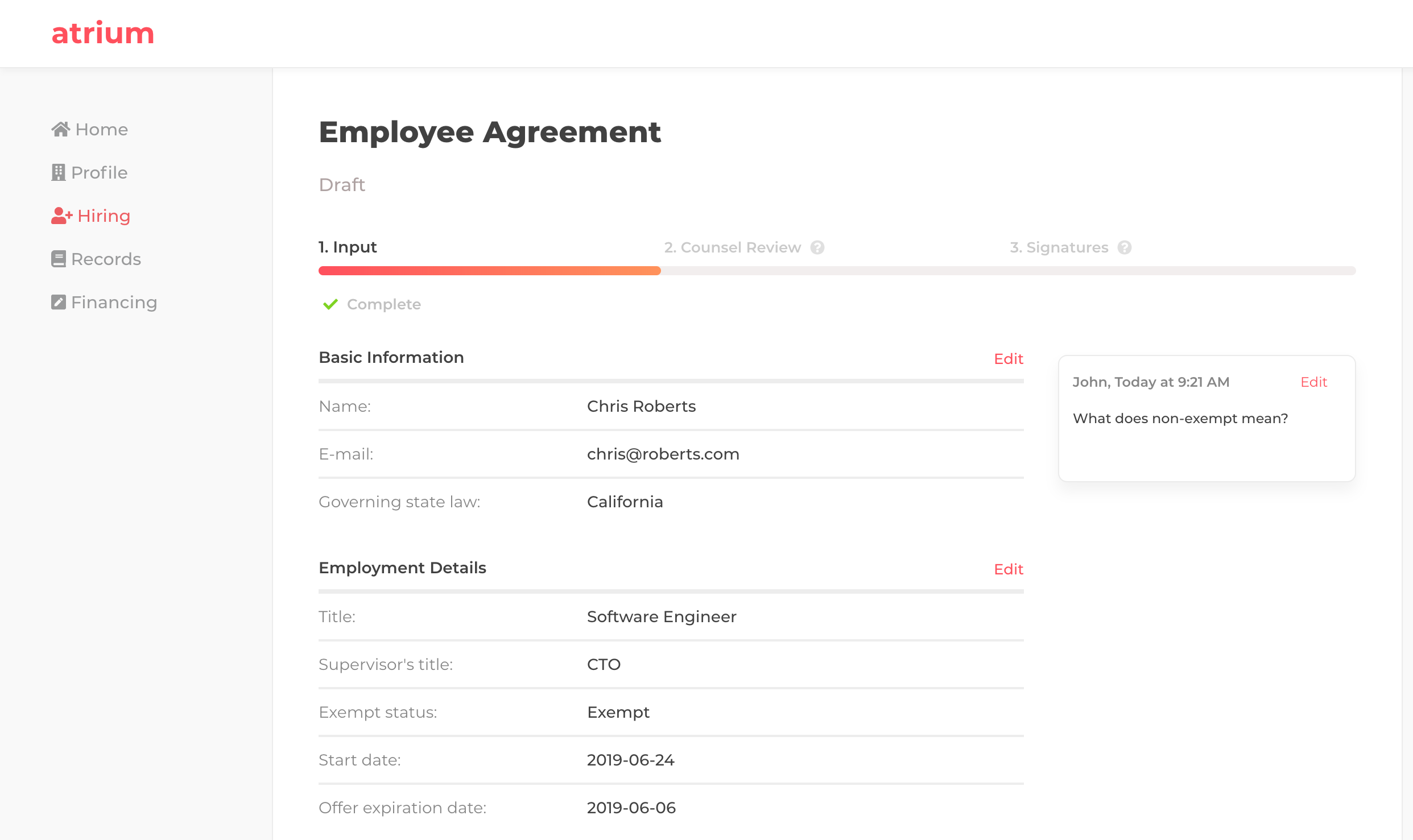

Atrium Records creates a collaborative file locker for you and your lawyer so you always have access to the latest versions of corporate documents. Atrium Hiring automatically generates hiring offers and contracts from details you add to a form, and tracks everyone’s approvals and signatures.

Atrium Records

Rather than having to pay for these tools separately, they come as part of a subscription to a bundle of Atrium’s legal services, with special projects like counsel through an acquisition costing extra. This business model incentivizes Atrium to work as efficiently as possible instead of bilking hourly rates, and build tools to eliminate less-skilled work or assist with common corporate duties. That’s allowed it to speed up legal work on incorporations, financings, M&A and contract negotiations.

“One of the reasons we partnered with Andreessen Horowitz on the last round [a $65 million Series B] was we really align with the way they approach venture capital,” Atrium co-founder and CEO Justin Kan tells me. “Marc’s initial observation was . . . let’s not just provide capital but also other services like a talent network. We have kind of done the same stuff. Not only are we helping people with the legal stuff they want to get done but with the other stuff surrounding it.”

Atrium CEO Justin Kan at TechCrunch Disrupt SF 2017

For example, Atrium’s Fundraising Concierge service provides assistance to startups for defining their narrative, setting up investor meetings and generating fair term sheets. Atrium has to date aided startups with raising more than $1 billion, from seed rounds of $200,000 to huge $50 million rounds

Developing drab but useful software for enterprises is a drastic shift for Kan. He pioneered life vlogging by strapping a camera to his head at his startup Justin.tv that eventually blossomed into Twitch and sold to Amazon for $1 billion. It’s been quite an adjustment for Kan going from making video-game-streaming consumer apps and angel investing to Atrium. “Two years. It has been an interesting and crazy ride. I wanted to get back to starting companies. That was the fastest learning I’d ever had. But I forgot learning means failing a lot,” he says with a wry smile.

Whatever tribulations they required seem worth it now that Atrium’s new products are ready. Atrium Records improves on the clumsy status quo where clients have to dig through emails from their lawyers hoping to find the most up-to-date versions of important corporate documents. If they can’t, they wait around after emailing their lawyer who has to hope they remember where they buried that term sheet or cap table in their firm’s file tree. This messy process can rack up billable hours, lead to data mismatches and let important signatures or approvals fall through the cracks.

Atrium Hiring

Kan says he’s seen some grisly situations. “You never signed your equity documents so you actually have no equity in this company. And now that there’s financing, there could be a taxable event. There’s often surprisingly serious problems that happen.” Atrium’s senior product manager Sahil Bhagat walks me through how Atrium can help clients avoid an issue like, “Maybe you hired 10 employees but didn’t update your cap table and then you’re hiring the 11th employee but you don’t have any equity to grant so you have to go through the hassle of increasing your options pool.”

Atrium Records acts like your searchable legal Dropbox. The startup works with your last law firm to ingest your documents around equity, taxes, employees and IP, and make sure they’re all up to date. Machine learning extracts critical data about financings and cap tables so that’s instantly available in the Atrium dashboard and you don’t have to dig into the original docs. Plus, you don’t have to pay for lawyers or paralegals to do that manually. And your lawyer can build a task list of documents for you to edit or sign so you always know what to do next, which is a relief when you’re wrangling approvals from all your existing investors.

Atrium Hiring operationalizes one of the biggest founder time-sucks. Instead of writing hiring contracts from scratch each time, you fill out a form and use menu selections to set the salary, share count, vesting schedule and offer expiration. Looking across its anonymized data set of contracts, Atrium can recommend the best clauses and most common set ups, like four-year vesting with one-year cliffs. You can see the status of the contracts every step of the way, from drafting and finalizing to getting employees to accept.

Kan tells me Atrium’s goal is to continue building on its archive of more than 100,000 legal documents to develop aggregated pools of data clients could opt into. If they’re willing to share their salary data, vendor contract pricing and more, they’ll get access to that of Atrium’s other clients. “You’ll be able to see if you’re on the high end of being paid by Salesforce for a contract,” Kan explains. That’s a much more data-driven approach than when most lawyers just think of the last few salaries they saw for that position and give you a rough average.

“Being able to tell what the market norms are is a powerful negotiating tool.” The startup has even been offering its tips for free as part of fundraising workshops it uses to attract clients. The challenge for the company will be ensuring efficiency doesn’t mean cutting corners.

Atrium has grown to 150 staffers split between legal practitioners and its product team in its two years since launch. Kan is trying to build a culture where everyone cooperates, unlike infamously cutthroat law firms where partners can compete for cases. He hopes that talent will stick with Atrium because it’s deleting the most tedious parts of their jobs. “No one wanted go to law school to review 1,000 hiring docs.”

Powered by WPeMatico

Let’s go beyond the high-level fundraising advice that fills VC blogs. If you have a compelling business and have educated yourself on crafting a pitch deck and getting warm intros to VCs, there are still specific questions about the strategy to follow for your fundraise.

How can you make your round “hot” and trigger a fear of missing out (FOMO) among investors? How can you fundraise faster to reduce the distraction it has on running your business?

“You’re trying to make a market for your equity. In order to make a market you need multiple people lining up at the same time.”

Unsurprisingly, I’ve noticed that experienced founders tend to be more systematic in the tactics they employ to raise capital. So I asked several who have raised tens (or hundreds) of millions in VC funding to share specific strategies for raising money on their terms. Here’s their advice.

(The three high-profile CEOs who agreed to share their specific playbooks requested anonymity so VCs don’t know which is theirs. I’ve nicknamed them Founder A, Founder B, and Founder C.)

Have additional fundraising tactics to share? Email me at eric.peckham@techcrunch.com.

“You’re trying to make a market for your equity. In order to make a market, you need multiple people lining up at the same time.”

That advice from Atrium CEO Justin Kan (a co-founder of companies like Twitch and former partner at Y Combinator) was reiterated by all the entrepreneurs I interviewed. Fundraising should be a sprint, not a marathon, otherwise the loss of momentum will make it more difficult.

Powered by WPeMatico

Microbiome pills, gambling for one-on-one video games and potential cancer cures were the highlights from legendary startup accelerator Y Combinator’s Winter 2018 Demo Day 2. You can read about all 64 startups that launched on Day 1 in verticals like biotech and robotics, our picks for the top 7 companies from Day 1 and our full coverage of another 64 startups from Day 2. TechCrunch’s writers huddled and took feedback from investors to create this list, so click (web) or scroll (mobile) to see our 8 picks for the top startups from Day 2.

Additional reporting by Greg Kumparak, Lucas Matney and Katie Roof

Powered by WPeMatico

Raising a Series A is hard for a founder. Especially when you consider they’re usually doing it for the first time, while the VCs on the other side of the table are essentially professional negotiators getting pitched and doing deals every day.

Raising a Series A is hard for a founder. Especially when you consider they’re usually doing it for the first time, while the VCs on the other side of the table are essentially professional negotiators getting pitched and doing deals every day.

So to help give founders a leg up Justin Kan’s new legal tech startup Atrium is launching a program to help founders become better… Read More

Powered by WPeMatico