Atomico

Auto Added by WPeMatico

Auto Added by WPeMatico

The startup investing market is crowded, expensive and rapid-fire today as venture capitalists work to preempt one another, hoping to deploy funds into hot companies before their competitors. The AI startup market may be even hotter than the average technology niche.

This should not surprise.

In the wake of the Microsoft-Nuance deal, The Exchange reported that it would be reasonable to anticipate an even more active and competitive market for AI-powered startups. Our thesis was that after Redmond dropped nearly $20 billion for the AI company, investors would have a fresh incentive to invest in upstarts with an AI focus or strong AI component; exits, especially large transactions, have a way of spurring investor interest in related companies.

That expectation is coming true. Investors The Exchange reached out to in recent days reported a fierce market for AI startups.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But don’t presume that investors are simply falling over one another to fund companies betting on a future that may or may not arrive. Per a Signal AI survey of 1,000 C-level executives, nearly 92% thought that companies should lean on AI to improve their decision-making processes. And 79% of respondents said that companies are already doing so.

The gap between the two numbers implies that there is space in the market for more corporations to learn to lean on AI-powered software solutions, while the first metric belies a huge total addressable market for startups constructing software built on a foundation of artificial intelligence.

Now deep in the second quarter, we’re diving back into the AI startup market this morning, leaning on notes from Blumberg Capital’s David Blumberg, Glasswing Ventures’ Rudina Seseri, Atomico’s Ben Blume and Jocelyn Goldfein of Zetta Venture Partners. We’ll start by looking at recent venture capital data regarding AI startups and dig into what VCs are seeing in both the U.S. and European markets before chatting about applied AI versus “core” AI — and in which context VCs might still care about the latter.

The exit market for AI startups is more than just the big Microsoft-Nuance deal. CB Insights reports that four of the largest five American tech companies have bought a dozen or more AI-focused startups to date, with Apple leading the pack with 29 such transactions.

Powered by WPeMatico

Sebastian Siemiatkowski, the co-founder and CEO of Klarna — the Swedish fintech “buy now, pay later” sensation that is currently Europe’s most valuable private tech company — is dismissive of the suggestion that non U.S. companies should relocate to Silicon Valley if they really want to grow.

“We did hear that and I think it’s very poor advice,” he says. An overheated market for tech talent and the fickle nature of employees that are constantly job-hopping, he argues, make it harder to build a company for the long term.

Then he goes further.

“When I went to San Francisco for the first time about 10 years ago, [it] was a magical place. It was the early days of Facebook, there was an amazing vibe. When I go to San Francisco today, it’s changed to become, in my opinion, fairly cold.”

Siemiatkowski, a Swedish national and the son of two immigrants from Poland, is also sceptical of the “American dream.” In contrast to America, he points out how Sweden is among the most successful societies in the world from a social mobility perspective — referencing its free education and free health care, which sets up as many people as possible for success. But there is one caveat: he doesn’t think first-generation immigrants in Sweden do nearly as well as their children.

“We didn’t have a lot of money,” he tells me. “My father was driving a cab, he was unemployed for many years, even though he had basically a doctorate in agronomy. That’s kind of the unfortunate part of this, but that has obviously created a massive amount of hunger with me.”

As second generation success stories go, the rise of Klarna is up there with the best, even if it has already been 15 years in the making.

Backed by the likes of Sequoia, Silverlake, and Atomico, a new $650 million funding round in September gave the company a whopping $10.65 billion valuation — almost double the price achieved a year earlier, cementing its status as a poster child for Europe’s ability to build tech companies valued far above $1 billion. Siemiatkowski still owns an 8.1 percent stake.

Klarna is also, perhaps, even more mythical than a unicorn: a fintech that has been profitable nearly from the get-go. That only changed in 2019, when it decided to incur losses in favor of investing millions trying to conquer the U.S. market, choosing New York and L.A. over San Francisco for its American offices.

The company has been built on the concept of giving consumers a way to buy things online without having to pay for them upfront, and without resorting to a credit card. It does this both by offering online retailer integrations where Klarna appears as an option at check out, and through its own “shopping mall” app, where users can browse all the stores that let you pay with Klarna. On the back of this, the company hopes to foster a bigger financial relationship with its users as a fully-fledged bank.

If a bank is partly about corralling enough users on to your platform to pay money in and out, Klarna is well on its way. Today, the company boasts a registered customer base of 90 million, 11 million of which are in the U.S. In the last year alone, 21 million users were added globally. Klarna’s direct to consumer app, which sits alongside its 200,000 strong merchant point of sale integrations, has 14 million active users globally. Combined, Klarna is processing over 1 million transactions per day through its platform.

Image Credits: Klarna

This growth has continued apace as Klarna rides one macro trend and bucks another: Prompted by the pandemic, e-commerce has gone gangbusters, while, conversely, consumer credit as a whole has been in decline as people are paying down longer-term debt in record numbers. Even before COVID-19, Klarna and other buy now, pay later providers had been successfully picking up the slack created by a credit card market that, in some countries, has been steadily contracting.

Yet with a business model that generates the majority of its revenue by offering consumers short-term credit — and against a backdrop where the idea of easy credit and infinite consumption is increasingly criticised — the fintech giant is not without detractors.

When I mention Klarna to people who work in the European tech industry, the reaction tends to fall into one of three camps: those who reference the company’s “weird” above the line advertising and social media campaigns; those who use the service regularly and talk in terms of guilty pleasures; and those who are outright scornful of the impact on society they perceive Klarna to be making. And it’s true: You can’t help but be suspicious of something that gives consumers the feeling that they can spend money they might not have. And those “Smoooth” ads (below) certainly don’t offer much reassurance.

Delve a little deeper, however, and it becomes clear that the company’s business model can be misunderstood and that the arguments playing out in the media for and against buy now, pay later is only one part of the Klarna story.

In a wide-ranging interview, Siemiatkowski confronts criticisms head on, including that Klarna makes it too easy to get into debt, and that buy now, pay later needs to be regulated. We also discuss Klarna’s business model and the balancing act required to win over consumers and keep merchants onside.

We also learn how, under his watch and as the company began to scale, Klarna missed the next big opportunity in fintech, instead being usurped by Adyen and Stripe. Siemiatkowski also shares what’s next for the company as it ventures further into the world of retail banking after gaining a bank license in 2017.

And, told publicly for the first time, Siemiatkowski reveals how he once sought out PayPal co-founder Max Levchin as an advisor, only to learn a little later that he had started Affirm, one of Klarna’s most direct U.S. competitors and sometimes described by Europeans as a Klarna clone.

But first, let’s go back to the beginning.

Klarna’s first ever transaction took place at 11:06:40 am on April 10, 2005 at a Swedish bookshop called Pocketklubben, according to the abbreviated history published on the company’s website. However, what is made less explicit is that there was likely very little technology involved. The real innovation was a business one, with Klarna’s young and non-technical founders, Sebastian Siemiatkowski, Niklas Adalberth and Victor Jacobsso, taking an old idea and reconfiguring it for the burgeoning e-commerce industry.

By enabling customers that shopped online to be mailed an invoice with 30 days to pay, online shopping could be made easier and safer for consumers, which in turn helped increase sales for retailers.

“The invoicing company”

“When they started, they didn’t position themselves so much as a startup or as a tech company,” recalls Skype founder Niklas Zennström, whose venture capital firm Atomico would eventually become a Klarna investor in 2012. “People referred to them as the invoicing company.”

Today, Klarna is most certainly a tech company, employing 1,300 software engineers out of a staff of over 3,500. The company is now entirely cloud based and with various fully automated processes, from credit risk processing to algorithms in the Klarna shopping app to personalize content for individual consumers to AI/machine learning for 24 hour customer service.

Crucially, however, even this early and rudimentary version of what would become ‘buy now, pay later’ ticked two important boxes. Consumers, especially those who were distrusting of e-commerce, could be sure they’d receive goods before being charged, and if for any reason a product needed to be returned, customers wouldn’t have to wait weeks to be reimbursed as they hadn’t outlaid cash in the first place. Arguably both problems were already solved by credit cards, but in countries like Sweden, credit card take up was low, while the humble debit card doesn’t carry the same consumer protections as a credit card.

“The reason that we were able to launch it and be successful was because we were in a market where debit cards were much more prevalent than credit cards,” says Siemiatkowski. “And most people who have credit cards don’t reflect on the fact that if you have a debit card and you shop online, you face a number of struggles that a credit card holder does not.”

Those “struggles” include tying up your own money for the time it takes to return an item and process a refund. In contrast, when you spend on a credit card, the merchant is effectively holding your credit card company’s money.

“If I am buying some items and feel a bit unsafe about the merchant I’m using, if there’s a credit card, I don’t feel like I’m risking my money. If it’s my salary money you’re actually holding as a merchant for three weeks while you’re processing the return, that’s a problem,” Siemiatkowski argues.

Instead, Klarna would step in and offer to pay the merchant up front while providing customers 30 days to settle their invoice. Later this would be extended to include installments as an option. In return for taking on all of the risk and promising to increase conversions, merchants would give the Swedish upstart a percentage cut of the transactions.

“They wanted to make it really simple by just putting in your name, your Social Security number, and then you can instantaneously get an option to get an invoice sent to you later on. So what it did was remove a lot of friction from buying,” says Zennström.

Meanwhile, the more retailers sold, the more revenue Klarna would generate, all without consumers having to be charged interest on what might otherwise be described as a short-term loan. Pitch perfect, you might think. However, in early 2005 and before the company was incorporated, the concept was stress-tested at a “Shark Tank”-style event held at the Stockholm School of Economics and attended by the King of Sweden. The judging panel, made up of prominent Swedish financiers, were not convinced and Klarna’s invoicing idea came last in the competition. Despite the loss, Siemiatkowski held on to feedback from an unknown member of the audience, who surmised that banks would never launch something similar. Siemiatkowski left undeterred.

Angel investment from a former Erlang Systems sales manager, Jane Walerud, followed and she put Klarna’s founders in contact with a team of developers who helped build the first version of the platform. However, it soon surfaced that there was a misunderstanding in relation to the equity promised and how it should be linked to a longer commitment to the project.

Reflects Siemiatkowski: “One of the drawbacks that we had at the company was that none of the three co-founders had any engineering background; we couldn’t code. We were connected to five engineers that by themselves were amazing engineers, but we had a slight misunderstanding. Their idea was that they were going to come in, build a prototype, ship it, and then leave for 37% of the equity. Our understanding was that they were going to come in, ship it, and if it started scaling they would stay with us and work for a longer period of time. This is the classic mistake that you do as a startup.”

Eventually, the original five engineers quit, leaving Siemiatkowski to manage something he didn’t understand. “We obviously hired a CTO, but I also needed to be able to evaluate his decision making and all of these things in order to be able to assess whether we had the right setup to achieve what we want to achieve,” he says.

Between 2006 and 2008, Klarna continued to grow as more people started shopping online. The company expanded beyond Sweden to neighboring Nordic countries Norway, Finland and Denmark, with a headcount that had reached 120 employees. Even though there were signs of growth, Siemiatkowski says it still took a long time to realise that if Klarna was ever going to be really successful, it needed to fully transform into a tech company.

“We were really good at sales, we were okay at marketing, [and] we were service oriented: we really delivered to our customers. But it wasn’t really that technology driven,” he concedes.

To attract the kind of tech talent required, Siemiatkowski decided he needed to woo a renowned tech investor. Further backing had come in 2007 from Swedish investment firm Investment AB Öresund, but by 2010 the Klarna CEO had two new targets in his sights: Niklas Zennström, the Swedish entrepreneur who had already achieved legend status back home after building and selling Skype, and Sequoia Capital, the Silicon Valley venture capital firm that had invested in Apple, Google and PayPal.

“Part of our thinking about how we make Klarna attractive for people with engineering backgrounds was to get an investor that really had the brand and could kind of put their mark on us and say, ‘this is a tech company,’” says Siemiatkowski.

There is every likelihood that Zennström’s Atomico would have joined Klarna’s cap table in 2010 if it weren’t for a single line of text published on the VC firm’s website, which read something like, “don’t contact us, we’ll contact you.” Europe’s startup ecosystem was still immature and what now seems like aloofness was probably nothing more than a crude way to deter cold pitches from non-venture type businesses. But whatever the intent, it would be another two years before the firm eventually had the opportunity to invest in Klarna at what was almost certainly a much higher valuation.

“That was our loss for being too arrogant,” says Zennström. “Clearly we didn’t pursue them, we didn’t discover them because we didn’t have them on our radar. When we got to know them [two years later], what we liked a lot as a firm was the pain point that they were addressing.

“E-commerce was a relatively low single digit penetration of all retail, but of course growing, and we have always believed that e-commerce is going to continue to grow and become bigger than physical retailers. We thought that if you can remove that friction of the payment, and offer people different payment methods, that’s a really big proposition.”

“I always tease Niklas about it,” admits Siemiatkowski. “They wanted to, you know, keep it exclusive and I get it. So we were like, ‘okay, we can’t get hold of them, so let’s talk to Sequoia instead.’”

However, cold calling Sequoia wasn’t going to cut it either, not only because the firm didn’t generally invest in Europe, but also by Siemiatkowski’s own admission, Klarna didn’t look much like a tech company at the time. Luckily, a mutual contact got wind that Sequoia was on the lookout for interesting companies in the region and Klarna’s name was promptly thrown into the mix.

“Chris [Olsen], who was working at Sequoia at the time, called me, [but] I had this idea that I needed to be hard to catch. So I decided to not call back for three days, which was a very nervous time where I was just sitting on my hands not doing anything,” he said. “It was like, I don’t want to look like I’m too interested in this. Eventually, after three days, I call back and we did an exclusive deal with them, which I don’t recommend companies do.”

In hindsight, the Klarna CEO advises that it’s always smarter to foster competition in a round. As the only show in town, Sequoia invested at a $100 million valuation. “They bought 25 percent of the company and that was kind of it,” he says.

Siemiatkowski believes a company is made up of three things.

The first he calls internal momentum: “How fast are we moving as an organisation? How good are the decisions we are taking? How much are we avoiding [company] politics? How much of a true meritocracy are we?”

The second is profit and loss.

And the third is valuation. In a small company these three things are closely correlated in time, he says, “so if you have great internal momentum, you will instantly see it in your P&L, and then you will instantly see that hopefully in your company valuation as well.”

But in a large company, because of its size, the challenge is that they start to become disconnected. “They’re obviously in the long term always 100% correlated, but in the short term, they can vary a lot,” cautions Siemiatkowski.

Unsurprisingly, fueled by Sequoia’s cash, Klarna continued to grow in 2010, ending the year with $54 million in annual revenue, an increase of 80%. In December 2011, General Atlantic and DST would invest $155 million in a round that gave Klarna the coveted status of a unicorn.

Siemiatkowski says, compared to the company’s subsequent $5.5 billion and $10.65 billion valuations, this is the one that put him under the most self-scrutiny.

“In just one and a half years, we went from $100 million to a $1 billion. And then I felt the pressure,” he tells me. “I felt like we made it such a competitive round because we wanted to compensate for what we saw partially as a mistake with Sequoia that we kind of went too far the other way.”

Klarna finally took Atomico’s money in 2012, and within two years had grown to over 1,000 employees. Along with multiple offices around the globe, the company moved to bigger headquarters in Stockholm and expanded to the U.K. with an office in central London. Yet, somewhere along the way, Siemiatkowski says Klarna had lost internal momentum.

“As the company scaled and we started adding more markets and growing fast, for me as CEO and co-founder, I found that very difficult,” he admits. “As long as we were up to 100 people, I found it easier, I understood how to talk to people, how to get things done, how to develop new products or features and so forth. It was all much less complex, and then we started approaching a couple of hundred people and I felt more and more lost in all of that.

“It was difficult, and at the same point of time, we still had a lot of success because we had built this product that worked really well and there was a lot of momentum coming solely from the product itself.”

Siemiatkowski says that most startups don’t recognize that “once you get the snowball rolling, you can actually do quite a lot of stupid things, and the snowball will continue rolling.”

The Klarna CEO doesn’t say it, but one of those “stupid things” came in 2012 when the startup faced a backlash in its home country. Instead of sending payment instructions in the post, the company had switched to email without considering that messages might go to spam or simply remain unread. This saw customers unintentionally defaulting and then being chased for payment, leading to accusations in the media that Klarna was tricking people so it could generate more revenue through late fees.

Powered by WPeMatico

Florida is renowned for its strange news stories. In recent weeks alone, one resident reported an alligator in her garage that turned out to be a pool floatie; another discovered a python in her washing machine; and a horse needed to be pulled out of a septic tank by firefighters.

Still, don’t dismiss Orlando residents who report seeing flying taxis overhead, because they may just be coming. Lilium Aviation, a five-year-old, Munich, Germany-based, venture-backed startup that designs and makes electric vertical take-off and landing jets, is reportedly seeking tax incentives from the city to build a 56,000-square-foot transportation hub with the promise that it will create 100 high-wage jobs in return.

According to the Orlando Business Sentinel, the proposed facility — a takeoff and landing area that would be part of Lilium’s first transportation network in the U.S. — would represent a $25 million investment and, according to the city’s own estimates, generate $1.7 million in economic impact in a 10-year period. (Lilium in September began separately exploring with Germany’s Düsseldorf Airport and Cologne Bonn Airport how to turn the two airports into regional air mobility hubs.)

It’s seemingly a smart time for Lilium — whose planes aren’t expected to be up and running until 2025 — to be talking with cities about additional airport revenue. Passenger traffic has fallen through the floor, owing to the pandemic, and cargo traffic has not been immune, either. Meanwhile, 95% of revenue from airports comes from aeronautical and non-aeronautical services.

Lilium also has a little more spending money after raising $35 million in fresh funding in June led by Baillie Gifford, the largest investor in Tesla — a round that brought the company’s total funding to date to $375 million.

Earlier investors in the company include Atomico, Tencent Holdings and Freigeist.

We sat down with Atomico founder Niklas Zennström in late 2016 when the firm had just led a €10 million Series A in Lilium. At the time, the bet seemed early, despite the existence of rivals like Terrafugia and AeroMobile, yet such vehicles may be an everyday reality sooner than imagined. Investors and founders seem to think so, at least. There are now at least 15 so-called flying cars and taxis in development.

Powered by WPeMatico

As part of Disrupt 2020 we wanted to look at the contrasting positions of both early and later-stage investing in Europe. Who better to unpack this subject than two highly experienced operators in these fields?

After a career at Spotify and then as a VC at Atomico, Sophia Bendz has rapidly gained a reputation in Europe as a keen early-stage investor. She recently left Atomico to pursue her early and seed-stage passion with Cherry Ventures. Bendz is a prolific angel investor, with a total of more than 44 deals in the last nine years. Her angel investments include AidenAI, Tictail, Joints Academy, Omnius, LifeX, Eastnine, Manual, Headvig, Simple Feast and Sana Labs. She is known for being a champion of the femtech space, and her angel investments in that space include Clue, Grace Health, Daye, O School and Boost Thyroid.

Carolina Brochado, the former Atomico partner and most recently a partner at SoftBank Vision Fund’s London office, recently joined EQT Ventures to help launch EQT’s Growth fund, which is positioned between ventures and private equity. Brochado led investments in a number of promising companies at Atomico, including logistics company OnTruck, health tech company Hinge Health and restaurant supply chain app Rekki.

After establishing that these two knew each other while at Atomico, I asked Bendz why she headed back into the seed-stage arena.

“I’m a trained marketeer and storyteller by heart… What makes me excited is new markets opportunities, people, culture, teams. So with that, in combination with my angel investing, I think I’m better suited to be in the earlier stages of investing. When I was investing before joining Atomico, I said to myself, I want to learn from the best, I want to see how it’s done, how you structure the process and how you think about the bigger investments.”

Brochado says the European “cat is out of the bag,” as it were:

When I first moved to Europe in 2012 and first joined Atomico, after having been at a very small startup, there was still a massive gap in funding and Europe versus the U.S. I think you know the European secret is no longer a secret, and you have incredible funds being started at that early-stage seed and Series A, and because I was here in 2012, I’ve seen the amazing pipeline of growth companies that are coming up the curve, how the momentum of those companies is accelerating and how the market cap of those businesses are growing. And so I just became super excited about helping those businesses scale… I just now felt like bridging that gap in between was really exciting.

One of the perennial topics that come up time and time again is whether or not founders should go with VC partners who have previously been operators, versus those with a finance background.

“Looking back, my years at Spotify, we had great investors, but there were not many of them that had the experience of scaling a big company,” Bendz said. “So, I’m happy to give [a startup] more than just the check in a way that I would have wished I had a sounding board when I was 25 and tackling that challenge at Spotify.”

Brochado concurred: “Having operators in the room is just is an incredible gift I think to a fund and at certain levels, having people that understand you know different forms of financing and different structures can also be incredibly helpful to founders who may not necessarily have that background. So I think that the funds that do it best have that diversity.”

Bendz is passionate about investing in female founders and femtech: “It’s such a massive business opportunity that is completely untapped. We’ve seen it many times when you have a female investment partner [that] the pipeline opens up and you get more deal flow from female founders…. So I think we have a lot of work to do. I think it’s definitely improved a lot in the last couple of years but not enough… That is one of the drivers for why I put my money where my mouth is and invest in lifting the founders, but also because there are incredibly interesting business opportunities… There are so many opportunities and products or services that we will see being developed. When we have a more equal society, and more women, both building their own companies, coding and also investing… I can’t wait to see what that world will look like.”

Brochado’s view is that “even beyond founders… the best managers today are putting a lot of focus on this and I think what’s exciting is, I think we’re past the point where you have to explain to people why diversity matters.”

Is there a post-Series A chasm?

Bendz thinks: “We have more big funds in Europe [now]. We have a really solid ground here in Europe of A, B and C investors.”

Brochado said: “It’s definitely getting better. You don’t hear as many founders say that to do my Series B or my Series C I have to move to the Valley as you used to. But there’s a lot of room still for growth investors in Europe. I think Series B is the hardest round actually because, at seed or Series A, you can raise on very early traction or the quality of the management team. At Series B the price goes up but the risk doesn’t necessarily go down as much. And so I think that’s where you really need investors who are sector or thematic focused, who can come with conviction and also some knowledge around the company to really propel that company forward.”

Did they both see European entrepreneurs still making silly mistakes, or has the ecosystem mastered?

Brochado thinks 10 years ago it was hard for European founders as a lot of the talent to scale companies was still in the U.S. “What you’ve seen is a lot of big companies grow up in Europe, a lot of people come back from the U.S., and so I think that pool of talent now is larger, which is very helpful. I don’t think it’s yet at the scale of where the U.S. is. But it gives us, you know as investors, a great window of opportunity to help get some of that talent for our portfolio companies.”

The impact of COVID-19

Bendz thinks we will “see a much slower spring, but… I think it has been overall a good exercise for some companies, and I have not seen a slower deal flow. I’ve actually done more angel deals this spring than I normally do… Some businesses have definitely accelerated their whole business concept because of COVID. Investments are being made even though we haven’t met the founders. We’re able to do everything remotely so I think the system is kind of adjusting.”

Brochado’s view is that at the growth stage “there’s been a flight to quality. So actually, the really great companies or the companies that are seeing great tailwinds or companies that will still be category-leading once [have] seen a lot of interest. It’s been a very busy summer, which usually it isn’t, particularly at the growth stage… I think a lot of money is still in the system, and has flown into technology. And so if you look at how tech in the public markets has performed it’s performed extremely well. And that includes European public companies and within tech.”

Watch the full panel below.

Powered by WPeMatico

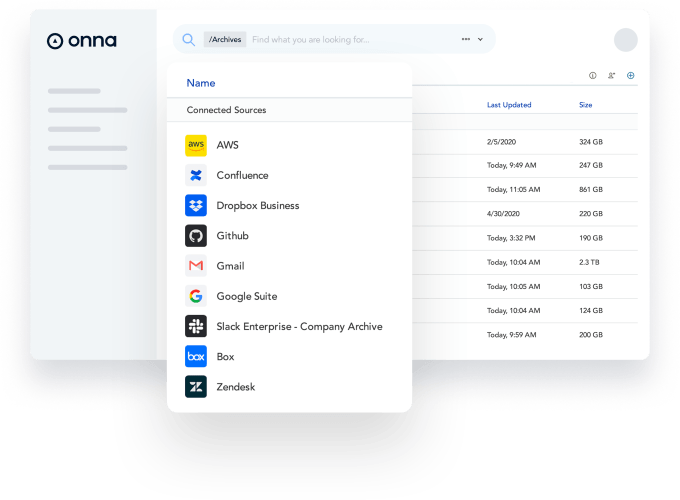

Onna, the “knowledge integration platform” (KIP) that counts Dropbox and Slack as backers, has raised $27 million in Series B funding.

Leading the round is Atomico, with participation from Glynn Capital. Previous investors Dawn Capital, Nauta Capital and Slack Fund also followed on.

Founded in 2015, Barcelona and New York-based Onna integrates with a plethora of workplace apps, including Slack, Dropbox, G Suite, Microsoft 365 and Salesforce, to help unlock the proprietary knowledge stored in a company’s various cloud and on-premise software. Typical applications for a KIP include compliance, governance, archiving and “eDiscovery.”

From communication apps to cloud storage to HR platforms, the idea is to unify all of this data and make it searchable but in a way that is secure and protects existing permissions and privacy. In fact, another way to think of Onna is like Apple’s Spotlight functionality but for the enterprise. However, pitched as a platform not just a feature, Onna also offers an API of its own so that various use cases can be built on top of this “single source of truth.”

“Onna’s knowledge integration platform is a centralised, searchable and secure hub that connects company data wherever it resides and makes it easier and faster to make informed decisions,” Onna founder and CEO Salim Elkhou tells TechCrunch. “It is a productivity tool built for the way businesses work today… something that didn’t exist before, creating a new industry standard which benefits all companies within the ecosystem.”

“Onna’s knowledge integration platform is a centralised, searchable and secure hub that connects company data wherever it resides and makes it easier and faster to make informed decisions,” Onna founder and CEO Salim Elkhou tells TechCrunch. “It is a productivity tool built for the way businesses work today… something that didn’t exist before, creating a new industry standard which benefits all companies within the ecosystem.”

Citing a report by single sign-in provider Okta, Elkhou notes that companies today use an average of 88 different apps across their workforce, a 21% increase from three years ago.

“The reason apps have become so popular is that they’re very effective for tackling specific challenges, or even a broad range of tasks. But the problem large organisations were coming up against is that their knowledge was spread across a wide range of apps that weren’t necessarily designed to work together.”

For example, a legal counsel could be looking to find contracts company-wide to assess a company’s exposure. The problem is that contracts may be saved in Salesforce, sent by email, shared over Slack or even saved on desktops. “Your company may have acquired another company, which has its own ways of saving information, so now the simple task of finding contracts can be a heavy lifting exercise, involving everyone’s time. With Onna, being the connective tissue across these applications, this search would take a split second,” claims Elkhou.

But the potential power of a KIP goes well beyond search alone. Elkhou says a more ambitious use case is unifying knowledge across apps and using Onna as infrastructure. “We believe that the next generation of workplace apps will be built on top of a knowledge integration platform like Onna,” he explains. “Due to our plug and play integrations with most enterprise apps and our open API, you can now build your own bespoke workflows on top of your company’s knowledge. More importantly, we handle all the heavy lifting on the back end when it comes to processing the right contextual information across multiple systems securely, which means you can get on with creatively building a more efficient workplace.”

“In Onna, we saw a product in a new and complementary category, providing a solution not at the data level but at the ‘knowledge level,’ ” adds Atomico’s Ben Blume, who has also joined the Onna board. “Onna’s core solution integrates with any tools in an organisation where knowledge resides, [and] ingests, indexes and classifies the knowledge inside, enabling it to power applications in many areas.”

Blume also points to the belief that some of the cloud tools vendors themselves have in Onna, with both Slack and Dropbox “investing, using and promoting” Onna’s solution. “As they look to grow their own penetration in organisations with a wider range of needs and demands, we saw partnering with Onna as a recognition of its best in class nature to their customers,” he says.

Meanwhile, I understand the new round of funding was done remotely due to lockdown, even though Atomico and Onna had already met and stayed in touch after the VC firm ended up not participating in the startup’s Series A.

Recalls Elkhou: “We had met with our investors in person over a year ago, and have had many video calls since and prior to the pandemic. However, soon after the lockdowns took effect, the need for remote collaboration tools skyrocketed which only accelerated the critical role Onna has in helping people within organisations access and share knowledge that was spread across an ever growing number of apps. If anything, it brought new urgency to the problem we were solving, because workplace serendipity no longer existed. You couldn’t answer questions over a coffee or by the water cooler, but these new remote workers still needed to access knowledge and share it securely.”

Powered by WPeMatico

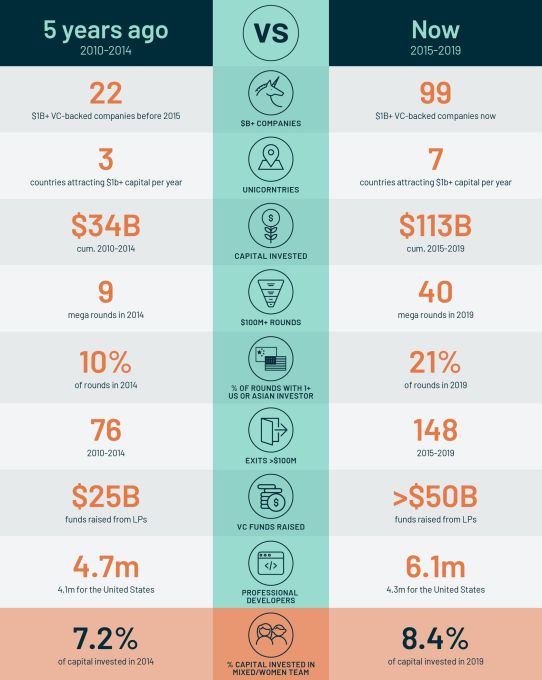

Atomico, the European venture capital firm founded by Skype’s Niklas Zennström, has released its latest annual The State of European Tech report, published in partnership with Slush and Orrick.

As part of the report, the authors surveyed 5,000 members of the ecosystem — including 1,000 founders — as well as pulling in robust data from other sources, such as Dealroom and the London Stock Exchange .

This year, the report reveals that the European tech ecosystem continues to mature and shows no sign of slowing — particularly highlighting the contrast from five years ago when the The State of European Tech report made its debut. Almost every key indicator is up and to the right, except, rather depressingly, diversity.

The data shows, for example, that competition for talent and access to the best founders has increased ferociously. And from a funding perspective, European founders have more choice than ever, especially with U.S. and Asian VC firms investing more and more in the region. Progress with gender diversity stalled, however, such as 92% of funding going to all-male teams.

I caught up with the report’s author Tom Wehmeier, Partner and Head of Insights at Atomico (also sometimes jokingly referred to as the “Mary Meeker of Europe”), where we discuss in more detail some of the key findings and why, it seems, that the rest of the world has finally woken up to Europe’s tech potential.

But first, a few headlines from the report:

Extra Crunch: It is 5 years since Atomico published the first The State of European Tech report, which really attempted to capture a data-driven snapshot of the entire ecosystem. What are some of the biggest changes you’ve seen within European tech in the intertwining years or in this year in particular?

Tom Wehmeier: If I think back to when we did the first report, people who believe that Europe could actually be an interesting player in global technology, were largely limited to people who were in the tech industry in Europe itself. If you then fast forward to today, what has clearly happened — and I think 2019 was the year where this really materialized and became part of the narrative — was that belief translating from people on the inside to a bunch of people that were on the outside.

Most obviously has been the strength of interest from from the U.S. and the number of top-tier U.S. funds that are not just increasing their level of investment activity but committing to spending more and more time here on the ground, hiring people, building teams, building a network, and getting to know companies. I think it probably surprises people to know that 19% of all rounds this year will involve at least one U.S. investor in Europe, which is more than double since since the first year we did the report.

I think the other thing, where I come back to this idea that now we have finally convinced a certain group of people about the role that Europe can play, is mainstream institutional investors. I know it is not going to be lost on you, [but] this is going to be another record year for VC fund raising from Europe. And whilst the headline numbers might not be a surprise, I think what should catch people’s attention is that the composition of the LP base here in Europe is now shifting. And finally, there’s an unlocking of institutional investors, [by which] I mean pension funds, funds of funds, insurance companies, sovereign wealth funds, who are committing to European VC at levels that are significantly increased and elevated from where they had been in the past. So, if you just take pension funds, we’re going to see close to a billion dollars invested which is up nearly three fold.

It’s a validation of what’s happening around European tech to see that now coming through and I think is ultimately something that helps to build a foundation for the next five years of success. As much as this is a report that’s looking back, it’s also about trying to understand where things go from here.

With regards to the pension funds, do you think that is driven by the general bullishness towards European tech, or do you think it’s more the macro economic reality that maybe other places where they could put their money aren’t very attractive at the moment?

I think it’s really a reflection that there’s a strong level of belief that European venture as an asset class is an attractive investment opportunity. And that is reflected by the numbers. One of the charts that we’ve got in the report is from Cambridge Associates who do the benchmarking for the VC indices… And when you look back over a 1, 3, 5, or even a 10 year horizon, the performance from European VC is demonstrating that this is a place where for anyone building a diversified portfolio, they should have some allocation. I think it’s fundamentally the strength of the investment opportunity. That is the single biggest driver for why you’re seeing this happen.

I think the biggest thing that Europe has been able to prove is that it can take a great idea and turn it into a great company and that company can scale to not just a billion dollar outcome but to a multi-billion dollar outcome and go all the way through into an IPO or into a large scale acquisition. What you’ve seen happen in 2019 is in part A reflection of what happened last year where it was obviously this record year with Spotify, Adyen, Farfetch, Elastic and others that really showed you can go full cycle from start all the way to finish. And that the magnitude of those outcomes can be at a scale that makes them globally relevant.

Are the pension funds shifting their allocation of VC away from other geographies or are they just doing more VC as a whole?

Powered by WPeMatico

Automation Hero, formerly SalesHero, has secured $14.5 million in new funding led by Atomico, with participation by Baidu Ventures and Cherry Ventures. As part of the deal, Atomico principal Ben Blume will join the company’s board of directors.

The automation startup launched in 2017 as SalesHero, giving sales orgs a simple way to automate back-office processes like filing an expense report or updating the CRM. It does this through an AI assistant called Robin — “Batman and Robin, it worked with the superhero theme, and it’s gender neutral,” co-founder and CEO Stefan Groschupf explained — that can be configured to go through the regular workflow and take care of repetitive tasks.

“We brought computers into the workplace because we believed they could make us more productive,” said Groschupf. “But in many companies, people spend a lot of time entering data and doing painful manual processes to make these machines happy.”

The idea was to give salespeople more time to actually do their job, which is selling to clients. If all the administrative and repetitive “paperwork” is done by a computer, human employees can become more productive and efficient at skilled tasks.

By weaving together click robots, Automation Hero users can build out their own workflows through a no-code interface, tying together a wide variety of both structured and unstructured data sources. Those workflows are then presented in the inbox each morning by Robin, the AI assistant, and are executed as soon as the user gives the go-ahead.

After launch, the team realized that other types of organizations, beyond sales departments, were building out automations. Insurance firms, in particular, were using the software to automate some of the repetitive tasks involved with filing and assessing claims.

This led to today’s rebrand to Automation Hero.

Groschupf said that by automating the process of filling out a single closing form, it saved one insurance firm’s 430 sales reps 18.46 years per year.

Automation Hero has now raised a total of $19 million.

“We’re really excited with Atomico to bring on a great VC and good people,” said Groschupf. “I’ve raised capital before and I’ve worked with some of the more questionable VCs, as it turns out. We’re super-excited we’ve found an investor that really bakes important things, like a diversity policy and a family leave policy, right into the company’s investment agreement.”

Though he didn’t confirm, it’s likely that Groschupf is referring to KPCB, which has run into its fair share of controversy over the past few years and was an investor in Groschupf’s previous startup, Datameer.

Powered by WPeMatico

If the last few years has seen a growing consensus that the tech industry has a diversity and inclusion problem, then what is clearly needed next are practical solutions. While most people agree that building a diverse and inclusive company culture is easier to achieve the earlier you set out to do so, for startups and even much larger companies it is often difficult to know where to start, let alone what your own eventual D&I strategy might look like.

Conversely, there’s a body of evidence that points to diverse teams creating more successful and longer-lasting companies. Besides, it’s never smart to leave talent on the table. Enter a new initiative from Diversity VC, a nonprofit partnership promoting diversity in Venture Capital, and London venture capital firm Atomico.

The pair have teamed up to launch what may well be an industry-first resource: a practical and hands-on guide for ambitious technology entrepreneurs to “help them build companies that have diversity and inclusion at their core.” The guide can be found online here, and is also in print. It was unveiled last week onstage at Slush 2018 by Diversity VC’s Check Warner and Atomico founder Niklas Zennström.

The objective of the “Founder Guide” is to be a central place for technology companies, large and small to “find pragmatic, actionable advice for planning, implementing and measuring their D&I strategy”. It’s also meant to be a work in progress, and with the help of feedback and suggestions, will evolve as the industry’s understanding of D&I develops.

More broadly, the guide focuses on diversity and inclusion in the workplace in its broadest sense, looking at ethnicity, socio-economic backgrounds, disability, gender, sexuality, religious faith, cognitive differences, dependants and caring responsibilities and how all those factors, and the “intersections of those factors,” can impact an individual’s success in tech companies, and therefore the success of companies overall.

In an email Q&A with Diversity VC co-founder and CEO Check Warner, we delved deeper into what the guide hopes to achieve, why D&I matters and what diversity and inclusion might look like as an end goal. I also argued that the way we think about D&I is currently too narrow and needs to put a greater emphasis on social mobility, which at times seems to be missing from the conversation entirely.

TC: Why did you decide to create a Diversity & Inclusion guide for tech companies? And why was it needed?

CW: The conversation on Diversity & Inclusion until now has focused on highlighting the challenges we face (which are significant), but there’s been very little actionable advice. The idea of the Diversity & Inclusion guide is to move the discussion forward. We want to start a positive conversation around what tech companies can do to promote diversity and inclusion, and we want entrepreneurs to start making simple, meaningful changes today. Sixty-five percent of founders surveyed in the Atomico State of European Tech Report said they didn’t have a Diversity & Inclusion policy for hiring, and 55 percent said there was no Diversity & Inclusion lead in their company (source — Atomico’s State of European Tech Report 2018).

The guide is intended to make it as simple and frictionless as possible to start that conversation and put in place a plan. At the same time, we know that this Guide is only the first step. It’s not a panacea for all ills. But we hope it helps move the conversation forward, and constitutes a step toward tackling the deep and nuanced challenge of creating an industry where everyone has a fair chance to succeed.

The organisation Diversity VC is a nonprofit dedicated to promoting diversity and inclusion in venture capital and tech. We focus on positive interventions and this guide is a high-impact, useful resource for VCs to give their portfolio companies, and for the industry as a whole. Atomico shares this mission and were being asked by their portfolio for help with Diversity and Inclusion, so we joined forces.

We hope that by publishing this guide now, and publishing it in a format which people can contribute and add to through our website www.inclusionintech.com, that we encourage input from companies who have had success in promoting Diversity and Inclusion. We’ve already started to see this happen, as we’ve had several notes from founders with suggestions of other interventions that can be made, even in the two days since the guide was released.

TC: Clearly diversity within the workforce is always going to be a “work in progress,” but in terms of an end goal, what does diversity actually look like?

CW: For us, success looks like a technology and venture capital industry where anyone, from any background, ability, religion, ethnicity, gender, sexuality and socio-economic background can succeed and thrive. We want there to be equity of opportunity between these groups and everyone else.

TC: What would you say to people who believe that although a diverse and inclusive workforce is a noble aim, early-stage companies and founders have much more immediate problems to solve, such as finding product-market fit, fundraising or making their first 10 hires. Therefore, a D&I strategy is nice to have but ultimately a distraction for a startup?

CW: Having a diversity and inclusion strategy is not “additional to” any of these things, but instead a key part of them, and an essential ingredient to success. When it comes to finding product-market fit, having a diverse team has been shown to increase creativity, and improve performance and profitability. A diverse team will also help the company connect to, and empathise with, a broader base of customers, which competitors who have homogenous teams will be in a much worse position to do. Having an inclusive company culture will ensure that a company can attract the broadest range of talent, and therefore pick and retain the very best people.

TC: The guide is pretty dense — yes, I’ve read it! — and packed with lots of actionable advice, but at times asks more questions of a company than it provides answers. Where should a founder or D&I champion within a company start if it all feels a bit overwhelming at first?

CW: Thank you for reading it! We’ve tried as much as possible to focus on practical advice and we have over 40 tech tools and resources included in the guide which can help with everything from hiring to culture to product design. There’s also a two-page summary of the key takeaways to make it as easy as possible for founders to digest. However — the structural inequalities that we’re talking about are multi-faceted and complex — so it’s unfortunately not something that can be simply “solved.” In our research we found the companies that were most successful in fostering a diverse and inclusive culture were the ones that included their employees, at all levels, in inputting and crafting solutions and answers, so we suggest that starting a conversation, asking questions and making sure that the whole company feels part of that conversation is a good beginning.

TC: The guide has a few passages on the role of PR as part of a D&I strategy. Shouldn’t this be one area where it explicitly isn’t about publicity as this leaves companies open to accusations — rightly or wrongly — of being superficial or so-called virtue signalling?

CW: The emphasis we have put on PR is about the need for leaders across the technology industry to show public commitment to promoting diversity and inclusion in their companies. For too long, this is a subject that people have been afraid of talking about for fear of “getting it wrong” or of revealing that they are not making progress fast enough. So long as the commitment to Diversity & Inclusion comes from a place of understanding and the actions being taken are genuine and actually helping, then companies should have nothing to fear in talking about their work in this area. In fact, I would like to see more leaders across the technology industry state, like Niklas Zennstrom has this week, where they are struggling and where they need to make more progress, as I think this will accelerate getting answers!

TC: The report provides some very good tips on how to get “buy in” for a D&I agenda across the whole company and from other stakeholders. Why is this important and what are the biggest mistakes a founder or other D&I champion can make in this regard along the way?

CW: Like any strategic project or undertaking, making sure that there’s a shared goal in terms of what the founder is trying to achieve is important, but it is particularly so when it comes to putting in place a D&I strategy because the impact of getting it wrong compounds as the company grows. One mistake I’ve seen is where well-meaning companies isolate a single group of people and focus their a D&I strategy on them, which may actually be to the detriment of other underrepresented groups, or to those at the intersection of multiple groups.

TC: It is very noticeable that in the “The current state of diversity and inclusion in tech” section of the guide the entire conversation is reduced to the underrepresentation of women in tech, leaving out other marginalised groups or other definitions of diversity. This seems to be quite common across the industry as a whole, where diversity at is times simply a byword for gender imbalances. Do you see this as a problem?

CW: I see this as a big problem. The whole guide is written to address the broad topic of diversity and we have deliberately chosen contributors to reflect these diverse perspectives, from LGBTQ founders, to people with cognitive and physical disabilities, to BAME founders and combinations of the above. Unfortunately the section on the “State of Diversity in Tech” is a reflection of the current frustrating lack of available data on any other aspect of diversity than gender diversity in the tech industry, which makes it very difficult to quantify the challenge.

This is something that Diversity VC and Atomico are working hard on. As an organization, Diversity VC is focused on Diversity & Inclusion in its broadest sense, and one of the big challenges that we set out to tackle was the lack of data on diversity in the VC industry. In 2019 we will be publishing the first-ever study on U.K. VCs that includes ethnicity data, educational backgrounds and career backgrounds, which will also help us understand the socio-economic backgrounds of the VC industry. Whilst this is not nearly enough, it goes some way to helping us understand diversity and inclusion beyond the narrow subject of gender imbalance.

TC: Related to this, socio-economic diversity, or the tech industry’s need to do a better job promoting social mobility as part of a D&I agenda, seems almost entirely lacking from the wider industry conversation and I’m not sure this guide does enough to change that. Isn’t this odd when it would seem evident to anyone who works in the tech industry that economic privilege and lack of social mobility is intrinsically linked to the marginalisation of many underrepresented groups?

CW: I agree that it’s hugely lacking in the conversation and that we need much more focus on this area. For me the biggest mindset shift required is to remove the rigid criteria of what hiring managers and recruiters are screening for when they are making hires. Our case study on Backstage Capital in section 3 is about recruiting through Twitter and Instagram, and having no set criteria for qualifications or subjects studied, and instead, hiring for aptitude and investing in training hires either on the job or through courses. Both apprenticeships and internships are an important part of this conversation and I’d like to see more done to promote these across the industry. At Diversity VC we are running an internship programme which aims to help people who don’t have qualifications (MBA or similar) which are sometimes sought by recruiters for venture capital. We’ve found this internship programme to be an effective way of getting young people into full-time jobs, despite the fact that a recruiter would probably have passed over their CV in a traditional recruitment process.

TC: I say this as a white male who comes from a middle class family (both my parents were teachers): You are a white woman who is private school and Oxbridge-educated and so some might say you are part of the problem as much as the solution. How do you square that circle in the important work you are doing at Diversity VC?

CW: Absolutely — this is something I’m very conscious of. I’ve been privileged in the opportunities I’ve had, which has given me an enormous leg up in getting into the industry. I find it completely unjust that others haven’t had the same chance which made me determined, almost as soon as I got into the industry, to get together with Travis, Lillian, Farooq and Anna, as well as our advisors, to do something about it. But, to echo a sentiment that I’m sure all of us share, the worst thing you can do in the face of something unjust is to stay silent.

The mission and the organization are also so much bigger than any individual. There are over 50 people across the industry that have volunteered on Diversity VC’s data projects, joined training programmes, mentored founders from diverse backgrounds, spoken at schools and universities, contributed to the Guide. In order for Diversity VC to be successful in its aims it is important that the leadership group is as diverse as possible, which is not the case today.

TC: Lastly, it is great to see a practical guide that has the potential to help produce some really tangible improvements in how tech companies approach D&I. If we look ahead, how different do you hope or expect the industry to be with regards to diversity and inclusion in one, five or 10 years?

CW: I hope that in one year’s time the industry is more comfortable and proactive in discussing the subject of diversity and inclusion, and that we have significantly more data than we do today to enable us to target solutions. In five and 10 years’ time I hope that the tech industry will have emerged as a leader in being inclusive and sets an example for other industries to follow. Since it is growing 5x faster than the economy, the impact that getting this right will make is hard to overstate.

Powered by WPeMatico

The only sure things in this life, according to Ben Franklin, are death and taxes. And a new startup called Visor has just raised $9 million in financing to make one of them as painless as possible.

Unlike Nectome, Visor won’t kill anyone, but it may ring the death knell for the high-end tax advisors that most Americans can’t even access to get help filing and paying their taxes. It’s like having a personalized accountant for the cost of a high-end do-it-yourself tax-prep service.

The $9 million Visor raised came from the venture capital firm Defy, with participation from Unusual Ventures, SVB Capital and existing investors like Obvious Ventures, Fika Ventures and Boxgroup, which had put a previous $6.5 million into the company.

The idea for the company had been percolating for co-founder and chief executive Gernot Zacke since he settled in the U.S.

Growing up in Sweden, Zacke was exposed to a much different process for paying taxes. “The experience of filing taxes in Sweden is that you receive a message from the government that stated how much you made and how much you were withholding. That’s it,” said Zacke. “Taxes should be as easy as ordering a cab.”

That’s the service that Visor aims to provide.

“If you think about the market there are two ways to get your taxes done. There’s the DIY space and then there are other online services but it requires the tax payer to fill out the forms and it leaves the tax payer with a little bit of anxiety,” said Zacke. “We’re delivering the CPA experience through the convenience of a web app and a mobile app.”

On average, Americans spend about 13 hours each year dealing with taxes, and the average American doesn’t have the benefits of a professional advisor who can help optimize the process. That’s what Visor wants to provide.

“You provide the same amount of information you provide to a CPA or TurboTax… we make sure that that information is filed securely on AWS and shared between the docs and the backend,” said Zacke.

The target customers for Zacke’s services are folks who have had a change to their tax situation — whether moving, buying a home or any other life event; or folks who have had a CPA and don’t want to pay the higher fees, he said.

Visor currently has an operations team of around 34 people split between San Francisco and Atlanta.

For Zacke, the pain point he’s solving with the Visor service is very real. A former employee of the European investment firm Atomico, Zacke bounced between the U.S. and Europe — eventually running U.S. investments for the firm before leaving to launch Visor.

Other co-founders and senior executives hail from the tax advisory world, and from employee benefits outsourcing services company Zenefits, along with former Venmo and Square developers.

“Taxpayers spend $20 billion a year to get their taxes prepared and are stuck between spending hours filling out DIY tax software and hiring an expensive CPA,” said Zacke, in a statement. “

Powered by WPeMatico

Teralytics’s big data analytics platform is targeting government agencies and transport companies wanting to understand complex problems relating to human mobility — from how to relieve transport pressure points to monitoring urban air quality without the need for CO2 sensors. Just plug in telecos’ data to play… Read More

Teralytics’s big data analytics platform is targeting government agencies and transport companies wanting to understand complex problems relating to human mobility — from how to relieve transport pressure points to monitoring urban air quality without the need for CO2 sensors. Just plug in telecos’ data to play… Read More

Powered by WPeMatico