asia pacific

Auto Added by WPeMatico

Auto Added by WPeMatico

Business, now more than ever before, is going digital, and today a startup that’s building a vertically integrated solution to meet business banking needs is announcing a big round of funding to tap into the opportunity. Airwallex — which provides business banking services directly to businesses themselves as well as via a set of APIs that power other companies’ fintech products — has raised $200 million, a Series E round of funding that values the Australian startup at $4 billion.

Lone Pine Capital is leading the round, with new backers G Squared and Vetamer Capital Management, and previous backers 1835i Ventures (formerly ANZi), DST Global, Salesforce Ventures and Sequoia Capital China also participating.

The funding brings the total raised by Airwallex — which has head offices in Hong Kong and Melbourne, Australia — to $700 million, including a $100 million injection that closed out its Series D just six months ago.

Airwallex will be using the funding both to continue investing in its product and technology as well as to continue its geographical expansion and to focus on some larger business targets. The company has started to make some headway into Europe and the U.K. and that will be one big focus, along with the U.S.

The quick succession of funding and rising valuation underscore Airwallex’s traction to date around what CEO and co-founder Jack Zhang describes as a vertically integrated strategy.

That involves two parts. First, Airwallex has built all the infrastructure for the business banking services that it provides directly to businesses with a focus on small and medium enterprise customers. Second, it has packaged up that infrastructure into a set of APIs that a variety of other companies use to provide financial services directly to their customers without needing to build those services themselves — the so-called “embedded finance” approach.

“We want to own the whole ecosystem,” Zhang said to me. “We want to be like the Apple of business finance.”

That seems to be working out so far for Airwallex. Revenues were up almost 150% for the first half of 2021 compared to a year before, with the company processing more than US$20 billion for a global client portfolio that has quadrupled in size. In addition to tens of thousands of SMEs, it also, via APIs, powers financial services for other companies like GOAT, Papaya Global and Stake.

Airwallex got its start like many of the strongest startups do: It was built to solve a problem that the founders encountered themselves. In the case of Airwallex, Zhang tells me he had actually been working on a previous startup idea. He wanted to build the “Blue Bottle Coffee” of Asia Pacific out of Australia, and it involved buying and importing a lot of different materials, packaging and, of course, coffee from all around the world.

“We found that making payments as a small business was slow and expensive,” he said, since it involved banks in different countries and different banking systems, manual efforts to transfer money between them and many days to clear the payments. “But that was also my background — payments and trading — and so I decided that it was a much more fascinating problem for me to work on and resolve.”

Eventually one of his co-founders in the coffee effort came along, with the four co-founders of Airwallex ultimately including Zhang, along with Xijing Dai, Lucy Liu and Max Li.

It was 2014, and Airwallex got attention from VCs early on in part for being in the right place at the right time. A wave of startups building financial services for SMBs were definitely gaining ground in North America and Europe, filling a long-neglected hole in the technology universe, but there was almost nothing of the sort in the Asia Pacific region, and in those earlier days solutions were highly regionalized.

From there it was a no-brainer that starting with cross-border payments, the first thing Airwallex tackled, would soon grow into a wider suite of banking services involving payments and other cross-border banking services.

“In the last six years, we’ve built more than 50 bank integrations and now offer payments across 95 countries, payments through a partner network,” he added, with 43 of those offering real-time transactions. From that, it moved on to bank accounts and “other primitive stuff” with card issuance and more, he said, eventually building an end-to-end payment stack.

Airwallex has tens of thousands of customers using its financial services directly, and they make up about 40% of its revenues today. The rest is the interesting turn the company decided to take to expand its business.

Airwallex had built all of its technology from the ground up itself, and it found that — given the wave of new companies looking for more ways to engage customers and become their one-stop shop — there was an opportunity to package that tech up in a set of APIs and sell that on to a different set of customers, those who also provided services for small businesses. That part of the business now accounts for 60% of Airwallex’s business, Zhang said, and is growing faster in terms of revenues. (The SMB business is growing faster in terms of customers, he said.)

A lot of embedded finance startups that base their business around building tech to power other businesses tend to stay at arm’s length from offering financial services directly to consumers. The explanation I have heard is that they do not wish to compete against their customers. Zhang said that Airwallex takes a different approach, by being selective about the customers they partner with, so that the financial services they offer would not be in direct competition with those of its customers. The GOAT marketplace for sneakers, or Papaya Global’s HR platform are classic examples of this.

However, as Airwallex continues to grow, you can’t help but wonder whether one of those partners might like to gobble up all of Airwallex and take on some of that service provision role itself. In that context, it’s very interesting to see Salesforce Ventures returning to invest even more in the company in this round, given how widely the company has expanded from its early roots in software for salespeople into a massive platform providing a huge range of cloud services to help people run their businesses.

For now, it’s been the combination of its unique roots in Asia Pacific, plus its vertical approach of building its tech from the ground up, plus its retail acumen that has impressed investors and may well see Airwallex stay independent and grow for some time to come.

“Airwallex has a clear competitive advantage in the digital payments market,” said David Craver, MD at Lone Pine Capital, in a statement. “Its unique Asia-Pacific roots, coupled with its innovative infrastructure, products and services, speak volumes about the business’ global growth opportunities and its impressive expansion in the competitive payment providers space. We are excited to invest in Airwallex at this dynamic time, and look forward to helping drive the company’s expansion and success worldwide.”

Updated to note that the coffee business was in Australia, not Hong Kong.

Powered by WPeMatico

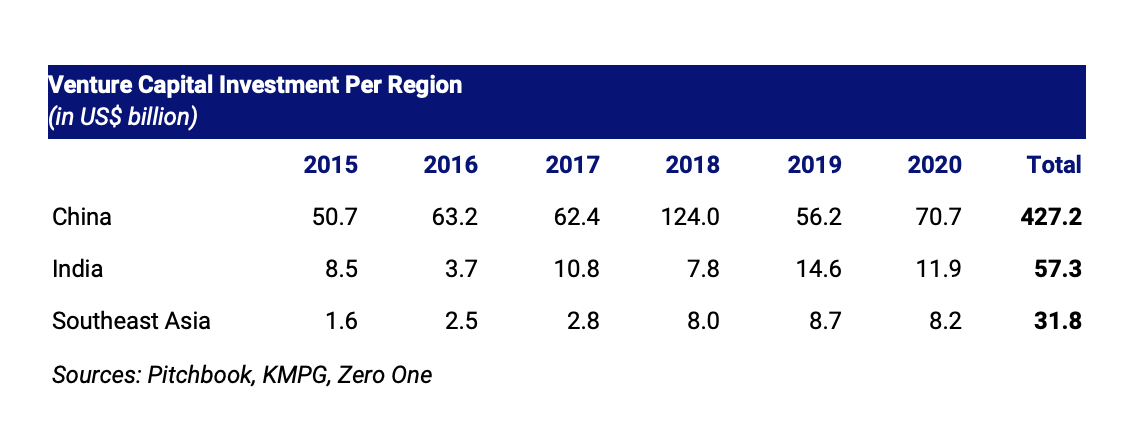

Southeast Asian tech companies are drawing the attention of investors around the world. In 2020, startups in the region raised over $8.2 billion, about four times more than they did in 2015. This trend continued in 2021, with regional M&A hitting a record high of $124.8 billion in the first half of 2021, up 83% from a year earlier.

This begs the question: Who exactly is investing in Southeast Asia?

Let’s explore the three key types of investors pouring money into and driving the growth of Southeast Asia’s tech ecosystem.

Over 229 family offices have been registered in Singapore since 2020, with total assets under management of an estimated $20 billion.

Southeast Asia has become an attractive market for U.S. and Chinese tech firms. Internet penetration here stands at 70%, higher than the global average, and digital adoption in the region remains nascent — it wasn’t until the pandemic that adoption of digital services such as e-wallets and online shopping took off.

China’s tech giants Tencent and Alibaba were among the first to support early e-commerce growth in Southeast Asia with investments in Sea Limited and Lazada, and have since expanded their footprint into other internet verticals. Alibaba has backed Akulaku, M-Pay (eMonkey), DANA, Wave Money and Mynt (GCash), while Tencent has invested in Voyager Innovations (PayMaya), SHAREit, iflix, Ookbee and Sanook.

U.S. tech firms have also recently entered the scene. In June 2020, Gojek closed a $3 billion Series F round from Google, Facebook, Tencent and Visa. Google, together with Singapore’s Temasek Holdings, invested some $350 million in Tokopedia in October. Meanwhile, Microsoft invested an undisclosed amount in Grab in 2018 and has invested $100 million in Indonesian e-commerce firm Bukalapak.

In Q1 2021, Southeast Asian startups raised $6 billion, according to DealStreetAsia, positioning 2021 as another record year for VC investment in the region.

The region is also rising in prominence as a destination for investment capital relative to the rest of Asia. Regional VC investment grew 5.2 times to $8.2 billion in 2020 from $1.6 billion in 2015, as we can see in the table below.

Image Credits: Jungle VC

Southeast Asia also has many opportunities for VC investment relative to its market size. From 2015 to 2020, China saw VC investment of nearly $300 per person; for Southeast Asia — despite a recent investment boom — this metric sits at just $47.50 per person, or just a sixth of that in China. This implies a substantial opportunity for investments to develop the region’s digital economy.

The region’s rising population and growth prospects are higher due to China’s population growth challenges, alongside the latter’s higher digital economy market saturation and maturity.

Powered by WPeMatico

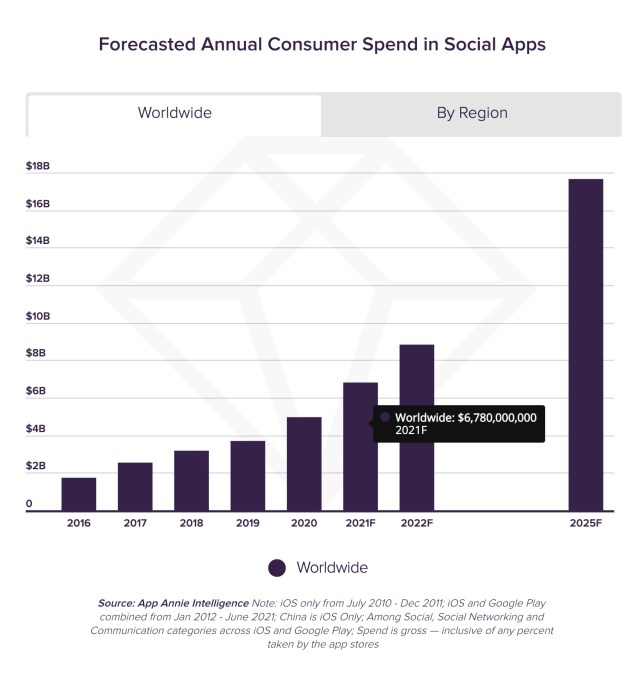

The livestreaming boom is driving a significant uptick in the creator economy, as a new forecast estimates consumers will spend $6.78 billion in social apps in 2021. That figure will grow to $17.2 billion annually by 2025, according to data from mobile data firm App Annie, which notes the upward trend represents a five-year compound annual growth rate (CAGR) of 29%. By that point, the lifetime total spend in social apps will reach $78 billion, the firm reports.

Image Credits: App Annie

Initially, much of the livestream economy was based on one-off purchases like sticker packs, but today, consumers are gifting content creators directly during their livestreams. Some of these donations can be incredibly high, at times. Twitch streamer ExoticChaotic was gifted $75,000 during a live session on Fortnite, which was one of the largest-ever donations on the game-streaming social network. Meanwhile, App Annie notes another platform, Bigo Live, is enabling broadcasters to earn up to $24,000 per month through their livestreams.

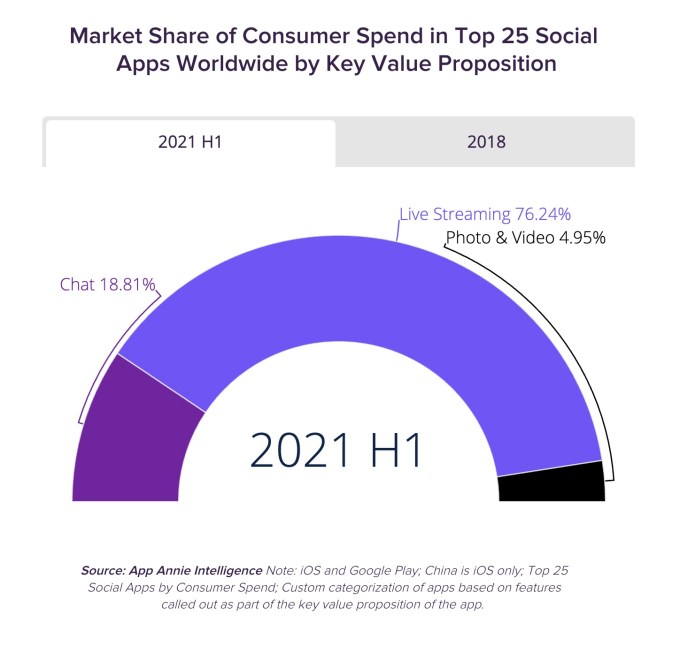

Apps that offer livestreaming as a prominent feature are also those that are driving the majority of today’s social app spending, the report says. In the first half of this year, $3 out every $4 spent in the top 25 social apps came from apps that offered livestreams, for example.

Image Credits: App Annie

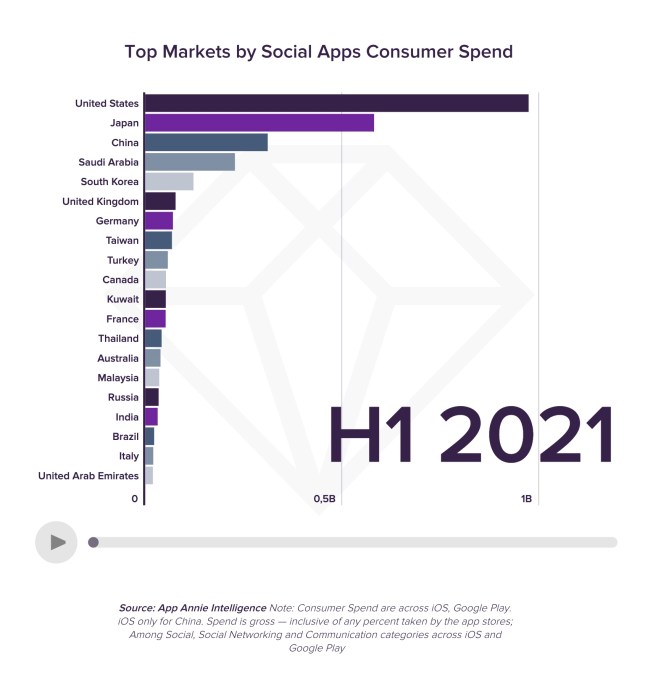

During the first half of 2021, the U.S. become the top market for consumer spending inside social apps, with 1.7x the spend of the next largest market, Japan, and representing 30% of the market by spend. China, Saudi Arabia and South Korea followed to round out the top 5.

Image Credits: App Annie

While both creators and the platforms are financially benefitting from the livestreaming economy, the platforms are benefitting in other ways beyond their commissions on in-app purchases. Livestreams are helping to drive demand for these social apps and they help to boost other key engagement metrics, like time spent in app.

One top app that’s significantly gaining here is TikTok.

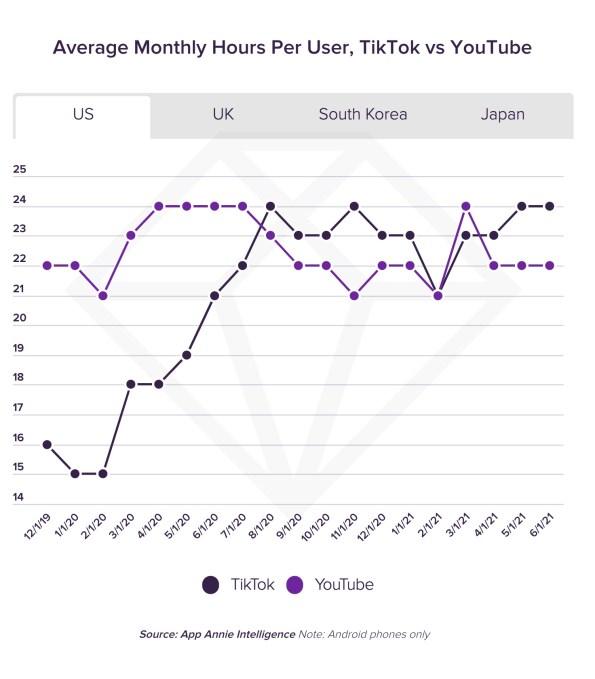

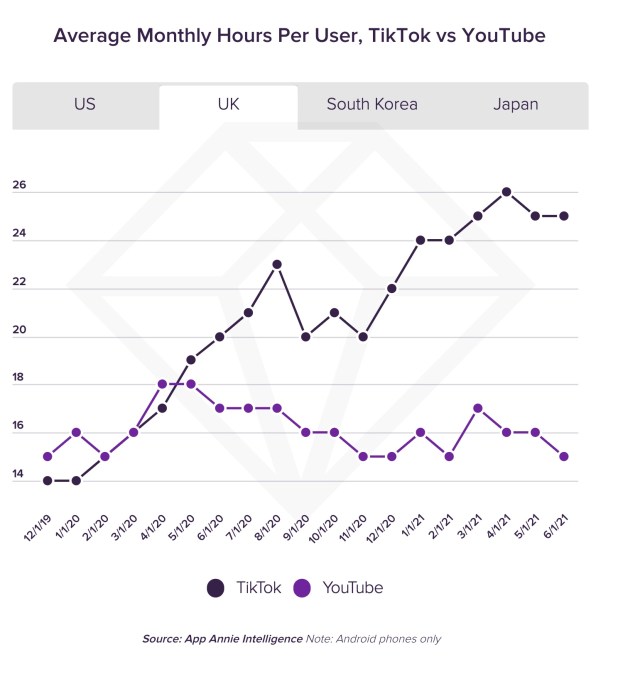

Last year, TikTok surpassed YouTube in the U.S. and the U.K. in terms of the average monthly time spent per user. It often continues to lead in the former market, and more decisively leads in the latter.

Image Credits: App Annie

Image Credits: App Annie

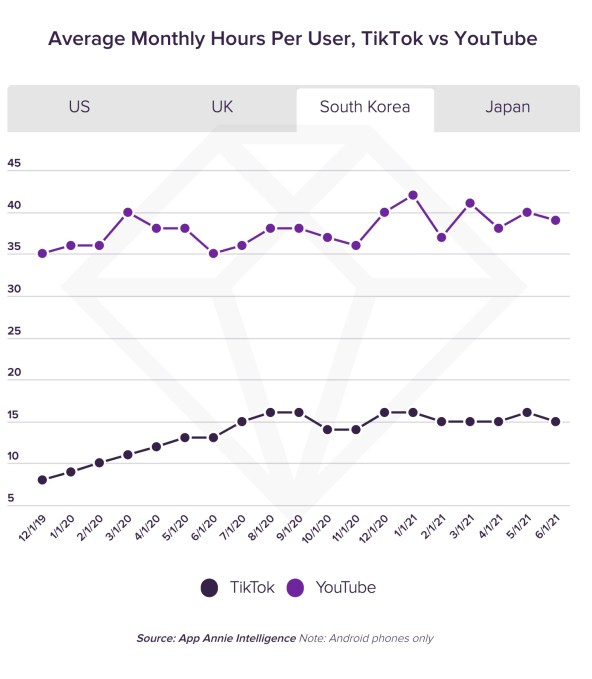

In other markets, like South Korea and Japan, TikTok is making strides, but YouTube still leads by a wide margin. (In South Korea, YouTube leads by 2.5x, in fact.)

Image Credits: App Annie

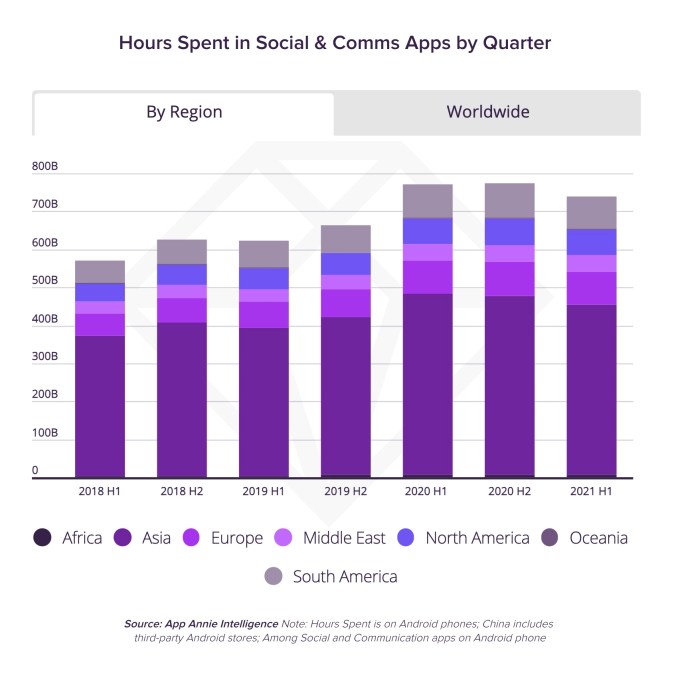

Beyond just TikTok, consumers spent 740 billion hours in social apps in the first half of the year, which is equal to 44% of the time spent on mobile globally. Time spent in these apps has continued to trend upwards over the years, with growth that’s up 30% in the first half of 2021 compared to the same period in 2018.

Today, the apps that enable livestreaming are outpacing those that focus on chat, photo or video. This is why companies like Instagram are now announcing dramatic shifts in focus, like how they’re “no longer a photo sharing app.” They know they need to more fully shift to video or they will be left behind.

The total time spent in the top five social apps that have an emphasis on livestreaming are now set to surpass half a trillion hours on Android phones alone this year, not including China. That’s a three-year CAGR of 25% versus just 15% for apps in the Chat and Photo & Video categories, App Annie noted.

Image Credits: App Annie

Thanks to growth in India, the Asia-Pacific region now accounts for 60% of the time spent in social apps. As India’s growth in this area increased over the past 3.5 years, it shrunk the gap between itself and China from 115% in 2018 to just 7% in the first half of this year.

Social app downloads are also continuing to grow, due to the growth in livestreaming.

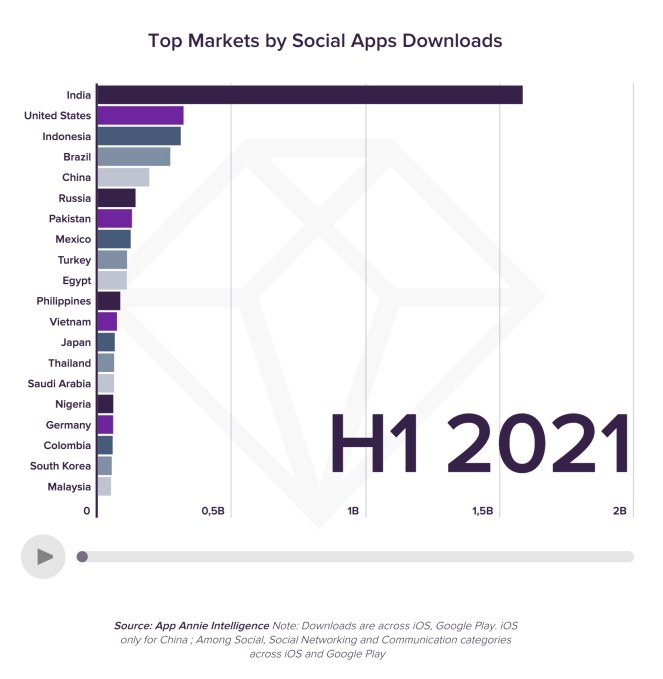

To date, consumers have downloaded social apps 74 billion times, and that demand remains strong, with 4.7 billion downloads in the first half of 2021 alone — up 50% year-over-year. In the first half of the year, Asia was the largest region region for social app downloads, accounting for 60% of the market.

This is largely due to India, the top market by a factor of 5x, which surpassed the U.S. back in 2018. India is followed by the U.S., Indonesia, Brazil and China, in terms of downloads.

Image Credits: App Annie

The shift toward livestreaming and video has also impacted what sort of apps consumers are interested in downloading, not just the number of downloads.

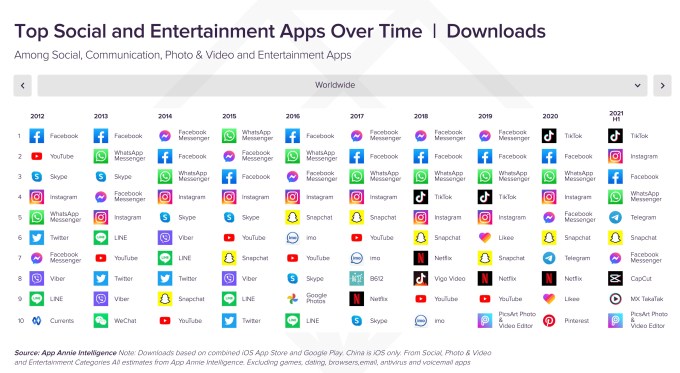

A chart that shows the top global apps from 2012 to the present highlights Facebook’s slipping grip. While its apps (Facebook, Messenger, Instagram and WhatsApp) have dominated the top spots over the years in various positions, TikTok popped into the number one position last year, and continues to maintain that ranking in 2021.

Further down the chart, other apps that aid in video editing have also overtaken others that had been more focused on photos or chat.

Image Credits: App Annie

Video apps like YouTube (#1), TikTok (#2) Tencent Video (#4), Bigo Live (#5), Twitch (#6), and others also now rank at the top of the global charts by consumer spending in the first half of 2021.

But YouTube (#1) still dominates in time spent compared with TikTok (#5), and others from Facebook — the company holds the next three spots for Facebook, WhatsApp and Instagram, respectively.

This could explain why TikTok is now exploring the idea of allowing users to upload even longer videos, by increasing the limit from 3 minutes to 5, for instance.

TikTok is testing a longer 5 minute video upload limit

pic.twitter.com/qiRbJmHkma

— Matt Navarra (@MattNavarra) August 25, 2021

In addition, because of livestreaming’s ability to drive growth in terms of time spent, it’s also likely the reason why TikTok has been heavily investing in new features for its TikTok LIVE platform, including things like events, support for co-hosts, Q&As and more, and why it made the “LIVE” button a more prominent feature in its app and user experience.

App Annie’s report also digs into the impact livestreaming has had on specific platforms, like Twitch and Bigo Live, the former which doubled its monthly active user base from the pre-pandemic era, and the latter which saw $314.2 million in consumer spend during H1 2021.

“The ability of social media users to communicate with each other using live video – or watch others’ live broadcasts – has not only maintained the growth of a social media app market, but contributed to its exponential growth in engagement metrics like time spent, that might otherwise have saturated some time ago,” wrote App Annie’s Head of Insights, Lexi Sydow, when announcing the new report.

The full report is available here.

Powered by WPeMatico

E-commerce is booming in Southeast Asia, but in many markets, the fragmented logistics industry is struggling to catch up. This means sellers run into roadblocks when shipping to buyers, especially outside of major metropolitan areas, and managing their supply chains. Locad, a startup that wants to help with what it describes as an “end-to-end solution” for cross-border e-commerce companies, announced today it has raised a $4.9 million seed round.

The funding was led by Sequoia Capital India’s Surge (Locad is currently a part of the program’s fifth cohort), with participation from firms like Antler, Febe Ventures, Foxmont, GFC and Hustle Fund. It also included angel investors Alessandro Duri, Alexander Friedhoff, Christian Weiss, Henry Ko, Huey Lin, Markus Bruderer, Dr. Markus Erken, Max Moldenhauer, Oliver Mickler, Paulo Campos, Stefan Mader, Thibaud Lecuyer, Tim Marbach and Tim Seithe.

Locad was founded in Singapore and Manila by Constantin Robertz, former Zalora director of operations Jannis Dargel and Shrey Jain, previously Grab’s lead product manager of maps. It now also has offices in Australia, Hong Kong and India. The startup’s goal is to close the gap between first-mile and last-mile delivery services, enabling e-commerce companies to offer lower shipping rates and faster deliveries while freeing up more time for other parts of their operations, such as marketing and sales conversions.

Since its founding in October 2020, Locad has been used by more than 30 brands and processed almost 600,000 items. Its clients range from startups to international brands, and include Mango, Vans, Payless Shoes, Toshiba and Landmark, a department store chain in the Philippines.

Locad is among a growing roster of other Southeast Asia-based logistics startups that have recently raised funding, including Kargo, SiCepat, Advotics and Logisly. Locad wants to differentiate by providing a flexible solution that can work with any sales channel and is integrated with a wide range of shipping providers.

Robertz told TechCrunch that Locad is able to keep an asset-light business model by partnering with warehouse operators and facility managers. What the startup brings to the mix is a cloud software platform that serves as a “control tower,” letting users get real-time information about inventory and orders across Locad’s network. The company currently has seven fulfillment centers, with four of its warehouses in the Philippines and the other three in Singapore, New South Wales, Australia and Hong Kong. Part of its funding will be used to expand into more Asia-Pacific markets, focusing on Southeast Asia and Australia.

Locad’s seed round will also used to add integrations to more couriers and sales channels (it can already be used with platforms like Shopify, WooCommerce, Amazon, Shopee, Lazada and Zalora), and develop new features for its cloud platform, including more data analytics.

Powered by WPeMatico

Mercuryo, a startup that has built a cross-border payments network, has raised $7.5 million in a Series A round of funding.

The London-based company describes itself as “a crypto infrastructure company” that aims to make blockchain useful for businesses via its “digital asset payment gateway.” Specifically, it aggregates various payment solutions and provides fiat and crypto payments and payouts for businesses.

Put more simply, Mercuryo aims to use cryptocurrencies as a tool for putting in motion next-gen, cross-border transfers or, as it puts it, “to allow any business to become a fintech company without the need to keep up with its complications.”

“The need for fast and efficient international payments, especially for businesses, is as relevant as ever,” said Petr Kozyakov, Mercuryo’s co-founder and CEO. While there is no shortage of companies enabling cross-border payments, the startup’s emphasis on crypto is a differentiator.

“Our team has a clear plan on making crypto universally available by enabling cheap and straightforward transactions,” Kozyakov said. “Cryptocurrency assets can then be used to process global money transfers, mass payouts and facilitate acquiring services, among other things.”

Image Credits: Left to right: Alexander Vasiliev, Greg Waisman, Petr Kozyakov / MercuryO

Mercuryo began onboarding customers at the beginning of 2019, and has seen impressive growth since with annual recurring revenue (ARR) in April surpassing over $50 million. Its customer base is approaching 1 million, and the company has partnerships with a number of large crypto players including Binance, Bitfinex, Trezor, Trust Wallet, Bithumb and Bybit. In 2020, the company said its turnover spiked by 50 times while run-rate turnover crossed $2.5 billion in April 2021.

To build on that momentum, Mercuryo has begun expanding to new markets, including the United States, where it launched its crypto payments offering for B2B customers in all states earlier this year. It also plans to “gradually” expand to Africa, South America and Southeast Asia.

Target Global led Mercuryo’s Series A, which also included participation from a group of angel investors and brings the startup’s total raised since its 2018 inception to over $10 million.

The company plans to use its new capital to launch a cryptocurrency debit card (spending globally directly from the crypto balance in the wallet) and continuing to expand to new markets, such as Latin America and Asia-Pacific.

Mercuryo’s various products include a multicurrency wallet with a built-in crypto exchange and digital asset purchasing functionality, a widget and high-volume cryptocurrency acquiring and OTC services.

Kozyakov says the company doesn’t charge for currency conversion and has no other “hidden fees.”

“We enable instant and easy cross-border transactions for our partners and their customers,” he said. “Also, the money transfer services lack intermediaries and require no additional steps to finalize transactions. Instead, the process narrows down to only two operations: a fiat-to-crypto exchange when sending a transfer and a crypto-to-fiat conversion when receiving funds.”

Mercuryo also offers crypto SaaS products, giving customers a way to buy crypto via their fiat accounts while delegating digital asset management to the company.

“Whether it be virtual accounts or third-party customer wallets, the company handles most cryptocurrency-related processes for banks, so they can focus more on their core operations,” Kozyakov said.

Mike Lobanov, Target Global’s co-founder, said that as an experiment, his firm tested numerous solutions to buy Bitcoin.

“Doing our diligence, we measured ‘time to crypto’ – how long it takes from going to the App Store and downloading the app until the digital assets arrive in the wallet,” he said.

Mercuryo came first with 6 minutes, including everything from KYC and funding to getting the cryptocurrency, according to Lobanov.

“The second-best result was 20 minutes, while some apps took forever to process our transaction,” he added. “This company is a game-changer in the field, and we are delighted to have been their supporters since the early days.”

Looking ahead, the startup plans to release a product that will give businesses a way to send instant mass payments to multiple customers and gig workers simultaneously, no matter where the receiver is located.

Powered by WPeMatico

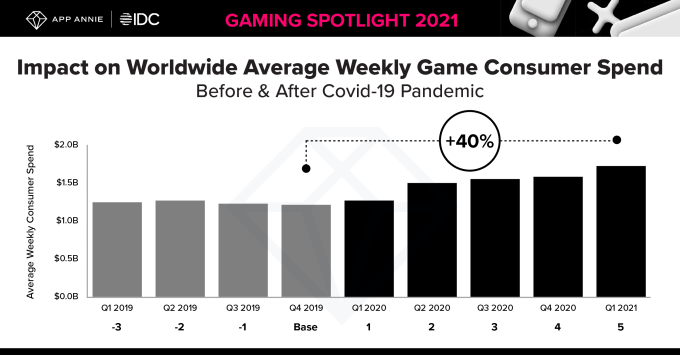

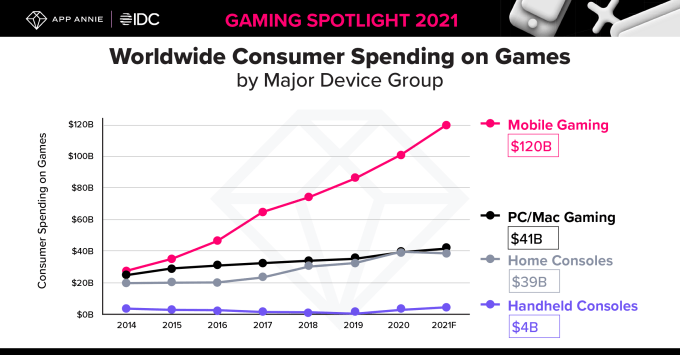

The COVID-19 pandemic drove increased demand for mobile gaming, as consumers under lockdowns looked to online sources of entertainment, including games. But even as COVID-19 restrictions are easing up, the demand for mobile gaming isn’t slowing. According to a new report from mobile data and analytics provider App Annie in collaboration with IDC, users worldwide downloaded 30% more games in the first quarter of 2021 than in the fourth quarter of 2019, and spent a record-breaking $1.7 billion per week in mobile games in Q1 2021.

That figure is up 40% from pre-pandemic levels, the report noted.

Image Credits: App Annie

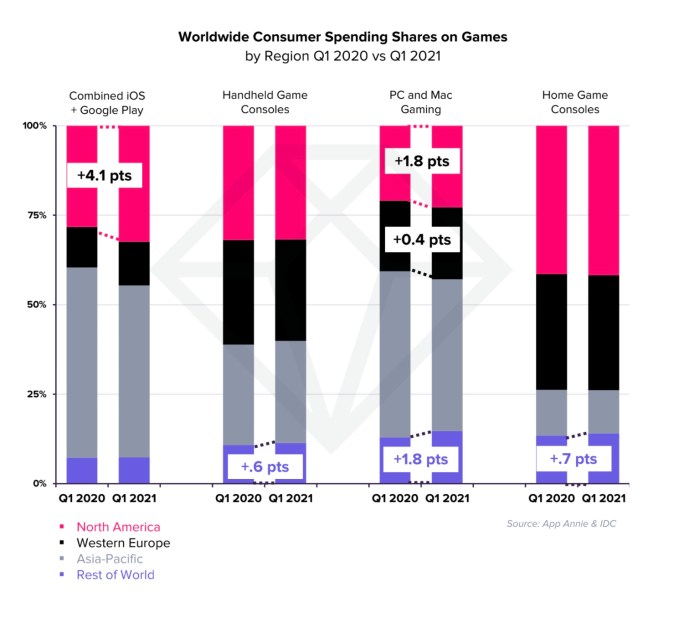

The U.S. and Germany led other markets in terms of growth in mobile game spending year-over-year as of Q1 2021 in the North American and Western European markets, respectively. Saudi Arabia and Turkey led the growth in the rest of the world, outside the Asia-Pacific region. The latter made up around half of the mobile game spend in the quarter, App Annie said.

The growth in mobile gaming, in part accelerated by the pandemic, also sees mobile further outpacing other forms of digital games consumption. This year, mobile gaming will increase its global lead over PC and Mac gaming to 2.9x and will extend its lead over home games consoles to 3.1x.

Image Credits: App Annie

However, this change comes at a time when the mobile and console market is continuing to merge, App Annie notes, as more mobile devices are capable of offering console-like graphics and gameplay experiences, including those with cross-platform capabilities and social gaming features.

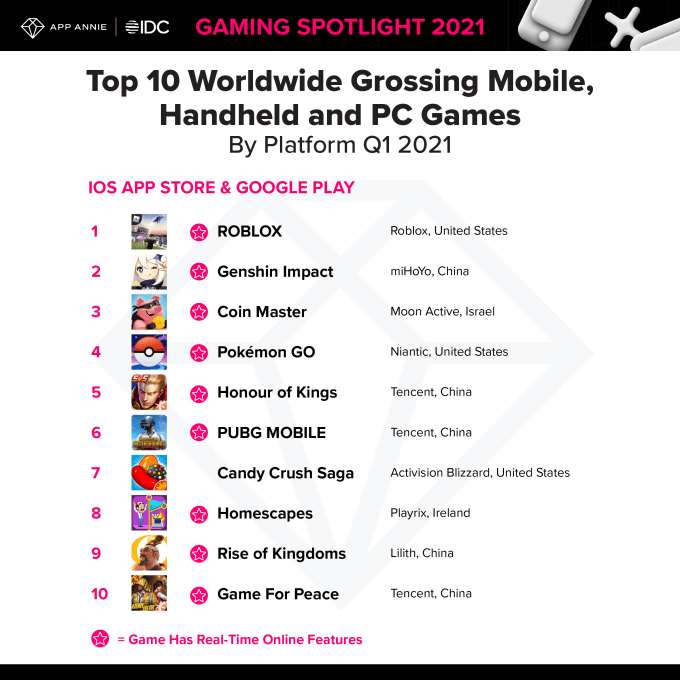

Games with real-time online features tend to dominate the Top Grossing charts on the app stores, including things like player-vs-player and cross-play features. For example, the top grossing mobile game worldwide on iOS and Google Play in Q1 2021 was Roblox. This was followed by Genshin Impact, which just won an Apple Design Award during the Worldwide Developer Conference for its visual experience.

Image Credits: App Annie

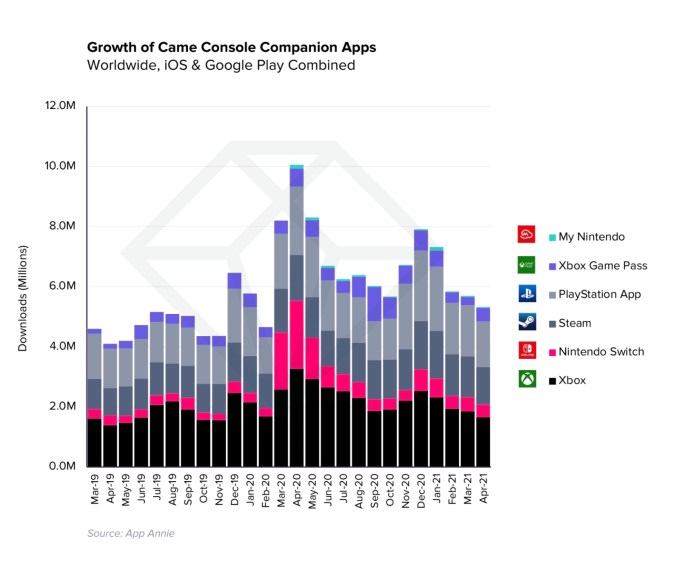

The report also analyzed the ad market around gaming and the growth of mobile companion apps for game consoles, including My Nintendo, Xbox Game Pass, PlayStation App, Steam, Nintendo Switch and Xbox apps. Downloads for these apps peaked under lockdowns in April 2020 in the U.S., but continue to see stronger downloads than pre-pandemic.

Image Credits: App Annie

On the advertising front, App Annie says user sentiment toward in-game mobile ads improved in Q3 2020 compared with Q3 2019, but rewarded video ads and playable ads were preferred in the U.S.

Powered by WPeMatico

On-demand mobility, when done successfully, strikes a balance between demand and supply while providing reliable service and making a profit. It’s a sweet spot that can be difficult, if not impossible, to find.

Autofleet, a startup that develops fleet optimization software to redirect underused vehicles into ride-hailing and delivery services, wants to solve that mission impossible. Now, the company founded by former Avis and Gett employees, has raised $7.5 million in seed and Series A funding to expand into international markets and grow its research and development team.

The Series A was led by MizMaa Ventures with participation from Maniv Mobility, Next Gear Ventures and Liil Ventures. Its seed financing was led by Maniv Mobility.

Autofleet developed a fleet management platform that can be used by rental car companies, car sharing operators and automakers to launch or better manage mobility services. The platform includes a booking app and integrations to delivery services, demand prediction, pooling and optimization algorithms as well as a driver app, and control center. The company also has developed a simulator tool that lets operators plan how a fleet will be deployed before a single vehicle hits the road.

For example, a rental company with abundant inventory and little demand for traditional multi-day contracts could use the platform to launch and then manage a car-sharing service. Autofleet already has partnerships with Avis Budget Group, Zipcar, Keolis and Suzuki .

That focus on managing supply side constraints is what attracted Maniv Mobility to invest in the seeding and Series A rounds, according the firm’s general partner Olaf Sakkers.

Autofleet’s biggest markets today are in Europe and the U.S., CEO Kobi Eisenberg told TechCrunch . The company is seeing early traction and fast growth in Latin America and Asia-Pacific. Eisenberg said they plan to double down on these markets. The company also expects to announce a partnership in Asia to accelerate growth in that region.

Autofleet is also looking for new opportunities for how vehicle fleets can be used, including ways to help micromobility companies improve their unit economics, according to Eisenberg.

In this age of COVID-19 — when asset-heavy businesses like rental car companies have seen their businesses upended — Autofleet has already discovered new uses for its platform. The platform is being used to help companies shift fleets to meet today’s demand for logistics and medical transportation. Autofleet is also selling its platform to companies looking to leverage their vehicle assets for their delivery services.

“We’re hearing from fleet partners around the globe who are experiencing dramatic drops in demand, and therefore significant portions of their fleet and drivers are un-utilized,” Eisenberg said. “At the same time, we have seen a sharp increase in demand for delivery services from businesses across all verticals: retail and supermarkets, restaurants.”

Powered by WPeMatico

One of the biggest trends in the world of financial technology has been an ongoing push towards consolidation, where larger fish are snapping up smaller fish (including a proliferation of interesting startups) to get improved economies of scale in a business model where every transaction brings incremental returns. But today, a startup that has built the concept of consolidation into its basic DNA has raised another round of funding to continue doubling down on its business.

Rapyd — a London-based startup that has built an API that lets customers tap into a range of financial services spanning payments, checkout, funds collection, fund disbursements, compliance as a service, foreign exchange, card issuing and soon logistics across a wide range of geographies — has picked up an additional $20 million. Rapyd’s valuation with the funding is now at $1.2 billion (up from just under $1 billion in October).

The $20 million comes from new investment firm Durable Capital Partners.

Notably, it was only in October that Rapyd announced a $100 million raise. CEO and co-founder and Arik Shtilman said that Rapyd has now raised $180 million in total, with previous investors in the startup including Oak HC/FT Tiger Global, Coatue, General Catalyst, Target Global, Stripe and Entrée Capital. (Stripe, itself a fast-growing fintech upstart, remains only a financial investor in the company, Shtilman confirmed.)

Durable is the firm founded by Henry Ellenbogen, formerly a star investor at T. Rowe Price, in what Rapyd said was the firm’s first investment. (Note: Durable was also announced earlier as an investor in Convoy’s $400 million round, some clear signs that it’s open for business now.)

With Rapyd only recently raising a round, Shtilman said that the reason for the — err — rapid follow up was because the company is gearing up to make some acquisitions, as it too moves in on the consolidation trend by adding in more tools into its “Swiss Army Knife” of services.

“We’ve started to look at two acquisitions that were bigger than what we originally planned, with prices more in the range of $100 million,” he said. Up to now, Rapyd has largely built its technology from the ground up, but this will be about “getting at new business very quickly,” he added. Both deals are in progress now and are likely to close in February / March. One is of a card issuing platform (a la Marqeta), and the other is of a company based in Asia Pacific that is a significant player in payments in the region.

The focus on Asia Pacific both for testing out new services and acquisitions is in part because this, along with Latin America, have shaped up to be important geographies for the company. In the last three months, Rapyd has signed on 20 additional large-scale companies, Shtilman said, with several of them based out of, or serving, customers out of the two regions.

In fact, Rapyd doesn’t talk much about actual customers, but they include e-commerce merchants, gig-economy platforms — including Uber — financial institutions, and technology providers. The basic pitch is that financial services are complex, and providing one like payments often means having to offer others. Building these from scratch if this is not your core competency can be time-consuming and costly, and so that is where a company like Rapyd steps in with its API.

This is what attracted its newest investor, too. “Durable Capital Partners LP has a vision to identify and invest in promising early stage growth companies and invest in teams that have bold ideas but can also execute at a world-class level and build much larger companies,” said Ellenbogen in a statement. “I believe the Fintech-as-a-Service category has tremendous potential as companies seek to embed financial services as an integral part of the next generation technology stack. I believe Rapyd is very well positioned to drive this trend and I believe Arik’s track record in scaling cloud-based businesses will deliver success in this sector.”

When we last talked with Rapyd in October, we asked Shtilman about whether the company would ever move into logistics as part of its range of tools. After all, when you think about the complexities of procuring, storing and moving goods, it’s clear that logistics is one of the cornerstones you need to get right in an online business.

He said that this was on the company’s roadmap, and now Rapyd is in a pilot in Indonesia — an interesting test bed, considering that the country’s is spread across thousands of islands — where it has integrated a logistics service and given access to a single merchant as stage one of its closed beta. It’s also in discussions with other companies about how it can incorporate their services into the Rapyd platform to provide further “logistics as a service” to customers. He also confirmed the Durable has been a help here, by making an introduction to Convoy as part of that wider strategy.

Powered by WPeMatico

The latest pairing between a tech upstart and a financial titan is a digital prepaid card targeted at Southeast Asia’s 430 million-plus unbanked and underserved population.

On Monday, Razer, the Singapore-based company best known for its gaming laptops and peripherals, announced a partnership with Visa to develop a Visa prepaid solution. The service, which allows unbanked users to top up and cash out easily, will be available as a mini program embedded in Razer Pay, the gaming company’s mobile payments app. That means Razer’s 60 million registered users will be able to pay at any of the 54 million merchant locations around the world that take Visa.

Going virtual is the natural step given the region’s fast-growing digital population, but the pair does not rule out the possibility to introduce a physical prepaid card down the road, Razer’s chief strategy officer Li Meng Lee told TechCrunch over a phone interview.

Both parties have something to gain from this marriage. Hong Kong-listed Razer has in recent years been doubling down on fintech to prove it’s more than a hardware company. Payment services seem like an inevitable development for Razer whose users in the region are accustomed to buying in-game credits at convenience stores.

“For many years, the people who have been making digital payments before it became a sexy word in the last couple of years… [many of them] are the gamers who go to a 7-Eleven, pay in cash, and get a pin code to buy virtual skins for the games,” noted Lee. “Because of that, we’ve been able to build up more than a million service points across Southeast Asia.”

The key differentiator of Razer’s prepaid service, Lee said, is that customers paying at Visa merchants don’t have to already own a bank account, whereas that prerequisite is common for many other e-wallet services.

Razer’s fintech arm Pay is handling transactions for a slew of internet services like Lazada and Grab and has made a big offline push, boasting a network of more than one million touchpoints through retailers including 7-Eleven and Starbucks where it’s accepted.

All in all, Razer claimed it processed over $1.4 billion in payment value last year — but that includes its “merchant services” business, covering on and offline payments, as well as Razer Pay.

The payment app first launched in Malaysia in mid-2018 and recently branched into Singapore as its second market. Lee said the service plans to roll out in the rest of Southeast Asia soon, upon which the Visa prepaid mini app will also be available in those markets.

For Visa, the tie-up with an internet firm could be a potential boost to its reach in the mobile-first Southeast Asia where some 213 million millennials and youths live.

“This is a great opportunity for us to be working with Razer in addressing how we work to bring the unbanked and underserved population into the financial system,” Chris Clark, Visa’s regional president for the Asia Pacific, told TechCrunch. “We will be doing some work with Razer on financial literacy and financial planning to bring that education to the population across the region.”

Razer’s fintech ambition has been evident since it announced to gobble up MOL, a company that offers online and offline payments in Southeast Asia, in April 2018. Besides payments, Lee said other microfinance services such as lending and insurance are also on the cards as part of an effort to ramp up user stickiness for Razer’s fintech arm.

Note: The original version of this article has been updated to correct that Razer’s $1.4 billion in GMV includes merchant services as well as Razer Pay.

Powered by WPeMatico

Spending on artificial intelligence systems in the Asia-Pacific region is expected to reach $5.5 billion this year, an almost 80% increase over 2018, driven by businesses in China and the retail industry, according to IDC. In a new report, the research firm also said it expects AI spending to climb at a compound annual growth rate of 50% from 2018 to 2022, reaching a total of $15.06 billion in 2022.

This means AI spending growth in the Asia-Pacific region is expected to outpace the rest of the world over the next three years. In March, IDC forecast that worldwide spending on AI systems is expected to grow at a CAGR of 38% between 2018 to 2022.

Most of the growth will happen in China, which IDC says will account for nearly two-thirds of AI spending in the region, excluding Japan, in all forecast years. Spending on AI systems will be driven by retail, professional services and government industries.

Retail demand for AI-based tools will also lead growth in the rest of the region, as companies begin to rely on it more for merchandising, product recommendations, automated customer service and supply and logistics. While the banking industry’s AI spending trails behind retail, it will also begin adopting the tech for fraud analysis, program advisors, recommendations and customer service. IDC forecasts that this year, companies will invest almost $700 million in automated service agents. The next largest area for investment is sales process recommendations and automation, with $450 million expected, and intelligent process automation at more than $350 million.

The fastest-growing industries for AI spending are expected to be healthcare (growing at 60.2% CAGR) and process manufacturing (60.1% CAGR). In terms of infrastructure, IDC says spending on hardware, including servers and storage, will reach almost $7 billion in 2019, while spending on software is expected to grow at a five-year CAGR of 80%.

Powered by WPeMatico