articles

Auto Added by WPeMatico

Auto Added by WPeMatico

Orbit, a startup that is building tools to help organizations build communities around their proprietary and open-source products, today announced that it has raised a $4 million seed funding round led by Andreessen Horowitz’s Martin Casado. A number of angel investors, including Chris Aniszczyk, Jason Warner and Magnus Hillestad, as well as the a16z’s Cultural Leadership Fund, also participated, in addition to previous backers Heavybit and Harrison Metal.

The company describes its service as a “community experience platform.” Currently, Orbit’s focus is on Developer Relations and Community teams, as well as open-source maintainers. There’s no reason the company couldn’t branch out into other verticals as well, though, given that its overall framework is really applicable across all communities.

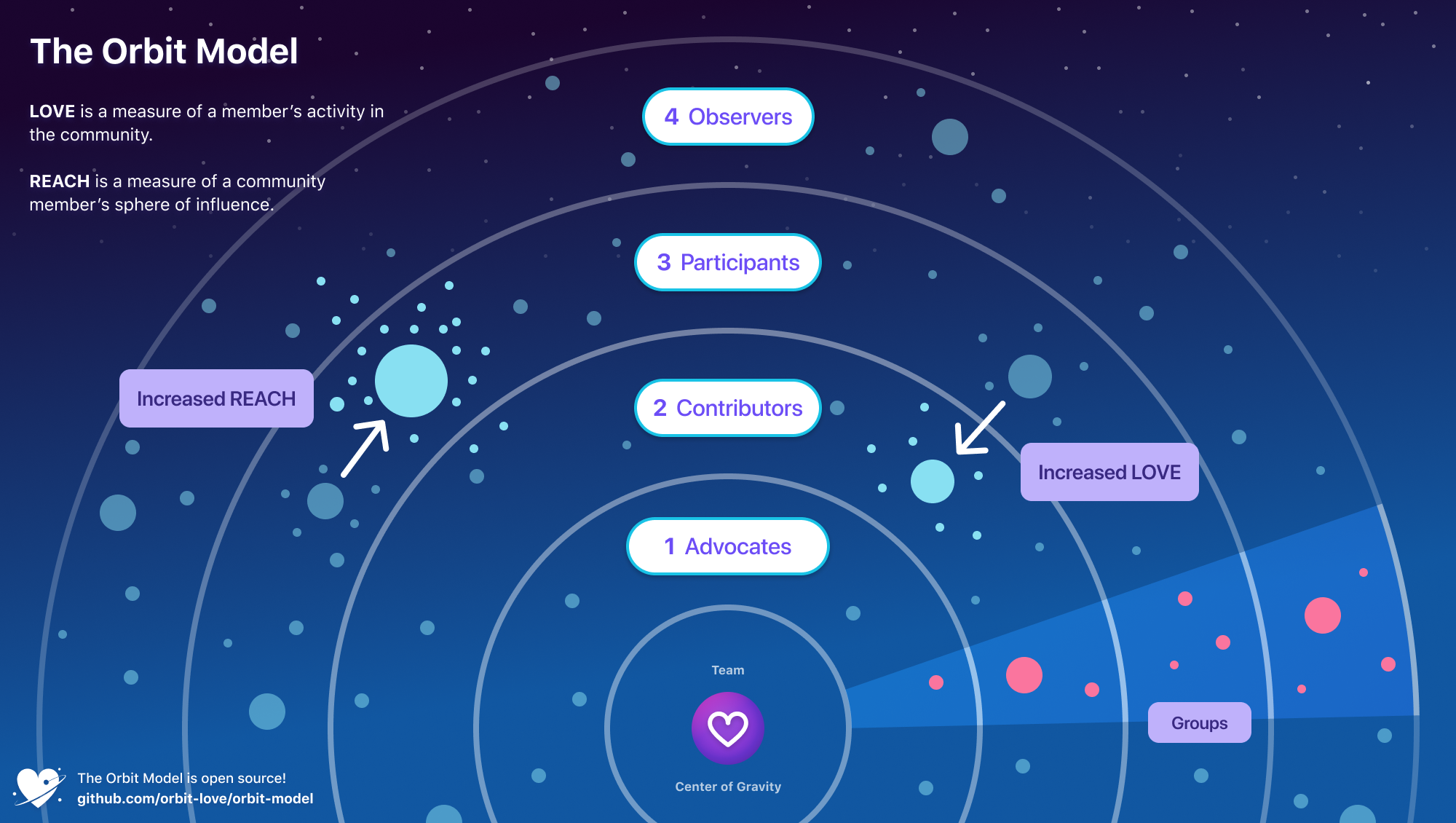

Orbit team: Patrick Woods, Nicolas Goutay and Josh Dzielak

As Orbit co-founder Patrick Woods told me, community managers have generally had a hard time figuring out who was really contributing to their communities because those contributions can come in lots of forms and often happen across a wide variety of platforms. In addition, the sales and marketing teams also often don’t understand how a community impacts a company’s bottom line. Orbit aggregates all of these contributions across platforms.

“There is a lack of understanding around the ways in which community impacts go-to-market and business value,” Woods told me when I asked him about the genesis of the idea. “There’s a big gap in terms of the tooling associated with that. Many companies agree that community is important, but if you put $1 in the community machine today, it’s hard to know where that’s going to come out — and is it going to come out in terms of $0.50 or $100? This was a set of challenges that we noticed across companies of all sizes.”

Image Credits: Orbit

Especially in open-source communities, there will always be community members who create a lot of value but who don’t have a commercial relationship with a company at all. That makes it even harder for companies to quantify the impact of their communities, even if they agree that community is an important way to grow their business and that, in Orbit’s words, “community is the new pre-sales.”

At the core of Orbit (the company) is Orbit the open-source community framework. The founding team of Woods (CEO) and Josh Dzielak (CTO) developed this framework to help organizations understand how to best build what the team calls a “high gravity community” to attract new members and retain existing ones — and how to evaluate them. You can read more about the concept here.

Image Credits: Orbit

“We’re trying to reframe the discussion away from an extractive worldview that says how much value can we generate from this lead? It’s actually more about how much love can we generate from these community members,” Woods said. “Because, if you think about the culture associated with what we’re trying to do, it’s fundamentally creative and generative. And our goal is really to help people think less about value extraction and more about value creation.”

At the end of the day, though, no matter the philosophy behind your community-building efforts, there has to be a way to measure ROI and turn some of those community members into paying customers. To do that, Orbit currently pulls in data from sources like GitHub, Twitter and Discourse, with support for Slack and other tools coming soon. With that, the service makes it far easier for community managers to keep tabs on what is happening inside their community and who is participating.

Image Credits: Orbit

In addition to the built-in dashboards, Orbit also provides an API to help integrate all of this data into third-party services as well.

“One of the key understandings that drives the Orbit vision is that a community is not a funnel and building a community is not about conversions, but making connections; cultivating dialog and engagement; being open and giving back; and creating value versus trying to capture it,” a16z’s Casado writes. “The model has proven to be very effective, and now Orbit has built a product around it. We strongly believe Orbit is a must-have product for those building developer-focused companies.”

The company is already working with just under 150 companies and its users include the likes of Postman, CircleCI, Kubernetes and Apollo GraphQL.

The company will use the new round, which closed a few weeks ago, to, among other things, build out its go-to-market efforts and develop more integrations.

Powered by WPeMatico

If I were to pick one thing that unites the global tech scene in terms of culture I would point to the respect and reverence accorded to startup founders.

After all, creating your own company is an ambition many of us harbor. It can bring with it unparalleled freedom, a lasting legacy, prestige, wealth and the ability to do good. Across social and traditional media the feats of founders big and small are lauded for their genius on a daily basis. Many entrepreneurs go to great lengths to showcase their backbreaking hard work and eye-popping success. An outsider would be forgiven for believing that every founder is living the dream as a result of their talent and toil.

Of course, as with nearly every image projected online, the reality is quite different. There is a seldom talked about price of being a founder — the impact on one’s mental health.

A recent study by the National Institute of Mental Health found that 72% of entrepreneurs are directly or indirectly impacted by mental health issues. This compares to 48% of the general population. The damage can also affect loved ones — 23% of entrepreneurs report that they have family members with problems, which is 7% higher than the relations of nonentrepreneurs.

I am in no way a mental health expert. But what I do know from both my own experience and speaking to scores of business owners I work with is that being a founder is an inherently lonely job. Pressure is high and uncertainty pervades every decision. Fear of failure is ever present. Unaddressed, these issues can take a serious toll.

The unpalatable truth is that the situation appears to be getting worse. A similar study conducted in 2015 by Dr. Michael A. Freeman found the rate of mental health issues among founders to be lower — at 50%. While comparing different research pieces is inexact, we only need to look at how the global recession has damaged many companies and how working from home has contributed to feelings of isolation, to know that the environment for startups has got harder this year. Added to this mix is how social media continues to promote an unhealthy fetishization of hustle culture and founding myths.

A number of founders have told me that they have constant feelings of inadequacy and guilt when they compare themselves to the startup gurus who celebrate working 24/7, are constantly selling, raising money or making their millions. They feel they should be working harder or be doing better — just like all the people they read about.

So how do we address this? The first step is talking about it. This means having an environment where we can be honest that not everything is always fine. Speaking to a fellow founder, not about commercial concerns, but about personal worries can be revelatory. I’ve seen it happen in our community. It’s like an “Emperor’s New Clothes” moment.

The myth of the bulletproof, genius, hustling founder can disappear in a puff of smoke as people suddenly realize they are not alone. They find that the concerns, anxieties and uncertainties they feel are almost universal.

Experienced founders can provide invaluable support to people new to the startup scene. They can share their experiences, both failures and success, and reveal some of their coping mechanisms. I would strongly advise founders who are experiencing some of the worries I’ve outlined to actively seek out advice from both their peers and potential mentors — much in the way they may seek out commercial guidance.

Next, we need to address how we tackle the culture and myths around being a founder. Business owners need to know that many of the extraordinary “success stories” they see celebrated online are exactly that — extraordinary.

Similarly, those that promote the principle that working all hours is the only way to be successful are at best talking about what works for them, and are at worst, engaging in a performance to achieve attention. We need to think carefully about how we respond to these posts. There is a fine line between being supportive and enabling unhealthy or damaging behavior and philosophy.

After all, success in the startup scene is all relative. For some owning a small business that makes them a decent income with a good work-life balance is the goal. For others, it is simply being able to do what they love in the way that they want. Very few will get the exit that makes them a millionaire, and an infinitesimally small minority will build the next Facebook . I cannot stress enough how important it is for founders to keep their aims and ambitions in perspective and ignore the noise they hear online.

More broadly, the industry, including the media, does need to get wiser about how it views and represents founders. For example, a pervasive myth is that some of the biggest tech companies in the world started in garages with no money, then through the genius and sheer bloodymindedness of their founder they were grown into a massive corporation.

The reality is that the vast majority of these tech companies benefited from substantial seed capital from family or connections almost from day one. These founders were also quickly surrounded by highly talented people who did a lot of the heavy lifting and, whisper it, a truckload of good luck. In short, the idea of the superhuman founder perpetuated in the industry is, in nearly all cases, nonsense.

In a similar vein, there are also issues around how we frame success and failure.

Success, as I’ve mentioned earlier, is nearly always couched in the most basic numerical terms. The “unicorn” label is bandied about so often that many people fail to realize that it’s simply a valuation that a few investors have given a company. It does not reflect whether the business is actually successful in the traditional sense, i.e., making money. Generally, the startup scene celebrates and idolizes founders who make big exits or achieve “unicorn status” — less is spoken about the thousands of SMEs that employ people, develop and patent new tech, make a tidy profit and pay taxes.

With failure, there is an altogether different problem. The startup scene downplays failure as par for the course. It is, on the face of it, one of the industry’s great virtues. It enables people to try without fear of embarrassment. However, in practice, it can actually minimize real-world fears nearly all founders have. Failure cannot just be brushed off if you’ve devoted years of your life, spent a lot of money and have staff who rely on you. By simply thinking of failure as part of the process we cannot address and talk about this real source of concern in an open way. “Fail fast” only works for those who can afford it.

Individually, these issues may seem like nothing but white noise and the cure for suffering founders may simply be to get off social media. Unfortunately, it isn’t that simple. Social and traditional media is amplifying startup culture, not creating it. The same tropes are on display at every tech conference and meetup. To fit in, the founder is expected to be a fearless, genius visionary. Deviation from this norm, such as by displaying vulnerability around mental health, is by inference, failure.

Despite its shortcomings in relation to diversity, the startup scene is generally one of the most progressive, collaborative and open industries in the world. These virtues are ideally suited to tackling the reluctance to discuss mental health and creating the network of support that ensures people don’t suffer alone.

To make this happen, we need to dispense with the myths and hagiography around being a founder and be more honest about what the reality of running a business actually entails.

Powered by WPeMatico

As President-elect Joe Biden readies his transition team and sets the agenda for his first 100 days in office, startups can expect to see some movement on long-stalled infrastructure initiatives that could mean big boosts to their business.

Infrastructure is high on the list of priorities of the incoming Biden Administration as the former vice president hopes to make good on his campaign promise to “build back better.”

American infrastructure has been crumbling for decades without significant investment from the federal government, and much of what will be replaced will also be upgraded with new technology, according to people familiar with the Biden plan.

That means tech companies focused on next-generation telecommunications and utility infrastructure, transportation, housing and construction tech around energy efficiency could see new dollars pour in over the next four years.

“Infrastructure and build out of the clean energy economy … doesn’t necessarily mean large wind or large solar projects. It could mean advanced metering … it can be new engine technologies,” said Dan Goldman, a managing partner at Clean Energy Ventures. “We think that that can be a huge opportunity for job creation … not only putting people back to work but putting people back to work in high quality jobs.”

And there’s a willingness to encourage these infrastructure projects in less partisan ways in states like Massachusetts, Virginia and Florida, which are actively building out electric vehicle infrastructure and renewable energy projects, Goldman said.

While the federal government will ultimately be distributing the cash, startups can expect to see the spending actually come from municipalities and state governments, which often have a better understanding of local needs and where the money should go.

The electrification of everything — a component of any zero-carbon movement — requires significant upgrades to existing power infrastructure. That means everything from systems management technologies to distribution facilities to ways to store power that can be moved on to the grid.

“Without that infrastructure investment it gets quite challenging,” said Abe Yokell, a co-founder and managing partner of Congruent Ventures.

He pointed to large-scale energy storage technologies as one solution, but management systems for utilities will be another area of interest.

Those infrastructure initiatives will likely mean good things for battery companies like Form Energy, which signed its first major contract with Great River Energy earlier this year; or Antora and Malta, which store energy as heat; or Quidnet, which has a pumped hydroelectric play for large-scale energy storage by pumping water into the gaps between rocks underground that creates pressure and can force water back up through a generator.

Other large-scale energy storage companies working on developing and installing batteries could benefit as well. That means good things for Tesla, which has a few major battery installs under its belt, and Fluence, which manages and operates big install projects.

Natel Energy, another startup working on energy storage (and generation) using hydropower, could also find its technology in the mix, according to company founder, Gia Schneider.

Schneider sees three potential pitches for her company’s technologies. “Climate change is water change,” she said. “We have a bucket in energy, a bucket of stuff in environmental and a bucket of stuff in working lands.”

Powered by WPeMatico

Startups need to live in the future. They create roadmaps, build products and continually upgrade them with an eye on next year — or even a few years out.

Big companies, often the target customers for startups, live in a much more near-term world. They buy technologies that can solve problems they know about today, rather than those they may face a couple bends down the road. In other words, they’re driving a Dodge, and most tech entrepreneurs are driving a DeLorean equipped with a flux-capacitor.

That situation can lead to a huge waste of time for startups that want to sell to enterprise customers: a business development black hole. Startups are talking about technology shifts and customer demands that the executives inside the large company — even if they have “innovation,” “IT,” or “emerging technology” in their titles — just don’t see as an urgent priority yet, or can’t sell to their colleagues.

How do you avoid the aforementioned black hole? Some recent research that my company, Innovation Leader, conducted in collaboration with KPMG LLP, suggests a constructive approach.

Rather than asking large companies about which technologies they were experimenting with, we created four buckets, based on what you might call “commitment level.” (Our survey had 211 respondents, 62% of them in North America and 59% at companies with greater than $1 billion in annual revenue.) We asked survey respondents to assess a list of 16 technologies, from advanced analytics to quantum computing, and put each one into one of these four buckets. We conducted the survey at the tail end of Q3 2020.

Respondents in the first group were “not exploring or investing” — in other words, “we don’t care about this right now.” The top technology there was quantum computing.

Bucket #2 was the second-lowest commitment level: “learning and exploring.” At this stage, a startup gets to educate its prospective corporate customer about an emerging technology — but nabbing a purchase commitment is still quite a few exits down the highway. It can be constructive to begin building relationships when a company is at this stage, but your sales staff shouldn’t start calculating their commissions just yet.

Here are the top five things that fell into the “learning and exploring” cohort, in ranked order:

Technologies in the third group, “investing or piloting,” may represent the sweet spot for startups. At this stage, the corporate customer has already discovered some internal problem or use case that the technology might address. They may have shaken loose some early funding. They may have departments internally, or test sites externally, where they know they can conduct pilots. Often, they’re assessing what established tech vendors like Microsoft, Oracle and Cisco can provide — and they may find their solutions wanting.

Here’s what our survey respondents put into the “investing or piloting” bucket, in ranked order:

By the time a technology is placed into the fourth category, which we dubbed “in-market or accelerating investment,” it may be too late for a startup to find a foothold. There’s already a clear understanding of at least some of the use cases or problems that need solving, and return-on-investment metrics have been established. But some providers have already been chosen, based on successful pilots and you may need to dislodge someone that the enterprise is already working with. It can happen, but the headwinds are strong.

Here’s what the survey respondents placed into the “in-market or accelerating investment” bucket, in ranked order:

Powered by WPeMatico

When salespeople in California’s dynamic tech economy transition between jobs, the value they bring to their new company is often their customer relationships. Startup founders and salespeople considering joining competitors often assume continuing to maintain these customer relationships is noncontroversial given California’s well-known policy favoring employment mobility and outlawing non-competition agreements.

Yet California trade secret law regarding the ability of salespeople to solicit these customers once they jump to a competitor is increasingly confused and fails to provide meaningful guidance on what type of conduct is permissible. Thus, a salesperson’s move from their current company to a competitor is risky given it is unclear whether and to what extent they can continue servicing clients or contacts they previously worked with.

A salesperson working for a value-added reseller (VAR), for instance, should understand what they are getting into before moving to a competitor — they may risk longstanding relationships with original equipment manufacturers (OEMs) and end users. This article explains the conflicting law on this issue so that salespeople planning on jumping ship, and the companies considering hiring them, can be informed regarding the current legal landscape.

In the vast majority of states, employers can, and do, require employees to enter into some form of non-competition agreement in exchange for continued employment.1 In contrast, California has a long-standing policy of favoring employment mobility over an employer’s concerns. California’s policy is embodied in Business and Professions Code section 16600, which provides: “Except as provided in this chapter, every contract by which anyone is restrained from engaging in a lawful profession, trade, or business of any kind is to that extent void.”

California courts “have consistently affirmed that section 16600 evinces a settled legislative policy in favor of open competition and employee mobility” that is intended to “ensure that every citizen shall retain the right to pursue any lawful employment and enterprise of their choice.”2 The policy also allows California employers to “compete effectively for the most talented, skilled employees in their industries, wherever they may reside.”3 Accordingly, unlike in most states, the “interests of the employee in [their] own mobility and betterment” generally outweigh the “competitive business interests of the employers.”4

Courts have broadly applied section 16600, invalidating non-competition agreements, which would prohibit or restrict an employee from leaving to work for a competitor.5 Importantly, courts have also invalidated contractual provisions purporting to restrict an employee’s ability to leave and then solicit the company’s customers.6 In other words, a salesperson cannot be contractually precluded from leaving their company, joining a competitor and continuing to solicit, service and communicate with their former company’s clients. Furthermore, with limited exceptions, California courts will disregard a “choice of law” provision purporting to mandate that the court follow the law from a state that enforces noncompetes.7

Powered by WPeMatico

Subscription services are on the rise. During the pandemic, Americans have been spending more time at home and more money on the digital products that make navigating our new normal easier.

More than ever, Americans’ lives are aided by companies like Netflix, Instacart and, of course, Amazon, which reported record-setting earnings from its 2020 Prime Day savings event.

A recent survey even found that spending on subscription services had more than tripled since March, with one in three respondents saying they’d purchased a new online subscription while quarantining.

Now, a new concern lingers: Is the market getting oversaturated? The question doesn’t just apply to streaming services and food delivery companies — it’s an issue financial technology businesses can’t afford to ignore.

As subscriptions become an increasingly alluring business model, fintechs will be forced to consider whether this proven strategy is worth the risk.

In the CompareCards survey, two-thirds of respondents said they purchased a new streaming service mainly for entertainment. Still, that doesn’t mean there isn’t room for fintechs to carve out their own space.

Bradley Leimer, co-founder of the financial consulting firm Unconventional Ventures, said he’s certainly seen more fintechs exploring subscription models. As Leimer explained, the financial services industry may have not fully embraced the idea, but it’s “starting to take notice.” Leimer, who has more than 25 years of experience in the industry, believes fintechs can learn a lot from subscription services — provided they’re willing to look in the right place.

One major lesson? Transparency. Subscription services give companies an opportunity to be upfront about their fees, as well as their benefits.

“When we talk about subscriptions, the more clear and more transparent we are, the better,” Leimer said.

Acorns is an easy case study. The microinvesting app offers three subscription levels — lite, personal and family — each with a clearly explained list of features. For what it’s worth, the company added more than 2 million users between March 2019 and March 2020, according to Forbes.

Leimer said fintechs should also take note of the way subscription services collaborate. For example, he pointed out how Amazon users can add an HBO subscription to their Prime Video account, essentially “bundling” two subscriptions into one. Fintechs, Leimer said, could stand to take a page out of that playbook.

“There are a lot of ways to sort of skin that cat — for a fintech company to generate income and for a customer to get value on top of that,” Leimer said.

Powered by WPeMatico

Now that COVID-19 has accelerated the adoption of digital education tools, edtech has become one of the hottest areas of investment.

As someone who has been in edtech for nearly 20 years, this sounds like the precise moment to capitalize on all the newfound interest. Which is why what I’m about to say might be surprising: I’m leaving edtech for the world of gaming with my new company, Solitaired.

I first got into edtech in high school, when a friend and I founded EasyBib, a website that helped students cite sources for their papers. At the time, we were just students who felt there had to be a better way than formatting tedious citations for research papers by hand. But as we dove into the business further, we realized there was a lot to like about bibliographies and education technology in general.

For one, the education market is large. There are more than 56 million K-16 students in the U.S., and over 1.3 billion globally. Federal, state and local governments spend an aggregate of 5% of GDP on education, and that doesn’t even include what students and parents spend on content and technology.

Secondly, it’s structured. Students generally all go through the same curriculum together. That means most students have the same problem in the same way; if you solve a problem for one group of users, you’ve probably solved it for most users.

The citation problem was just like that. When we sold our company to Chegg, we were already reaching four out of five students that needed bibliographies, or over 30 million students in the U.S. Edtech companies that help students with math, chemistry, homework help, tutoring and other curricular needs can build massive audiences quickly.

Edtech that’s part of the curriculum also has high engagement. EasyBib users stayed on our site for nearly ten minutes per session, creating one citation after another for their bibliographies. For direct-to-consumer edtech companies that are ad and subscription driven, this behavior creates many monetization opportunities.

While we grew fast, our endemic market opportunity was limited. Why? The strengths of edtech can also be its downsides, especially for a startup. On the user growth front, we focused on school relationships, marketing and SEO. But once we reached four out of every five students in the U.S., there wasn’t much more room to grow.

To increase engagement even further, we tried a number of things: encouraging more citation creation, adding research and note-taking features and building a Chrome extension to be more ever-present in the user’s research journey. Those efforts fell short too. Ultimately, the school calendar dictated how often students needed to use us, and we were constrained by the number of research papers teachers assigned.

These challenges can certainly be overcome. But as a startup, we had to decide if we wanted to pursue adjacencies and expansions ourselves. Ultimately, this realization was one of the reasons we decided to sell our company to Chegg, which had a wider user base and product synergies that we couldn’t achieve on our own. As anyone who follows Chegg might know, they’ve been very successful in accelerating the edtech digital transformation.

When we began thinking about our second business, we had these lessons in the back of our mind. That’s when we discovered gaming.

Powered by WPeMatico

Year-in, year-out, the gender gap in venture capital investment continues to be a problem women founders face. While the gender gap in other areas (such as the number of women entering tech in general) may be on the right path, this disparity in funding seems to be stagnant. There has been little movement in the amount of VC dollars going to women-founded companies since 2012.

In fintech, the problem is especially prominent: Women-founded fintechs have raised a meager 1% of total fintech investment in the last 10 years. This should come as no surprise, given that fintech combines two sectors traditionally dominated by men: finance and technology. Though by no means does this mean that women aren’t doing incredible work in the field and it’s only right that women founders receive their fair share of VC investment.

In the short term, women founders can take action to boost their chances at VC success in the current investment climate, including leveraging their community and support network and building the necessary self-belief to thrive. In the long term, there needs to be foundational change to level the playing field for women entrepreneurs. VC funds must look at ways they can bring in more women decision-makers, all the way up to the top.

Let’s dive into the state of gender bias in VC investing as it stands, and what founders, stakeholders and funds themselves can do to close the gap.

In 2019, less than 3% of all VC investment went to women-led companies, and only one-fifth of U.S. VC went to startups with at least one woman on the founder team. The average deal size for female-founded or female co-founded companies is less than half that of only male-founded startups. This is especially concerning when you consider that women make up a much bigger portion of the founder community than proportionately receive investment (around 28% of founders are women). Add in the intersection of race and ethnicity, and the figures become bleaker: Black women founders received 0.6% of the funding raised since 2009, while Latinx female founders saw only 0.4% of total investment dollars.

The statistics paint a stark picture, but it’s a disparity that I’ve faced on a personal level too. I have been faced with VC investors who ask my co-founder — in front of me — why I was doing the talking instead of him. On another occasion, a potential investor asked my co-founder who he was getting into business with, because “he needed to know who he’d be going to the bar with when the day was up.”

This demonstrates a clear expectation on the part of VC investors to have a male counterpart within the founding team of their portfolio companies, and that they often — whether subconsciously or consciously — value men’s input over that of the women on the leadership team.

So, if you’re a female founder faced with the prospect of pitching to VCs — what steps can you take to set yourself up for success?

Women founders looking to receive VC investment can take a number of steps to increase their chances in this seemingly hostile environment. My first piece of advice is to leverage your own community and support network, especially any mentors and role models you may have, to introduce you to potential investors. Contacts that know and trust your business may be willing to help — any potential VC is much more likely to pay you attention if you come as a personal recommendation.

If you feel like you’re lacking in a strong support network, you can seek out female-founder and startup groups and start to build your community. For example, The Next Women is a global network of women leaders from progress-driven companies, while Women Tech Founders is a grassroots organization on a mission to connect and support women in technology.

Confidence is key when it comes to fundraising. It’s essential to make sure your sales, pitch and negotiation skills are on point. If you feel like you need some extra training in this area, seek out workshops or mentorship opportunities to make sure you have these skills down before you pitch for funding.

When talking with top male VCs and executives, there may be moments where you feel like they’re responding to you differently because of your gender. In these moments, channeling your self-belief and inner strength is vital: The only way that they’re going to see you as a promising, credible founder is if you believe you are one too.

At the end of the day, women founders must also realize that we are the first generation of our gender playing the VC game — and there’s something exciting about that, no matter how challenging it may be. Even when faced with unconscious bias, it’s vital to remember that the process is a learning curve, and those that come after us won’t succeed if we simply hand the task over to our male co-founder(s).

While there are actions that women can take on an individual level, barriers cannot be overcome without change within the VC firms themselves. One of the biggest reasons why women receive less VC investment than men is that so few of them make up decision-makers in VC funds.

A study by Harvard Business Review concluded that investors often make investment decisions based on gender and ask women founders different questions than their male counterparts. There are countless stories of women not being taken seriously by male investors, and subsequently not being seen as a worthwhile investment opportunity. As a result of this disparity in VC leadership teams, women-focused funds are emerging as a way to bridge the funding gender gap. It’s also worth noting that women VCs are not only more likely to invest in women-founded companies, but also those founded by Black entrepreneurs. In addition to embracing women and minority-focused investors, the VC community as a whole should ensure they’re bringing in more women leaders into top positions.

From day one, the Prometeo team has made concerted efforts to have both men and women in decision-maker roles. Having women in the founding team and in leadership positions has been crucial in not only helping to fight the unconscious bias that might take place, but also in creating a more dynamic work environment, where diversity of thought powers better business decisions.

Striving for gender equality, both within the walls of VC funds and in the founder community, is also better for businesses’ bottom line. In fact, a study by Boston Consulting Group found that women-founded startups generate 78% for every dollar invested, compared to 31% from men-founded companies.

Here in Latin America, women founders receive a higher proportion of VC investment than anywhere else in the world, so it’s no surprise that women are leading the region’s fintech revolution. Having more women in leadership positions is ultimately a better bet for business.

Closing the gender gap in VC funding is no simple task, but it’s one that must be undertaken. With the help of internal VC reform and external initiatives like community building, training opportunities and women-focused support networks, we can work toward finally making the VC game more equitable for all.

Powered by WPeMatico

So much can change in a day.

This morning, news that a trial COVID-19 vaccine candidate had an effective rate of more than 90% shook the financial world. The Pfizer vaccine is reportedly so effective, the company “will have manufactured enough doses to immunize 15 to 20 million people” by the end of the year, according to the New York Times, appears to have given investors the green light to pile back into companies harmed by the pandemic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The shift of money from shares that proved popular during the summer is massive and abrupt. Zoom and Peloton are down sharply this morning, while Uber and Lyft are soaring. Indeed, the Dow Jones Industrial Average and S&P 500 indices are up around 4.8% and 3.3% respectively, while SaaS and cloud share are off 3.5%.

Investors are taking money out of companies that were expected to do well thanks to the pandemic and moving that capital into firms that were weakened by the pandemic.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Short-term market movements do not always predict the future accurately, so we should not treat today’s trading as gospel.

That said, it’s not hard to draw some basic conclusions from the trading activity. Here’s what I think we can deduce from today’s stock market activity:

Powered by WPeMatico

Whether space is the final frontier remains to be seen, but it’s certainly the next one as far as we’re concerned. On December 16-17, we’re hosting TC Sessions: Space 2020, a two-day online conference and our first event focused squarely on space technology and the early-stage startups and investors that make it possible.

The future of this industry is wide open, and it’s going to require cultivating a deep bench of visionaries to sustain it. And it starts with affordable access for students eager to turn science fiction into fact. Grab your $50 student pass here and get ready to shift your career into warp speed.

Pro Tip: We offer a range of ticket options for nonstudents (including discounts for government, military and nonprofits). Buy yours before early-bird pricing ends on November 13 at 11:59 p.m. PST. Also, current Extra Crunch subscribers receive an additional 20% discount on passes.

This is your chance to hear from the best and brightest people leading this universal expedition. You’ll meet and engage with engineers, founders, investors, executives, military and government officials.

We’re talking officials like NASA administrator Jim Bridenstine and Space Command’s General John W. Raymond. We’re talking founders like Relativity Space’s Tim Ellis and Rocket Lab’s Peter Beck. We’re talking investors like Bessemer Venture Partners’ Tess Hatch and SpaceFund’s Meagan Crawford. And that’s just the tip of the rocket, so to speak.

We’re packing the two-day event with top-notch programming. Set coordinates for the main stage for fireside chats and moderated panel discussions. TechCrunch editors ask the tough questions and dig deep on topics like launch services, orbital operations, ground station networks, broadband communications, earth observation data, manufacturing and military operations in space.

Don’t miss the breakout sessions and Q&As. Breakouts let you explore specific topics. Main stage events always generate lots of questions, and the Q&A sessions give the audience a chance to pose questions to speakers who appeared on the main stage.

Searching for a stellar internship or a job that’s out of this world? Ouch. Explore the expo area where you’ll find early-stage space startups and sponsors showcasing their tech and talent.

That brings us to networking. Remember, this virtual conference reaches thousands of people around the world. It’s prime territory for expanding your network — an essential part of startup success. You’ll have free use of CrunchMatch, our AI-powered networking platform.

It makes quick, efficient work out of finding, scheduling and meeting people. Not just any people — people who align with your startup interests. People who can help you build a business or a career. Answer a few quick questions when you register and CrunchMatch goes to work for you.

We’ll have plenty more to announce over the next two months, so stay tuned. TC Sessions: Space 2020 blasts off on December 16-17. Don’t wait, buy your $50 student pass today and boldly go!

Is your company interested in sponsoring TC Sessions: Space 2020? Click here to talk with us about available opportunities.

Powered by WPeMatico