Argentina

Auto Added by WPeMatico

Auto Added by WPeMatico

There has been significant hype around Latin America’s startup success. For good reason, too: Startups have raised $9.3 billion in just the first half of 2021, almost double the amount in all of 2020, and mega-rounds are a growing trend.

But while the industry hails the rise of the region’s ecosystem and its growing fleet of unicorns, Latin America’s startup story has a far longer past. And it’s one we should keep in mind as entrepreneurs and investors around the world forge the region’s future.

People often ask me: How are consumers different in Brazil? How does the Peruvian market behave compared to the United States? These questions don’t really see each country for its inherent value, but instead gear people up to expect the unexpected from a historically economically disadvantaged region.

In fact, the evolution of business shares far more similarities across countries than we might expect. Latin America’s market has evolved over a very long time — as long as Silicon Valley and any other hub. This region has a global outlook, spectacular universities, a diverse population and an army of entrepreneurs.

It’s important for investors outside of Latin America to get involved in fundraising at earlier stages, when founders need extra support from everyone around.

That’s why the unicorns and megadeals should come as no surprise: They’re the natural evolution of the ecosystem, of more capital generating more success after years of hard work.

As Latin America has grown, competition has grown even more intense in the United States. VCs have more money than ever, and it’s getting increasingly expensive to invest in North America. So they’re looking to diversify their investments with high-potential opportunities abroad. Big funds are now dedicating resources to exclusively targeting Latin America, from SoftBank creating a region-specific fund, to Sequoia saying it will pay more attention to the region.

These incoming investors must bring more than money to ensure that entrepreneurship continues to grow in a healthy manner, rather than set it off balance. Investors should bring a local strategy that makes them an asset to Latin America’s startup ecosystem.

Most Latin American companies reaching unicorn status and going public now were started around 2012. This is not very different from the timeline of businesses in other markets such as the United States. For instance, e-commerce giant MercadoLibre launched in Argentina around the time eBay was emerging.

What this tells us is that foreign investors would do well to keep a sharp eye on emerging opportunities beyond heavily covered markets like Brazil and Mexico. There is a huge opportunity to do what local investors did in Brazil and Mexico years ago, and play a significant role in the next chapter of countries with blossoming markets like Colombia, Peru or Uruguay.

The amount of VC capital being funneled into Latin American startups has surged since 2017, with angel investment close behind. However, much of this investment comes from local and regional investors. Every top university in Brazil has a pool of angels. Investors in the Andean region cover Peru, Chile and Colombia. If today’s ecosystem is flourishing, it’s largely because native investors are lighting the spark.

Meanwhile, U.S. investor presence at the early stages is still low and risk averse. It’s much harder for a pre-seed or seed startup to get foreign investor interest than when they’ve already reached Series A or B. Investors also tend to come in on an ad hoc basis or as outliers brought about by a mutual contact. Foreign investors are the exception, not the rule.

It’s important for investors outside of Latin America to get involved in fundraising at earlier stages, when founders need extra support from everyone around. Investors should be pursuing a long-term strategy that will bring more consistency to the local ecosystem as a whole.

Your contribution as an investor is largely about the resources you can offer. That’s especially challenging for a foreigner who has less of an understanding of the local industry and lacks a network and people on the ground.

While investors may say their your regular value offering is enough — network and U.S. customers — in truth, this won’t necessarily be of much use. Your hiring network might not be ideal for a Latin American company, and your thorough understanding of the U.S. market might not reflect developments in Latin America.

Remember that the region has a plethora of VC organizations who have worked with local startups over the course of a decade. Latin America is a very welcoming and open market, and local investors and accelerators will happily work with foreign investors, including in deal-sharing opportunities.

It’s crucial to create incentives within the ecosystem, which — like in the United States — largely means matching founders with unique opportunities. In North America, this often happens organically, because people are on the ground and actively engaged with what’s happening in the region, from networking events, to awards, and grants and partnership opportunities.

To create this in Latin America, foreign investors need to dedicate a team and money to their regional commitments. They will have to understand the local industry and be available to mentor founders with diverse perspectives.

In my experience helping EA, Pinterest and Facebook land in Latin America, we always had someone on the ground or working remotely but fully dedicated to the region. We had people focused on localizing the product, and we had research teams studying similarities and differences in user behavior. That’s how corporations land their products; it’s how VCs should land their money.

The idea is for foreign investors to strike a balance locally while creating disruptions when it helps startups look outward rather than attempting to overhaul steady, positive internal growth. That can mean encouraging companies to incorporate in the United States to make it easier for investors from anywhere to invest or preparing the company to go global. Local investors can help investors new to the region understand the balance of things that should or shouldn’t be disrupted.

Don’t be surprised when Latin America’s apparent “boom” starts happening in other emerging markets like Africa and Asia. This isn’t about a secret hack coming in from the outside. It’s just about creating the right environment for local talent to flourish and ensuring it maintains healthy growth.

Powered by WPeMatico

Kavak, the Mexican startup that’s disrupted the used car market in Mexico and Argentina, today announced its Series D of $485 million, which now values the company at $4 billion. This round more than triples their previous valuation of $1.15 billion, which established them as a unicorn just a couple of months ago in October of 2020. Kavak is now one of the top five highest-valued startups in Latin America.

The round was led by D1 Capital Partners, Founders Fund, Ribbit and BOND, and brings Kavak’s total capital raised to date to more than $900 million. Kavak recently soft-launched in Brazil, and this new round of funding will be used to build out the Brazilian market and beyond, said Carlos García Ottati, Kavak’s CEO and co-founder. The company plans to do a full launch in Brazil in the next 60 days, García said, and we can expect to see Kavak in markets outside Latin America in the next 24 months, he added.

“We were built to solve emerging market problems,” García said.

Kavak, which was founded in 2016, is an online marketplace that aims to bring transparency, security and access to financing to the used car market. The company also offers its own financing through its fintech arm, Kavak Capital, and counts more than 2,500 employees and 20 logistics and reconditioning hubs in Mexico and Argentina.

“In Latin America, 90% of the [used car] transactions are informal, which leads to a 40% fraud rate,” said García, who experienced these challenges firsthand when he moved to Mexico from Colombia a couple of years ago and bought a used car.

“My budget allowed me to buy a used car, but there was no infrastructure around it. It took me six months to buy the car, and then the car had legal and mechanical issues and I lost most of my money,” he said. Kavak buys cars from individuals, refurbishes them and offers warranties to buyers.

“Instead of buying a new car, they can buy a better car that still has all the warranties. It’s a really aspirational process,” said García. The company, which really amounts to four companies in one given its areas of focus, was built to be comprehensive by design in order to meet the various gaps in the market, García said.

“When you’re building a business here [Latin America], you need to build several businesses because so many things are broken,” he said. That’s why the financing option, for example, has been a key to their success, according to García.

Financing has traditionally been hard to come by in Brazil, and as García said, the used car market lacks infrastructure there, too. That being said, Brazil is Latin America’s fintech hub, and the space has made leaps and bounds over the last 7-10 years with companies such as Nubank, PagSeguro, Creditas, PicPay, and others leading the way. As a result, credit cards and loans are more widely available today in the region, offering competition for Kavak Capital. While Kavak has localized some of its product for the Brazilian market — namely building out a Portuguese language version of the app and website — García said the markets are very similar.

“In Brazil, you still have the same problems that you have in Mexico, but Brazil is a little more developed, especially in fintech, which is light years ahead of Mexico,” he said.

With the Brazilian product heading to the races, García said they already have plans for other regions, though he declined to name them.

“80% of people in emerging markets don’t have access to a car,” García said of the global market size. “We want to go into big markets where customers are facing similar problems and where Kavak can really change their lives,” he added.

Powered by WPeMatico

Lana, a new startup based in Madrid, is looking to be the next big thing in Latin American fintech.

Founded by serial entrepreneur Pablo Muniz, whose last business was backed by one of Spain’s largest financial services institutions, BBVA, Lana is looking to be the all-in-one financial services provider for Latin America’s gig economy workers.

Muniz’s last company, Denizen, was designed to provide expats in foreign and domestic markets with the financial services they would need as they began their new lives in a different country. While the target customer for Lana may not be the same middle to upper-middle-class international traveler that he had previously hoped to serve, the challenges gig economy workers face in Latin America are much the same.

Muniz actually had two revelations from his work at Denizen. The first — he would never try to launch a fintech company in conjunction with a big bank. And the second was that fintechs or neobanks that focus on a very niche segment will be successful — so long as they can find the right niche.

The biggest niche that Muniz saw that was underserved was actually in the gig economy space in Latin America. “I knew several people who worked at gig economy companies and I knew that their businesses were booming and the industry was growing,” he said. “[But] I was concerned about the inequalities.”

Workers in gig economy marketplaces in Latin America often don’t have bank accounts and are paid through the apps on which they list their services in siloed wallets that are exclusive to that particular app. What Lana is hoping to do is become the wallet of wallets for all of the different companies on which laborers list their services. Frequently, drivers will work for Uber or Cabify and deliver food for Rappi. Those workers have wallets for each service.

(Photo by Cris Faga/Pacific Press/LightRocket via Getty Images)

Lana wants to unify all of those disparate wallets into a single account that would operate like a payment account. These accounts can be opened at local merchant shops and, once opened, workers will have access to a debit card that they can use at other locations.

The Lana service also has a bill pay feature that it’s rolling out to users, in the first evolution of the product into a marketplace for financial services that would appeal to gig workers, Muniz said.

“We want to become that account in which they receive funds,” he said. “We are still iterating the value proposition to gig economy companies.”

Working with companies like Cabify, and other, undisclosed companies, Lana has plans to roll out in Mexico, Chile, Peru and, eventually, Colombia and Argentina.

Eventually, Lana hopes to move beyond basic banking services like deposits and payments and into credit services. Already hundreds of customers are using the company’s service through the distribution partnership with Cabify, which ran the initial pilot to determine the viability of the company’s offering.

“The idea of creating Lana was initially tested as an internal project at Cabify,” Muniz wrote in an email. “Soon Cabify and some potential investors saw that Lana could have a greater impact as an independent company, being able to serve gig economy workers from any industry and decided to start over a new entrepreneurial project.”

Through those connections with Cabify, Lana was able to bring in other investors like the Silicon Valley-based investment firm Base 10.

“One of the things we’ve been interested in is in inclusion generally and in fintech specifically,” said Adeyemi Ajao, the firm’s co-founder. “We had gotten very close to investing in a couple of fintech companies in Latin America and that is because the opportunity is huge. There are several million people going from unbanked to banked in the region.”

Along with a few other investors, Base 10 put in $12.5 million to finance Lana as it looks to expand. It’s a market that has few real competitors. Nubank, Latin America’s biggest fintech company, is offering credit services across the continent, but most of their end users already have an established financial history.

“Most of their end users are not unbanked,” said Ajao. “With Lana it is truly gig workers… They can start by being a wallet of wallets and then give customers products that help them finance their cars or their scooters.”

The ultimate idea is to get workers paid faster and provide a window into their financial history that can give them more opportunities at other gig economy companies, said Ajao. “The vision would be that someone can plug in their financial information for services. If they’re working for Rappi and have never been an Uber driver and they want to be an Uber driver, Lana can use their financial history with Rappi to offer a loan on a car,” he said.

That financial history is completely inaccessible to a traditional bank, and those established financial services don’t care about the history built in wallets that they can’t control or track. “Today if you’ve been a gig worker and you go to a bank, that’s worth nothing,” said Ajao.

Powered by WPeMatico

The Not Company, Latin America’s leading contender in the plant-based meat and dairy substitute market, is about to close on an $85 million round of funding that would value it at $250 million, according to sources familiar with the company’s plans.

The latest round of funding comes on the heels of a series of successes for the Santiago-based business. In the two years since NotCo launched on the global stage, the company has expanded beyond its mayonnaise product into milk, ice cream and hamburgers. Other products, including a chicken meat substitute, are also on the product roadmap, according to people familiar with the company.

NotCo is already selling several products in Chile, Argentina and Latin America’s largest market — Brazil — and has signed a blockbuster deal with Burger King to be the chain’s supplier of plant-based burgers. It’s in this Burger King deal that NotCo’s approach to protein formulation is paying dividends, sources said. The company is responsible for selling 48 sandwiches per store per day in the locations where it’s supplying its products, according to one person familiar with the data. That figure outperforms Impossible Foods per-store sales, the person said.

NotCo is also now selling its burgers in grocery stores in Argentina and Chile. And while the company is not break-even yet, sources said that by December 2021 it could be — or potentially even cash flow positive.

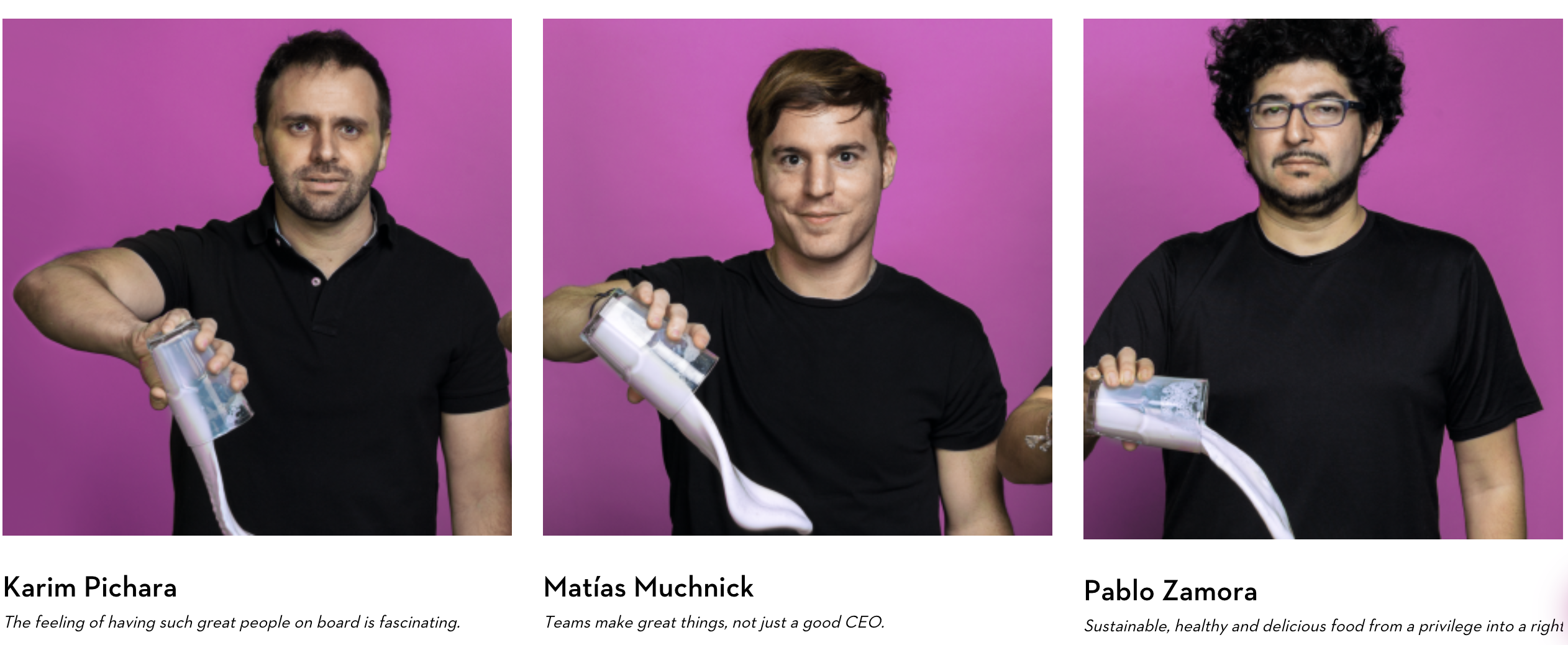

NotCo co-founders Karim Pichara, Matias Muchnick and Pablo Zamora. Image Credit: The Not Company

With the growth both in sales and its diversification into new products, it’s little wonder that investors have taken note.

Sources said that the consumer brand-focused private equity firm L Catterton Partners and the Biz Stone-backed Future Positive were likely investors in the new financing round for the company. Previous investors in NotCo include Bezos Expeditions, the personal investment firm of Amazon founder Jeff Bezos; the London-based CPG investment firm, The Craftory; IndieBio; and SOS Ventures.

Alternatives to animal products are a huge (and still growing) category for venture investors. Earlier this month Perfect Day closed on a second tranche of $160 million for that company’s latest round of financing, bringing that company’s total capital raised to $361.5 million, according to Crunchbase. Perfect Day then turned around and launched a consumer food business called the Urgent Company.

These recent rounds confirm our reporting in Extra Crunch about where investors are focusing their time as they try to create a more sustainable future for the food industry. Read more about the path they’re charting.

Meanwhile, large food chains continue to experiment with plant-based menu items and push even further afield into cell-based meat using cultures from animals. KFC recently announced that it would be expanding its experiment with Beyond Meat’s chicken substitute in the U.S. — and would also be experimenting with cultured meat in Moscow.

Behind all of this activity is an acknowledgement that consumer tastes are changing, interest in plant-based diets are growing, and animal agriculture is having profound effects on the world’s climate.

As the website ClimateNexus notes, animal agriculture is the second-largest contributor to human-made greenhouse gas emissions after fossil fuels. It’s also a leading cause of deforestation, water and air pollution and biodiversity loss.

There are 70 billion animals raised annually for human consumption, which occupy one-third of the planet’s arable and habitable land surface, and consume 16% of the world’s freshwater supply. Reducing meat consumption in the world’s diet could have huge implications for reducing greenhouse gas emissions. If Americans were to replace beef with plant-based substitutes, some studies suggest it would reduce emissions by 1,911 pounds of carbon dioxide.

Powered by WPeMatico

We’re excited to announce that Extra Crunch is now available to readers in Argentina, Brazil and Mexico. That adds to our existing support in the U.S., Canada, the U.K., and select European countries.

You can sign for Extra Crunch here.

Latin America has always caught the eye of big tech. For companies like Facebook, Amazon and Uber, Latin America has represented a massive growth opportunity. But it’s not just big tech that’s investing in Latin America. The startup scene is booming. According to Crunchbase, VCs invested billions into Latin America in 2018 and 2019.

In 2018, the TechCrunch team took a trip to São Paulo, Brazil to host Startup Battlefield Latin America. We knew about the hot startup scene and massive investments, and wanted to meet the founders fueling the fire in person.

The excitement, wit, creativity and energy of the entrepreneurs in Latin America was impressive. We were dazzled by the pitches from budding startup teams, and we were enlightened by the investors sharing their wealth of knowledge about the ecosystem. What we saw in person helped us tie the funding to the faces of the teams building the future. The entrepreneurial mentality of Silicon Valley doesn’t have borders; it’s alive and well across Latin America.

We wanted to bring Extra Crunch to Latin America to help support the startups and investors in this market because community has always been our top priority. We hope that Extra Crunch’s deep analysis and company-building resources will help the Latin America tech community grow even stronger than it is today.

We’ve been polling our audience about expanded country support for over a year now, and Argentina, Brazil and Mexico have always been near the top of the list. Now, we’re delivering on the promise to bring Extra Crunch to everyone who asked for it.

We’re optimistic that Extra Crunch will be a big hit in Latin America, and we hope entrepreneurs and investors in the region who have not yet heard of TechCrunch will give it a try.

You can sign for Extra Crunch here.

Extra Crunch is a membership program from TechCrunch that features research and reporting, reader utilities and savings on software services and events. We deliver more than 100 exclusive articles per month, with a focus on startup teams and investors.

Our weekly Extra Crunch investor surveys will help members find out where startup investors plan to write their next checks. Extra Crunch subscribers will be able to build a company better with how-tos and interviews from experts on fundraising, growth, monetization and other key work topics. Readers can also learn about the best startups through our IPO analysis, late-stage deep dives and other exclusive reporting delivered daily.

Here’s a taste of the articles you can expect to see in Extra Crunch:

Beyond articles, Extra Crunch also features a series of reader utilities and discounts to help save time and money. This includes an exclusive newsletter, no banner ads on TechCrunch.com, Rapid Read mode, List Builder tool and more. Committing to an annual or two-year Extra Crunch membership will unlock discounts on TechCrunch events and access to Partner Perks. Our Partner Perks can help you save on services like AWS, Brex, Canva, DocSend, Zendesk and more.

Thanks to all of our readers who voted on where to expand support for Extra Crunch, and thanks to all who participated in the Extra Crunch beta in Latin America. If you haven’t voted and you want to see Extra Crunch in your local country, let us know here. We’re actively working on expanding support to more countries, and input from readers is greatly appreciated.

You can sign up or learn more about Extra Crunch here.

Powered by WPeMatico

Andreessen Horowitz <3 Latin American startups.

Latin America is the only region outside of the U.S. where the venture firm is routinely investing capital, and it just made another commitment, doubling down on its early-stage support for the point-of-sale lending startup ADDI.

ADDI picked up $12.5 million in new financing in April of this year as the company looks to expand its lending services online.

For an American audience, the closest corollary to what ADDI is up to is likely Affirm, the point-of-sale lender that’s raised a ton of cash and come in for some (valid) criticism for its basic business model.

Like Affirm, ADDI lets its borrowers apply for credit at the moment of purchase. The company likens its service to the layaway and credit plans that already exist in Colombia — but involve pretty onerous requirements to use. Company co-founder Santiago Suarez and Andreessen Horowitz general partner Angela Strange both commented on how, in some cases, Colombian shoppers have to have three people vouch for a borrower before a store will issue credit or agree to a layaway plan.

The difference between an ADDI loan — or any loan — and layaway is that an installment payment plan doesn’t charge interest (and even with the fees that installment plans do charge, they are often still cheaper than taking out a loan).

But financial products are coming for consumers in Latin America whether those buyers like it or not — and for the most part, it seems they do like it.

Historically, only the wealthiest clientele in Latin America received anything resembling the kinds of financial products that are more widely available in the United States, according to Strange. And the investment in ADDI is just part of her firm’s thesis in trying to make more services more broadly available in a region where a technological transformation is creating unprecedented opportunities for challengers.

That assessment is what drew Santiago Suarez back to Latin America only two years ago. A former executive at Lending Club who previously had worked as the head of New Product Development and Emerging Services at J.P. Morgan, Suarez saw the tremendous growth happening in Latin America and returned to Colombia to see if he could bring some much needed services to his home country.

Suarez partnered with his childhood friend, Elmer Ortega, who was working as the chief technology officer of the local hedge fund where he had previously been employed as a derivatives trader before learning how to code.

Together, the two men, who had known each other since they were five years old, set out to transform how credit was offered in retail shops. It’s an industry that Suarez had known well since his parents had owned stores.

“In the U.S. there are all of these gaps that fintech companies are filling,” says Suarez. “But the gaps in Latin America are bigger.”

Suarez and Ortega incorporated the company in September 2018, around the same time they raised $2.3 million from the regional investment firm, Monashees, Andreessen and Village Global . They then raised another $1.5 million in an internal round of financing before closing the most recent funding.

The company offers loans at annual percentage rates ranging from 19.99% to 28.90%. The company started with a digital solution for brick and mortar retailers because 90% of retail in Colombia still happens offline.

Although it’s in its early days, the company has already originated 10,000 borrowers and typically loans out roughly $500 since it launched on February 22, according to Suarez. He declined to comment on the company’s default rate on loans.

Now with 40 employees on staff, the company is looking to bring its lending tool to more e-commerce and physical retailers, according to Suarez. And despite the threat of cyclical political turmoil, Suarez says there’s no better time to be investing in Colombia.

“It’s the most stable country outside of Chile… Way more stable than Brazil, way more stable than Argentina and way more stable than Mexico,” Suarez says. “What we’re looking at is more than cyclical instability… those things go beyond that. Nubank was able to build a multibillion business in the worst political and economic crisis in Brazil’s history. I think Colombia is an incredibly attractive space with a deep talent pool.”

Powered by WPeMatico

Rappi represents a new era for Latin American technology startups.

Based in Bogotá, Colombia, the on-demand delivery startup has taken the region by storm, attracting a record amount of venture capital funding in mere months. Today marks the beginning of a new round of explosive growth as SoftBank, the Japanese telecom giant and prolific Silicon Valley tech investor, has confirmed a $1 billion investment in the business.

The king-sized financing comes two months after SoftBank announced its Innovation Fund, a new pool of capital committed to spending billions on the growing tech ecosystem in Central and South America.

VC funding in Latin America catapulted to new heights in 2018. Startups located across Argentina, Brazil, Chile, Colombia and more have secured nearly $2.5 billion since the beginning of 2018, according to PitchBook, up from less than $1 billion invested in 2017.

SoftBank plans to transfer the Rappi investment to the Innovation Fund “upon the fund’s establishment,” according to a press release. For now, the SoftBank Group and affiliated Vision Fund will each invest $500 million in the company. Jeffrey Housenbold, a managing director at SoftBank responsible for investments in Brandless, Opendoor and DoorDash, will join Rappi’s board of directors.

“SoftBank’s vision of accelerating the technology revolution deeply resonated with our mission of improving how people live through digital payments and a super-app for everything consumers need,” Rappi co-founder Sebastian Mejia said in a statement. “We will continue to focus on building innovations for couriers, restaurants, retailers and start-ups that translate into new sources of growth.”

Mejia, Simón Borrero and Felipe Villamarin launched Rappi in 2015, graduating from the Y Combinator startup accelerator the following year. It didn’t take long for the business to capture the attention of American VCs, including the likes of Andreessen Horowitz, DST Global and Sequoia Capital .

The latest round, the largest ever for a Latin American tech startup, brings Rappi’s total raised to date to a whopping $1.2 billion. The company was valued at more than $1 billion last year with a $200 million financing.

Rappi is among few venture-backed “unicorns” based in Latin America. São Paulo-based Nubank, a fast-growing fintech startup, garnered a $4 billion valuation last year with a $180 million investment.

Rappi didn’t immediately respond to a request for comment.

Powered by WPeMatico

Madrid-based micromobility startup Movo has closed a €20 million (~$22.5M) Series A funding round to accelerate international expansion.

The 2017-founded Spanish startup targets cities in its home market and in markets across LatAm, offering last-mile mobility via rentable electric scooters (e-mopeds and e-scooters) plotted on an app map. It’s a subsidiary of local ride-hailing firm Cabify, which provided the seed funding for the startup.

Movo’s Series A round is led by two new investors: Insurance firm Mutua Madrileña, doubtless spying strategic investment potential in helping diversify its business by growing the market for humans to scoot around cities on two wheels — and VC fund Seaya Ventures, an early investor in Cabify.

Both Mutua Madrileña and Seaya Ventures are now taking a seat on Movo’s board.

Commenting on the Series A in a statement, Javier Mira, general director of Mutua Madrileña, said: “The equity investment in Movo reflects Mutua Madrileña’s aspiration to respond to the new mobility needs that are emerging, and to the economic and social changes that are occurring and that are transforming our life habits.”

Movo currently operates in six cities across five countries — Spain, México, Colombia, Perú and Chile.

It first launched an e-moped service in Madrid a year ago, according to a spokeswoman, and has since expanded domestic operations to the southern Spanish coastal city of Malaga, as well as riding into Latin America.

The new funding is mostly pegged for further international expansion, with a plan to expand into new markets in LatAm, including Argentina, Brazil and Uruguay. Movo is targeting operating in a total of 10 countries by the end of 2019.

The Series A will also be used to grow its vehicle fleet in existing markets, it said.

“We are very excited to be able to offer a solution to the problems of mobility in cities, particularly for short distances in areas with high population density,” said CEO Pedro Rivas in a statement. “We are committed to working together with governments to complement mass public transport with these new micromobility alternatives, so that people can get around in a more sustainable and efficient way.”

Commenting on its investment in the Cabify subsidiary, Seaya Ventures’ Beatriz Gonzalez, founder and managing partner, said the fund is “committed to the evolution of mobility towards sustainable alternatives in the world’s major cities.”

“We want to be part of the transport revolution by promoting projects like Cabify and, of course, Movo,” she said in a statement, which seeks to paint micromobility as a solution for urban congestion and poor air quality. “We are motivated to continue to promote companies with which we share this sense of responsibility towards the development and improvement of people’s quality of life.”

Powered by WPeMatico

One of the stranger things that Y Combinator has supported — among the many more interesting things they’ve started to back like prosthetic legs, macrobiotic research and Uber-for-marijuana startups — is a non-profit that built an entire political party in Buenos Aires, Argentina. DemocracyOS is a software platform that allows regular voters to debate and forward policy ideas.… Read More

One of the stranger things that Y Combinator has supported — among the many more interesting things they’ve started to back like prosthetic legs, macrobiotic research and Uber-for-marijuana startups — is a non-profit that built an entire political party in Buenos Aires, Argentina. DemocracyOS is a software platform that allows regular voters to debate and forward policy ideas.… Read More

Powered by WPeMatico