apple pay

Auto Added by WPeMatico

Auto Added by WPeMatico

Would you pay with a “Google Card?” TechCrunch has obtained imagery that shows Google is developing its own physical and virtual debit cards. The Google card and associated checking account will allow users to buy things with a card, mobile phone or online. It connects to a Google app with new features that let users easily monitor purchases, check their balance or lock their account. The card will be co-branded with different bank partners, including CITI and Stanford Federal Credit Union.

A source provided TechCrunch with the images seen here, as well as proof that they came from Google. Another source confirmed that Google has recently worked on a payments card that its team hopes will become the foundation of its Google Pay app — and help it rival Apple Pay and the Apple Card. Currently, Google Pay only allows online and peer-to-peer payments by connecting a traditionally issued payment card. A “Google Pay Card” would vastly expand the app’s use cases, and Google’s potential as a fintech giant.

By building a smart debit card, Google has the opportunity to unlock new streams of revenue and data. It could potentially charge interchange fees on purchases made with the card or other checking account fees, and then split them with its banking partners. Depending on its privacy decisions, Google could use transaction data on what people buy to improve ad campaign measurement or even targeting. Brands might be willing to buy more Google ads if the tech giant can prove they drive a sales lift.

The long-term implications are even greater. While once the industry joke was that every app eventually becomes a messaging app, more recently it’s been that every tech company eventually becomes a financial services company. A smart debit card and checking accounts could pave the way for Google offering banking, stock brokerage, financial advice or robo-advising, accounting, insurance or lending.

Image Credits: jossnatu / Getty Images

Google’s vast access to data could allow it to more accurately manage risk than traditional financial institutions. Its deep connection to consumers via apps, ads, search and the Android operating system gives it ample ways to promote and integrate financial services. With the COVID-19 downturn taking shape, high-margin finance products could help Google develop efficient revenue opportunities and build its share price back up.

When TechCrunch asked Google for confirmation, it did not dispute our findings or assertions. The company offered us a statement it provided reporters following a November story, wherein Google told The Wall Street Journal’s Peter Rudegeair and Liz Hoffman it was experimenting in the checking account space. TechCrunch is the first to report Google’s debit card plans:

We’re exploring how we can partner with banks and credit unions in the US to offer smart checking accounts through Google Pay, helping their customers benefit from useful insights and budgeting tools, while keeping their money in an FDIC or NCUA-insured account. Our lead partners today are Citi and Stanford Federal Credit Union, and we look forward to sharing more details in the coming months.

For now, Google’s strategy is to let partnered banks and credit unions provide the underlying financial infrastructure and navigate regulation while it builds smarter interfaces and user experiences. It’s forseeable that one day Google might cut out the banks and take all the spoils for itself. Google launched a Wallet debit card in 2013 as an extension of its old payment app Google Wallet, but shut the card down in 2016. Given Google’s penchant for renaming or shutting down then reviving products, building a new debit card feels on-brand.

With people around the world suddenly more concerned about their finances amidst the coronavirus economic disaster, a debit card with more transparency and controls could be appealing.

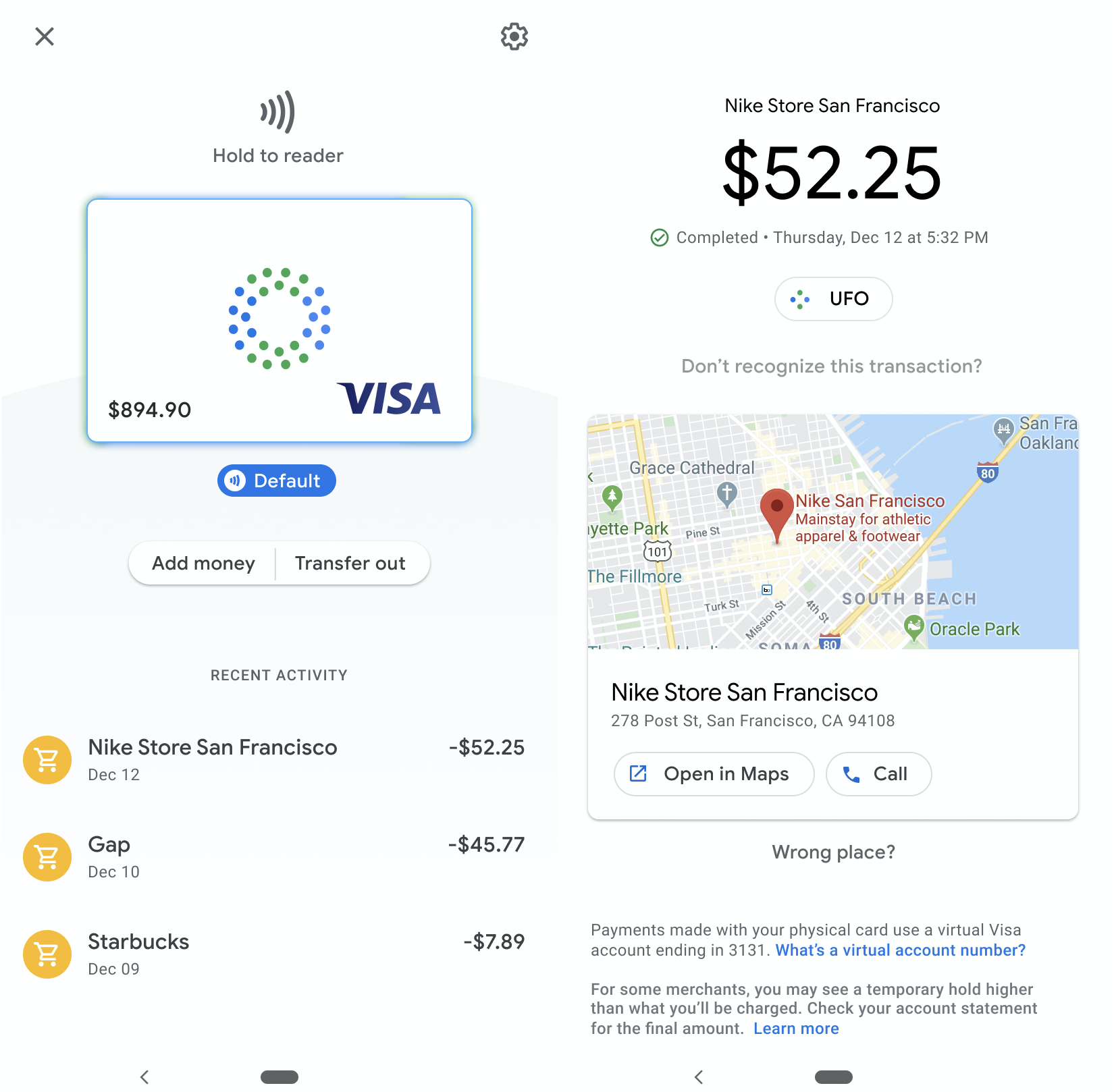

Traditional banking products can be clunky, often requiring phone communication with customer service or sifting through cluttered websites to address security issues. Google hopes to make financial management as intuitive as its email and mapping apps. The card and app designs shown here are not final, and it’s unclear when Google’s debit card may launch. But let’s take a look at what these internal Google materials reveal about its ambitions for its payment instrument.

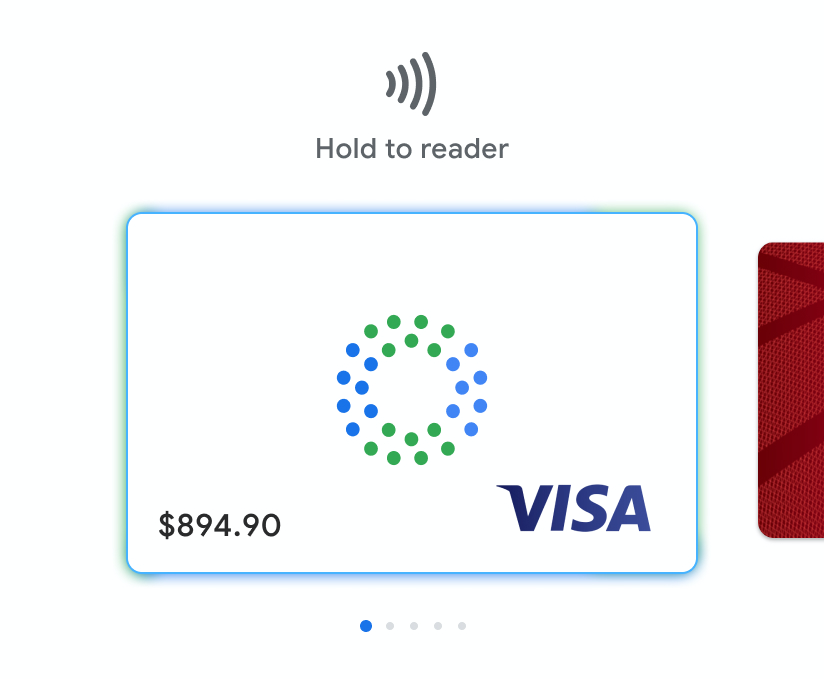

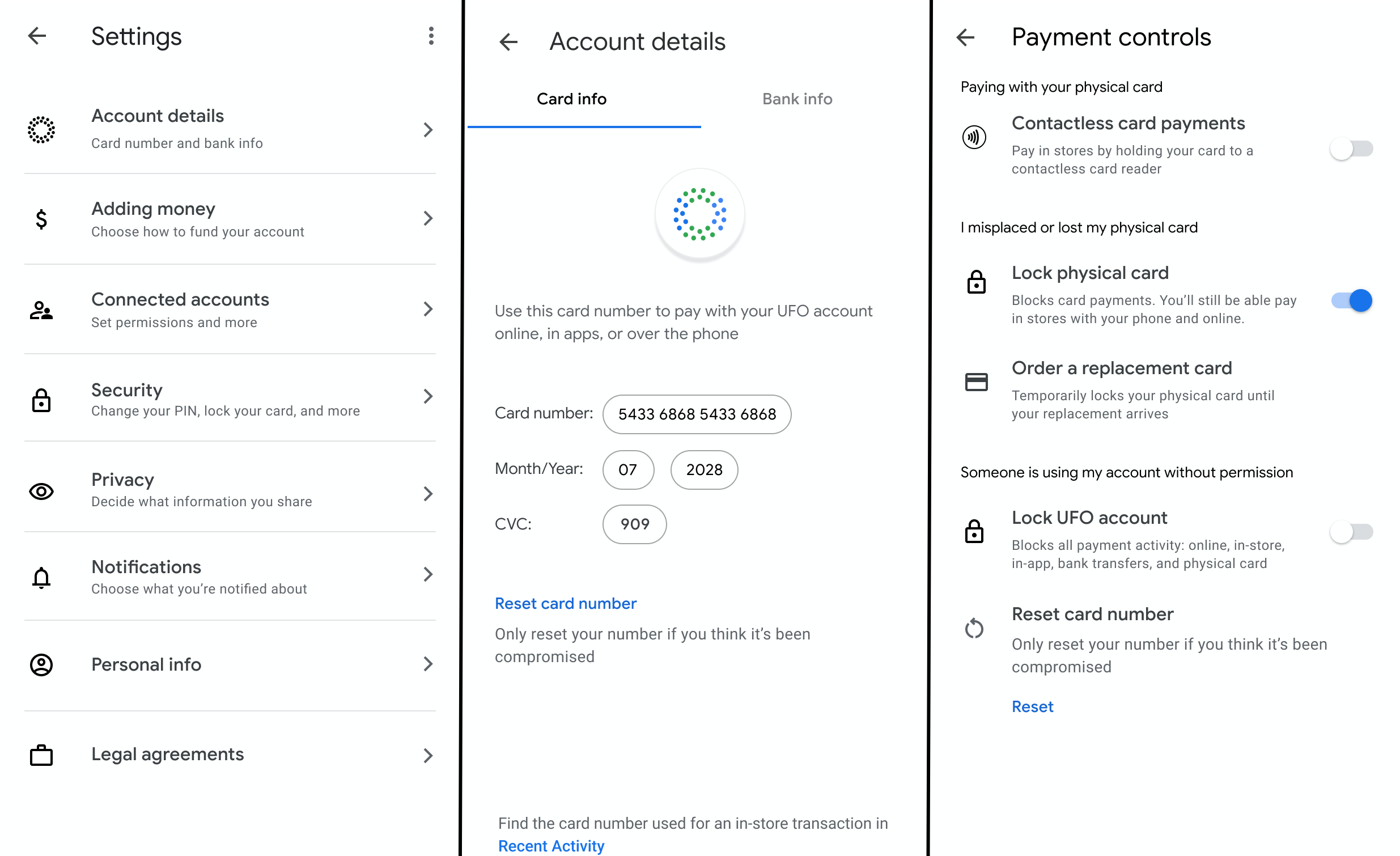

The Google debit card will come co-branded with the Google name and its partnered bank, though the exact name of the product is still unknown. In the designs, it’s a chip card on the Visa network, though Google could potentially support other networks like Mastercard. Users are able to add money or transfer funds out of their account from the connected Google app, which is likely to be Google Pay, and use a fingerprint and PIN for account security.

Once connected to their bank or credit union account, users could pay for purchases in retail stores with a physical Google debit card, including with contactless payments, by just holding it up to a card reader. A virtual version of the card that lives on a user’s phone can also be used for Bluetooth mobile payments. Meanwhile, a virtual card number can be used for online or in-app payments.

Users are shown a list of recent transactions, with each including the merchant name, date and price. They can dig into each transaction to see the location on a map, get directions or call the store. If users don’t recognize a transaction, it’s easy to protect themselves with the card’s vast security options.

If a customer suspects foul play because they lost their card, they can lock it and optionally order a replacement while still being able to pay with their phone or online, thanks to Google’s virtual card number system that’s different than the one on their physical card. If instead they suspect their virtual card number was stolen by a hacker, they can quickly reset it. And if they believe someone has gained unauthorized access to their account, they can lock it entirely to block all types of payments and transfers.

The settings reveal options for notifications and privacy controls to “decide what information you share,” though we don’t have imagery of what’s contained in those menus. It’s unclear how much power Google will give customers to limit the company or merchant’s data access. Google’s decisions there could impact how transaction data might fuel its other businesses.

Google is a relative late-comer to offering its own card. Apple launched its Apple Card in August, offering a slickly designed titanium Mastercard credit card backed by Goldman Sachs. It charges minimal customer fees, comes with a virtual card for use through Apple Pay and generates interest.

Apple Card

Apple does collect interchange fees from merchants, though, which Google could similarly gather to earn revenue. Last month, Apple changed the Card’s privacy settings to share more data with Goldman Sachs that might also help the two provide additional financial services. Apple Pay now accounts for 5% of global card transactions, and is forecast to hit 10% by 2024, according to Bernstein research. The underlines the gigantic market Google is gunning for here.

The stock brokerage and robo-advisor apps have also joined the payments race. Wealthfront launched cash accounts and debit cards last February, bringing in $1 billion in assets in two months and doubling the company’s total holdings to $20 billion by September. Betterment launched its checking product in October 2019 with a Visa debit card, but it doesn’t generate interest.

Robinhood botched the December 2018 launch of its checking accounts due to ineligible insurance, but relaunched in October 2019 with debit card withdrawls from 75,000 ATMs and a solid interest rate. It’s unclear how Google’s card will work with ATMs or how its checking accounts will generate interest.

Robinhood’s debit cards

The appeal for Google and the rest is clear. It seems whenever companies help move people’s money around, some of it inevitably “falls off the truck” and lands in their pockets. Financial services are typically low-overhead ways to generate revenue. That could be especially enticing, as Google has found many of its side hustle “other bets” to be unsustainable. It’s moved to prune some of these tertiary projects, such as its Makani wind energy kites.

Google may never find businesses as lucrative as its core in search and advertising, but it has the advantages to become a serious player in fintech. Its vast sums of cash, deep bench of engineering talent, experience building complex utilities, numerous consumer touch points and near-bottomless well of data could give it an edge over stodgier old banks and scrappier startups. And while Facebook slams into regulatory scrutiny and is forced to scale back its Libra cryptocurrency, Google’s more familiar approach via debit cards could pay off.

Powered by WPeMatico

Ahead of the upcoming school year, Apple this morning announced it’s bringing contactless student IDs in Apple Wallet to several more U.S. universities. The expansion will allow more than 100,000 additional college students to carry their student ID on their iPhone or Apple Watch, where it can be used for a variety of tasks, including paying for their meals and snacks and entry into buildings, like the student’s dorm and other campus facilities.

The expanded list of universities includes: Clemson University, Georgetown University, University of Tennessee, University of Kentucky, University of San Francisco, University of Vermont, Arkansas State University, South Dakota State University, Norfolk State University, Louisburg College, University of North Alabama and Chowan University.

These join the previously supported schools: Duke University, University of Oklahoma, University of Alabama, Temple University, Johns Hopkins University, Marshall University and Mercer University.

Apple first announced its plans for contactless student IDs at WWDC 2018, then rolled out to its debut schools last October.

The contactless IDs not only serve as a means of student identification, but also work as a payment mechanism for on-campus transactions — like meals at the cafeteria or textbooks and supplies at the college’s bookstore, for example. Contactless entry into buildings is also now common on college campuses, and these digital IDs can work to open doors, too, as an alternative to swiping an entry card.

Support for college student IDs is only one way that Apple is trying to replace the physical wallet. The company also supports the ability to add your debit and credit cards, transit and loyalty cards, tickets and even paper money through Apple Pay Cash. And now it’s launching its own credit card, too, which rewards you with cashback for shopping Apple and using Apple Pay.

“We’re happy to add to the growing number of schools that are making getting around campus easier than ever with iPhone and Apple Watch,” said Jennifer Bailey, Apple’s vice president of Internet Services, in a statement about the expansion. “We know students love this feature. Our university partners tell us that since launch, students across the country have purchased 1.25 million meals and opened more than 4 million doors across campuses by just tapping their iPhone and Apple Watch.”

Related to this launch, Apple says it’s also adding support for CBORD, Allegion and HID — solution providers for campus credentials and mobile access. With these technologies on board, Apple will be able to reach other schools integrated with these systems in the future.

Powered by WPeMatico

Apple has finally listened to its small, but slowly growing user base in India. The iPhone-maker today announced a range of features in iOS 13 that are designed to appease users in the world’s second largest smartphone market.

First up, the company says its Siri voice assistant now offers all new and “more natural” Indian English male and female voices. It has also introduced a bilingual keyboard, featuring support for Hindi and English languages. The keyboard offers typing predictions in Devanagari Hindi that can suggest the next word as a user types and it learns from their typing over time.

Additionally, the keyboard in iOS 13 supports all of 22 Indian languages, with the inclusion of 15 new Indian language keyboards: Assamese, Bodo, Dogri, Kashmiri (Devanagari, Arabic), Konkani (Devanagari), Manipuri (Bangla, Meetei Mayek), Maithili, Nepali, Sanskrit, Santali (Devanagari, Ol Chiki), and Sindhi (Devanagari, Arabic).

The addition of these features comes as Apple cautiously grows more serious about India, where it holds about just 1% of the smartphone market share, according to research firm Counterpoint. Even as smartphone shipment is declining in much of the world, India has emerged as the fastest growing market for handsets in recent years. According to Counterpoint, more than 145 million smartphones shipped in India last year, up 10% year-over-year.

But users in India have long complained about Apple services not being fully optimized for local conditions. Siri, for instance, has so far offered limited functionalities in India, and many Apple services such as Apple Pay and Apple News are yet to launch in the nation.

The upcoming version of iOS, which will ship to a range of iPhone handsets later this year, also includes four new system fonts in Indian languages: Gurmukhi, Kannada, Odia, and Gujarati. These will “help deliver greater clarity and ease when reading in apps like Safari, typing in Messages and Mail, or swiping through Contacts,” the company said in a statement.

Additionally, there are 30 new document fonts for Indian languages Hindi, Marathi, Nepali, Sanskrit, Bengali, Assamese, Tamil, Telugu, Gujarati, Kannada, Gurmukhi, Malayalam, Odia, and Urdu.

Apple says iOS 13 will also enable improved video downloading option for patchy networks. It says users in India can now set an optimized time of the day in video streaming apps such as Hotstar and Netflix for downloading videos. Consumption of video apps is increasingly skyrocketing in India. Just last week, Alibaba said it was investing $100 million in its short video app called Vmate in the nation.

In recent months, Apple has also improved Apple Maps in India. Earlier this year, Apple Maps added support for turn-by-turn navigation, and enabled users to book a cab — from Ola or Uber — directly from within the maps app. The company has also been aggressively hiring people to expand its maps and other software teams in the country, according to job postings on the its site.

Improvements to software aside, Apple has also been working to reduce the cost of iPhones in India, the single major factor for their poor sales in the country. Two years ago, Apple started to assemble the iPhone 7 handset in India. It plans to ramp up its local production in the coming weeks, a person familiar with the matter told TechCrunch.

As part of local government’s ‘Make in India’ program, phone vendors that assemble phones in the country are offered tax and other benefits. Ravi Shankar Prasad, an Indian minister who oversees law and justice, telecom, and electronics and IT departments, said at a press conference earlier today (local time) that Bharatiya Janata Party, the ruling party which was reelected last month, will work on expanding Make in India program as one of its top priorities.

Powered by WPeMatico

A little more retail momentum for Apple Pay: Apple has announced another clutch of U.S. retailers will soon support its eponymous mobile payment tech — most notably discount retailer Target.

Apple Pay is rolling out to Target stores now, according to Apple, which says it will be available in all 1,850 of its U.S. retail locations “in the coming weeks.”

Also signing up to Apple Pay are fast food chains Taco Bell and Jack in the Box; Speedway convenience stores; and Hy-Vee supermarkets in the Midwest.

“With the addition of these national retailers, 74 of the top 100 merchants in the US and 65 per cent of all retail locations across the country will support Apple Pay,” notes Apple in a press release.

Speedway customers can use Apple Pay at all of its approximately 3,000 locations across the Midwest, East Coast and Southeast from today, according to Apple, as well as at Hy-Vee stores’ more than 245 outlets in the Midwest.

It says the payment tech is also rolling out to more than 7,000 Taco Bell and 2,200 Jack in the Box locations “in the next few months.”

Back in the summer Apple announced it had signed up longtime holdout CVS, with the pharmacy introducing Apple Pay across its ~8,400 standalone locations last year.

Also signing up then: 7-Eleven, which Apple says has now launched support for Apple Pay in 95 percent of its U.S. convenience stores in 2018.

Last year retail giant Costco also completed the rollout of Apple Pay to its more than 500 U.S. warehouses.

While, in December, Apple Pay also finally launched in Germany — where Apple slated it would be accepted at a range of “supermarkets, boutiques, restaurants and hotels and many other places” at launch, albeit “cash only” remains a common demand from the country’s small businesses.

Update: In a blog post about the Apple Pay launch, Target confirmed that users of its Target REDcard credit or debit cards cannot use the store payment card with Apple Pay.

The retail giant also said it will soon support contactless mobile payment technologies on the Android smartphone platform, naming Google Pay and Samsung Pay specifically, as well as supporting contactless payment cards from Mastercard, Visa, American Express and Discover.

“Offering guests more ways to conveniently and quickly pay is just another way we’re making it easier than ever to shop Target,” said Target’s chief information officer, Mike McNamara, in a statement.

Powered by WPeMatico

Apple’s mobile payment technology has finally launched in Germany, some four years after it debuted in the U.S.

On its newly launched Apple Pay website for Germany, Apple lists partner banks and credit card companies at launch, with customers from the likes of Deutsche Bank, O2 Banking, N26, Comdirect, HypoVerensbank, Bunq and Boon able to tap up the payment method directly.

Some fifteen banks and services are supported at launch. A further nine banks are slated as adding support in 2019, including DKB, INK and Revolut.

iOS users in the country can now add supported debit or credit cards to Apple Pay to make contactless payments with their device, rather than having to carry cash. Apple’s Face ID and Touch ID biometrics are used to a security layer to the payment system.

The local Apple Pay site also lists a selection of retailers, with Apple writing: “Apple Pay works in supermarkets, boutiques, restaurants, hotels and many other places. You can also use Apple Pay in many apps — and on participating websites with Safari on your Mac, iPhone or iPad.”

Aside from convenience, the other consumer advantage Apple touts for the system is privacy, with Apple Pay using a device-specific number and unique transaction code — and the user’s actual card numbers never stored on their device or on Apple’s servers — which means trackable card numbers aren’t shared with merchants, so purchases can’t be tied back to the individual.

While that might sound like an abstract concern, a Bloomberg report this summer revealed details of a multi-million deal in which Google pays for transaction data from Mastercard — in order to try to link online ad views with offline purchases in the US.

Facebook has also long been known to buy offline data to supplement the interest signals it collects on users from inside (and outside) its social network — further fleshing out ad-targeting profiles.

So escaping the surveillance net of one flavor of big tech can require buying into another. Or else going low tech and paying in cash.

Apple does not say what took it so long to add Germany to its now pretty long list of Apple Pay countries but Apple Insider suggests the relatively late adoption was down to pushback from local banks over fees, noting that it’s four months after the official announcement of a German launch.

It’s also true that paying by plastic isn’t always an option in Germany, as cash remains the dominant payment method of choice — also, seemingly, for privacy purposes. So Apple Pay is at least aligned with those concerns.

Powered by WPeMatico

Apple is fixing one of the worst parts of the concert experience: waiting in line for a beer while you miss your favorite song. Last week’s BottleRock music festival near San Francisco was the first to try a new “order ahead with Apple Pay” feature that Apple hopes to bring to more events. You just open the festival’s app, select the closest concession stand, choose your drinks, Apple Pay with your face or fingerprint and pick up the beverages at a dedicated window with no queue.

Check out our demo video below.

BottleRock’s upscale wine and oldies music fest, 100 miles from the tech giant’s headquarters, has become a testbed for Apple Pay. Last year, every concession stand got equipped with the Square’s Apple Pay-ready point of sale system and special fast lanes for customers who used it instead of cash or credit card. Thirty percent of all transactions at BottleRock were made with Apple Pay, according to an Apple spokesperson, proving people wanted a faster way to get back to the show.

With order ahead, your drinks are ready for pick up so you don’t even have to break your dance stride. Having gone to 14 Coachellas, I’d learned to forego booze rather than risk losing my friends or a chance to hear that hit single while stewing in the beer garden lines. But Apple Pay powered the best concert commerce experience I’ve had yet. I’m sure I’m not the only one who knocked back a few more drinks last weekend because it was so convenient.

That’s why I foresee music festivals jumping at the chance to integrate into their apps order ahead with Apple Pay. They and their vendors will see more sales, while attendees see more music. Meanwhile, it’s a smart way for Apple to reach a juicy demographic. Apple Pay is especially helpful when you’re in a rush, but festival goers will return home more likely to use it day-to-day.

Often times, music festival tech, like friend-finding apps and location-based alerts, can interrupt the moment. Apple Pay succeeds here by fading away, keeping you in harmony with the present.

Powered by WPeMatico

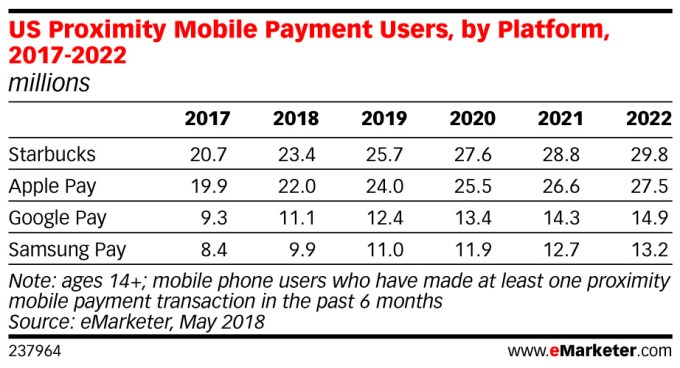

People really love getting their coffee more quickly. Starbucks, which has operated its own mobile payments service since 2011, is the market leader in terms of mobile payments users, beating out Apple Pay, Google Pay, and Samsung Pay, according to a new reporter from eMarketer out this morning. However, Starbucks’ lead over Apple Pay is only a small one – in 2017, it had 20.7 million U.S. users compared with Apple Pay’s 19.7 million. And that gap will remain small this year, with 23.4 million using Starbucks’ mobile payments compared with 22 million using Apple Pay.

The wide adoption of the Starbucks mobile payment service is not only due to speed and convenience that the barcode-based payment system offers – it’s also because payments are tied to loyalty, and the Starbucks app is where customers can monitor and manage their card balance and their “star rewards.” In addition, Starbucks has the benefit of being able to offer a consistent payments experience across its stores – there’s never a question in consumers’ minds as to whether they can use its mobile payments service. They know they can.

Other mobile proximity payment services don’t have the same advantage, as many retailers still don’t offer payment terminals that support the tap-to-pay services like Apple Pay and Google Pay.

According to eMarketer’s forecast, 23.4 million people ages 14 and older will use the Starbucks app to make a point-of-sale purchase at least once every six months, compared with 22 million who will use Apple Pay, 11.1 million who will use Google Pay, and 9.9 million who will use Samsung Pay.

Those numbers will increase across the board through 2022, but the rankings will remain the same – with Starbucks then seeing 29.8 million users to Apple Pay’s 27.5 million.

However, this forecast appears to be discounting the impact of the recent expansion of Apple Pay, which will allow users to send payments to friends through iMessage. When you receive this money, it’s added to an Apple Pay Cash card in your iPhone’s Wallet, which can then be used in stores, in addition to in apps or online. This built-in payments service inside one of the largest messaging platforms could prompt more users to adopt Apple Pay, even if they hadn’t before.

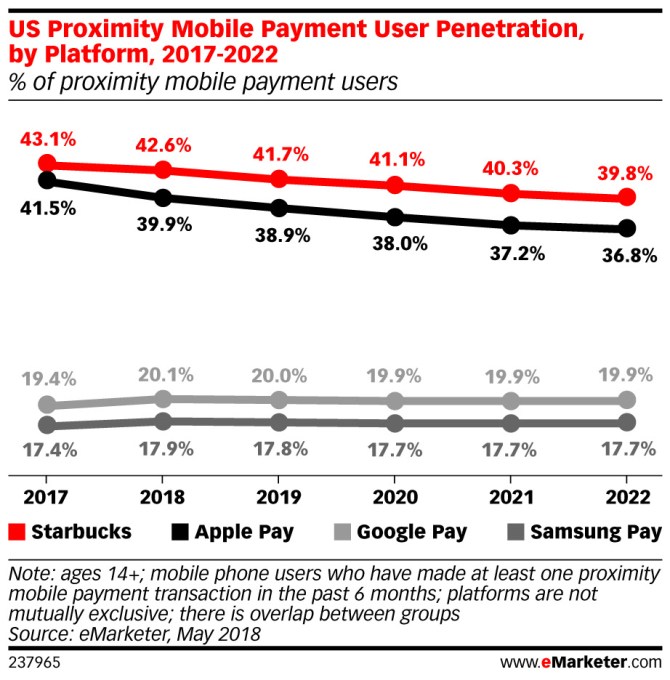

Another note: it seems which services are more popular than others is also tied to how long they’ve been around.

Apple Pay launched before Samsung and Google Pay, and is now accepted at more than half of U.S. merchants. Google Pay isn’t as widely accepted, but is pre-installed on Android, which will help it grow. Samsung Pay, meanwhile, has the lowest adoption in terms of users, but is most accepted by merchants, says eMarketer.

The rankings of the various payment services wasn’t the only notable finding from eMarketer’s new report.

The analysts also found that this year, for the first time, more than 25 percent of U.S. smartphone users ages 14 and older, will have used a mobile payment service at least once every six months. The number of payments users will increase by 14.5 percent to reach 55 million by the end of 2018, the firm estimates.

But over the next several years, these top four services will see their share of the mobile payments drop, even as their user numbers grow. That’s because they’ll face increased competition from other new payment apps, including those from merchants themselves.

“Retailers are increasingly creating their own payment apps, which allow them to capture valuable data about their users. They can also build in rewards and perks to boost customer loyalty,” eMarketer forecasting analyst Cindy Liu says.

eMarketer’s forecast (paywalled) is based on an analysis of third-party data, including Forrester, Juniper Research, and Crone Consulting’s data on U.S. mobile payments users.

Note: Updated after publication to clarify the data is focused on U.S. mobile users

Powered by WPeMatico

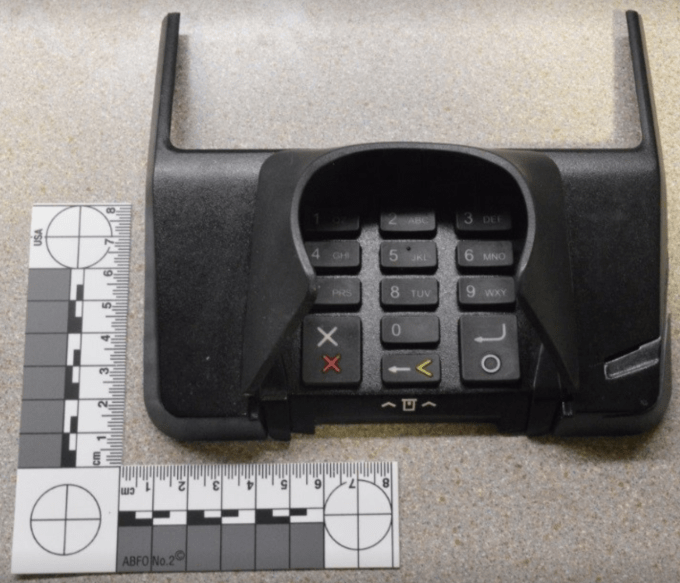

Police in Lower Pottsgrove, Pennsylvania have spotted a group of thieves who are placing completely camouflaged skimmers on top of credit card terminals in Aldi stores. The skimmers, which the gang placed in plain sight of surveillance video cameras, look exactly like the original credit card terminals but would store debit card numbers and PINs of unsuspecting shoppers. “While Aldi… Read More

Police in Lower Pottsgrove, Pennsylvania have spotted a group of thieves who are placing completely camouflaged skimmers on top of credit card terminals in Aldi stores. The skimmers, which the gang placed in plain sight of surveillance video cameras, look exactly like the original credit card terminals but would store debit card numbers and PINs of unsuspecting shoppers. “While Aldi… Read More

Powered by WPeMatico

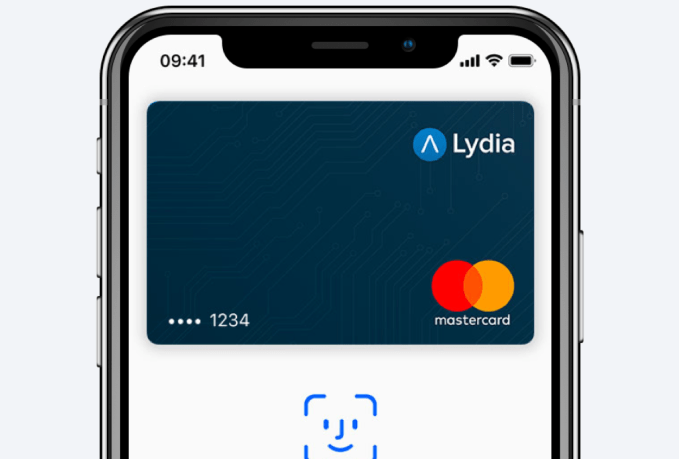

A peer-to-peer payment app that works similarly to Venmo from startup Lydia in France now works with Apple Pay (a feature originally announced in July), making it possible to spend your balance from the app wherever MasterCard and Apple Pay are accepted. It’s a neat use of Apple Pay to make it possible to do mobile payments without requiring that a user have a credit card – and it… Read More

A peer-to-peer payment app that works similarly to Venmo from startup Lydia in France now works with Apple Pay (a feature originally announced in July), making it possible to spend your balance from the app wherever MasterCard and Apple Pay are accepted. It’s a neat use of Apple Pay to make it possible to do mobile payments without requiring that a user have a credit card – and it… Read More

Powered by WPeMatico

Apple Pay Cash is finally starting to roll out to users in the States, bringing the ability to send other iOS users payments directly through iMessage. The update is arriving piece by piece to those who’ve downloaded iOS 11.2, which launched two days back with a not-yet-live version of the feature. Apple Pay Cash was announced back in June at WWDC. However, the company added ahead of… Read More

Apple Pay Cash is finally starting to roll out to users in the States, bringing the ability to send other iOS users payments directly through iMessage. The update is arriving piece by piece to those who’ve downloaded iOS 11.2, which launched two days back with a not-yet-live version of the feature. Apple Pay Cash was announced back in June at WWDC. However, the company added ahead of… Read More

Powered by WPeMatico