app stores

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to This Week in Apps, the Extra Crunch series that recaps the latest OS news, the applications they support and the money that flows through it all.

The app industry is as hot as ever, with a record 204 billion downloads in 2019 and $120 billion in consumer spending in 2019, according to App Annie’s recently released “State of Mobile” annual report. People are now spending 3 hours and 40 minutes per day using apps, rivaling TV. Apps aren’t just a way to pass idle hours — they’re a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus.

In this Extra Crunch series, we help you keep up with the latest news from the world of apps, delivered on a weekly basis.

This week we look at the sad, strange death of HQ Trivia, spying app ToTok getting booted from Google Play (again!), Android 11, an enticing Apple rumor about opening up iOS further to third-party apps, Google Stadia updates, the App Store book Apple wants banned, apps abusing subscriptions and much more.

Once-hot HQ Trivia believed it had invented a new kind of online gaming — live trivia played through your phone. Investors threw $15 million into the company hoping that was true. But the novelty wore off, cheaters came in, prize money dwindled and copycats emerged. Then co-founder Colin Kroll passed away and things at HQ Trivia got worse, including a failed internal mutiny, firings and layoffs. This week, HQ Trivia announced its demise. It then hosted one last, insane night of gaming featuring drunken and cursing hosts who sprayed champagne, called out trolls and begged for new jobs. (Sure, because they exited this one so professionally.)

Powered by WPeMatico

Welcome back to ThisWeek in Apps, the Extra Crunch series that recaps the latest OS news, the applications they support and the money that flows through it all.

The app industry is as hot as ever with a record 204 billion downloads in 2019 and $120 billion in consumer spending in 2019, according to App Annie’s recently released “State of Mobile” annual report. People are now spending 3 hours and 40 minutes per day using apps, rivaling TV. Apps aren’t just a way to pass idle hours — they’re a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus.

In this Extra Crunch series, we help you keep up with the latest news from the world of apps, delivered on a weekly basis.

This week, there was a ton of app news. We’re digging into the latest with Apple’s antitrust issues, Tencent’s plan to leverage WeChat to fend off the TikTok threat, AppsFlyer’s massive new round, the booming subscription economy, Disney’s mobile game studio sale, Pokémon GO’s boost to tourism, Match Group’s latest investment and much more. And did you see the app that lets you use your phone from within a paper envelope? Or the new AR social network? It’s Weird App Week, apparently.

Powered by WPeMatico

Zendesk acquired Base CRM in 2018 to give customers a CRM component to go with its core customer service software. After purchasing the company, it changed the name to Sell, and today the company announced the launch of the new Sell Marketplace.

Officially called The Zendesk Marketplace for Sell, it’s a place where companies can share components that extend the capabilities of the core Sell product. Companies like MailChimp, HubSpot and QuickBooks are available at launch.

App directory in Sell Marketplace. Screenshot: Zendesk

Matt Price, SVP and general manager at Zendesk, sees the marketplace as a way to extend Sell into a platform play, something he thinks could be a “game changer.” He likened it to the impact of app stores on mobile phones.

“It’s that platform that accelerated and really suddenly [transformed smart phones] from being just a product to [launching an] industry. And that’s what the marketplace is doing now, taking Sell from being a really great sales tool to being able to handle anything that you want to throw at it because it’s extensible through apps,” Price explained.

Price says that this ability to extend the product could manifest in several ways. For starters, customers can build private apps with a new application development framework. This enables them to customize Sell for their particular environment, such as connecting to an internal system or building functionality that’s unique to them.

In addition, ISVs can build custom apps, something Price points out they have been doing for some time on the Zendesk customer support side. “Interestingly Zendesk obviously has a very large community of independent developers, hundreds of them, who are [developing apps for] our support product, and now we have another product that they can support,” he said.

Finally, industry partners can add connections to their software. For instance, by installing Dropbox for Sell, it gives sales people a way to save documents to Dropbox and associate them with a deal in Sell.

Of course, what Zendesk is doing here with Sell Marketplace isn’t new. Salesforce introduced this kind of app store concept to the CRM world in 2006 when it launched AppExchange, but the Sell Marketplace still gives Sell users a way to extend the product to meet their unique needs, and that could prove to be a powerful addition.

Powered by WPeMatico

Consumers downloaded a record 204 billion apps in 2019, up 6% from 2018 and up 45% since 2016, and spent $120 billion on apps, subscriptions and other in-app spending in the past year. The average mobile user, meanwhile, is spending 3.7 hours per day using apps. This data and more comes from App Annie’s annual report, “State of Mobile,” which highlights the biggest app trends for the past year, and sets forecasts for the years ahead.

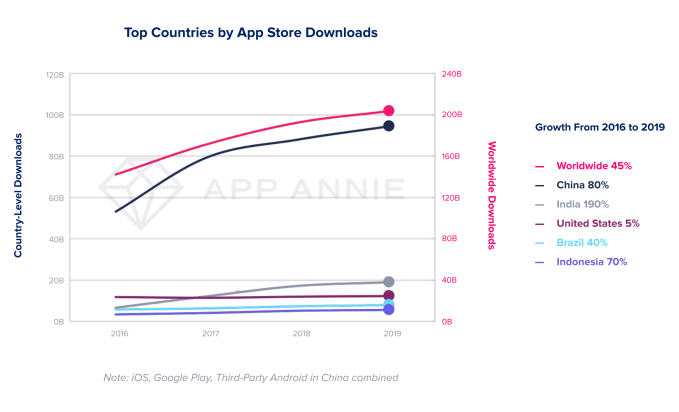

According to App Annie, the record growth in mobile downloads in 2019 can be attributed to the growth taking place in emerging markets like India, Brazil and Indonesia, which have seen downloads soar 190%, 40% and 70%, respectively, since 2016. Meanwhile, download growth in the U.S. has slowed to just 5% during that same time, while China saw 80% growth.

That doesn’t mean users in mature markets aren’t downloading apps, only that the growth in year-over-year download numbers is starting to level off. Still, these more mature markets continue to see large numbers of installs, with more than 12.3 billion downloads in the U.S. in 2019, 2.5 billion in Japan and 2 billion in South Korea.

The record numbers are notable also, given that App Annie’s analysis excludes re-installs and app updates.

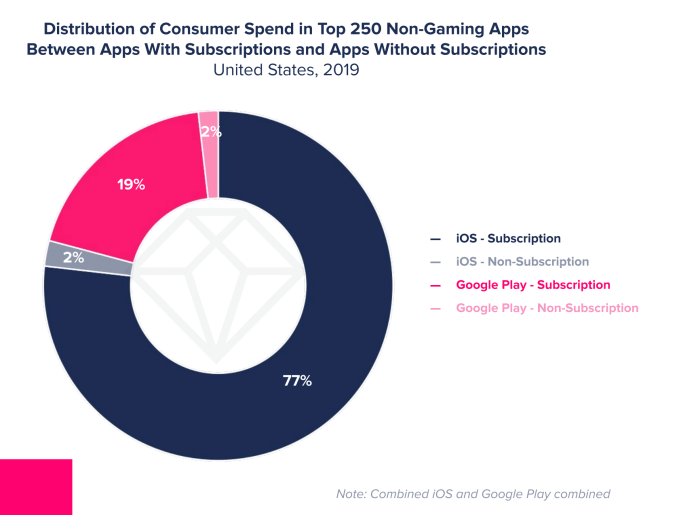

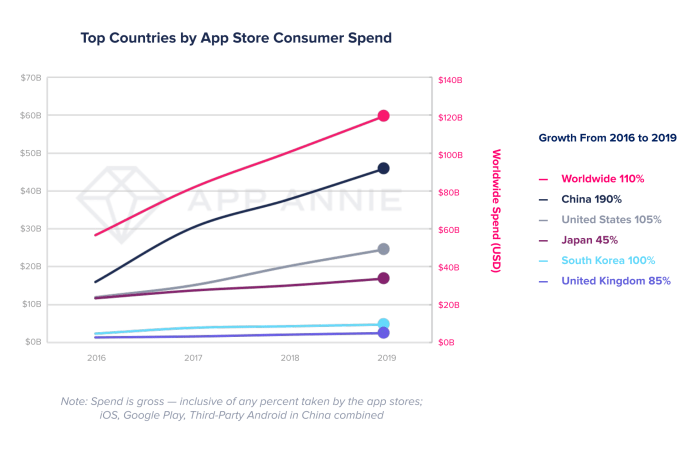

App store consumer spending was on the rise in 2019, as well, with $120 billion spent on apps — a figure that’s up 2.1x from 2016. Games continue to account for the majority (72%) of that spending, but the shift toward subscriptions has played a role, too. Last year, subscriptions in non-gaming apps accounted for 28% of consumer spending, up from 18% in 2016.

Subscriptions are now the primary way many non-gaming apps generate revenue. For example, 97% of consumer spending in the top 250 U.S. iOS apps was driven by subscriptions, and 94% of the apps used subscriptions. On Google Play, 91% of the consumer spending was subscription-based, while 79% of the top 250 apps used subscriptions.

In particular, dating apps like Tinder and video apps like Netflix and Tencent Video topped 2019’s consumer spend charts, thanks to subscription revenue.

Mature markets, including the U.S., Japan, South Korea and the U.K. are helping to fuel consumer spending across both games and subscriptions, App Annie found. But China remains the largest market by far, accounting for 40% of global spend.

App Annie also forecast that the mobile industry will contribute $4.8 trillion to the global GDP by 2023.

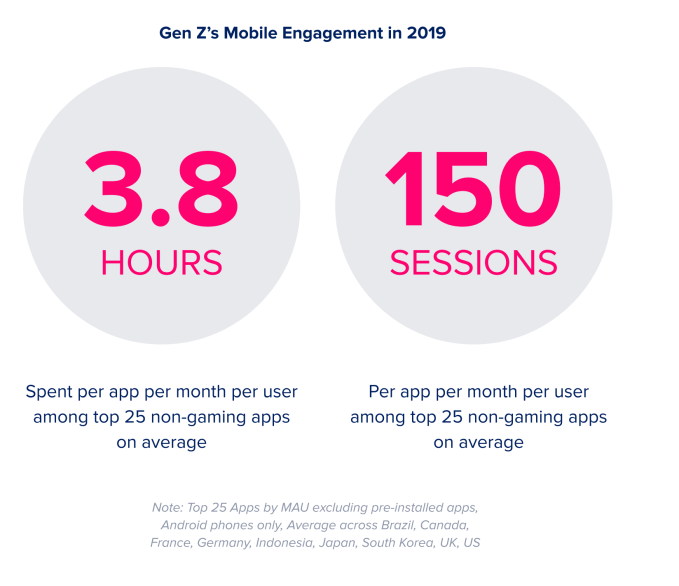

The report additionally identified several mobile trends from 2019, including the mobile app connection to the Internet of Things and smart home devices (106 million downloads for the top 20 IoT apps last year); the huge mobile engagement by Gen Z (3.8 hours per app per month, among the top 25 non-game apps, on avgerage); and mobile ad spend’s growth ($190 billion in 2019 to $240 bilion in 2020).

Ad spending combined with consumer spending is expected to reach $380 billion worldwide by 2020, App Annie forecast.

Gaming was given a big breakout section, given its contribution to consumer spending.

Consumer spending in mobile gaming was 2.4x that of Mac/PC gaming, and 2.9x more than game consoles. In 2019, mobile gaming saw 25% more spending than all other gaming, and is on track to surpass $100 billion across all app stores by next year.

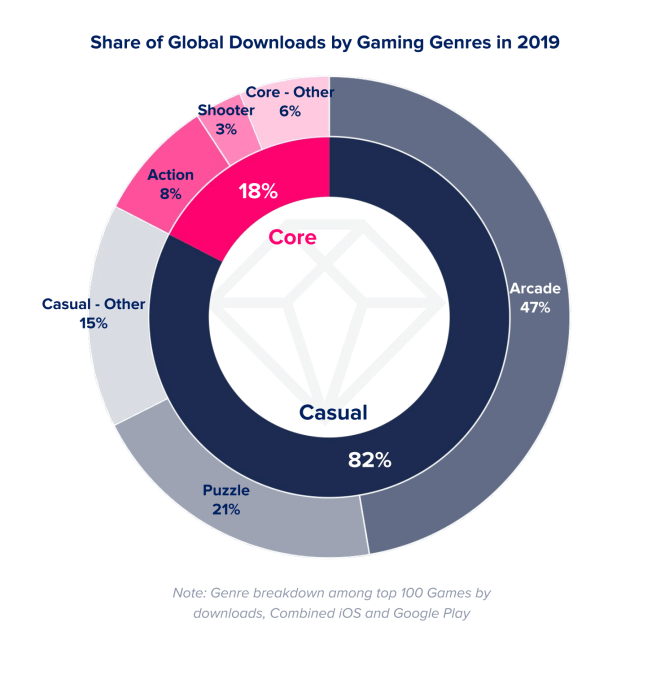

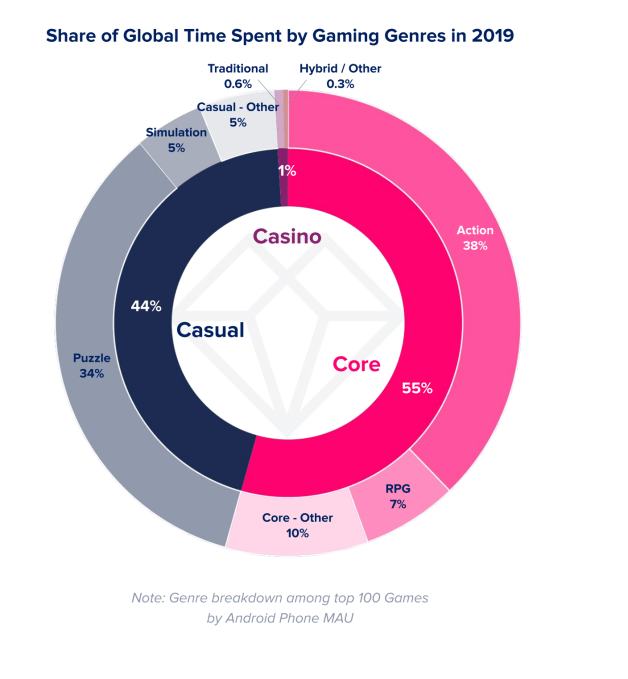

Casual gaming (led by Puzzle and Arcade) was the most downloaded type of games in 2019. Meanwhile, core games (e.g. Action, RPG, etc.) — which were only 18% of downloads — accounted for 55% of time spent in top games. PUBG Mobile was the No. 1 core game (action) on Android in 2019, in terms of time spent, while Anipop (puzzle) was the top casual game.

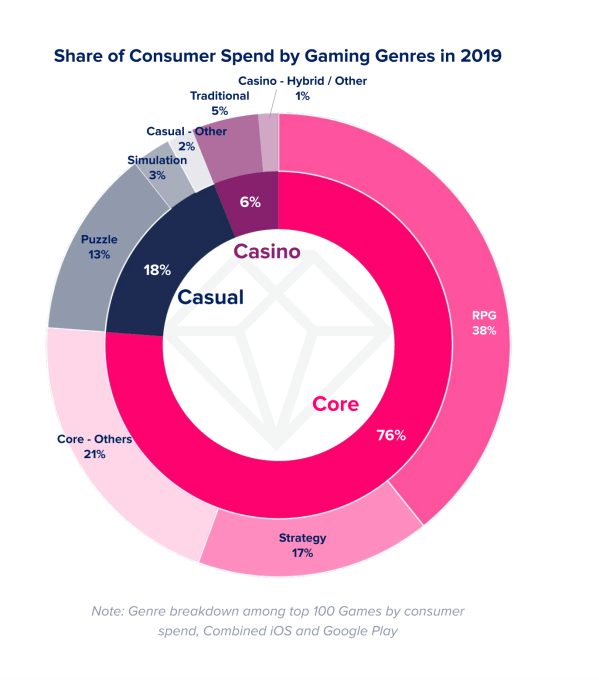

Core games also accounted for the majority (76%) of game spending, followed by casual (18%), then casino (6%).

In 2019, 17% more games surpassed $5 million in consumer spending versus 2017. And the number of games to top $100 million grew 59% compared to two years prior. Despite the sizable growth in revenues, App Annie also pointed to new models in mobile gaming, like Apple Arcade, which is giving other types of games a chance to thrive. Unfortunately, no third-party firm is able to track Arcade revenues, which will become a glaring blind spot for App Annie in the years ahead.

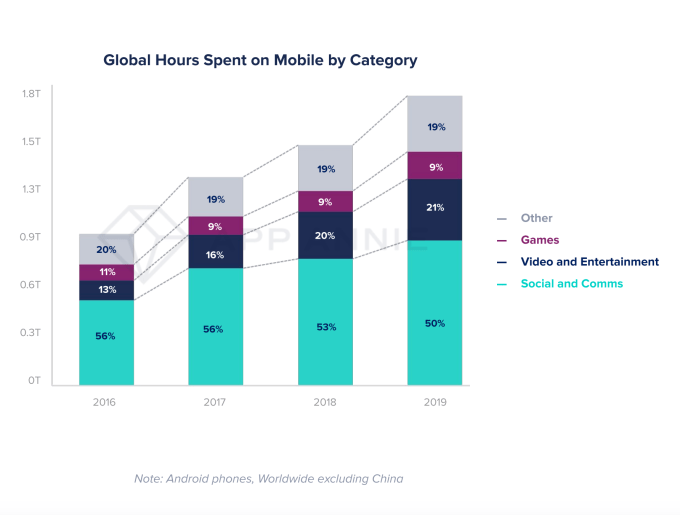

App Annie also examined other sizable segments of the mobile market for trends, including fintech, retail, streaming and social. Some of the more significant findings included: the fintech app user base growth topping that of traditional banking apps; shopping app downloads saw 20% year-over-year growth to reach 5.4 billion downloads; streaming growth that included 50% sessions in 2019 compared to 2017; and 50% of time spent on mobile was spent in social networking and communication apps.

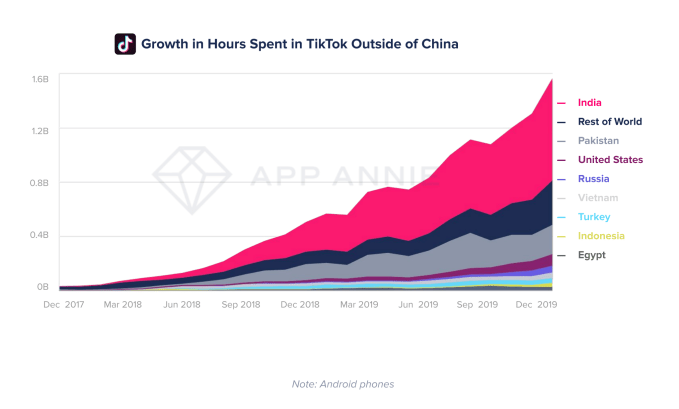

TikTok was given special attention, given its rapid growth last year. Time spent in the short-form video app grew 210% year-over-year in 2019 globally. Even though eight out of every 10 minutes spent in TikTok were by users in China, the app’s usage skyrocketed in other markets as well, App Annie said.

TikTok was given special attention, given its rapid growth last year. Time spent in the short-form video app grew 210% year-over-year in 2019 globally. Even though eight out of every 10 minutes spent in TikTok were by users in China, the app’s usage skyrocketed in other markets as well, App Annie said.

Industries App Annie identified as being transformed by mobile in 2019 included ridesharing, fast food/food delivery, dating, sports streaming, plus health and fitness. The full report offers a few more details and mobile trends for each of these.

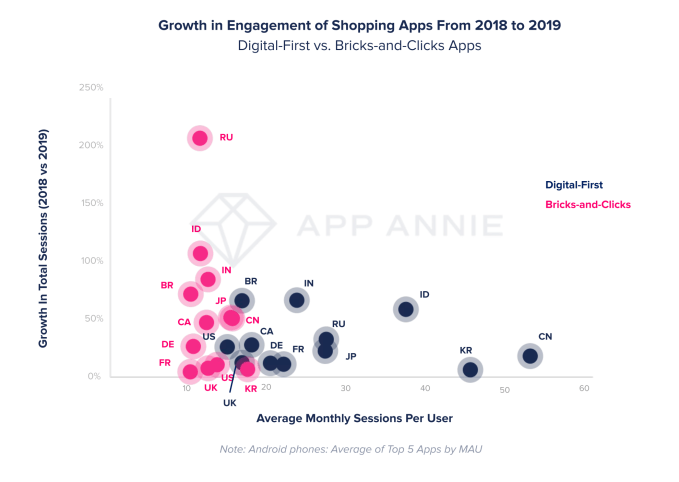

One bigger highlight was that digital-first shopping apps still had 3.2x more average monthly sessions per user compared with apps from traditional brick-and-mortar retailers (dubbed “bricks-and-clicks” apps in the report).

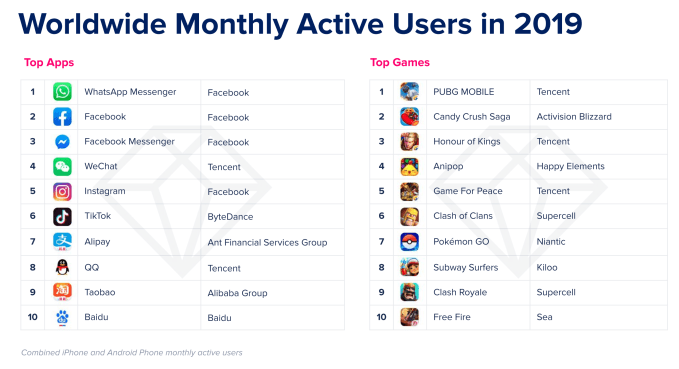

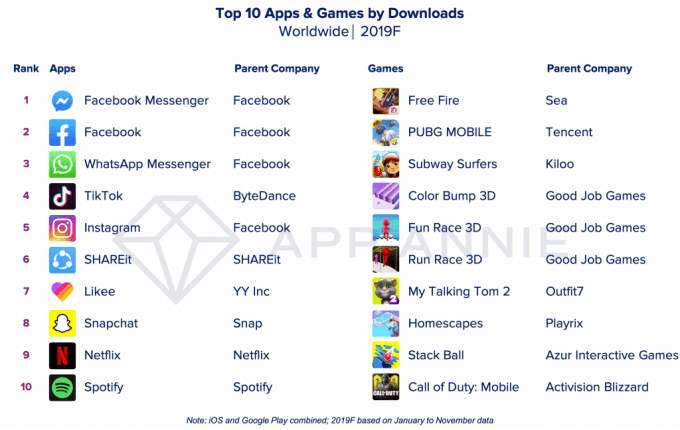

App Annie also compiled its own list of the top apps of 2019 by active users, downloads and revenue. Facebook apps still led by engagement, with WhatsApp, Facebook and Messenger in the top three spots and Instagram as No. 5. And they maintained similar positions by downloads, only swapping places with one another.

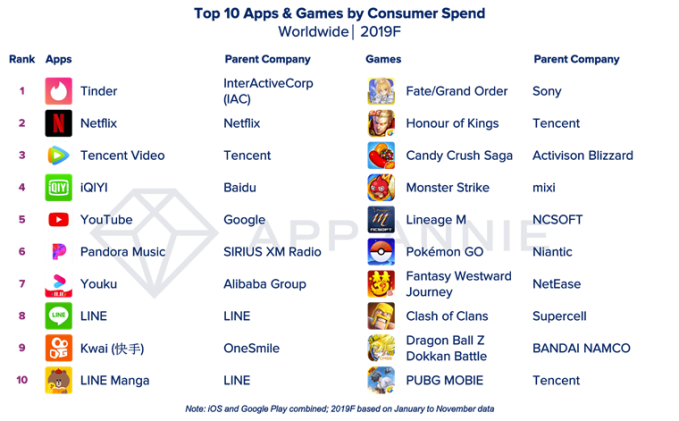

Consumer spending was a different story, with Tinder generating the most revenue in 2019, followed by entertainment and streaming apps like Netflix, Tencent Video, iQIYI, YouTube and others.

Powered by WPeMatico

In Marc Benioff’s book, Trailblazer, he tells the tale of how Steve Jobs planted the seeds of the idea that would become the first enterprise app store, and how Benioff eventually paid Jobs back with the gift of the AppStore.com domain.

While Salesforce did truly help blaze a trail when it launched as an enterprise cloud service in 1999, it took that a step further in 2006 when it became the first SaaS company to distribute related services in an online store.

In an interview last year around Salesforce’s 20th anniversary, company CTO and co-founder Parker Harris told me that the idea for the app store came out of a meeting with Steve Jobs three years before AppExchange would launch. Benioff, Harris and fellow co-founder Dave Moellenhoff took a trip to Cupertino in 2003 to meet with Jobs. At that meeting, the legendary CEO gave the trio some sage advice: to really grow and develop as a company, Salesforce needed to develop a cloud software ecosystem. While that’s something that’s a given for enterprise SaaS companies today, it was new to Benioff and his team in 2003.

As Benioff tells it in his book, he asked Jobs to elucidate on what he meant by an application ecosystem. Jobs replied that how he implemented the idea was up to him. It took some time for that concept to bake, however. Benioff wrote that the notion of an app store eventually came to him as an epiphany at dinner one night a few years after that meeting. He says that he sketched out that original idea on a napkin while sitting in a restaurant:

One evening over dinner in San Francisco, I was struck by an irresistibly simple idea. What if any developer from anywhere in the world could create their own applications for the Salesforce platform? And what if we offered to store these apps in an online directory that allowed any Salesforce user to download them?

Whether it happened like that or not, the app store idea would eventually come to fruition, but it wasn’t originally called the AppExchange, as it is today. Instead, Benioff says he liked the name AppStore.com so much that he had his lawyers register the domain the next day.

When Benioff talked to customers prior to the launch, while they liked the concept, they didn’t like the name he had come up with for his online store. He eventually relented and launched in 2006 with the name AppExchange.com instead. Force.com would follow in 2007, giving programmers a full-fledged development platform to create applications, and then distribute them in AppExchange.

Meanwhile, AppStore.com sat dormant until 2008, when Benioff was invited back to Cupertino for a big announcement around iPhone. As Benioff wrote, “At the climactic moment, [Jobs] said [five] words that nearly floored me: ‘I give you App Store.”

Benioff wrote that he and his executives actually gasped when they heard the name. Somehow, even after all that time had passed since that the original meeting, both companies had settled upon the same name. Except Salesforce had rejected it, leaving an opening for Benioff to give a gift to his mentor. He says that he went backstage after the keynote and signed over the domain to Jobs.

In the end, the idea of the web domain wasn’t even all that important to Jobs in the context of an app store concept. After all, he put the App Store on every phone, and it wouldn’t require a website to download apps. Perhaps that’s why today the domain points to the iTunes store, and launches iTunes (or gives you the option of opening it).

Even the App Store page on Apple.com uses the sub-domain “app-store” today, but it’s still a good story of how a conversation between Jobs and Benioff would eventually have a profound impact on how enterprise software was delivered, and how Benioff was able to give something back to Jobs for that advice.

Powered by WPeMatico

Mobile consumers worldwide will have downloaded a record 120 billion apps from Apple’s App Store and Google Play by the end of 2019, according to App Annie’s year-end report on app trends. This represents a 5% increase from 2018 — a notable achievement given that the number doesn’t include re-installations or app updates. Consumer spending on apps, meanwhile, approached $90 billion in 2019 across both app stores, up 15% from last year. The new report also examined the year’s biggest apps, including the most downloaded apps and games, as well as the most profitable.

Worldwide, the most downloaded non-game apps remained relatively consistent in 2019, with only one new entry on the list of the most downloaded apps — a short-form video creation and sharing app called Likee, which is benefiting from the overall popularity of short-form video. Elsewhere on the chart, TikTok came in at No. 4, beating out Facebook-owned Instagram, plus Snapchat, Netflix and Spotify.

However, Facebook still owned the top of the charts. Its Messenger app was the most downloaded non-game app of 2019, followed by Facebook’s main app, then WhatsApp.

The top 10 games chart showed more volatility in 2019, as seven out of the top 10 games were new to the chart this year. This included the hyper-casual title Fun Race 3D, as well as the anticipated Call of Duty: Mobile, representing the battle royale genre.

While mobile gaming drives the majority of consumer spending on apps, the subscription economy in 2019 played a big role in increasing app revenues, as well.

Specifically, the non-game apps driving revenue growth this year included those in the Photo & Video and Entertainment categories — a trend App Annie predicts will continue in 2020, as new video services, like Disney+, continue to rise. 2020 will additionally see the launch of several other video services, including HBO Max, NBCU’s Peacock and Jeffrey Katzenberg’s Quibi, which could aid in those increases.

Already, many of the top apps are subscription-based, App Annie had previously noted. During the 12 months ending in September 2019, more than 95% of the top 100 non-gaming apps by consumer spend were offering subscriptions through in-app purchases. Publishers’ growing use of subscription services will continue in 2020 to drive consumer spending even higher, the firm says.

This year, Tinder switched places with Netflix for the No. 1 spot on this chart — last year, it was the other way around. HBO NOW, which saw a surge in spending thanks to “Game of Thrones,” also fell out of the top chart this year, allowing LINE Manga to take its spot. Tencent Video and iQIYI have the same positions as 2018, while YouTube grew from No. 7 to No. 5, and Pandora slipped from No. 5 to No. 6 compared with last year.

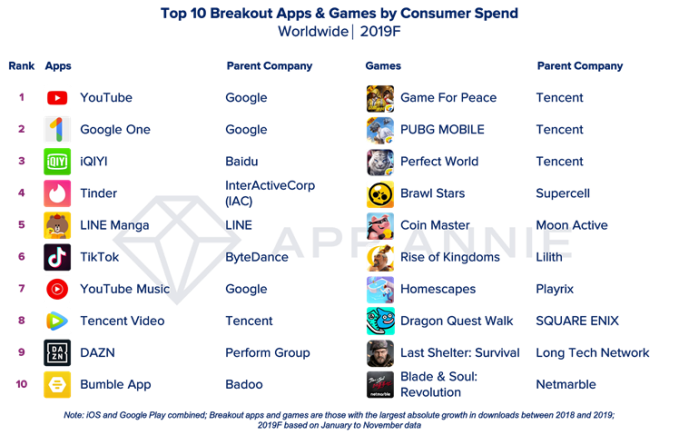

App Annie also took a look at a new category of apps that it’s calling the “breakout” apps of the year. These are those that saw the largest absolute growth in downloads or consumer spending between 2018 and 2019. On this list, the No. 7 most-downloaded app of the year, Likee, from YY Inc., becomes the No. 1 “breakout” app of the year, followed by YY Inc.’s Noizz and Helo. Meanwhile, Indian users drove the adoption of social gaming app Hago at No. 4, which is also popular with Gen Z users in Indonesia.

Breakout apps by consumer spending included YouTube, iQIYI, DAZN and Tencent Video — similar to the top 10 list.

On the gaming side, hyper-casual titles were successful, claiming seven out of 10 slots on the breakout games of the year chart. Hot releases like Mario Kart Tour and Call of Duty: Mobile also appeared. But by consumer spending, core games like No. 1 Game for Peace and No. 2 PUBG Mobile, both published by Tencent, made up the top spots.

Powered by WPeMatico

Global app revenue continues to climb, thanks to the growth in mobile gaming and the subscription economy. In the third quarter of 2019, consumer revenue grew 22.9% year-over-year from $17.9 billion to reach an estimated $21.9 billion across both the App Store and Google Play worldwide, according to new data from Sensor Tower.

Notably, the App Store continues to account for the large majority of this revenue, the report found, making up 65% of total spending compared with just 35% on Google Play.

App Store users spent $14.2 billion, up 22.3% from the $11.6 billion they spent in Q3 2018. Google Play generated $7.7 billion in revenue, up 24% from the $6.2 billion spent in the year-ago quarter.

Sensor Tower’s revenue estimates are a bit lower than those provided by App Annie’s recent report, which said the quarter saw $23 billion in consumer spending, not ~$22 billion.

App Annie also estimated nearly 31 billion downloads in Q3, while Sensor Tower claimed 29.6 billion.

In both cases, Google Play is still said to be the main source for downloads, with nearly three times more first-time installs than the App Store. In Q3, the total number of downloads was up 9.7% year-over-year to 29.6 billion, said Sensor Tower, with Google Play accounting for 21.6 billion of those.

Despite the overall growth, one big app market — China — saw a slight decline, Sensor Tower found. Its installs dropped 6% year-over-year to 2.2 billion in the quarter. But its revenue grew by 26.9% to $4.1 billion, up from $3.2 billion the year prior. This could be attributed to the nine-month game license freeze in China which, though now lifted, had slowed momentum.

Sensor Tower’s charts don’t include third-party app stores, so it’s not a full picture of the Chinese app market, it’s worth noting.

The top money-making (non-game) app in the quarter was again Tinder, which generated $233 million in consumer spending, up 7% over the prior quarter. Netflix was No. 2 and YouTube clocked in at No. 3, at $164 million in Q3.

App Annie has a slightly different ranking. It has Tinder and Netflix leading the top-grossing charts, but puts IQIYI ahead of YouTube. This could be because App Annie has a bigger window into the Chinese app market.

In terms of downloads, TikTok is continuing to disrupt Facebook-owned apps’ dominance over the top of the charts. In Sensor Tower’s rankings, WhatsApp was No. 1 and Messenger was No. 3, but Facebook and Instagram dropped to No. 4 and No. 5, respectively. And TikTok reached No. 2.

This isn’t the first time TikTok has passed Facebook, Sensor Tower said — it did so back in Q4 2018 and in Q1 2019, before dropping to No. 4 again last quarter. But with 177 million downloads in Q3, it’s inching its way up to the top.

App Annie, on the other hand, sees TikTok having just a bit more of climb, sticking it at No. 3 in the quarter, behind Messenger and Facebook. It also called out some Q3 break-out hits, like the return of FaceApp’s popularity (No. 9 in downloads) and the growing subscription revenue of Google One (No. 7 in non-game revenue). Sensor Tower put FaceApp at No. 6 instead, but agreed on Google One.

Mobile gaming continues to generate most of the cash, and did so again in Q3 with $16.3 billion in mobile game gross revenue — or 74% of the total in-app spending, the new report said. The App Store accounted for $9.8 billion of that figure, with Google Play users spending $6.5 billion.

Game downloads across both Google Play and the App Store increased by 17.6% in Q3 from 9.5 billion last year to 11.1 billion.

The top three games in the quarter by downloads were Fun Race 3D (123 million downloads), PUBG Mobile (94 million) and newcomer Mario Kart Tour, which hit 86 million downloads despite only launching in late September.

PUBG Mobile was the top-grossing game with $496 million in revenue, up 652% over last year. The No. 2 title, Tencent’s Honor of Kings, and No. 3 Aniplex’s Fate/Grand Order generated $377 million and $354 million, respectively.

Image credits: Sensor Tower

Correction: App Annie estimated nearly 31 billion downloads in Q3, not 23 billion as first written. We corrected this. Apologies for the error.

Powered by WPeMatico

Following the well-received launch of Apple Arcade, Google today is officially introducing its own take on subscription-based access to premium mobile games — or, in Google’s case, premium mobile apps, too. The new Google Play Pass subscription, arriving this week, will offer more than 350 apps and games that are completely unlocked, with no upfront fees, in-app purchases or advertisements. And the initial price point is something of a no-brainer — it’s just $1.99 per month for the first year, Google says.

That price will increase to $4.99 per month after the first 12 months have passed, which is the same price as Apple Arcade at launch. This launch promotion is only available until October 10, 2019, however.

The two services are similar in concept, as both are providing a large library of premium content for a monthly subscription. But there are some differences between the two.

For starters, Apple Arcade is filled with exclusives — meaning its games will not be found on Andriod. The reverse is not true for Google Play Pass. Instead, the Play Pass catalog includes many cross-platform titles, including some that even found their fame first on iOS, like ustwo’s Monument Valley.

In addition, Play Pass’s launch titles aren’t all games. There are also ad-free versions of popular mobile apps, like AccuWeather, Facetune and Pic Stitch, for example.

Notable launch titles include Stardew Valley, Risk, Terraria, Monument Valley, Star Wars: Knights of the Old Republic, Reigns: Game of Thrones, Titan Quest and Wayward Souls. Some lesser-known additions include LIMBO, Lichtspeer, Mini Metro and Old Man’s Journey. Others, like This War of Mine and Cytus, are coming soon. And for little kids, there are some preschooler-friendly titles like Toca Boca classics and the My Town series.

More titles are added on a monthly basis, Google says.

Because it’s not relying on exclusives; Google’s catalog is more than triple the size of Apple’s at launch. That being said, Apple’s Arcade library is filled with gorgeous, high-quality games while Play Pass is rounded out with a lot more utilities, like weather apps and photo editors.

![]() Like Apple Arcade, the new subscription gets its own tab in the Google Play app, where the games are organized by genre, popularity and other factors — just like a mini app store. However, unlike Apple Arcade, where games are only found in the Arcade tab or through search, Google Play Pass titles will appear directly in the Play Store. They’ll be designated with a Play Pass ticket badge, so you can easily identify them.

Like Apple Arcade, the new subscription gets its own tab in the Google Play app, where the games are organized by genre, popularity and other factors — just like a mini app store. However, unlike Apple Arcade, where games are only found in the Arcade tab or through search, Google Play Pass titles will appear directly in the Play Store. They’ll be designated with a Play Pass ticket badge, so you can easily identify them.

The Play Pass subscription also allows the games to be shared with the whole family. The family manager can share their Play Pass subscription with up to five other family members, who can each access the titles independently. This is comparable to Apple Arcade.

We already knew Google was working on an Apple Arcade competitor before today. The Play Pass subscription’s existence had been leaked, and Google later confirmed the service with a tweet. What we didn’t yet know was the launch date, lineup or the official pricing.

Google Play Pass service is rolling out this week to Android devices in the U.S., with more countries coming soon. A 10-day subscription is available, before it converts to the $1.99 per month limited promotion, followed by the $4.99 per month price point when the promotion ends.

While neither Apple nor Google is discussing the terms of their deals with developers, Google says the more people download a Play Pass title, the more the revenue developers receive on a recurring basis. It also explained that Google itself is funding the initial launch offer, so developers can gain more subscriber interest without impacting their revenue.

Powered by WPeMatico

App store spending is continuing to grow, although not as quickly as in years past. According to a new report from Sensor Tower, the iOS App Store and Google Play combined brought in $39.7 billion in worldwide app revenue in the first half of 2019 — that’s up 15.4% over the $34.4 billion seen during the first half of last year. However, at that time, the $34.4 billion was a 27.8% increase from 2017’s numbers, then a combined $26.9 billion across both stores.

Apple’s App Store continues to massively outpace Google Play on consumer spending, the report also found.

In the first half of 2019, global consumers spent $25.5 billion on the iOS App Store, up 13.2% year-over-year from the $22.6 billion spent in the first half of 2018. Last year, the growth in consumer spending was 26.8%, for comparison’s sake.

Still, Apple’s estimated $25.5 billion in the first half of 2019 is 80% higher than Google Play’s estimated gross revenue of $14.2 billion — the latter a 19.6% increase from the first half of 2018.

The major factor in the slowing growth is iOS in China, which contributed to the slowdown in total growth. However, Sensor Tower expects to see China returning to positive growth over the next 12 months, we’re told.

To a smaller extent, the downturn could be attributed to changes with one of the top-earning apps across both app stores: Netflix.

Last year, Netflix dropped in-app subscription sign-ups for Android users. Then, at the end of December 2018, it did so for iOS users, too. That doesn’t immediately drop its revenue to zero, of course — it will continue to generate revenue from existing subscribers. But the number will decline, especially as Netflix expands globally without an in-app purchase option, and as lapsed subscribers return to renew online with Netflix directly.

In the first half of 2019, Netflix was the second highest earning non-game app with consumer spending of $339 million, Sensor Tower estimates, down from $459 million in the first half of 2018. (We should point out the firm bases its estimates on a 70/30 split between Netflix and Apple’s App Store that drops to 85/15 after the first year. To account for the mix of old and new subscribers, Sensor Tower factors in a 25% cut. But Daring Fireball’s John Gruber claims Netflix had a special relationship with Apple where it had an 85/15 cut from year one.)

In any event, Netflix’s contribution to the app stores’ revenue is on the decline.

In the first half of last year, Netflix had been the No. 1 non-game app for revenue. This year, that spot went to Tinder, which pulled in an estimated $497 million across the iOS App Store and Google Play, combined. That’s up 32% over the first half of 2018.

But Tinder’s dominance could be a trend that doesn’t last.

According to recent data from eMarketer, dating app audiences have been growing slower than expected, causing the analyst firm to revise its user estimates downward. It now expects that 25.1 million U.S. adults will use a dating app monthly this year, down from its previous forecast of 25.4 million. It also expects that only 21% of U.S. single adults will use a dating app at all in 2019, and that will only grow to 23% by 2023.

That means Tinder’s time at the top could be overrun by newcomers in later months, especially as new streaming services get off the ground (assuming they offer in-app subscriptions); if TikTok starts taking monetization seriously; or if any other large apps from China find global audiences outside of China’s third-party app stores.

For example, Tencent Video grossed $278 million globally in the first half of 2019, outside of the third-party Chinese Android app stores. That made it the third-largest non-game app by revenue. And Chinese video platform iQIYI and YouTube were the No. 4 and No. 5 top-grossing apps, respectively.

Meanwhile, iOS app installs actually declined in the first half of the year, following the first quarter that saw a decline in downloads, Q1 2019, attributed to the downturn in China.

The App Store in the first half of 2019 accounted for 14.8 billion of the total 56.7 billion app installs.

Google Play installs in the first half of the year grew 16.4% to 41.9 billion, or about 2.8 times greater than the iOS volume.

The most downloaded apps in the first half of 2019 were the same as before: WhatsApp, Messenger and Facebook led the top charts. But TikTok inched ahead of Instagram for the No. 4 spot, and it saw its installs grow around 28% to nearly 344 million worldwide.

In terms of mobile gaming specifically, spending was up 11.3% year-over-year in the first half of 2019, reaching $29.6 billion across the iOS App Store and Google Play. Thanks to the fallout of the game licensing freeze in China, App Store revenue growth for games was at $17.6 billion, or 7.8% year-over-year growth. Google Play game spending grew by 16.8% to $12 billion.

The top-grossing games, in order, were Tencent’s Honor of Kings, Fate/Grand Order, Monster Strike, Candy Crush Saga and PUBG Mobile.

Meanwhile, the most downloaded games were Color Bump 3D, Garena Free Fire and PUBG Mobile.

Image credits: Sensor Tower

Powered by WPeMatico

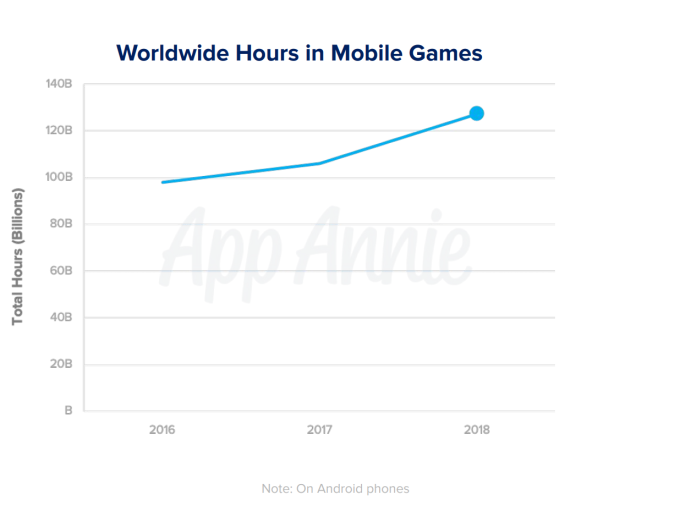

Mobile gaming continues to hold its own, accounting for 10% of the time users spend in apps — a percentage that has remained steady over the years, even though our time in apps overall has grown by 50% over the past two years. In addition, games are continuing to grow their share of consumer spend, notes App Annie in a new research report out this week, timed with E3.

Thanks to growth in hyper-casual and cross-platform gaming in particular, mobile games are on track to reach 60% market share in consumer spend in 2019.

The new report looks at how much time users spend gaming versus using other apps, monetization and regional highlights within the gaming market, among other things.

Despite accounting for a sizable portion of users’ time, games don’t lead the other categories, App Annie says.

Instead, social and communications apps account for half (50%) of the time users spent globally in apps in 2018, followed by video players and editors at 15%, then games at 10%.

In the U.S., users generally have eight games installed per device; globally, we play an average of two to five games per month.

The number of total hours spent on games continues to grow roughly 10% year-over-year, as well, thanks to existing gamers increasing their time in games and from a broadening user base, including a large number of mobile app newcomers from emerging markets.

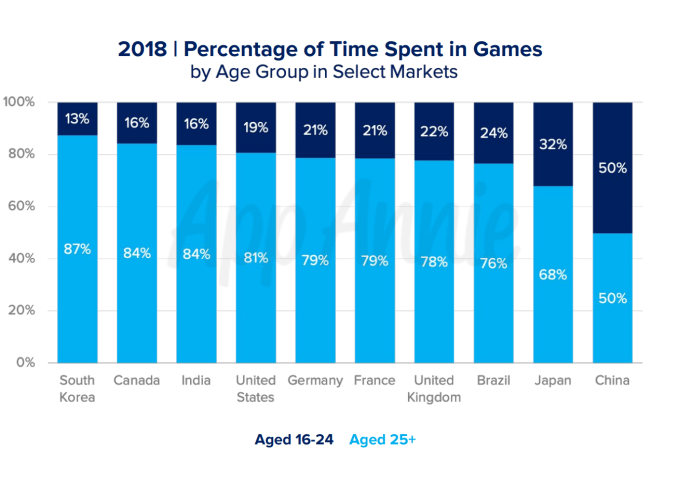

This has also contributed to a widening age range for gamers.

Today, the majority of time spent in gaming is by those aged 25 and older. In many cases, these players may not even classify themselves as “gamers,” App Annie noted.

While games may not lead the categories in terms of time spent, they do account for a large number of mobile downloads and the majority of consumer spending on mobile.

One-third of all worldwide downloads are games across iOS, Google Play and third-party app stores.

Last year, 1.6+ million games launched on Google Play and 1.1+ million arrived on iOS.

On Android, 74 cents of every dollar is spent on games, with 95% of those purchases coming as in-app purchases, not paid downloads. App Annie didn’t have figures for iOS.

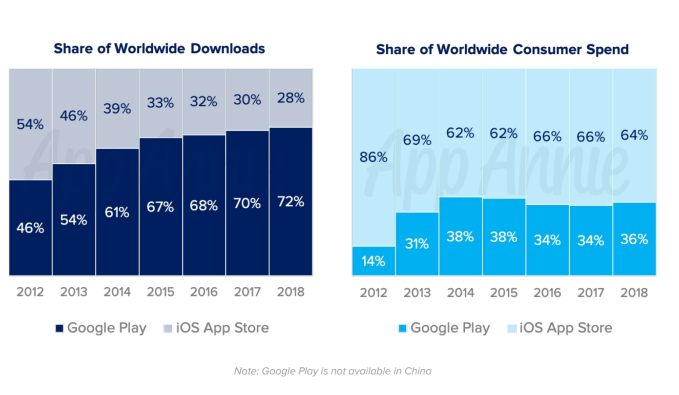

Google Play is known for having more downloads than iOS, but continues to trail on consumer spend. In 2018, Google Play grabbed a 72% share of worldwide downloads, compared with 28% on iOS. Meanwhile, Google Play only saw 36% of consumer spend versus 64% on iOS.

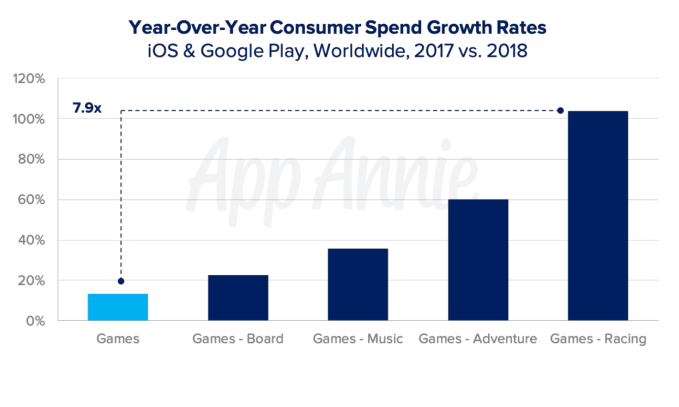

One particular type of gaming jumped out in the new report: racing games.

Consumer spend in this subcategory of gaming grew 7.9 times as fast as the overall mobile gaming market. Adventure games did well, too, growing roughly five times the rate of games in general. Music games and board games were also popular.

Of course, gaming expands beyond mobile. But it’s surprising to see how large a share of the broader market can be attributed to mobile gaming.

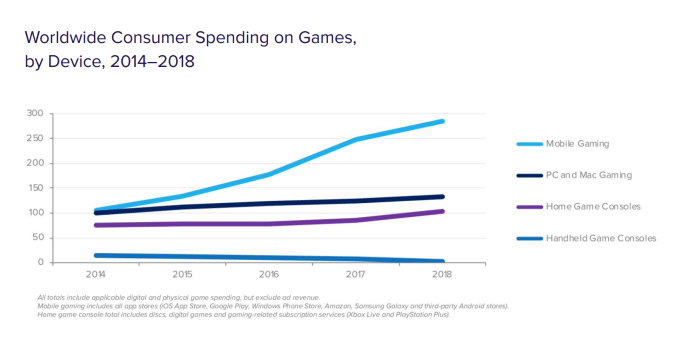

According to App Annie, mobile gaming is larger than all other channels, including home game consoles, handheld consoles and computers (Mac and PC). It’s also 20% larger than all these other categories combined — a shift from only a few years ago, attributed to the growth in the mobile consumer base, which allows mobile gaming to reach more people.

Cross-platform gaming is a key gaming trend today, thanks to titles like PUBG and Fortnite in particular, which were among the most downloaded games across several markets last year.

Meanwhile, hyper-casual games are appealing to those who don’t think of themselves as gamers, which has helped to broaden the market further.

App Annie is predicting the next big surge will come from AR gaming, with Harry Potter: Wizards Unite expected to bring Pokémon Go-like frenzy back to AR, bringing the new title $100 million in its first 30 days. The game is currently in beta testing in select markets, with plans for a 2019 release.

In terms of regions, China’s impact on gaming tends to be outsized, but its growth last year was limited due to the game license regulations. This forced publishers to look outside the country for growth — particularly in markets like North America and Japan, App Annie said.

Meanwhile, India, Brazil, Russia and Indonesia lead the emerging markets with regard to game

downloads, but established markets of the U.S. and China remain strong players in terms of sheer numbers.

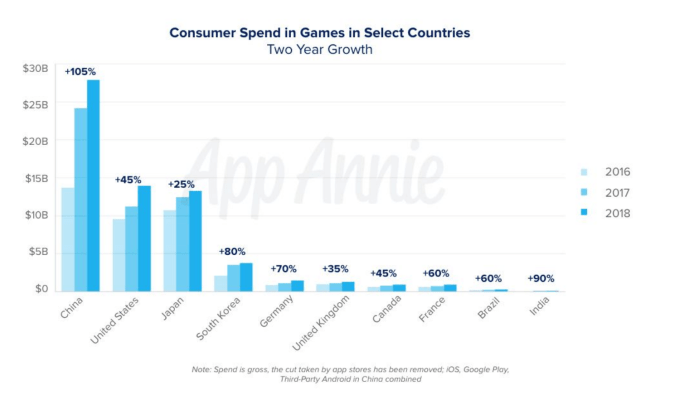

With the continued steady growth in consumer spend and the stable time spent in games, App Annie states the monetization potential for games is growing. In 2018, there were 1,900 games that made more than $5 million, up from 1,200 in 2016. In addition, consumer spend in many key markets is still growing too — like the 105% growth in two years in China, for example, and the 45% growth in the U.S.

The full report delves into other regions as well as game publishers’ user acquisition strategies. It’s available for download here.

Powered by WPeMatico