anthemis

Auto Added by WPeMatico

Auto Added by WPeMatico

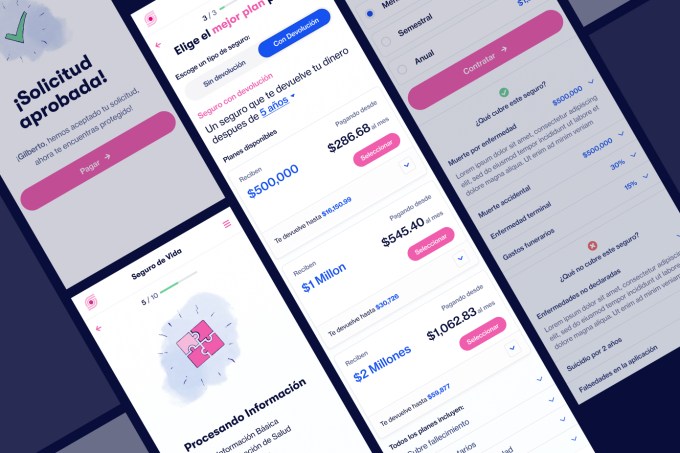

Super.mx, an insurtech startup based in Mexico City, has raised $7.2 million in a Series A round led by ALLVP.

Co-founded in 2019 by a trio of former insurance industry executives, Super.mx’s self-proclaimed mission is to design insurance for “the emerging Latin American middle class,” according to CEO Sebastian Villarreal.

“That means insurance that is easy to buy – it can be bought on a cell phone in minutes – and that pays quickly with no adjusters,” he said. The company has built its offering with proprietary models that are used both on the underwriting side to predict risk and on the claims side to make payments automatically.

Goodwater Capital, Kairos Angels and Bridge Partners also participated in the Series A round in addition to angels such as Joe Schmidt IV, vice president of business development at insurtech Ethos and former investor at Accel and Kyle Nakatsuji, founder and CEO of auto insurance startup Clearcover (and also a former VC). Better Tomorrow Ventures led Super.mx’s $2.4 million seed round, which also saw capital from 500 Startups Mexico, Village Global, Anthemis and Broadhaven Ventures, among others.

Unlike most insurtech startups in Latin America, Villarreal emphasizes that Super.mx is neither an aggregator nor a carrier. Instead, it’s an MGA, or managing general agent.

“This lets us have a ‘best of both worlds’ approach,” Villarreal said. “We handle the entire user experience just like a direct to consumer carrier, but with the breadth of product choice offered by an aggregator.”

That product choice includes property, natural disasters and life insurance. The company soon plans to expand to also offer health insurance.

The founding team brings a variety of insurance experience to the table. Villarreal previously co-founded Chicago-based Kin Insurance (which raised over $150 million in funding from the likes of Flourish Ventures, Commerce Ventures and QED Investors). He was also once head of auto product at Avant, a growth-stage company funded by General Atlantic and Tiger Global, among others.

With over two decades of insurance industry experience, Dario Luna once served as Mexico’s insurance regulator and helped develop Mexico’s disaster risk management strategy. Marco Ahedo has designed parametric insurance products for 19 Caribbean countries. He was also once a solvency expert for life and health insurance lines at MetLife, and has developed financial models for several P&C carriers.

Villarreal lived in the U.S. for a while before deciding to move back to Mexico, which he recognized was home to an “underinsurance problem.”

“That’s actually a very acute problem,” he said. “People in Latin America buy a lot less insurance than they do in the U.S., and people in Mexico, in particular, buy a lot less insurance than they do in other Latin countries.”

Some have blamed the lack of insurance coverage on the country’s culture but Super.mx operates under the belief that this notion is “total BS.”

“It’s not a cultural problem,” Villarreal said. “The problem is that the insurance products that exist in the market just suck. They’re super expensive. They’re really hard to buy, and they pay very little.”

Image Credits: Super.mx

So far, Super.mx has sold “thousands of policies” but is more focused now on increasing the number of products that it’s selling. The company started out by selling earthquake insurance before adding COVID insurance, and more recently, in April, it launched life insurance. Next, it’s going to offer property, renter’s and health insurance.

“It’s really a different strategy than what you would find in the U.S.,” Villarreal said. “In the U.S, when you look at insurtechs, it’s like everyone just does one thing, but here, it’s very different because when someone says ‘I want insurance,’ really what they’re saying is ‘Hey, something happened that makes me nervous that didn’t make me nervous before.’”

That something could be a new child, for example, that prompts a need for life insurance.

“What we’re trying to do is like Lemonade, Roots and Hippo or Kin all rolled into one,” he added. It’s a big, big play.”

Digital adoption in Mexico, and Latin America in general, has increased exponentially in recent years. The bigger hurdle for Super.mx, according to Villarreal, has less to do with technology and more to do with Mexicans getting over what he describes a “deep mistrust” based on bad experiences in the past.

“People are really distrustful and that’s a huge hurdle, but once you show them that you actually are different,” Villarreal told TechCrunch, “that you actually do things in a different way, you get this incredible emotional response.”

Eventually, Super.mx plans to outside of Mexico to other countries in Latin America.

ALLVP’s Federico Antoni said his Mexico City-based firm had been looking for a team building in this space “for years” before investing in Super.mx. The venture firm was impressed with the company’s technical knowledge and industry expertise. It was also drawn to their multi-product approach and “capacity to ship highly complex products to the market quickly” — both of which he believes are “unique” in the region.

Citing statistics from MAPFRE Economics, Antoni pointed out that globally, the insurance market has been growing over the last 10 years. During that time, Latin America expanded faster on average (4.4% vs. 2.4% worldwide), albeit with more volatility. Life insurance has been driving this growth, at 6.1%, over the period.

“Insurtech may be even bigger than fintech. Also, harder,” he told TechCrunch via email. “We knew the team to unlock the market potential would need to be highly competent and highly disruptive.”

Antoni said he is also convinced that Insurtech is the “next frontier” in financial inclusion in Latin America especially as digitization continues to increase.

“Providing risk coverage to individuals and businesses in the region, brings financial stability to families and unlocks economic potential for SMEs,” he said. “Moreover, the insurance incumbents have been unable to address a growing and underserved market.”

Powered by WPeMatico

StepLadder, another London-based startup aiming to help so-called “generation rent” get onto the housing ladder, has raised £1.5 million in seed funding.

Backing the round is Spanish banking giant BBVA and fintech VC Anthemis via the London-based venture studio on which the pair have partnered. Early investor Seedcamp also followed on, in addition to unnamed angel investors.

StepLadder says it will use the new capital and support provided by BBVA/Anthemis to further develop its “collaborative finance platform.” The startup is also eyeing international expansion.

Founded in 2015 by Matthew Addison and joined by Lucy Mullins and Mihir Bhushan, StepLadder’s collaborative deposit saving platform is designed to motivate renters to save for a deposit so they can purchase their first home.

Using a financial model known as a “Rotating Credit and Savings Association” (ROSCA), StepLadder puts its members into “Circles,” whereby each individual member contributes an identical amount on a monthly basis — ranging from £25 to £1,000. A random draw then takes place each month and the winner is provided with that month’s full pot to use toward their deposit.

“For most first-time buyers, it’s really difficult to get on the property ladder,” says Addison. “Home ownership rates amongst 25 to 34-years-olds have collapsed… [with around] 250,000 fewer first-time buyers every year, for over a decade, in the U.K. alone. Raising the deposit is the biggest hurdle. At StepLadder we’re using something called a ROSCA, a form of collaborative finance where people work together in groups to help our members raise their property deposits, on average, 45% faster.”

As an example, StepLadder might match you to a £500 a month Circle for 20 months to raise £10,000. This would see it find 19 other members to be in the same Circle. “Each month the £10,000 is randomly allocated and you could be drawn at any point in that 20 months,” explains StepLadder’s Lucy Mullins. “You have to keep making your £500 a month payment for the full 20 months, so at the end everybody has paid in £10,000 and everybody has received £10,000.”

To help protect the platform from being abused, Mullins says that while a member is still part of a Circle, the startup will only release the pot to their solicitor for use as a property deposit. “So, if somebody stops paying after they have been drawn then we wouldn’t release their payout until they had made catch-up payments.”

StepLadder also supports members along the house-buying journey. The app lets members engage with a community of like-minded people and access group-buying discounts on services such as mortgages, solicitor fess and surveyors. The latter forms part of the company’s revenue stream.

“We introduce our members (at their request) to high-quality service providers, such as mortgage brokers, lending banks, surveyors and insurance providers,” says Addison. “In return, these partners pay us fees or commissions. We offer discounts on these transaction services via the combined buying power of our members in their Circles.”

In addition, there is a small monthly fee (between 2-5%) to be part of a Circle, which Mullins says covers the cost of delivering the service.

This includes holding money securely in a client money account, a payment waiver if a member were to become sick or unemployed after buying a property with their StepLadder deposit, credit bureau costs and the cost of a Circle host to support members on the journey.

“We do not aim to profit from the monthly administration fees we charge members and would usually be able to save our members much more in discounts than they pay in fees,” says Mullins.

Meanwhile, StepLadder has plans to expand the use cases for Circles and evolve the platform to also cover general savings goals and targeted “big ticket items.”

Explains Addison: “In Brazil, ROSCAs are used by nine million consumers for everything from dishwashers to cars to homes. We have already begun to demonstrate this potential with both our First Step offering (smaller circles from £25 a month) and proposed partnered launches.”

Powered by WPeMatico

Pretty much everything about making a self-driving car is difficult, but among the most difficult parts is making sure the vehicles know what pedestrians are doing — and what they’re about to do. Humanising Autonomy specializes in this, and hopes to become a ubiquitous part of people-focused computer vision systems worldwide.

The company has raised a $5.3 million seed round from an international group of investors on the strength of its AI system, which it claims outperforms humans and works on images from practically any camera you might find in a car these days.

HA’s tech is a set of machine learning modules trained to identify different pedestrian behaviors — is this person about to step into the street? Are they paying attention? Have they made eye contact with the driver? Are they on the phone? Things like that.

The company credits the robustness of its models to two main things. First, the variety of its data sources.

“Since day one we collected data from any type of source — CCTV cameras, dash cams of all resolutions, but also autonomous vehicle sensors,” said co-founder and CEO Maya Pindeus. “We’ve also built data partnerships and collaborated with different institutions, so we’ve been able to build a robust data set across different cities with different camera types, different resolutions and so on. That’s really benefited the system, so it works in nighttime, rainy Michigan situations, etc.”

Notably their models rely only on RGB data, forgoing any depth information that might come from lidar, another common sensor type. But Pindeus said that type of data isn’t by any means incompatible, it just isn’t as plentiful or relevant as real-world, visual-light footage.

In particular, HA was careful to acquire and analyze footage of accidents, because these are especially informative cases of failure of AVs or human drivers to read pedestrian intentions, or vice versa.

The second advantage Pindeus claimed is the modular nature of the models the company has created. There isn’t one single “what is that pedestrian doing” model, but a set of them that can be individually selected and tuned according to the autonomous agent’s or hardware’s needs.

“For instance, if you want to know if someone is distracted as they’re crossing the street. There’s a lot of things that we do as humans to tell if someone is distracted,” she said. “We have all these different modules that kind of come together to predict whether someone’s distracted, at risk, etc. This allows us to tune it to different environments, for instance London and Tokyo — people behave differently in different environments.”

“For instance, if you want to know if someone is distracted as they’re crossing the street. There’s a lot of things that we do as humans to tell if someone is distracted,” she said. “We have all these different modules that kind of come together to predict whether someone’s distracted, at risk, etc. This allows us to tune it to different environments, for instance London and Tokyo — people behave differently in different environments.”

“The other thing is processing requirements; Autonomous vehicles have a very strong GPU requirement,” she continued. “But because we build in these modules, we can adapt it to different processing requirements. Our software will run on a standard GPU when we integrate with level 4 or 5 vehicles, but then we work with aftermarket, retrofitting applications that don’t have as much power available, but the models still work with that. So we can also work across levels of automation.”

The idea is that it makes little sense to aim only for the top levels of autonomy when really there are almost no such cars on the road, and mass deployment may not happen for years. In the meantime, however, there are plenty of opportunities in the sensing stack for a system that can simply tell the driver that there’s a danger behind the car, or activate automatic emergency braking a second earlier than existing systems.

While there are lots of papers published about detecting pedestrian behavior or predicting what a person in an image is going to do, there are few companies working specifically on that task. A full-stack sensing company focusing on lidar and RGB cameras needs to complete dozens or hundreds of tasks, depending on how you define them: object characterizations and tracking, watching for signs, monitoring nearby and distant cars and so on. It may be simpler for them and for manufacturers to license HA’s functioning and highly specific solution rather than build their own or rely on more generalized object tracking.

“There are also opportunities adjacent to autonomous vehicles,” pointed out Pindeus. Warehouses and manufacturing facilities use robots and other autonomous machines that would work better if they knew what workers around them were doing. Here the modular nature of the HA system works in its favor again — retraining only the parts that need to be retrained is a smaller task than building a new system from scratch.

Currently the company is working with mobility providers in Europe, the U.S. and Japan, including Daimler Mercedes Benz and Airbus. It’s got a few case studies in the works to show how its system can help in a variety of situations, from warning vehicles and pedestrians about each other at popular pedestrian crossings to improving path planning by autonomous vehicles on the road. The system can also look over reams of past footage and produce risk assessments of an area or time of day given the number and behaviors of pedestrians there.

The $5 million seed round, led by Anthemis, with Japan’s Global Brain, Germany’s Amplifier and SV’s Synapse Partners, will mostly be dedicated to commercializing the product, Pindeus said.

“The tech is ready, now it’s about getting it into as many stacks as possible, and strengthening those tier 1 relationships,” she said.

Obviously it’s a rich field to enter, but still quite a new one. The tech may be ready to deploy, but the industry won’t stand still, so you can be sure that Humanising Autonomy will move with it.

Powered by WPeMatico

Entering into the world of Anthemis is a bit like stepping into the frame of a Wes Anderson film. Eclectic, offbeat people situated in colorful interiors? Check. A muse in the form of a renowned British-Venezuelan economist? Check. A design-forward media platform to provoke deep thought? Check. An annual summer retreat ensconced in the French Alps? Bien sûr.

Sitting atop this most unusual fintech(ish) VC is its ponytailed founder and chairman Sean Park, whose difficult-to-place accent and Philosophy professor aura belie his extensive fixed income capital markets experience. He’s joined by founder and CEO Amy Nauiokas, who in addition to being one of Fintech’s most prominent female investors also owns a high-minded film and television production company.

When Arman Tabatabai and I recently sat down with Park and Nauiokas in their New York office, the firm’s leaders were in an upbeat mood, having blown past the temporary perception-setback associated with the abrupt resignation last year of Anthemis’ former CEO Nadeem Shaikh (for more on this, read TechCrunch writer Steve O’Hear’s coverage of the situation).

And as the conversation below demonstrates, Park and Nauiokas are well poised to bring the quirk into everything they touch, which these days runs the gamut from backing companies involved in sustainable finance, advancing their home-grown media platform and preparing a soon-to-be-announced initiative elevating female entrepreneurs.

Gregg Schoenberg: With the two of you now at the helm, how does Anthemis present itself today?

Sean Park: I’ll step back and say that when Amy and I were working at big financial institutions in the noughties, we saw that the industry was going to change and that existing business models were running into their natural diminishing returns.

We tried to bring some new ideas to the organizations we were working in, but we each had epiphany moments when we realized that big organizations weren’t built to do disruptive transformation — for bad reasons, but also good reasons, too.

GS: Let’s fast forward to today, where you have several strong Fintech VCs out there. But unlike others, Anthemis puts weirdness at the heart of its model.

Yes, you’ve backed some big names like Betterment and eToro, but you’ve done other things that are farther afield. What’s the underlying thesis that supports that?

Amy Nauiokas: Whatever we do at Anthemis has to be a non-zero-sum game. It has to be for good, not for evil. So that means that we aren’t looking in any place where you see predatory opportunities to make money.

Powered by WPeMatico

The Valley’s rocky history with cleantech investing has been well-documented.

Startups focused on non-emitting-generation resources were once lauded as the next big cash cow, but the sector’s hype quickly got away from reality.

Complex underlying science, severe capital intensity, slow-moving customers and high-cost business models outside the comfort zones of typical venture capital ultimately caused a swath of venture-backed companies and investors in the cleantech boom to fall flat.

Yet, decarbonization and sustainability are issues that only seem to grow more dire and more galvanizing for founders and investors by the day, and more company builders are searching for new ways to promote environmental resilience.

While funding for cleantech startups can be hard to find nowadays, over time we’ve seen cleantech startups shift down the stack away from hardware-focused generation plays toward vertical-focused downstream software.

A far cry from past waves of venture-backed energy startups, the downstream cleantech companies offered more familiar technology with more familiar business models, geared toward more recognizable verticals and end users. Now, investors from less traditional cleantech backgrounds are coming out of the woodwork to take a swing at the energy space.

An emerging group of non-traditional investors getting involved in the clean energy space are those traditionally focused on fintech, such as New York and Europe-based venture firm Anthemis — a financial services-focused team that recently sat down with our fintech contributor Gregg Schoenberg and I (check out the full meat of the conversation on Extra Crunch).

The tie between cleantech startups and fintech investors may seem tenuous at first thought. However, financial services have long played a significant role in the energy sector and is now becoming a more common end customer for energy startups focused on operations, management and analytics platforms, thus creating real opportunity for fintech investors to offer differentiated value.

Though the conversation around energy resources and decarbonization often focuses on politics, a significant portion of decisions made in the energy generation business is driven by pure economics — is it cheaper to run X resource relative to resources Y and Z at a given point in time? Based on bid prices for request for proposals (RFPs) in a specific market and the cost-competitiveness of certain resources, will a developer be able to hit their targeted rate of return if they build, buy or operate a certain type of generation asset?

Alternative generation sources like wind, solid oxide fuel cells or large-scale or even rooftop solar have reached more competitive cost levels — in many parts of the U.S., wind and solar are in fact often the cheapest form of generation for power providers to run.

Thus as renewable resources have grown more cost competitive, more infrastructure developers and other new entrants have been emptying their wallets to buy up or build renewable assets like large-scale solar or wind farms, with the American Council on Renewable Energy even forecasting cumulative private investment in renewable energy possibly reaching up to $1 trillion in the U.S. by 2030.

A major and swelling set of renewable energy sources are now led by financial types looking for tools and platforms to better understand the operating and financial performance of their assets, in order to better maximize their return profile in an increasingly competitive marketplace.

Therefore, fintech-focused venture firms with financial service pedigrees, like Anthemis, now find themselves in pole position when it comes to understanding cleantech startup customers, how they make purchase decisions, and what they’re looking for in a product.

In certain cases, fintech firms can even offer significant insight into shaping the efficacy of a product offering. For example, Anthemis portfolio company kWh Analytics provides a risk management and analytics platform for solar investors and operators that helps break down production, financial analysis and portfolio performance.

For platforms like kWh analytics, fintech-focused firms can better understand the value proposition offered and help platforms understand how their technology can mechanically influence rates of return or otherwise.

The financial service customers for clean energy-related platforms extends past just private equity firms. Platforms have been and are being built around energy trading, renewable energy financing (think financing for rooftop solar) or the surrounding insurance market for assets.

When speaking with several of Anthemis’ cleantech portfolio companies, founders emphasized the value of having a fintech investor on board that not only knows the customer in these cases, but that also has a deep understanding of the broader financial ecosystem that surrounds energy assets.

Founders and firms seem to be realizing that various arms of financial services are playing growing roles when it comes to the development and access to clean energy resources.

By offering platforms and surrounding infrastructure that can improve the ease of operations for the growing number of finance-driven operators or can improve the actual financial performance of energy resources, companies can influence the fight for environmental sustainability by accelerating the development and adoption of cleaner resources.

Ultimately, a massive number of energy decisions are made by financial services firms and fintech firms may often know the customers and products of downstream cleantech startups more than most. And while the financial services sector has often been labeled as dirty by some, the vital role it can play in the future of sustainable energy offers the industry a real chance to clean up its image.

Powered by WPeMatico

Europe has seen a large wave of startup banks pop up in the last few years — companies like N26, Atom and Monzo that are taking on the big incumbents by creating faster and cheaper services for a new class of consumers as they grow up and enter the working world. Now a startup has raised a sizeable Series A to tackle what it believes is a similar opportunity in the small business… Read More

Europe has seen a large wave of startup banks pop up in the last few years — companies like N26, Atom and Monzo that are taking on the big incumbents by creating faster and cheaper services for a new class of consumers as they grow up and enter the working world. Now a startup has raised a sizeable Series A to tackle what it believes is a similar opportunity in the small business… Read More

Powered by WPeMatico