Andrew Chen

Auto Added by WPeMatico

Auto Added by WPeMatico

Wildfires are burning in countries all around the world. California is dealing with some of the worst wildfires in its history (a superlative that I use essentially every year now) with the Caldor fire and others blazing in the state’s north. Meanwhile, Greece and other Mediterranean nations have been fighting fires for weeks to bring a number of massive blazes under control.

With the climate increasingly warming, millions of homes just in the United States alone are sitting in zones at high risk for wildfires. Insurance companies and governments are putting acute pressure on homeowners to invest more in defending their homes in what is typically dubbed “hardening,” or ensuring that if fires do arrive, a home has the best chance to survive and not spread the disaster further.

SF-based Firemaps has a bold vision for rapidly scaling up and solving the problem of home hardening by making a complicated and time-consuming process as simple as possible.

The company, which was founded just a few months ago (in March), sends out a crew with a drone to survey a homeowner’s house and property if it is in a high-risk fire zone. Within 20 minutes, the team will have generated a high-resolution 3D model of the property down to the centimeter. From there, hardening options are identified and bids are sent out to trade contractors to perform the work on the company’s marketplace.

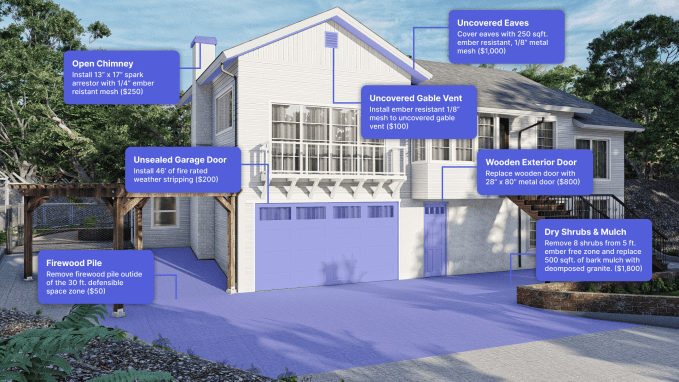

Once the drone scans a house, Firemaps can create a full CAD model of the structure and the nearby property. Image Credits: Firemaps.

While early, it’s already gotten traction. In addition to hundreds of homeowners who have signed up on its website and a few dozen that have been scanned, Andrew Chen of a16z has led a $5.5 million seed round into the business (the Form D places the round sometime around April). Uber CEO Dara Khosrowshahi and Addition’s Lee Fixel also participated.

Firemaps is led by Jahan Khanna, who co-founded it along with his brother, who has a long-time background in civil engineering, and Rob Moran. Khanna was co-founder and CTO of early ridesharing startup Sidecar, where Moran joined as one of the company’s first employees. The trio spent cycles exploring how to work on climate problems, while staying focused on helping people in the here and now. “We have crossed certain thresholds [with the climate] and we need to get this problem under control,” Khanna said. “We are one part of the solution.”

Over the past few years Khanna and his brother explored opening a solar farm or a solar-powered home in California. “What was wild, whenever we talked to someone, is they said you cannot build anything in California since it will burn down,” Khanna said. “What is kind of the endgame of this?” As they explored fire hardening, they realized that millions of homeowners needed faster and cheaper options, and they needed them sooner rather than later.

While there are dozens of options to harden a home to fire, some popular options include constructing an ember-free zone within a few feet of a home, often by placing gravel made of granite on the ground, as well as ensuring that attic vents, gutters and siding are fireproof and can withstand high temperatures. These options can vary widely in cost, although some local and state governments have created reimbursement programs to allow homeowners to recoup at least some of the expenses of these improvements.

A Firemaps house in 3D model form with typical hardening options and associated prices. Image Credits: Firemaps.

The company’s business model is simple: vetted contractors pay Firemaps to be listed as an option on its platform. Khanna believes that because its drone offers a comprehensive model of a home, contractors will be able to bid for contracts without doing their own site visits. “These contractors are getting these shovel-ready projects, and their acquisition costs are basically zero,” Khanna said.

Long-term, “our operating hypothesis is that building a platform and building these models of homes is inherently valuable,” Khanna said. Right now, the company is launched in California, and the goal for the next year is to “get this model repeatable and scalable and that means doing hundreds of homes per week,” he said.

Powered by WPeMatico

Buzzy live voice chat app Clubhouse has confirmed that it has raised new funding – without revealing how much – in a Series B round led by Andreessen Horowitz through the firm’s partner Andrew Chen. The app was reported to be raising at a $1 billion valuation in a report from The Information that landed just before this confirmation. While we try to track down the actual value of this round and the subsequent valuation of the company, what we do know is that Clubhouse has confirmed it will be introducing products to help creators on the platform get played, including subscriptions, tipping and ticket sales.

This funding round will also support a ‘Creator Grant Program’ being set up by Clubhouse, which will be used to “support emerging Clubhouse creators” according to the startup’s blog post. While the app has done a remarkable job attracting creator talent, including high-profile celebrity and political users, directing revenue towards creators will definitely help spur sustained interest, as well as more time and investment from new creators who are potentially looking to make a name for themselves on the platform, similar to YouTube and TikTok influencers before them.

Of course, adding monetization for users also introduces a method for Clubhouse itself to monetize. The platform is free to all users, and doesn’t yet offer any kind of premium plan or method of charging users, nor is it ad-supported. Adding ways for users to pay other users provides an opportunity for Clubhouse to retain a cut for its services.

The plans around monetization routes for creators appear to be relatively open-ended at this point, with Clubhouse saying it’ll be launching “first tests” around each of the three areas it mentions (tipping, tickets and subscriptions) over the “next few months.” It sounds like these could be similar to something like a Patreon built right into the platform. Tickets are a unique option that would go well with Clubhouse’s more formal roundtable discussions, and could also be a way that more organizations make use of the platform for hosting virtual events.

The startup also announced that it will be starting work on its Android app (it’s been iOS only for now) and that it will also invest in more backend scaling to keep up with demand, as well as support team growth and tools for detecting and prevuing abuse. Clubhouse has come under fire for its failure in regards to moderation and prevention of abuse in the past, so this aspect of its product development will likely be closely watched. The platform will also see changes to discovery aimed at surfacing relevant users, groups (‘clubs’ in the app’s parlance) and rooms.

During a regular virtual town hall the app’s founders host on the platform, CEO Paul Davison revealed that Clubhouse now has 2 million weekly active users. It’s also worth noting that Clubhouse says it now has “over 180 investors” in the company, which is a lot for a Series B – though many of those are likely small, independent investors with very little stake.

Powered by WPeMatico

Yes, the media f’ing gorged on the Quibi story yesterday. We did, they did, everyone did. And really, truly, how could anyone not? Nearly $2 billion came in (with $350 million heading back), a star-studded lineup of executives and production teams, an absolutely massive advertising campaign, and a PR strategy that all but begged the sun to melt Icarus’ wings.

Our collective exhalation on the complete clusterfuck that was Quibi though leads to a legitimate and interesting question: Are we obnoxiously attacking a good-faith failure? Wasn’t Quibi a bet just like every other startup, a bet that just happened to fail? A16Z’s general partner Andrew Chen put it vividly on Twitter, saying “It’s gross” and lauding the entrepreneurial challenge of building a startup:

all the people rushing to their keyboards to type in their “i told you so” hot takes on Quibi:

It’s gross. Building a company is hard, why celebrate a fail?

Go build something instead of using your energy to let twitter know how smart you are the say the consensus thing.

— Andrew Chen

(@andrewchen) October 22, 2020

I understand this view, deeply. In fact, all of us at TechCrunch understand this. One of the things that we pride ourselves on here is respecting the hustle. We know how hard it is to launch a startup. As a team, we collectively talk to thousands of founders every year, and we hear the heartbreaking stories and the downright trauma at times that comes with building a company. Occasionally (and yes, we focus most of our reporting here), we hear about the wins and successes too.

Let’s be honest: Most startups fail. Most ideas turn out wrong. Most entrepreneurs are never going to make it. That doesn’t mean no one should build a startup, or pursue their passions and dreams. When success happens, we like to talk about it, report on it and try to explain why it happens — because ultimately, more entrepreneurial success is good for all of us and helps to drive progress in our world.

But let’s also be clear that there are bad ideas, and then there are flagrantly bad ideas with billions in funding from smart people who otherwise should know better. Quibi wasn’t the spark of the proverbial college dropout with a passion for entertainment trying to invent a new format for mobile phones with ramen money from friends and family. Quibi was run by two of the most powerful and influential executives in the United States today, who raised more money for their project than other female founders have raised collectively this year.

Chen makes an important point that many obvious ideas in tech started as dumb ideas. That’s true! In fact, the history of technology is littered with examples of ideas that investors and the press thought were either dumb or impossible to build (which is a more polite way to say “dumb”).

for everyone who “obviously” knows when they see a bad idea in tech – everyone citing Quibi today – here’s a thread for you. https://t.co/QpXXKG16Vm

— Andrew Chen

Why do supposedly dumb ideas turn out to be smart? Part of the reason is that what starts out as dumb slowly iterates into something that is very smart. Facebook was just a “facebook” for checking out your classmates on college campuses. If it had ended there and withered away like many other social networks before it, we might well have put it in the waste bin of history. But Zuckerberg and his crew iterated — adding features like photos, a feed, messaging and more with an extreme focus on growth that made the product so much more than when it started.

We’ve seen this pattern again and again throughout time. Founders get feedback from users, they iterate, they pivot, they try new things and slowly but surely they start to migrate from what might have been a very raw concept to something much more ready to compete in the ferocious marketplace of business and consumer attention today.

This was never the story with Quibi. There was never an iteration of the product, or a long-range plan to assiduously cultivate users and talent as the company found traction while carefully husbanding its capital for the inevitable tough moments in the growth of any company.

Yes, we in the commentariat do make mistakes, but analysts weren’t dumb in pointing out all of Quibi’s glaring, red-alert flaws. Those analysts were smart. They were right. They might not be right next time, of course — no analyst should get too overconfident in their predictions. But at the same time, we shouldn’t just collectively throw up our hands and declare every idea that comes our way a brilliant gift from the heavens. Most ideas are dumb, and we and everyone else have every right to point that out.

So respect the hustle. Don’t kick a hardworking entrepreneur down who is just trying to get their project out there and show it the world. But that doesn’t mean you can’t call out stupid when you see it. The best entrepreneurs know that — even at its most vituperative — critical feedback is the necessary ingredient to startup success. Lauding everyone lauds no one.

Powered by WPeMatico

We recently invested in a team of co-founders who had voluntarily made their own vesting longer than four years. Four-year vesting is the industry standard. Why would someone voluntarily make it longer for themselves?

Their answer: “These days, with companies taking seven to 10 years to reach exit, it would make sense for founders to be on a similar schedule.”

This matters because the four-year co-founder vesting schedule frequently harms startup founders’ interests. Sometimes it damages their startup irreparably.

A growing number of founders are starting to realize this. I talked to quite a few about this over the last two years. Mostly, the “longer-than-four-years-

Importantly, this group of founders assumes they are going to be the ones actually building the company. They created the company. They are the company. Nobody is forcing them out. I suspect founders who already believe this about their own startup will find this post most helpful.

Given the massive implications of co-founder vesting schedules, all startup founders should consider co-founder vesting lengths more carefully and then choose what makes sense for them. You make this decision around the time of incorporation but feel the effects over the lifetime of your company.

As far back as the 1980s, the standard startup vesting schedule was four or five years, with five being more prevalent on the East Coast. Nobody seems to remember a time it was anything different. The closest I’ve gotten to a logical answer on why it’s four years today stretches back to a pre-401(k) era, from before Reagan’s tax reforms in the ’80s. Prior to then, tax rules incentivized big company pension plans to have vesting periods of at least five years.

Startups didn’t offer traditional pension plans. Instead, startups offered employees stock, vesting over four years instead of five as a competitive move. That is all moot today. It has no relevance for startup founders in 2020.

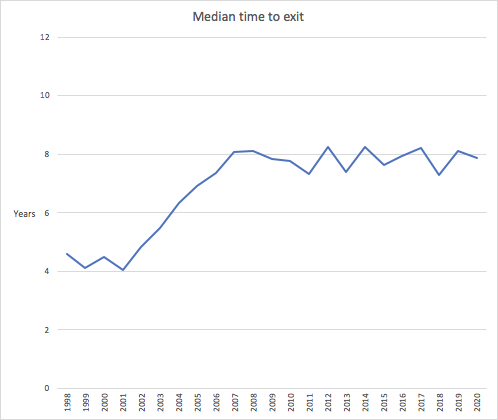

More relevantly, time from founding to exit has gone from four years in 1999 to eight years in 2020. Yet founder vesting remains stuck at four. This is dangerous.

Exit data from U.S. startups with minimum $1 million in venture funding. Image Credits: PitchBook

Powered by WPeMatico

At TechCrunch Disrupt, the original tech startup conference, venture capitalists remain amongst the premier guests.

VCs are responsible for helping startups — the focus of the three-day event — get off the ground, and, as such, they are often the most familiar with trends in the startup ecosystem, ready to deliver insights, anecdotes and advice to our audience of entrepreneurs, investors, operators, managers and more.

In the first half of 2019, VCs spent $66 billion purchasing equity in promising upstarts, according to the latest data from PitchBook. At that pace, VC spending could surpass $100 billion for the second year in a row. We plan to welcome a slew of investors to TechCrunch Disrupt to discuss this major feat and the investing trends that have paved the way for recording funding.

Mega-funds and the promise of unicorn initial public offerings continue to drive investment. SoftBank, of course, began raising its second Vision Fund this year, a vehicle expected to exceed $100 billion. Meanwhile, more traditional VC outfits revisited limited partners to stay competitive with the Japanese telecom giant. Andreessen Horowitz, for example, collected $2.75 billion for two new funds earlier this year. We’ll have a16z general partners Chris Dixon, Angela Strange and Andrew Chen at Disrupt for insight into the firm’s latest activity.

At the early-stage, the fight for seed deals continued, with larger funds moving downstream to muscle their way into seed and Series A financings. Pre-seed has risen to prominence, with new funds from Afore Capital and Bee Partners helping to legitimize the stage. Bolstering the early-stage further, Y Combinator admitted more than 400 companies across its two most recent batches,

We’ll welcome pre-seed and seed investor Charles Hudson of Precursor Ventures and Redpoint Ventures general partner Annie Kadavy to give founders tips on how to raise VC. Plus, Y Combinator CEO Michael Seibel and Ali Rowghani, the CEO of YC’s Continuity Fund, which invests in and advises growth-stage startups, will join us on the Disrupt Extra Crunch stage ready with tips on how to get accepted to the respected accelerator.

Moreover, activity in high-growth sectors, particularly enterprise SaaS, has permitted a series of outsized rounds across all stages of financing. Speaking on this trend, we’ll have AppDynamics founder and Unusual Ventures co-founder Jyoti Bansal and Battery Ventures general partner Neeraj Agrawal in conversation with TechCrunch’s enterprise reporter Ron Miller.

We would be remiss not to analyze activity on Wall Street in 2019, too. As top venture funds refueled with new capital, Silicon Valley’s favorite unicorns completed highly anticipated IPOs, a critical step toward bringing a much needed bout of liquidity to their investors. Uber, Lyft, Pinterest, Zoom, PagerDuty, Slack and several others went public this year, and other well-financed companies, including Peloton, Postmates and WeWork, have completed paperwork for upcoming public listings. To detail this year’s venture activity and IPO extravaganza, David Krane, CEO and managing partner of Uber and Slack investor GV, will be on deck, as will Sequoia general partner Jess Lee, Floodgate’s Ann Miura-Ko and Aspect Ventures’ Theresia Gouw.

There’s more where that came from. In addition to the VCs already named, Disrupt attendees can expect to hear from Bessemer Venture Partners’ Tess Hatch, who will provide her expertise on the growing “space economy.” Forerunner Ventures’ Eurie Kim will give the Extra Crunch Stage audience tips on building a subscription product, Mithril Capital’s Ajay Royan will explore opportunities in the medical robotics field and SOSV’s Arvind Gupta will dive deep into the cutting-edge world of health tech and more.

Disrupt SF runs October 2-4 at the Moscone Center in the heart of San Francisco. Passes are available here.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about the flurry of IPO filings. Before that, I noted the differences between raising cash from angels vs. traditional venture capitalists.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

Venture capitalists look for companies poised to disrupt markets untouched by innovative technology. Believe it or not, a very small percentage of jewelry shopping is done online, which means there’s a big opportunity — for the right team — to bring jewelry buyers and sellers to the 21st century.

Enter Pietra, a new startup that’s just raised $4 million in a round led by Andreessen Horowitz’s Andrew Chen (Substack & Hipcamp investor). Robert Downey Jr.’s VC fund Downey Ventures and Will Smith’s fund Dreamers Fund also participated, as did Hollywood manager Scooter Braun, Michael Ovitz and supermodel Joan Smalls.

I spoke to the founding team, which includes Uber alum Ronak Trivedi and Ashley Bryan, who hails from fashion e-commerce site Moda Operandi. The pair bring a healthy mix of technology and fashion expertise to the mix. Trivedi tells TechCrunch he’s drawn on his Uber experience to recruit engineers from top tech companies and to advocate for fast growth. Meanwhile, Bryan has leveraged her fashion industry connections to establish relationships with luxury designers.

“Fashion is typically really under-resourced in terms of tech,” Bryan tells TechCrunch. “[The fashion industry] is great at the creativity part but it’s tough, especially with jewelry because you really have to put up a lot of capital.”

Pietra’s plan is to create a high-end marketplace for consumers to connect with jewelry designers. To do this, the team has adopted the standard marketplace approach, taking a 30% marketplace fee from sellers, as well as a 7% fee from buyers commissioning jewelry on the platform.

“Whether you do custom jewelry or engagement jewelry or you do jewelry for celebrities like Drake, you can come on Pietra and connect with a global marketplace,” says Trivedi.

The jewelry market is expected to be worth more than $250 billion by 2020, according to McKinsey research. And where there’s a billion-dollar market, there are VCs.

“Even though gemstones and jewelry have been at the center of art, commerce, and culture since the dawn of human civilization — going from stone jewelry created 40,000 years ago in Africa to the trade routes between East and West to Fifth Avenue in New York to the Instagram feed on your phone — the technology for discovering, designing, and purchasing jewelry online hasn’t evolved much at all,” writes a16z’s Chen, who overlapped with Trivedi during his Uber tenure.

Pietra completed its official launch this week. It has 100 designers on the platform and counting, along with what the founders say is a lengthy waitlist.

This week I published a long feature on the state of seed investing in the Bay Area. The TL;DR? Mega-funds are increasingly battling seed-stage investors for access to the hottest companies. As a result, seed investors are getting a little more creative about how they source deals. It’s a dog-eat-dog world out there and everyone wants a stake in The Next Big Thing. Read the story here.

Y Combinator graduated another batch of 200 companies this week. We were there both days, taking notes on each and every company. To make things easy on you, I’ve put together the ultimate YC reading list:

Here’s a look at some of the profiles we’ve written on the S19 companies:

We recorded two great episodes of Equity, TechCrunch’s venture capital podcast, this week. The first was with YC CEO Michael Seibel, in which he speaks to trends at the seed stage of investing, changes at the accelerator program, including its move to San Francisco and more. You can listen to that one here. Plus, we had on Unusual Ventures co-founder and partner John Vrionis, who talked to us about direct listings versus IPOs and the future of DoorDash and Airbnb. You can listen to that one here.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast and Spotify.

Contributors Tyler Elliston and Kevin Barry share advice for B2B companies: “Over the years, we’ve seen a lot of B2B companies apply ineffective demand generation strategies to their startup. If you’re a B2B founder trying to grow your business, this guide is for you. Rule #1: B2B is not B2C. We are often dealing with considered purchases, multiple stakeholders, long decision cycles, and massive LTVs. These unique attributes matter when developing a growth strategy. We’ll share B2B best practices we’ve employed while working with awesome B2B companies like Zenefits, Crunchbase, Segment, OnDeck, Yelp, Kabbage, Farmers Business Network, and many more.” Read the full story here. (Extra Crunch membership required.)

Powered by WPeMatico

The last few decades have produced many successful marketplaces. We went from goods marketplace pioneers such as eBay and Amazon to simple service marketplaces such as Uber, Lyft, Doordash, Upwork, Thumbtack, TaskRabbit, and Fiverr. But why haven’t we seen many successful B2B service marketplaces?

Some would argue that companies such as Upwork, Thumbtack, Fiverr, or TaskRabbit are horizontal B2B marketplaces in the sense that they provide access to suppliers of different services. But while businesses do indeed transact with freelancers on such “horizontal” marketplaces, for most service verticals these are limited-value, one-off transactions. They fail to enable long-term business collaborations.

So, such marketplaces haven’t delivered more valuable services nor introduced a new paradigm for how businesses buy specific services at scale and on an on-going basis. Why is that?

Horizontal services marketplaces don’t provide much value beyond matching clients with quality service providers. In other words, they don’t facilitate collaboration between buyers and suppliers, never mind provide ways for the two parties to collaborate more efficiently over time as they engage in follow-on projects.

In essence, the model these marketplaces were built around is not much different from the likes of Craigslist, which put a convenient UX on traditional classified advertisements.

In their article “What’s Next for Marketplace Startups?,” Andrew Chen and Li Jin found that there aren’t many successful service marketplaces because those offerings are complex, diverse, and difficult to evaluate. It’s challenging to define a successful transaction in a service marketplace because it’s harder to quantify success.

One reason is that several service providers must often work together to complete a single job for a buyer, requiring a complex workflow from end to end. As a result, it’s difficult for marketplaces to not only mediate service delivery but also make it significantly more efficient for buyers and suppliers. If both the buyer and suppliers don’t see a significant efficiency gain other than being initially matched, why would they continue using the marketplace?

(Image via Getty Images / Lidiia Moor)

The $50 billion translation industry is a prime example of complex B2B services marketplaces. On the supply side are roughly 50,000 small agencies around the globe responsible for more than 85% of this $50 billion industry. (Note we are referring to agencies here as suppliers, though they play on both sides.)

On the demand side are businesses that need to translate text from one language into another. Plus about 1,500,000 freelance linguists work in this industry, many of whom are more specialized than professionals in other industries.

Anyone can find and hire a translator on Fiverr or Upwork. Both provide a vast selection of language translators. However, the quality and cost of the translation depends on the translation tools available to the translator as well as their subject expertise.

Neither Fiverr nor Upwork provide computer-aided translation (CAT) and collaborative workflow solutions for users of their platforms. Additionally, neither provides an effective way for all parties to collaborate and continuously improve the efficiency and quality.

But the problem with traditional marketplaces goes even further: Multiple translators and reviewers are usually needed to complete a single job for a customer. Multi-language translation projects are even more complicated. Such projects require multiple service providers and cost estimates, in addition to project management tools.

This is why building a B2B service marketplace is difficult. Service marketplaces must not only connect buyers and suppliers, but also provide tools to enable an efficient and collaborative workflow that reduces wasted time and effort.

In addition to the problems already outlined, traditional marketplaces experience another issue that prevents them from growing and retaining market participants: Buyer and supplier attrition.

Many business services are based on regularly recurring engagements. In some cases, a buyer and a service provider interact daily, requiring a different workflow than gig-marketplaces are built around.

Buyers and suppliers have little motivation to continue interacting on a platform with no workflow automation solutions. They lack a way to improve service efficiency and quality, automate collaboration, payment, paperwork, and other basic processes required for a business.

This is why many traditional marketplaces suffer from slow network effects and high attrition. (A network effect is what happens when a platform, product, or service delivers more value the more it is used.

Think Facebook, eBay, WhatsApp.) Why wouldn’t companies work directly with service providers outside of a marketplace after they were introduced? What incentives keep the service transaction on the marketplace? These are critical questions to answer when building a marketplace.

Traditional marketplaces target broad services, making it nearly impossible to provide workflow solutions for buyers and suppliers. Going forward, successful service marketplaces will be developed relying on an industry-specific SaaS workflow. This will focus buyers and suppliers on longer-term projects and interactions that serve the unique needs of collaborations and transactions in a specific vertical.

Image via Getty Images / OstapenkoOlena

In “The next 10 Years Will Be About Market Networks,” James Currier, Managing Partner at NFX Ventures, defines a new era of service marketplaces, which he calls market networks.

A market network is a platform that combines elements of an n-sided marketplace, a network, and workflow solutions. An n-sided marketplace is one that requires coordination of multiple supply-side parties to provide a complex service for a single buyer.

Market networks enable multiple buyers and suppliers to interact, collaborate, and transact on the same platform. They provide users with industry-specific workflow solutions that enable efficient, ongoing collaboration on long-term projects. This reduces costs and leads to a higher quality of services and increased overall value for all users.

But how do you actually build a successful market-network platform? While the answer to that varies from company to company, here is our approach. We were able to build a market network for the translation industry that combines the components: network, marketplace, and workflow solution.

The first step to building an effective complex market network is to develop a workflow that is easy for users to embrace. It might not seem like much, but this increases productivity by enabling teams to perform tasks that were previously impossible.

Powered by WPeMatico