Andreessen Horowitz

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to this week’s transcribed edition of Equity.

This week, TechCrunch’s Danny Crichton filled in for co-host Alex Wilhelm – who was out in preparation for his wedding this weekend – joining Kate to cover the big news of the week.

Kate and Danny dive straight into Slack’s IPO and the implications of its direct listing strategy, before shifting gears to discuss the launch of Facebook’s new ‘Libra’ cryptocurrency and the VCs backing the initiative.

The duo then took a look at Lime’s latest fundraising efforts and the potential headwinds facing scooter companies with an appetite for capital. Lastly, Kate and Danny talk about underappreciated tensions for founders, including getting pushed out of their own companies and handling their own salaries.

Crichton: Talking about founders and compensation, our correspondent, Ron Miller, talked to a bunch of VCs to ask how are founders paying themselves today? Obviously, the cost of living in the Bay Area, in New York and other startup hubs has increased dramatically. So VCs have had to become acutely aware of their founders’ financial means.

One of the things that really came out of this survey though, from my perspective, was just how high the numbers are. We surveyed small number. We put it out in the interviews. It came out to post-Series A people are starting to get paid around 200K. But the numbers, even a couple of years ago, I seem to recall was like $120 was the magic number around the Series A, $90K if you had a serious seed fund and like $60 to $80 if you are just getting started.

But the numbers that we saw out of this were significantly higher. I think that shows a lot about how the cost of living has just continued to creep up in San Francisco and in New York.

Clark: Yeah. I think the point is made in the story. If you live in San Francisco and you’re paying a mortgage and you have kids, of course, you need to make six figures really to get by, which is just an unfortunate reality. I can’t say I was surprised by how those salaries looked. Seeing $125K for a founder, if anything, I thought was maybe a little low.

But it reminded me of, nearly a year ago at this point, when I wrote something on how much VCs are paid. I had written it based off data that was provided to me from a consulting firm. People were just up in arms at what I had written because, and I understand looking back, I think it grouped VCs together as VCs who work at really big funds who are getting the 2% carry out of a multi-billion dollar fund and who are paid a lot more.

And there are of course VCs who run seed funds or any kind of fund. There are many different sizes of VC funds. Some VCs actually don’t have a salary at all and are up against the same challenges, if not even more difficult challenges, of a startup founder.

Want more Extra Crunch? Need to read this entire transcript? Then become a member. You can learn more and try it for free.

Kate Clark: Hello, and welcome back to Equity, TechCrunch’s venture capital-focused podcast. My co-host, Alex, is getting married this weekend so he’s not with us today, unfortunately. But we’ve got TechCrunch editor, Danny Crichton on the line. Danny, how are you?

Powered by WPeMatico

Slack, the popular workplace messaging company, is expected to list on the New York Stock Exchange on Thursday in the second major direct listing in the U.S. after Spotify introduced the concept to investors in April of last year.

At this point, plenty of industry observers think it makes sound sense for Slack to embrace the direct listing approach, wherein a company places its stock on a public exchange without raising any money or using underwriters. Though the company warned last week that its operating losses are widening as it chases new customers, it has $800 million on its balance sheet, meaning it doesn’t need to raise more right now.

Slack also doesn’t need underwriters who typically discount a company’s shares in order to ensure that they appreciate in value when they begin trading. It’s a known brand in the tech world, and that universe is broadening by the day. Put another way, Slack doesn’t need to be “sold” for investors to want to snap up its shares.

Still, we wondered about some of the thinking that has gone into preparing Slack for its move into the world of publicly traded companies, so we talked with a couple of people who are familiar with what’s happening behind the scenes to find out more. They asked not to be named, but here’s what we learned:

1) Unlike with the popular streaming music platform Spotify, which has more than 100 million premium subscribers and roughly twice as many active monthly users, Slack wasn’t as well-known to Wall Street as Silicon Valley might imagine. In fact, we’re told the bankers that were selected to advise Slack on its offering — Morgan Stanley, Goldman Sachs and Allen & Co., which are the same three that advised Spotify — had to provide more education to analysts and institutional investors this time around.

2) There will (hopefully) be enough shares to go around, while also not a glut of them. The big concern in a direct offering — which does not feature a lock-up period — is that too many people will dump their shares on the market, crushing the company’s share price, or else that too few will part with their holdings, turning the buying and selling of the company’s shares into a financial game of chicken. We’ll see what happens here, but we’re told the banks have spent the last six months trying to ensure that many — but not all — of the company’s institutional shareholders will be selling some of their stakes at the offering, Also worth noting is that unlike with Spotify, some Slack employees have restricted stock units that will vest upon its public listing and so be part of the supply of shares on its first day.

3) In establishing guidance around how Spotify’s shares should be valued, the banks advising the company looked almost entirely to its private market trades, of which there were many. There has been less secondary activity with Slack’s shares, so the banks are likely to rely on these sales but also to use other inputs. We’ll learn soon enough what they settle on, but based on the latest prices at which its shares have traded in the private market, Slack’s presumed valued right now is at $16.7 billion, or 36 times trailing 12-month sales.

4) You might imagine that banks hate direct listings because of the rich underwriting fees they aren’t collecting, and they probably do. Still, even with a direct listing, they get paid pretty well, thanks to both advisory fees and also because investors often trade through the banks named as advisers in the prospectus. There are also fewer mouths to feed on a deal with a direct listing. In Slack’s case — as happened with Spotify — Morgan Stanley, Goldman Sachs and Allen & Co. will reportedly reap almost all of the spoils — or a reported 90% of the $22 million in fees earmarked for all the advisers involved in the deal. In a traditional IPO, a longer number of banks that promise research coverage are given shares to sell, which eats into lead underwriters’ allotment.

5) One risk that Slack shouldn’t necessarily run into but that may have adversely impacted Uber’s IPO is its investor base. According to Slack’s S-1, its biggest outside shareholders include Accel (it owns 24% sailing into the offering), Andreessen Horowitz (13.3%), Social Capital (10.2%) and SoftBank (7.3 %). Why it matters: Slack doesn’t have to worry about less traditional private company backers like mutual funds not wanting to buy up its shares because they’re too busy trying to offload some.

6) Direct listings may well become a more popular product for consumer companies because companies can avoid further dilution, and there’s no lock-up on their shares, creating a shorter path to liquidity for the company and its employees and its investors. Still, Slack is probably anomalous as an enterprise company with a high enough profile to pull one off. The listings are really for companies that don’t need money any time soon and whose shares are already of interest to investors, who don’t need inducements to pay attention.

7) This is the second direct listing of a highly valued privately held company and, for the second time, it’s happening on the NYSE, with the same market maker, Citadel Securities, charged with ensuring orderly trading; the same bank, Morgan Stanley, selected to advise Citadel; and even the same law firms that worked on Spotify’s direct listing pulled back into service.

It’s nice if you’re part of this particular club, and no one can blame Slack for not wanting to reinvent the wheel. But one wonders how nervous it makes Nasdaq, as well as other banks and law firms, to be shut out of this process a second time.

Powered by WPeMatico

William Hockey, co-founder, chief technology officer and president of the fast-growing fintech business Plaid, will step down next week, TechCrunch has learned.

The former Bain associate (pictured above left) co-founded the startup in 2012 alongside chief executive officer Zach Perret. Today, the San Francisco-based company employs 300 with additional offices in Salt Lake City and New York.

Plaid has confirmed the news, stating that Hockey will remain on the company’s board of directors.

“This conclusion was neither a rash nor a recent decision,” Hockey writes in a blog post shared with TechCrunch. “Over the past couple of years, I have known that there would come a point at which I would choose to move to a purely strategic and advisorial role.”

Most companies should be constantly running running at least one exec search. Post-product/market fit, the limiting factor to scale generally derives from some version of not having enough great leaders.

— Zachary Perret (@zachperret) June 18, 2019

Plaid builds infrastructure that allows consumers to interact with their bank account on the web, powering a number of third-party applications, like Venmo, Robinhood, Coinbase, Acorns and LendingClub. It rose to prominence recently, closing a $250 million Series C investment at a $2.65 billion valuation late last year. The deal was led by famed venture capitalist and author of the Internet Trends report Mary Meeker, who’s joined the startup’s board of directors.

In total, Plaid has secured $310 million in venture capital funding from Andreessen Horowitz, Index Ventures, Norwest Venture Partners, Coatue Management, Goldman Sachs, NEA, Spark Capital and others.

Plaid has integrated with 15,000 banks in the U.S. and Canada and says 25% of people living in those countries with bank accounts have linked with Plaid through at least one of the hundreds of apps that leverage Plaid’s application program interfaces (APIs) — an increase from 13% last year. Last month, the company launched its fintech platform in the U.K.

“As we’ve done in the U.S., Plaid will become the foundation for that growth by providing access to a financial network that allows developers to deliver the experience users expect from their financial apps,” the company wrote in a blog post.

TechCrunch participated in a panel discussion with Hockey and Brex CEO Henrique Dubugras last month, in which Hockey gave no indication of impending plans to leave the business. In fact, taking off just as Plaid amps up its global expansion efforts and accelerates growth is strange timing for a founder to depart.

Oftentimes, when a startup co-founder steps down from the C-suite, it’s to make room for a more experienced executive to lead the company through periods of fast growth. Recently, for example, Lime announced its co-founder Toby Sun would transition out of the CEO role to focus on company culture and R&D. Brad Bao, a Lime co-founder and longtime Tencent executive, assumed chief responsibilities.

Other times, it comes amid turmoil. Mike Cagney’s departure from SoFi, of course, is an example of this. One month after reports of a sexual harassment and wrongful termination lawsuit against the online lending business surfaced, SoFi announced Cagney would step down.

In Hockey’s case, the move was planned and calculated, he said. Plaid chief operating officer Eric Sager, who joined earlier this year, Perret and other executives will take over engineering and product reports, among Hockey’s other responsibilities.

“In tech, it has historically been taboo to talk about founders or executives transitioning to different roles inside companies,” Hockey writes. “Leadership transitions need to become a bedrock of any company that desires to endure across decades.”

Powered by WPeMatico

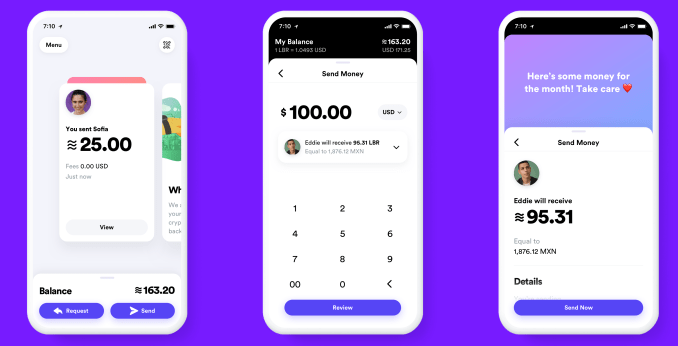

Facebook has finally revealed the details of its cryptocurrency, Libra, which will let you buy things or send money to people with nearly zero fees. You’ll pseudonymously buy or cash out your Libra online or at local exchange points like grocery stores, and spend it using interoperable third-party wallet apps or Facebook’s own Calibra wallet that will be built into WhatsApp, Messenger and its own app. Today Facebook released its white paper explaining Libra and its testnet for working out the kinks of its blockchain system before a public launch in the first half of 2020.

Facebook won’t fully control Libra, but instead get just a single vote in its governance like other founding members of the Libra Association, including Visa, Uber and Andreessen Horowitz, which have invested at least $10 million each into the project’s operations. The association will promote the open-sourced Libra Blockchain and developer platform with its own Move programming language, plus sign up businesses to accept Libra for payment and even give customers discounts or rewards.

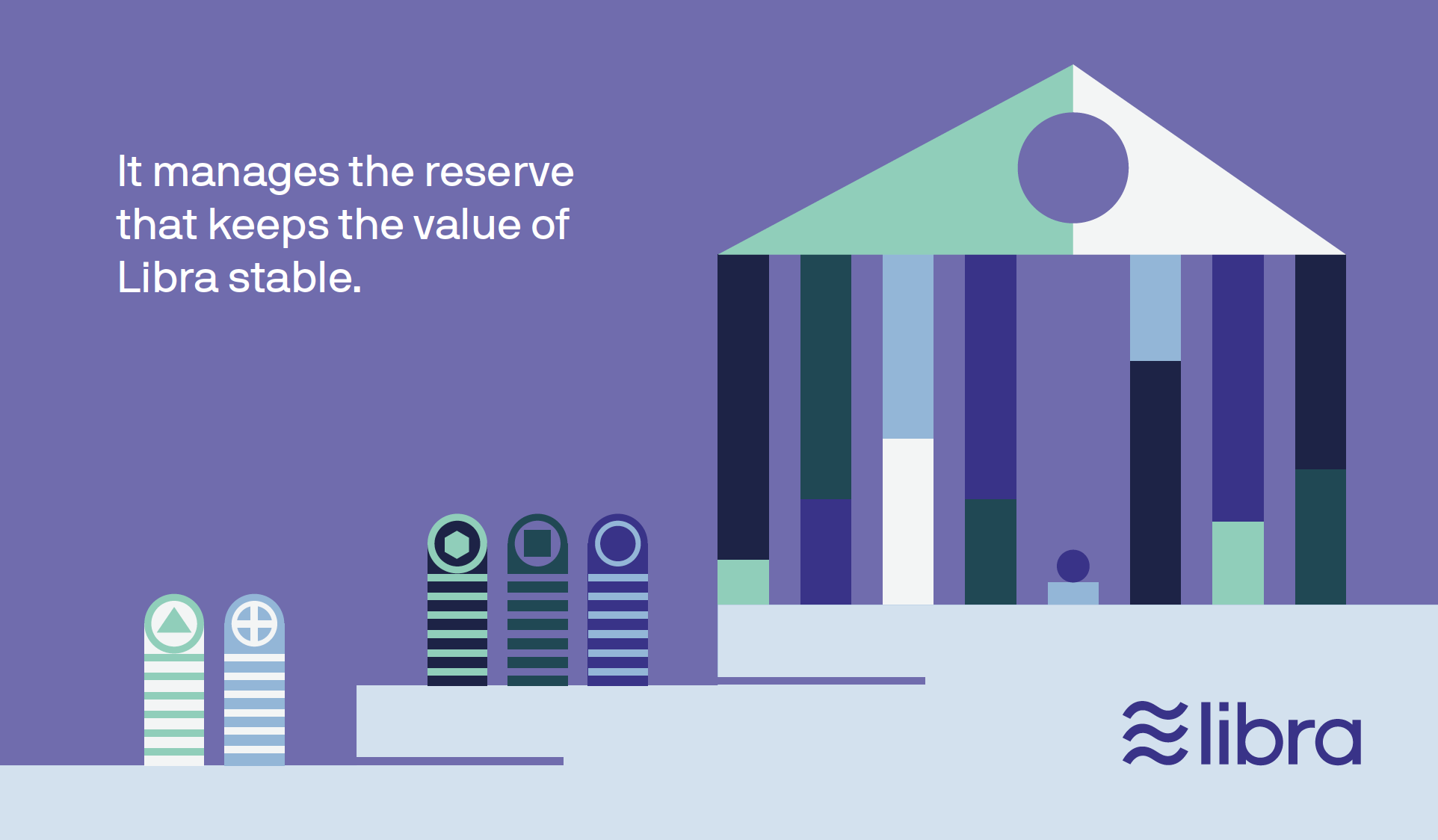

Facebook is launching a subsidiary company also called Calibra that handles its crypto dealings and protects users’ privacy by never mingling your Libra payments with your Facebook data so it can’t be used for ad targeting. Your real identity won’t be tied to your publicly visible transactions. But Facebook/Calibra and other founding members of the Libra Association will earn interest on the money users cash in that is held in reserve to keep the value of Libra stable.

Facebook’s audacious bid to create a global digital currency that promotes financial inclusion for the unbanked actually has more privacy and decentralization built in than many expected. Instead of trying to dominate Libra’s future or squeeze tons of cash out of it immediately, Facebook is instead playing the long-game by pulling payments into its online domain. Facebook’s VP of blockchain, David Marcus, explained the company’s motive and the tie-in with its core revenue source during a briefing at San Francisco’s historic Mint building. “If more commerce happens, then more small businesses will sell more on and off platform, and they’ll want to buy more ads on the platform so it will be good for our ads business.”

In cryptocurrencies, Facebook saw both a threat and an opportunity. They held the promise of disrupting how things are bought and sold by eliminating transaction fees common with credit cards. That comes dangerously close to Facebook’s ad business that influences what is bought and sold. If a competitor like Google or an upstart built a popular coin and could monitor the transactions, they’d learn what people buy and could muscle in on the billions spent on Facebook marketing. Meanwhile, the 1.7 billion people who lack a bank account might choose whoever offers them a financial services alternative as their online identity provider too. That’s another thing Facebook wants to be.

Yet existing cryptocurrencies like Bitcoin and Ethereum weren’t properly engineered to scale to be a medium of exchange. Their unanchored price was susceptible to huge and unpredictable swings, making it tough for merchants to accept as payment. And cryptocurrencies miss out on much of their potential beyond speculation unless there are enough places that will take them instead of dollars, and the experience of buying and spending them is easy enough for a mainstream audience. But with Facebook’s relationship with 7 million advertisers and 90 million small businesses plus its user experience prowess, it was well-poised to tackle this juggernaut of a problem.

Now Facebook wants to make Libra the evolution of PayPal . It’s hoping Libra will become simpler to set up, more ubiquitous as a payment method, more efficient with fewer fees, more accessible to the unbanked, more flexible thanks to developers and more long-lasting through decentralization.

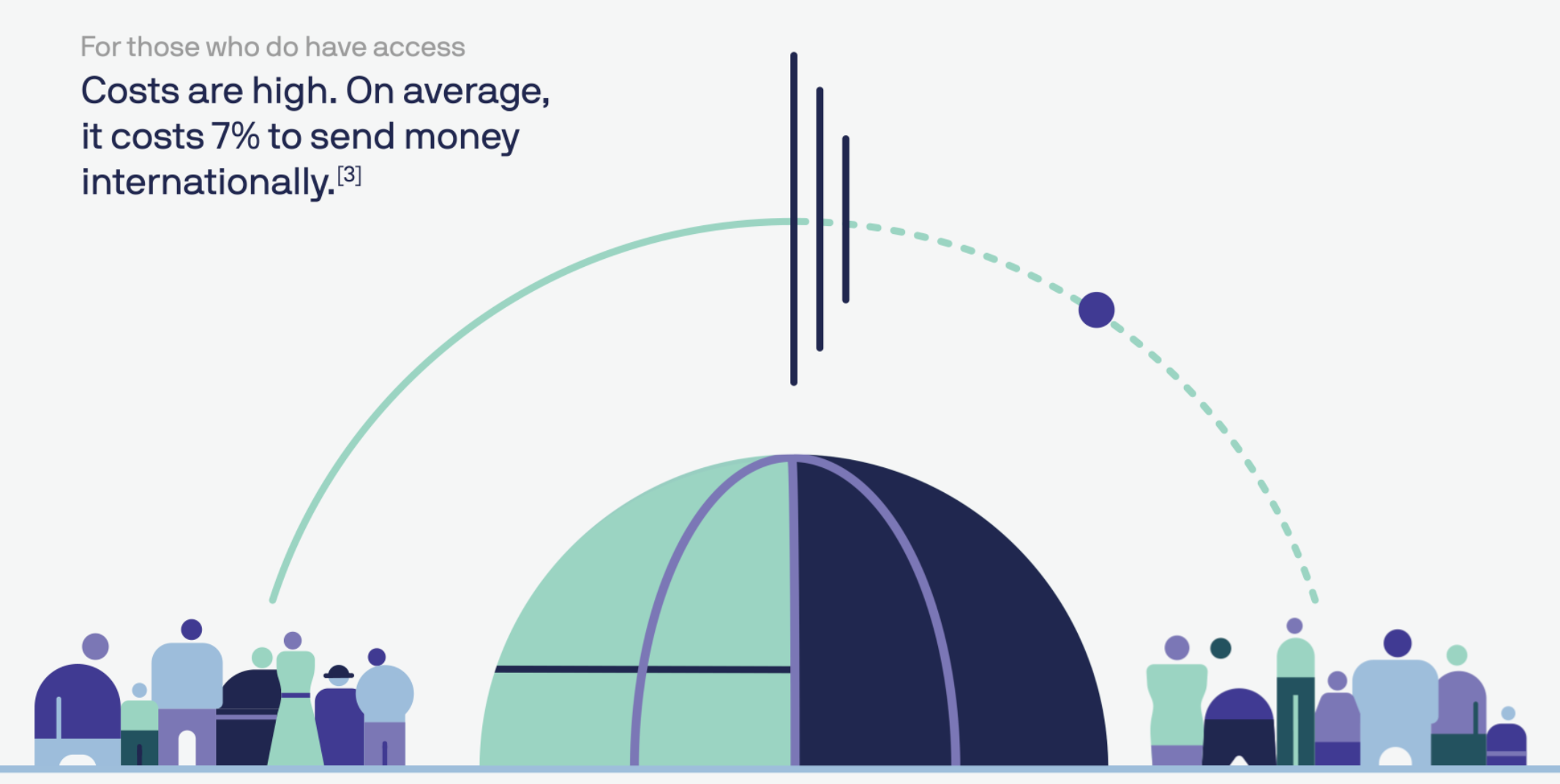

“Success will mean that a person working abroad has a fast and simple way to send money to family back home, and a college student can pay their rent as easily as they can buy a coffee,” Facebook writes in its Libra documentation. That would be a big improvement on today, when you’re stuck paying rent in insecure checks while exploitative remittance services charge an average of 7% to send money abroad, taking $50 billion from users annually. Libra could also power tiny microtransactions worth just a few cents that are infeasible with credit card fees attached, or replace your pre-paid transit pass.

…Or it could be globally ignored by consumers who see it as too much hassle for too little reward, or too unfamiliar and limited in use to pull them into the modern financial landscape. Facebook has built a reputation for over-engineered, underused products. It will need all the help it can get if wants to replace what’s already in our pockets.

By now you know the basics of Libra. Cash in a local currency, get Libra, spend them like dollars without big transaction fees or your real name attached, cash them out whenever you want. Feel free to stop reading and share this article if that’s all you care about. But the underlying technology, the association that governs it, the wallets you’ll use and the way payments work all have a huge amount of fascinating detail to them. Facebook has released more than 100 pages of documentation on Libra and Calibra, and we’ve pulled out the most important facts. Let’s dive in.

Facebook knew people wouldn’t trust it to wholly steer the cryptocurrency they use, and it also wanted help to spur adoption. So the social network recruited the founding members of the Libra Association, a not-for-profit which oversees the development of the token, the reserve of real-world assets that gives it value and the governance rules of the blockchain. “If we were controlling it, very few people would want to jump on and make it theirs,” says Marcus.

Each founding member paid a minimum of $10 million to join and optionally become a validator node operator (more on that later), gain one vote in the Libra Association council and be entitled to a share (proportionate to their investment) of the dividends from interest earned on the Libra reserve into which users pay fiat currency to receive Libra.

The 28 soon-to-be founding members of the association and their industries, previously reported by The Block’s Frank Chaparro, include:

Facebook says it hopes to reach 100 founding members before the official Libra launch and it’s open to anyone that meets the requirements, including direct competitors like Google or Twitter. The Libra Association is based in Geneva, Switzerland and will meet biannually. The country was chosen for its neutral status and strong support for financial innovation including blockchain technology.

To join the association, members must have a half rack of server space, a 100Mbps or above dedicated internet connection, a full-time site reliability engineer and enterprise-grade security. Businesses must hit two of three thresholds of a $1 billion USD market value or $500 million in customer balances, reach 20 million people a year and/or be recognized as a top 100 industry leader by a group like Interbrand Global or the S&P.

Crypto-focused investors must have more than $1 billion in assets under management, while Blockchain businesses must have been in business for a year, have enterprise-grade security and privacy and custody or staking greater than $100 million in assets. And only up to one-third of founding members can by crypto-related businesses or individually invited exceptions. Facebook also accepts research organizations like universities, and nonprofits fulfilling three of four qualities, including working on financial inclusion for more than five years, multi-national reach to lots of users, a top 100 designation by Charity Navigator or something like it and/or $50 million in budget.

The Libra Association will be responsible for recruiting more founding members to act as validator nodes for the blockchain, fundraising to jump-start the ecosystem, designing incentive programs to reward early adopters and doling out social impact grants. A council with a representative from each member will help choose the association’s managing director, who will appoint an executive team and elect a board of five to 19 top representatives.

Each member, including Facebook/Calibra, will only get up to one vote or 1% of the total vote (whichever is larger) in the Libra Association council. This provides a level of decentralization that protects against Facebook or any other player hijacking Libra for its own gain. By avoiding sole ownership and dominion over Libra, Facebook could avoid extra scrutiny from regulators who are already investigating it for a sea of privacy abuses as well as potentially anti-competitive behavior. In an attempt to preempt criticism from lawmakers, the Libra Association writes, “We welcome public inquiry and accountability. We are committed to a dialogue with regulators and policymakers. We share policymakers’ interest in the ongoing stability of national currencies.”

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

The name Libra comes from the word for a Roman unit of weight measure. It’s trying to invoke a sense of financial freedom by playing on the French stem “Lib,” meaning free.

The Libra Association is still hammering out the exact start value for the Libra, but it’s meant to be somewhere close to the value of a dollar, euro or pound so it’s easy to conceptualize. That way, a gallon of milk in the U.S. might cost 3 to 4 Libra, similar but not exactly the same as with dollars.

The idea is that you’ll cash in some money and keep a balance of Libra that you can spend at accepting merchants and online services. You’ll be able to trade in your local currency for Libra and vice versa through certain wallet apps, including Facebook’s Calibra, third-party wallet apps and local resellers like convenience or grocery stores where people already go to top-up their mobile data plan.

Each time someone cashes in a dollar or their respective local currency, that money goes into the Libra Reserve and an equivalent value of Libra is minted and doled out to that person. If someone cashes out from the Libra Association, the Libra they give back are destroyed/burned and they receive the equivalent value in their local currency back. That means there’s always 100% of the value of the Libra in circulation, collateralized with real-world assets in the Libra Reserve. It never runs fractional. And unliked “pegged” stable coins that are tied to a single currency like the USD, Libra maintains its own value — though that should cash out to roughly the same amount of a given currency over time.

When Libra Association members join and pay their $10 million minimum, they receive Libra Investment Tokens. Their share of the total tokens translates into the proportion of the dividend they earn off of interest on assets in the reserve. Those dividends are only paid out after Libra Association uses interest to pay for operating expenses, investments in the ecosystem, engineering research and grants to nonprofits and other organizations. This interest is part of what attracted the Libra Association’s members. If Libra becomes popular and many people carry a large balance of the currency, the reserve will grow huge and earn significant interest.

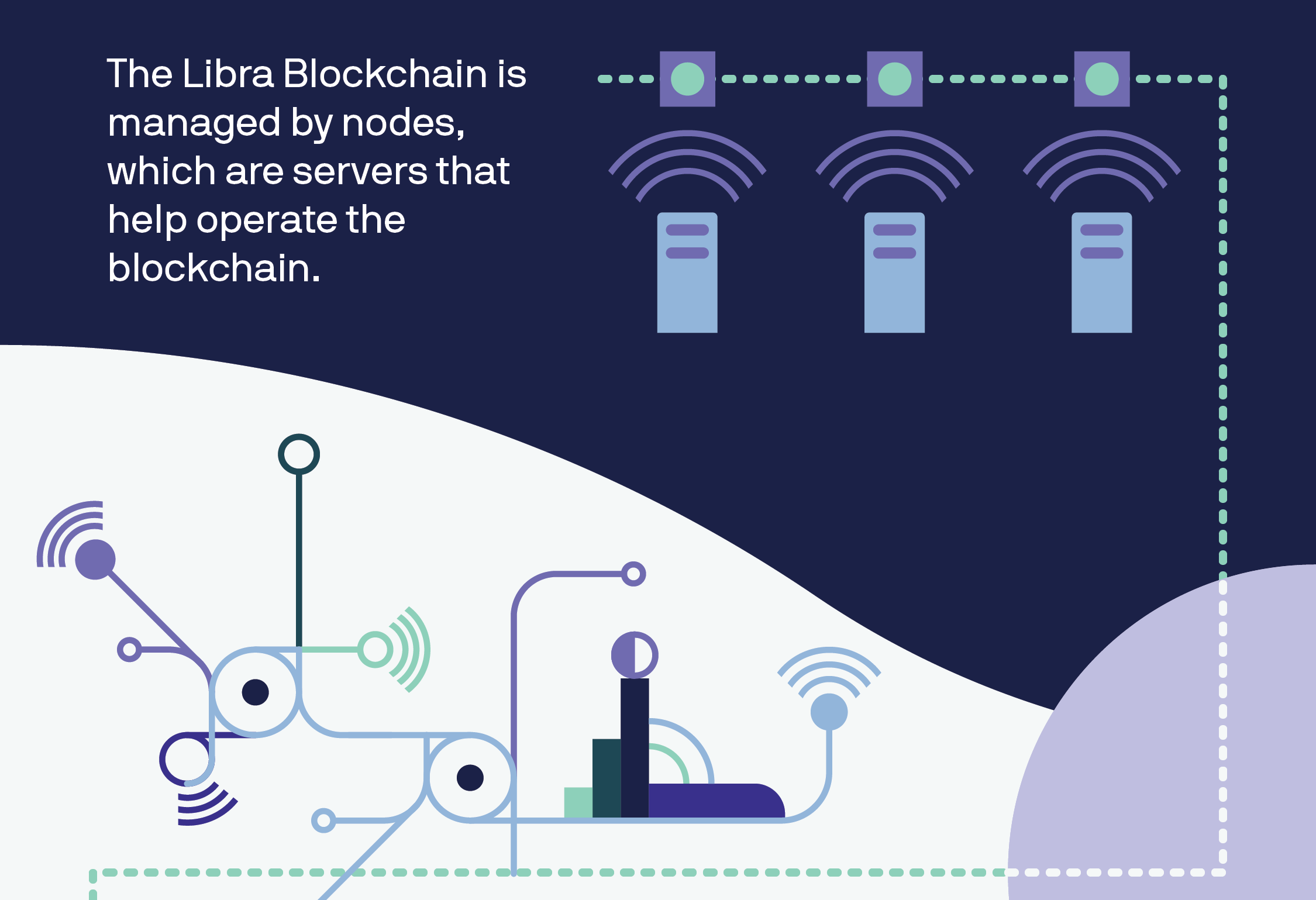

Every Libra payment is permanently written into the Libra Blockchain — a cryptographically authenticated database that acts as a public online ledger designed to handle 1,000 transactions per second. That would be much faster than Bitcoin’s 7 transactions per second or Ethereum’s 15. The blockchain is operated and constantly verified by founding members of the Libra Association, which each invested $10 million or more for a say in the cryptocurrency’s governance and the ability to operate a validator node.

When a transaction is submitted, each of the nodes runs a calculation based on the existing ledger of all transactions. Thanks to a Byzantine Fault Tolerance system, just two-thirds of the nodes must come to consensus that the transaction is legitimate for it to be executed and written to the blockchain. A structure of Merkle Trees in the code makes it simple to recognize changes made to the Libra Blockchain. With 5KB transactions, 1,000 verifications per second on commodity CPUs and up to 4 billion accounts, the Libra Blockchain should be able to operate at 1,000 transactions per second if nodes use at least 40Mbps connections and 16TB SSD hard drives.

Transactions on Libra cannot be reversed. If an attack compromises over one-third of the validator nodes causing a fork in the blockchain, the Libra Association says it will temporarily halt transactions, figure out the extent of the damage and recommend software updates to resolve the fork.

Transactions aren’t entirely free. They incur a tiny fraction of a cent fee to pay for “gas” that covers the cost of processing the transfer of funds similar to with Ethereum. This fee will be negligible to most consumers, but when they add up, the gas charges will deter bad actors from creating millions of transactions to power spam and denial-of-service attacks. “We’ve purposely tried not to innovate massively on the blockchain itself because we want it to be scalable and secure,” says Marcus of piggybacking on the best elements of existing cryptocurrencies.

Currently, the Libra Blockchain is what’s known as “permissioned,” where only entities that fulfill certain requirements are admitted to a special in-group that defines consensus and controls governance of the blockchain. The problem is this structure is more vulnerable to attacks and censorship because it’s not truly decentralized. But during Facebook’s research, it couldn’t find a reliable permissionless structure that could securely scale to the number of transactions Libra will need to handle. Adding more nodes slows things down, and no one has proven a way to avoid that without compromising security.

That’s why the Libra Association’s goal is to move to a permissionless system based on proof-of-stake that will protect against attacks by distributing control, encourage competition and lower the barrier to entry. It wants to have at least 20% of votes in the Libra Association council coming from node operators based on their total Libra holdings instead of their status as a founding member. That plan should help appease blockchain purists who won’t be satisfied until Libra is completely decentralized.

The Libra Blockchain is open source with an Apache 2.0 license, and any developer can build apps that work with it using the Move coding language. The blockchain’s prototype launches its testnet today, so it’s effectively in developer beta mode until it officially launches in the first half of 2020. The Libra Association is working with HackerOne to launch a bug bounty system later this year that will pay security researchers for safely identifying flaws and glitches. In the meantime, the Libra Association is implementing the Libra Core using the Rust programming language because it’s designed to prevent security vulnerabilities, and the Move language isn’t fully ready yet.

Move was created to make it easier to write blockchain code that follows an author’s intent without introducing bugs. It’s called Move because its primary function is to move Libra coins from one account to another, and never let those assets be accidentally duplicated. The core transaction code looks like: LibraAccount.pay_from_sender(recipient_address, amount) procedure.

Eventually, Move developers will be able to create smart contracts for programmatic interactions with the Libra Blockchain. Until Move is ready, developers can create modules and transaction scripts for Libra using Move IR, which is high-level enough to be human-readable but low-level enough to be translatable into real Move bytecode that’s written to the blockchain.

The Libra ecosystem and the Move language will be completely open to use and build, which presents a sizable risk. Crooked developers could prey on crypto novices, claiming their app works just the same as legitimate ones, and that it’s safe because it uses Libra. But if consumers get ripped off by these scammers, the anger will surely bubble up to Facebook. Yet still, Calibra’s head of product tells me, “There are no plans for the Libra Association to take a role in actively vetting [developers],” Calibra’s head of product Kevin Weil tells me.

Even though it’s tried to distance itself sufficiently via its subsidiary Libra and the association, many people will probably always think of Libra as Facebook’s cryptocurrency and blame it for their woes.

Read our full story on the dangers of Libra’s unvetted developer platform

The Libra Association wants to encourage more developers and merchants to work with its cryptocurrency. That’s why it plans to issue incentives, possibly Libra coins, to validator node operators who can get people signed up for and using Libra. Wallets that pull users through the Know Your Customer anti-fraud and money laundering process or that keep users sufficiently active for over a year will be rewarded. For each transaction they process, merchants will also receive a percentage of the transaction back.

Businesses that earn these incentives can keep them, or pass some or all of them along to users in the form of free Libra tokens or discounts on their purchases. This could create competition between wallets to see which can pass on the most rewards to their customers, and thereby attract the most users. You could imagine eBay or Spotify giving you a discount for paying in Libra, while wallet developers might offer you free tokens if you complete 100 transactions within a year.

“One challenge for Spotify and its users around the world has been the lack of easily accessible payment systems – especially for those in financially underserved markets,” Spotify’s Chief Premium Business Officer Alex Norström writes. “In joining the Libra Association, there is an opportunity to better reach Spotify’s total addressable market, eliminate friction and enable payments in mass scale.”

This savvy incentive system should massively help ratchet up Libra’s user count without dictating how businesses balance their margins versus growth. Facebook also has another plan to grow its developer ecosystem. By offering venture capital firms like Andreessen Horowitz and Union Square Ventures a portion of the reserve interest, they’re motivating to fund startups building Libra infrastructure.

So how do you actually own and spend Libra? Through Libra wallets like Facebook’s own Calibra and others that will be built by third-parties, potentially including Libra Association members like PayPal. The idea is to make sending money to a friend or paying for something as easy as sending a Facebook Message. You won’t be able to make or receive any real payments until the official launch next year, though, but you can sign up for early access when it’s ready here.

None of the Libra Association members agreed to provide details on what exactly they’ll build on the blockchain, but we can take Facebook’s Calibra wallet as an example of the basic experience. Calibra will launch alongside the Libra currency on iOS and Android within Facebook Messenger, WhatsApp and a standalone app. When users first sign up, they’ll be taken through a Know Your Customer anti-fraud process where they’ll have to provide a government-issued photo ID and other verification info. They’ll need to conduct due diligence on customers and report suspicious activity to the authorities.

From there you’ll be able to cash in to Libra, pick a friend or merchant, set an amount to send them and add a description and send them Libra. You’ll also be able to request Libra, and Calibra will offer an expedited way of paying merchants by scanning your or their QR code. Eventually it wants to offer in-store payments and integrations with point-of-sale systems like Square.

The Libra Association’s e-commerce members seem particularly excited about how the token could eliminate transaction fees and speed up checkout. “We believe blockchain will benefit the luxury industry by improving IP protection, transparency in the product life cycle and — as in the case of Libra — enable global frictionless e-commerce,” says FarFetch CEO Jose Neves.

Facebook CEO Mark Zuckerberg explained some of the philosophy behind Libra and Calibra in a post today. “It’s decentralized — meaning it’s run by many different organizations instead of just one, making the system fairer overall. It’s available to anyone with an internet connection and has low fees and costs. And it’s secured by cryptography which helps keep your money safe. This is an important part of our vision for a privacy-focused social platform — where you can interact in all the ways you’d want privately, from messaging to secure payments.”

By default, Facebook won’t import your contacts or any of your profile information, but may ask if you wish to do so. It also won’t share any of your transaction data back to Facebook, so it won’t be used to target you with ads, rank your News Feed, or otherwise earn Facebook money directly. Data will only be shared in specific instances in anonymized ways for research or adoption measurement, for hunting down fraudsters or due to a request from law enforcement. And you don’t even need a Facebook or WhatsApp account to sign up for Calibra or to use Libra.

“We realize people don’t want their social data and financial data commingled,” says Marcus, who’s now head of Calibra. “The reality is we’ll have plenty of wallets that will compete with us and many of them will not be in social, and if we want to successfully win people’s trust, we have to make sure the data will be separated.”

In case you are hacked, scammed or lose access to your account, Calibra will refund you for lost coins when possible through 24/7 chat support because it’s a custodial wallet. You also won’t have to remember any long, complex crypto passwords you could forget and get locked out from your money, as Calibra manages all your keys for you. Given Calibra will likely become the default wallet for many Libra users, this extra protection and smoother user experience is essential.

For now, Calibra won’t make money. But Calibra’s head of product Kevin Weil tells me that if it reaches scale, Facebook could launch other financial tools through Calibra that it could monetize, such as investing or lending. “In time, we hope to offer additional services for people and businesses, such as paying bills with the push of a button, buying a cup of coffee with the scan of a code or riding your local public transit without needing to carry cash or a metro pass,” the Calibra team writes. That makes it start to sound a lot like China’s everything app WeChat.

Facebook got one thing right for sure: Today’s money doesn’t work for everyone. Those of us living comfortably in developed nations likely don’t see the hardships that befall migrant workers or the unbanked abroad. Preyed on by greedy payday lenders and high-fee remittance services, targeted by muggers and left out of traditional financial services, the poor get poorer. Libra has the potential to get more money from working parents back to their families and help people retain credit even if they’re robbed of their physical possessions. That would do more to accomplish Facebook’s mission of making the world feel smaller than all the News Feed Likes combined.

If Facebook succeeds and legions of people cash in money for Libra, it and the other founding members of the Libra Association could earn big dividends on the interest. And if suddenly it becomes super quick to buy things through Facebook using Libra, businesses will boost their ad spend there. But if Libra gets hacked or proves unreliable, it could cost lots of people around the world money while souring them on cryptocurrencies. And by offering an open Libra platform, shady developers could build apps that snatch not just people’s personal info like Cambridge Analytica, but their hard-earned digital cash.

Facebook just tried to reinvent money. Next year, we’ll see if the Libra Association can pull it off. It took me 4,000 words to explain Libra, but at least now you can make up your own mind about whether to be scared of Facebook crypto.

Powered by WPeMatico

Andreessen Horowitz <3 Latin American startups.

Latin America is the only region outside of the U.S. where the venture firm is routinely investing capital, and it just made another commitment, doubling down on its early-stage support for the point-of-sale lending startup ADDI.

ADDI picked up $12.5 million in new financing in April of this year as the company looks to expand its lending services online.

For an American audience, the closest corollary to what ADDI is up to is likely Affirm, the point-of-sale lender that’s raised a ton of cash and come in for some (valid) criticism for its basic business model.

Like Affirm, ADDI lets its borrowers apply for credit at the moment of purchase. The company likens its service to the layaway and credit plans that already exist in Colombia — but involve pretty onerous requirements to use. Company co-founder Santiago Suarez and Andreessen Horowitz general partner Angela Strange both commented on how, in some cases, Colombian shoppers have to have three people vouch for a borrower before a store will issue credit or agree to a layaway plan.

The difference between an ADDI loan — or any loan — and layaway is that an installment payment plan doesn’t charge interest (and even with the fees that installment plans do charge, they are often still cheaper than taking out a loan).

But financial products are coming for consumers in Latin America whether those buyers like it or not — and for the most part, it seems they do like it.

Historically, only the wealthiest clientele in Latin America received anything resembling the kinds of financial products that are more widely available in the United States, according to Strange. And the investment in ADDI is just part of her firm’s thesis in trying to make more services more broadly available in a region where a technological transformation is creating unprecedented opportunities for challengers.

That assessment is what drew Santiago Suarez back to Latin America only two years ago. A former executive at Lending Club who previously had worked as the head of New Product Development and Emerging Services at J.P. Morgan, Suarez saw the tremendous growth happening in Latin America and returned to Colombia to see if he could bring some much needed services to his home country.

Suarez partnered with his childhood friend, Elmer Ortega, who was working as the chief technology officer of the local hedge fund where he had previously been employed as a derivatives trader before learning how to code.

Together, the two men, who had known each other since they were five years old, set out to transform how credit was offered in retail shops. It’s an industry that Suarez had known well since his parents had owned stores.

“In the U.S. there are all of these gaps that fintech companies are filling,” says Suarez. “But the gaps in Latin America are bigger.”

Suarez and Ortega incorporated the company in September 2018, around the same time they raised $2.3 million from the regional investment firm, Monashees, Andreessen and Village Global . They then raised another $1.5 million in an internal round of financing before closing the most recent funding.

The company offers loans at annual percentage rates ranging from 19.99% to 28.90%. The company started with a digital solution for brick and mortar retailers because 90% of retail in Colombia still happens offline.

Although it’s in its early days, the company has already originated 10,000 borrowers and typically loans out roughly $500 since it launched on February 22, according to Suarez. He declined to comment on the company’s default rate on loans.

Now with 40 employees on staff, the company is looking to bring its lending tool to more e-commerce and physical retailers, according to Suarez. And despite the threat of cyclical political turmoil, Suarez says there’s no better time to be investing in Colombia.

“It’s the most stable country outside of Chile… Way more stable than Brazil, way more stable than Argentina and way more stable than Mexico,” Suarez says. “What we’re looking at is more than cyclical instability… those things go beyond that. Nubank was able to build a multibillion business in the worst political and economic crisis in Brazil’s history. I think Colombia is an incredibly attractive space with a deep talent pool.”

Powered by WPeMatico

After a decade in the peculiar world of venture capital, Andreessen Horowitz managing director Scott Kupor has seen it all when it comes to the dos and don’ts for dealing with Valley VCs and company building. In his new book Secrets of Sand Hill Road (available on June 3), Scott offers up an updated guide on what VCs actually do, how they think and how founders should engage with them.

TechCrunch’s Silicon Valley editor Connie Loizos will be sitting down with Scott for an exclusive conversation on Tuesday, June 4 at 11:00 am PT. Scott, Connie and Extra Crunch members will be digging into the key takeaways from Scott’s book, his experience in the Valley and the opportunities that excite him most today.

Tune in to join the conversation and for the opportunity to ask Scott and Connie any and all things venture.

To listen to this and all future conference calls, become a member of Extra Crunch. Learn more and try it for free.

Powered by WPeMatico

Slack, the ubiquitous workplace messaging tool, will make its pitch to prospective shareholders on Monday at an invite-only event in New York City, the company confirmed in a blog post on Wednesday. Slack stock is expected to begin trading on the New York Stock Exchange as soon as next month.

Slack, which is pursuing a direct listing, will live stream Monday’s Investor Day on its website.

An alternative to an initial public offering, direct listings allow businesses to forgo issuing new shares and instead sell directly to the market existing shares held by insiders, employees and investors. Slack, like Spotify, has been able to bypass the traditional roadshow process expected of an IPO-ready business, as well as some of the exorbitant Wall Street fees.

Spotify, if you remember, similarly live streamed an event that is typically for investors eyes only. If Slack’s event is anything like the music streaming giant’s, Slack co-founder and chief executive officer Stewart Butterfield will speak to the company’s greater mission alongside several other executives.

Slack unveiled documents for a public listing two weeks ago. In its SEC filing, the company disclosed a net loss of $138.9 million and revenue of $400.6 million in the fiscal year ending January 31, 2019. That’s compared to a loss of $140.1 million on revenue of $220.5 million for the year before.

Additionally, the company said it reached 10 million daily active users earlier this year across more than 600,000 organizations.

Slack has previously raised a total of $1.2 billion in funding from investors, including Accel, Andreessen Horowitz, Social Capital, SoftBank, Google Ventures and Kleiner Perkins.

Powered by WPeMatico

Carta, a seven-year-old, San Francisco-based startup, is the newest unicorn in tech. The company, which largely helps private company investors, founders, and employees manage their equity and ownership, tells TechCrunch it has raised $300 million in a Series E round at a $1.7 billion valuation, led by Andreessen Horowitz. Firm co-founder Marc Andreessen is also joining the board.

The round has been a poorly kept secret. The outlet The Information reported more than a month ago the details that Carta is sharing today. In fact, that leak has given people in the industry who understand Carta’s business time to quietly ask of its valuation whether it isn’t high for a company that does what it does.

Unsurprisingly, Carta argues that it is not, that it has evolved considerably from the outset — which is true. Though it launched as a way for venture-backed companies to mange equity, issue securities, and track their cap tables, by 2014, Carta, formerly known as eShares, had moved beyond replacing paper records and into selling as a monthly service appraisals of the fair market value of private companies’ common stock in order to determine their strike price. It calls this “409A-as-a-service.”

Carta has continued tacking on more services. Among the most notable was the launch last year of a fund administration product designed to help venture capital firms not only manage their portfolio stakes more easily but to more seamlessly work with their own investors or limited partners. Toward this end, Carta now provides portfolio analytics, including deal IRRs and cash management, it helps VCs distribute their quarterly investor reports and it integrates with third-party tax and payroll providers.

Carta has so many pieces in place that in a call on Friday, founder and CEO Henry Ward told us Carta is taking what may be its biggest step yet and becoming the first real “private stock market for companies.” Its massive new funding round is “about act three,” he said. “Now that you have this network of companies and investors all on one platform and the ability to transfer securities, you can build liquidity on top of it.” It’s this vision that enticed Andreessen to jump aboard, he suggested.

There’s unquestionably a need for a kind of private stock market. Private funding has been outpacing IPO funding for years, and it shows no sign of stopping. It’s largely why the SEC is trying to better enable people who are not accredited investors to access private company shares. Most of the U.S. has missed out on the wealth creation happening before companies go public or sell to other companies.

It’s also true that Carta has its hooks into a meaningful number of startups and venture firms at this point. The company says more than 700,000 shareholders are on its platform, that it works with more than 11,000 companies and that its fund administration product now serves 143 venture firms.

Still, some longtime industry observers wonder if Carta isn’t mashing together a lot of disparate, moderately lucrative businesses and positioning it as the next-big platform company, and the view resonates. For one thing, Carta likes to talk about assets managed, though it’s really talking about how much in assets the startups and VCs that use its platform control, which is $575 billion altogether. Carta — which now employs nearly 600 employees across seven offices — says its own annual revenue run rate is currently $55 million.

Relatedly, while Ward says Carta’s primary revenue right now is its software subscription business — another revenue stream is the money it’s paid by the venture firms that use it as a fund administrator — people who question Carta’s fundraising note the people-intensive nature of the kind of work that Carta has been systemizing. Yes, there’s a sophisticated software component, but Carta is more Accenture than Salesforce, and services businesses are valued very differently.

There’s also the question of growth. Ward points to the roughly 450 startups that are garnering venture funding each month right now — all potential customers for Carta. But plenty of companies are also quietly going out of business all the time, a process that will accelerate whenever this very long funding boom finally slows.

This newest business conveys the impression that big things are coming, though it doesn’t sound exactly like a private stock market as Ward describes it, either. Primarily, it won’t provide the relative transparency that stock markets do. We don’t think that’s the case, anyway. Ward was somewhat dismissive of questions we asked about how Carta’s newest business will be fundamentally different than that of secondary players in the market that are already making it possible for shareholders to value and transact shares.

Indeed, though Carta says it’s changing how assets are acquired, valued and transacted, Ward also did not respond to several simple follow-up queries sent to him on Friday about the mechanics of this new business, dubbed CartaX. Instead, he thanked us for our efforts to understand and articulate Carta’s business. Meanwhile, his press team told us it was limited in what it can say about how CartaX operates for now.

Carta has savvy investors. In addition to Andreessen Horowitz, this newest round includes Lightspeed Venture Partners, Goldman Sachs Principal Strategic Investments, Tiger Global, Thrive Capital and earlier backers Tribe Capital, Menlo Ventures and Meritech Capital.

No doubt that in valuing the company, they took into account that Solium — a Canada-based software-as-a-service for stock administration, financial reporting and compliance that was publicly traded — sold for $900 million in cash earlier this year to Morgan Stanley. That’s roughly double Carta’s total funding so far of $447 million.

More likely, they were viewing the company based on its potential as a kind of more liquid market, ambitious as that might seem today. Consider that the parent company to both the NYSE and the Chicago Stock Exchange currently has a market cap of roughly $45 billion. Then again, that company operates 12 exchanges and marketplaces altogether, and it enjoyed more than $6 billion in revenue last year by transacting more than a $100 billion dollars in volume on the NYSE alone on a daily basis.

Perhaps most important to them, Carta is now as well-positioned as anyone to capture and cater to the growing number of privately held companies looking to provide more of their employees liquidity and to cash out early investors. Add to the mix a mega-round and a star board member, and the company may well get to where Ward and his investors want it to go.

We’ll be watching to see.

[Correction: We’d originally misstated the market cap of Intercontinental Exchange, owner of the NYSE and Chicago Stock Exchange, among other marketplaces; we cited its annual revenue instead.]

Powered by WPeMatico

The microbiome testing service uBiome has placed its founders and co-chief executives, Jessica Richman and Zac Apte, on administrative leave following an FBI raid on the company’s offices last week.

The company’s board of directors have named John Rakow, currently the company’s general counsel, as its interim chairman and chief executive, the company said in a statement.

Directors of the company are also conducting an independent investigation into the company’s billing practices, which is being overseen by a special committee of the board.

It was only last week that the FBI went to the company’s headquarters to search for documents related to an ongoing investigation. What’s at issue is the way that the company was billing insurers for the microbiome tests it was performing on customers.

“As interim CEO of uBiome, I want all of our stakeholders to know that we intend to cooperate fully with government authorities and private payors to satisfactorily resolve the questions that have been raised, and we will take any corrective actions that are needed to ensure we can become a stronger company better able to serve patients and healthcare providers,” Rakow said in a statement.

”My confidence is based on the significant clinical evidence and medical literature that demonstrates the utility and value of uBiome’s products as important tools for patients, health care providers and our commercial partners.” added Mr. Rakow.

It’s been a rough few weeks for consumer companies working on developing microbiome testing services and treatments based on those diagnosis. In addition to the FBI raid, the Seattle-based company, Arivale, was forced to shut down its “consumer program” after raising more than $50 million from investors, including Maveron, Polaris Partners and ARCH Venture Partners.

UBiome is backed by investors including Andreessen Horowitz, OS Fund, 8VC, Y Combinator, DNA Capital, Crunchfund, StartX, Kapor Capital, Starlight Ventures and 500 Startups.

Powered by WPeMatico

PagerDuty debuted on the New York Stock Exchange today, and as we type, shares of the nine-year-old, San Francisco-based incident response software company are trading at nearly $39.

That’s up more than 60 percent above their IPO range of $24 per share, which was itself adjusted from the range of $21 to $23 that had been expected earlier and gives the company a valuation of close to $3 billion. That’s an awful lot for a company whose software helps technical teams at 11,000 companies spot problems with applications and respond to incidents. Though it’s growing quickly — revenue was up 48 percent last year — it still pulled in just $117.8 million in 2018. Meanwhile, its net loss widened last year, to $40.7 million from $38.1 million in 2017.

Certainly, its performance has to make the company’s investors — who last assigned the company a valuation of $1.3 billion back in September — very happy. Some of the VCs poised to win big if PagerDuty’s shares continue flying high include Andreessen Horowitz, which owned 18.4 percent of PagerDuty’s shares sailing into the IPO; Accel, which owned 12.3 percent; and Bessemer, which owned 12.2 percent. Other winners include Baseline Ventures (6.7 percent) and Harrison Metal (5.3 percent).

It’s also exciting for CEO Jennifer Tejada, a proven operator who was brought in to lead PagerDuty in 2016 and now becomes part of a small — but growing — club of women CEOs to take their tech companies public, including Katrina Lake of Stitch Fix and Julia Hartz of Eventbrite.

We talked with Tejada earlier today about the company’s big day. In addition to crediting company co-founders (and shareholders) Andrew Miklas and Baskar Puvanathasan, both of whom have since left the company, Tejada thanked PagerDuty co-founder Alex Solomon, who remains the company’s CTO. She also told us a little bit about what today has been like, and how the IPO changes things — and doesn’t. Our chat has been edited for length.

TC: First and foremost, how are you feeling?

JT: It’s been an incredible day. It’s been an incredible several months. You have to enjoy it when it’s going well.

TC: How does the vision for the company change now that it’s public? Have you been thinking ahead to possible acquisitions?

JT: The vision doesn’t change. We intend to do exactly what we’ve been doing, which is to provide the best real-time operations platform available to companies as they undergo digital transformation to meet the growing demands of their customers. We think we’re [facing] an early and very large opportunity that will be available to us for a long time. So our job continues to be to build great products, stay close to our customers, expand regionally and continue doing what has allowed us to be a successful private company.

TC: You and I had talked about the challenges of retaining employees in San Francisco when we sat down together in November. It’s a battle for every local company. How do you keep employees beyond the lock-up period? How do you ensure they stay focused on performance and not your share price?

JT: I think that mindset of, ‘It’s all over when you go public,’ is kind of a Silicon Valley fable. If you look at the most successful SaaS companies on the planet, they’ve gained 10x, 20x, 30x their value post their IPO. I also think what employees look for ahead of their financial success is career success. Am I being developed and recognized and can I build my career at this company? And we’ve worked really hard to create those career opportunities for our employees who [I think see, as I do] the IPO like a racing boat pushing off the dock, across the starting line, and into the open ocean, where the next adventure awaits.

In the meantime, we’ve already lessened our reliance on [overheated job markets] by opening offices in Toronto and Atlanta and Seattle and London and Sydney, even while we’re still hiring in San Francisco and Seattle.

TC: Obviously, Lyft’s shares have been up and down, owing to short sellers. Have you been monitoring short interest? Are you at all concerned about investors driving the price sky high, then selling it on the way down?

JT: I haven’t even looked at the stock price in the last several hours . . . There are a lot of things outside of my control, and the free market is one of them.

TC: PagerDuty is rare in that is doesn’t have a dual-class structure, which can greatly empower leaders over everyone else associated with a company. Presumably, this is a great relief to your investors; I just wonder whether it was ever a consideration?

JT: I’m a little bit of a traditionalist. I’ve been around long enough to know how checks and balances work, and a single-class structure made sense for PagerDuty. Also, dual-class structures tend to emerge more when you have deeply involved founders, and though Alex is still very much a part of the business, PagerDuty’s other two founders have worked outside of the business for some time.

TC: You have plenty of operating experience, including previously running Keynote Systems, but you’ve never taken a company public. Were there ways in which you found the roadshow experience surprising?

JT: I was surprised by how fun it was! [Laughs.] When you have a great story, and a great partner helping you tell it — in my case that’s [PagerDuty CFO] Howard Wilson, who I’ve worked with for 10 years — it’s great. We had a great reception from investors. I loved our IPO team; our Top were both led by women and whenever I had a question, they [had the answer]. I also had this cocoon of experience surrounding me thanks to our board. If anyone tells you that [in this position] they are super comfortable, they’re either lying or [clueless] but I was very lucky. I also have a whole bunch of buddies who are CEOs [and other executives] in SaaS and I’ve been shaking them down for advice for months, so I felt well-prepared.

TC: What was some of the advice you received from those friends about how your life is about to change?

JT: Some of it was about the need to keep people focused and not get distracted, to remind everyone that this is a milestone, not the goal. [Some centered on] surrounding yourself with a great team and the importance of great investor relations, a function you don’t have as a private company but that can create huge value and provide support and understanding of the market.

One CEO said to just make sure you keep having fun, to try and stay “you,” to find joy in the same things as before. There will be stressful moments and tough questions — that’s true of any company that’s scaling — but I heard a lot of advice about just taking care of myself, including on the roadshow. In fact, there were a lot of really supportive notes and private tweets that, in a job that can feel lonely, made me feel not alone, and I’m very appreciative of that.

TC: People call IPOs just another funding event, but that’s kind of baloney, isn’t it? If you had to list the most meaningful moments in your life on a scale from 1 to 10, 1 being the most important, where might today fall? Would today be up there on that list?

JT: When I think of most meaningful moments, I think of the day my daughter was born, and my wedding. Another day that was very meaningful to me was when I approved our pledge to donate one percent [of PagerDuty’s equity, one percent of its product and one percent of employees’ time] to social impact. We did it a lot later in the game than some companies; our equity was already valuable. But we knew that it was going to create meaningful impact over time.

But yes, it is a gratifying day, especially for the co-founders who were pulling the idea together for PagerDuty a couple of years before they even launched it, and for employees who’ve been with the company for nearly as long and who turned down safer and higher-paying jobs along the way. Seeing their joy today — that is a memory that will be in my top 10 for sure.

Powered by WPeMatico