Anchorage

Auto Added by WPeMatico

Auto Added by WPeMatico

While the enterprise world likes to talk about “big data”, that term belies the real state of how data exists for many organizations: the truth of the matter is that it’s often very fragmented, living in different places and on different systems, making the concept of analysing and using it in a single, effective way a huge challenge.

Today, one of the big up-and-coming startups that has built a platform to get around that predicament is announcing a significant round of funding, a sign of the demand for its services and its success so far in executing on that.

SingleStore, which provides a SQL-based platform to help enterprises manage, parse and use data that lives in silos across multiple cloud and on-premise environments — a key piece of work needed to run applications in risk, fraud prevention, customer user experience, real-time reporting and real-time insights, fast dashboards, data warehouse augmentation, modernization for data warehouses and data architectures and faster insights — has picked up $80 million in funding, a Series E round that brings in new strategic investors alongside its existing list of backers.

The round is being led by Insight Partners, with new backers Dell Technologies Capital, Hercules Capital; and previous backers Accel, Anchorage, Glynn Capital, GV (formerly Google Ventures) and Rev IV also participating.

Alongside the investment, SingleStore is formally announcing a new partnership with analytics powerhouse SAS. I say “formally” because they two have been working together already and it’s resulted in “tremendous uptake,” CEO Raj Verma said in an interview over email.

Verma added that the round came out of inbound interest, not its own fundraising efforts, and as such, it brings the total amount of cash it has on hand to $140 million. The gives the startup money to play with not only to invest in hiring, R&D and business development, but potentially also M&A, given that the market right now seems to be in a period of consolidation.

Verma said the valuation is a “significant upround” compared to its Series D in 2018 but didn’t disclose the figure. PitchBook notes that at the time it was valued at $270 million post-money.

When I last spoke with the startup in May of this year — when it announced a debt facility of $50 million — it was not called SingleStore; it was MemSQL. The company rebranded at the end of October to the new name, but Verma said that the change was a long time in the planning.

“The name change is one of the first conversations I had when I got here,” he said about when he joined the company in 2019 (he’s been there for about 16 months). “The [former] name didn’t exactly flow off the tongue and we found that it no longer suited us, we found ourselves in a tiny shoebox of an offering, in saying our name is MemSQL we were telling our prospects to think of us as in-memory and SQL. SQL we didn’t have a problem with but we had outgrown in-memory years ago. That was really only 5% of our current revenues.”

He also mentioned the hang up many have with in-memory database implementations: they tend to be expensive. “So this implied high TCO, which couldn’t have been further from the truth,” he said. “Typically we are ⅕-⅛ the cost of what a competitive product would be to implement. We were doing ourselves a disservice with prospects and buyers.”

The company liked the name SingleStore because it is based a conceptual idea of its proprietary technology. “We wanted a name that could be a verb. Down the road we hope that when someone asks large enterprises what they do with their data, they will say that they ‘SingleStore It!’ That is the vision. The north star is that we can do all types of data without workload segmentation,” he said.

That effort is being done at a time when there is more competition than ever before in the space. Others also providing tools to manage and run analytics and other work on big data sets include Amazon, Microsoft, Snowflake, PostgreSQL, MySQL and more.

SingleStore is not disclosing any metrics on its growth at the moment but says it has thousands of enterprise customers. Some of the more recent names it’s disclosed include GE, IEX Cloud, Go Guardian, Palo Alto Networks, EOG Resources, SiriusXM + Pandora, with partners including Infosys, HCL and NextGen.

“As industry after industry reinvents itself using software, there will be accelerating market demand for predictive applications that can only be powered by fast, scalable, cloud-native database systems like SingleStore’s,” said Lonne Jaffe, managing director at Insight Partners, in a statement. “Insight Partners has spent the past 25 years helping transformational software companies rapidly scale-up, and we’re looking forward to working with Raj and his management team as they bring SingleStore’s highly differentiated technology to customers and partners across the world.”

“Across industries, SAS is running some of the most demanding and sophisticated machine learning workloads in the world to help organizations make the best decisions. SAS continues to innovate in AI and advanced analytics, and we partner with companies like SingleStore that share our curiosity about how data and analytics can help organizations reimagine their businesses and change the world,” said Oliver Schabenberger, COO and CTO at SAS, added. “Our engineering teams are integrating SingleStore’s scalable SQL-based database platform with the massively parallel analytics engine SAS Viya. We are excited to work with SingleStore to improve performance, reduce cost, and enable our customers to be at the forefront of analytics and decisioning.”

Powered by WPeMatico

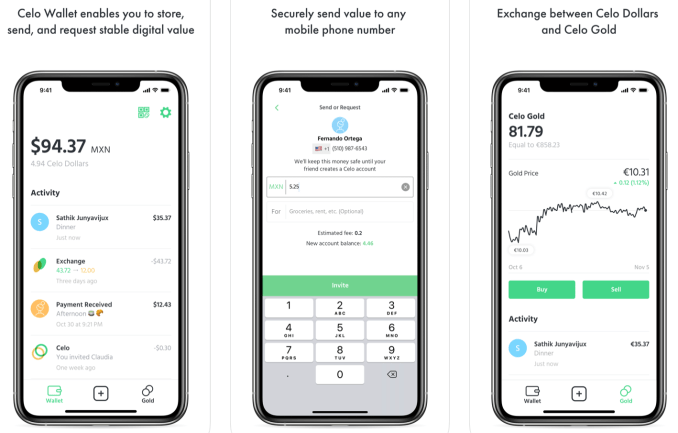

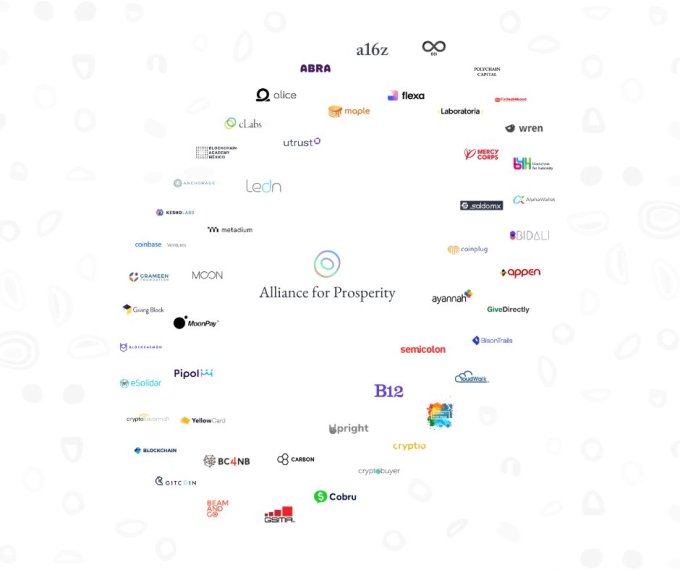

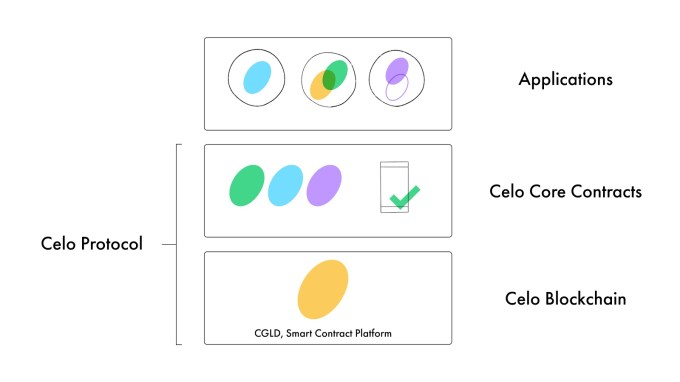

Some Libra Association members like Andreessen Horowitz and Coinbase Ventures are double-dipping, backing a competing cryptocurrency developer platform. Launching today with over 50 partners, non-profit The Celo Foundation’s ‘Alliance For Prosperity’ offers a way for developers to build decentralized mobile apps that are based on Celo’s blockchain platform and USD stablecoin.

The open-source Celo platform is still in testing with plans to officially launch its mainnet in April. The non-profit founded in 2017 has raised $36.4 million, including its Series A where Andreessen Horowitz’s a16z Crypto bought $15 million worth of Celo Gold tokens.

The biggest differentiator of Celo’s network versus other blockchains is that payments in the Celo Dollar stablecoin can be sent to people’s phone numbers rather than complicated addresses. The goal is to make delivering utility via blockchain easier by building a flexible network of applications that doesn’t scare regulators like Libra has.

The Alliance For Prosperity includes Andreessen Horowitz (which funded Celo), Coinbase (Ventures), Bison Trails, Anchorage, and Mercy Corps — all of which are also Libra Association members. That could potentially create a conflict of interest regarding which cryptocurrency and developer platform they promote to their portfolio companies, integrate into their products, or focus on for delivering financial services to the needy.

Other high-profile Alliance partners include Carbon, GiveDirectly, Grameen Foundation, Maple, and Polychain. Partners have made a somewhat vague commitment to “backing development efforts of the project, building infrastructure, implementing desired use cases on the platform, integrating Celo assets in their projects, or collaborating on education campaigns in their communities to further advance the use of blockchain technology” according to Chuck Kimble, Celo’s cLabs head of business development and head of the Alliance. Anyone can apply to join the open network, and there’s no minimum financial investment like Libra’s $10 million prerequisite.

Celo isn’t trying to replace the dollar with its own synthetic currency, and its reserve is backed with other cryptocurrencies rather than fiat cash. That might make it more acceptable to regulators who were worried that Libra’s token and fiat currency bundle-backed reserve could impact the global financial system. The first of the decentralized apps on the platform, the Celo Wallet, is already available for iOS and Android.

Like many blockchain projects, there are some lofty intentions for social impact with Celo. Use cases include “powering mobile and online work, enabling faster and affordable remittances, reducing the operational complexities of delivering humanitarian aid, facilitating payments, and enabling microlending” says Kimble. The real driver of this potential is Celo’s promise of much lower transaction fees than traditional middlemen charge.

When asked what the biggest threats to Celo’s success are, he told me “Banking infrastructure improving faster than we expect” and “Mobile adoption or LTE data not expanding on their current trajectory.” He did not mention the developer fatigue, regulatory scrutiny, technical complexity, or slow adoption of blockchain utilities that have plagued other crypto for good projects.

Here’s the full list of members working towards these goals:

Abra, Alice, AlphaWallet, Anchorage, Appen, Ayannah, Andreessen Horowitz, B12, BC4NB (Blockchain for the Next Billion), BeamAndGo, Bidali, Bison Trails, Blockchain Academy Mexico, Blockchain.com, Blockchain for Humanity (b4h), Blockchain for Social Impact (BSIC), Blockdaemon, Carbon, cLabs, CloudWalk Inc, Cobru, Coinbase, Coinplug, Cryptio, Cryptobuyer, CryptoSavannah, eSolidar, Fintech4Good, Flexa, Gitcoin, GiveDirectly, Grameen Foundation, GSMA, KeshoLabs, Laboratoria, Ledn, Maple, Mercy Corps, Metadium, Moon, MoonPay, Pipol, Pngme, Polychain, Project Wren, SaldoMX, Semicolon Africa, The Giving Block, Utrust, Upright, Yellow Card, and 88i. [Update: Ledger joined this morning.]

“Many of these organizations have on-the-ground operations that will begin to get Celo into the hands of those who have been underserved by the current global financial system” Andreessen Horowitz general partner Katie Haun told me. “Our hope is that this partnership will start unlocking the potential of internet money”. To spur adoption, the Alliance will distribute ‘Prosperity Gifts’ in the form of financial grants to developers proposing Celo products that would benefit society.

There are also some peculiar characteristics of Celo’s system. People exchange other cryptocurrencies for Celo Gold, then exchange that for Celo Dollars they can spend. The reserve is backed with other cryptocurrencies like bitcoin and ethereum rather that fiat, and isn’t fully collateralized. That could make it vulnerable to a Celo bank run or crash in price of those currencies. Celo also lets arbitrageurs pocket the difference if Celo Gold and Celo Dollars get out of sync.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

So far, 130 teams have expressed interest in building on the Celo platform. For reference, Libra said 1,500 organizations had said they wanted to work on that project four months after its reveal. Celo Camp and Blockchain for Social Impact Incubator will also be fostering projects for the blockchain.

Celo could make banking cheaper and more accessible while power new fintech innovation. But for any of that to happen, it will need to get enough developers building truly useful products, make the blockchain and currency exchange simple enough for mainstream audiences in developing nations, and grow adoption to meaningful levels few cryptocurrency projects have yet achieved. The Alliance For Prosperity will have to throw their weight into this project, not just their names, if it’s going to succeed.

Powered by WPeMatico

Not the city, the $57 million-funded cryptocurrency custodian startup. When someone wants to keep safe tens or hundreds of millions of dollars in Bitcoin, Ethereum or other coins, they put them in Anchorage’s vault. And now they can trade straight from custody so they never have to worry about getting robbed mid-transaction.

With backing from Visa, Andreessen Horowitz and Blockchain Capital, Anchorage has emerged as the darling of the cryptocurrency security startup scene. Today it’s flexing its muscle and war chest by announcing its first acquisition, crypto risk modeling company Merkle Data.

Anchorage Founders

Anchorage has already integrated Merkle’s technology and team to power today’s launch of its new trading feature. It eliminates the need for big crypto owners to manually move assets in and out of custody to buy or sell, or to set up their own in-house trading. Instead of grabbing some undisclosed spread between the spot price and the price Anchorage quotes its clients, it charges a transparent per transaction fee of a tenth of a percent.

It’s stressful enough trading around digital fortunes. Anchorage gives institutions and token moguls peace of mind throughout the process while letting them stake and vote while their riches are in custody. Anchorage CEO Nathan McCauley tells me, “Our clients want to be able to fund a bank account with USD and have it seamlessly converted into crypto, securely held in their custody accounts. Shockingly, that’s not yet the norm — but we’re changing that.”

Founded in 2017 by leaders behind Docker and Square, Anchorage’s core business is its omnimetric security system that takes out of the equation passwords that can be lost or stolen. Instead, it uses humans and AI to review scans of your biometrics, nearby networks and other data for identity confirmation. Then it requires consensus approval for transactions from a set of trusted managers you’ve whitelisted.

With Anchorage Trading, the startup promises efficient order routing, transparent pricing and multi-venue liquidity from OTC desks, exchanges and market makers. “Because trading and custody are directly integrated, we’re able to buy and sell crypto from custody, without having to make risky external transfers or deal with multiple accounts from different providers,” says Bart Stephens, founder and managing partner of Blockchain Capital.

Trading isn’t Anchorage’s primary business, so it doesn’t have to squeeze clients on their transactions, and can instead try to keep them happy for the long-term. That also sets up Anchorage to be a foundational part of the cryptocurrency stack. It wouldn’t disclose the terms of the Merkle Data acquisition, but the Pantera Capital-backed company brings quantitative analysts to Anchorage to keep its trading safe and smart.

“Unlike most traditional financial assets, crypto assets are bearer assets: In order to do anything with them, you need to hold the underlying private keys. This means crypto custodians like Anchorage must play a much larger role than custodians do in traditional finance,” says McCauley. “Services like trading, settlement, posting collateral, lending and all other financial activities surrounding the assets rely on the custodian’s involvement, and in our view are best performed by the custodian directly.”

Anchorage will be competing with Coinbase, which offers integrated custody and institutional brokerage through its agency-only OTC desk. Fidelity Digital Assets combines trading and brokerage, but for Bitcoin only. BitGo offers brokerage from custody through a partnership with Genesis Global Trading. But Anchorage hopes its experience handling huge sums, clear pricing and credentials like membership in Facebook’s Libra Association will win it clients.

McCauley says the biggest threat to Anchorage isn’t competitors, though, but hazy regulation. Anchorage is building a core piece of the blockchain economy’s infrastructure. But for the biggest financial institutions to be comfortable getting involved, lawmakers need to make it clear what’s legal.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about Stripe’s grand plans. Before that, I noted Peloton’s secret weapons.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

The best companies are built by people who have personally experienced the problem they’re attempting to solve. Lauren Jonas, the founder and chief executive officer of Part & Parcel, is intimately familiar with the struggles faced by the women she’s building for.

San Francisco-based Part & Parcel is a plus-sized clothing and shoe startup providing dimensional sizing to women across the U.S. The company operates a bit differently than your standard direct-to-consumer business by seeking to include the women who wear and evangelize the Part & Parcel designs by giving them a cut of their sales.

Here’s how it works: Ambassadors sign up to receive signature styles from Part & Parcel, which they then share and sell to women in their network. Ultimately, the sellers are eligible to receive up to 30% of the profit per sale. The out-of-the-box model, which might remind you somewhat of Mary Kay or Tupperware’s business strategy, is meant to encourage a sense of community and usher in a new era in which plus-sized women can facilitate other plus-sized women’s access to great clothes.

“I bought a brown men’s polyester suit and wore it to an interview,” Jonas, an early employee at Poshmark and the long-time author of the popular blog, ‘The Pear Shape,’ tells TechCrunch. “I was that kid wearing a men’s suit.”

Clothing tailored to plus-sized women has long been missing from the retail market. Increasingly, however, new brands are building thriving businesses by catering precisely to the historically forgotten demographic. Dia&Co., for example, raised another $70 million in venture capital funding last fall from Sequoia and USV. And Walmart recently acquired another brand in the space, ELOQUII, for an undisclosed amount. Part & Parcel, for its part, has raised $4 million in seed funding in a round led by Lightspeed Venture Partners’ Jeremy Liew.

The startup launched earlier this year in Anchorage, “a clothing desert,” and has since grown its network to include women in several other underserved markets. Given her own history struggling to find a fitted woman’s suit, Jonas launched her line with structured pieces, including suits and blouses — though the startup’s biggest success yet, she says, has been its boots, which come in three different calf width options.

“Seventy percent of women in this country are plus-sized,” Jonas said. “I’m bringing plus out of the dark corner of the department store.”

Image: Bryce Durbin / TechCrunch

TechCrunch’s Megan Rose Dickey published a highly anticipated deep dive on the state of sex tech this week. The piece provides new data on funding in sex tech and wellness companies, analysis on sex tech startup’s battle for public advertising and responses from industry leaders on how we can destigmatize sex with technology. Here’s a short passage from the story:

Cindy Gallop sees a market opportunity in every type of business obstacle she encounters. That’s why All The Sky will also seek to invest in startups that tackle the infrastructural tools needed to fuel sextech, like payments, hosting providers and e-commerce sites.

“I want to fund the sextech ecosystem to maintain and sustain a portfolio for All the Skies, to create a bloody huge sextech ecosystem and three, to monopolistically build out the ecosystem to be a multi-trillion-dollar market,” Gallop says.

I swung by Contrary Capital‘s Demo Day this week, in which a number of startups gave a 4- to 5-minute pitch. Next on my list is Alchemist‘s Demo Day in Menlo Park. The accelerator welcomes enterprise startups for a six-month program focused on early customer adoption, company development and mentorship.

Also on my radar is Females To The Front. The event began this week in Palm Springs and if I were based in SoCal, I would have swung by. Led by Amy Margolis, the event is said to be the largest gathering of female cannabis founders and funders to date. Here’s how the group describes the event: “Females to the Front Retreat will mix immersive and hands-on workshops, pitch training, investment deck preparation and business skill set education with investor meetings and plenty of shared meals, pool time, yoga, connections, rest and rejuvenation. Every workshop is built to directly engage attendees instead of powerpoint and panels. Be prepared to return home inspired, engaged and with so many more tools in your toolbox.”

For the record, I don’t advertise events in my newsletter just wanted to give props to this one because it’s a great development for the cannabis tech ecosystem.

We are just weeks away from our flagship conference, TechCrunch Disrupt San Francisco. We have dozens of amazing speakers lined up. In addition to taking in the great line-up of speakers, ticket holders can roam around Startup Alley to catch the more than 1,000 companies showcasing their products and technologies. And, of course, you’ll get the opportunity to watch the Startup Battlefield competition live. Past competitors include Dropbox, Cloudflare and Mint… You never know which future unicorn will compete next.

You can take a look at the full agenda here. And if you still need convincing, here’s five reasons to attend this year’s conference from our COO himself.

This week, the lovely Alex Wilhelm, editor-in-chief of Crunchbase News, and I gathered to discuss a number of topics including WeWork’s IPO and Uber’s attempts to bypass a new law meant to protect gig workers. Listen here.

Powered by WPeMatico

Y Combinator-backed startup Astranis is now set to launch its first commercial telecommunication satellite aboard a Falcon 9 rocket, with a launch time frame currently set for sometime starting in the fourth quarter of next year. Astranis aims to address the market of people who don’t currently have broadband internet access, which is still a huge number globally, and they hope to do so using low-cost satellites that massively undercut the price of existing global telecommunications hardware, which can be built and launched much faster than existing spacecraft, too.

Astranis satellites are much more cost-efficient because they’re smaller and easier to make, which changes the economics of deployment for potential carrier and connectivity provider partners. Its approach has already attracted the partnership of Microcom subsidiary Pacific Dataport, an Anchorage company that was formed to expand satellite broadband access in Alaska. This will be the goal of the company’s first launch with SpaceX, to deliver a single satellite to geostationary orbit that will add more than 7.5 Gbps of capacity to the internet provider’s network in Alaska, tripling capacity and potentially reducing costs by “up to three times,” according to Astranis.

This isn’t the first-ever satellite that Astranis has sent up to space — it launched a demonstration satellite in 2018 to show that its tech could work as advertised. Astranis’ approach is distinct from others attempting to offer satellite-based connectivity, including SpaceX’s own Starlink project, because it focuses on building satellites that remain in a fixed orbital position relative to the area on the ground where they’re providing service, as opposed to using a large constellation of low Earth orbit satellites that offer coverage because one or more are bound to be over the coverage area at any given time as they orbit the Earth, handing off connections from one to the next.

Powered by WPeMatico

Visa and Andreessen Horowitz are betting even bigger on cryptocurrency, funding a big round for fellow Facebook Libra Association member Anchorage’s omnimetric blockchain security system. Instead of using passwords that can be stolen, Anchorage requires cryptocurrency withdrawals to be approved by a client’s other employees. Then the company uses both human and AI review of biometrics and more to validate transactions before they’re executed, while offering end-to-end insurance coverage.

This new-age approach to cryptocurrency protection has attracted a $40 million Series B for Anchorage, led by Blockchain Capital and joined by Visa and Andreessen Horowitz. The round adds to Anchorage’s $17 million Series A that Andreessen led just six months ago, demonstrating extraordinary momentum for the security startup.

“As a custodian, our work is focused on building financial plumbing that other companies depend on for their operations to run smoothly. In this regard we have always looked at Visa as a model,” Anchorage co-founder and president Diogo Mónica tells me.

“Visa was ‘fintech’ before the term existed, and has always been on the vanguard of financial infrastructure. Visa’s investment in Anchorage is helpful not only to our company but to our industry, as a validation of the entire ecosystem and a recognition that crypto will play a key role in the future of global finance.”

Cold-storage, where assets are held in computers not connected to the internet, has become a popular method of securing Bitcoin, Ether and other tokens. But the problem is that this can prevent owners from participating in governance of certain cryptocurrency where votes are based on their holdings, or earning dividends. Anchorage tells me it’s purposefully designed to permit this kind of participation, helping clients to get the most out of their assets like capturing returns from staking and inflation, or joining in on-chain governance.

As three of the 28 founding members of the Libra Association that will govern the new Facebook-incubated cryptocurrency, Anchorage, Visa and Andreessen Horowitz will be responsible for ensuring the stablecoin stays secure. While Facebook is building its own custodial wallet called Calibra for users, other Association members and companies hoping to dive into the ecosystem will need ways to protect their Libra stockpiles.

“Libra is exactly the kind of asset that Anchorage was created to hold,” Mónica wrote the day Libra was revealed. “Our custody solution enables online participation with offline assets, so that asset-holders don’t face a trade-off between security and usability.” The company believes that custodians shouldn’t dictate which coins their clients hold, so it’s working to support all types of digital assets. Anchorage tells me that will include support for securing Libra in the future.

You’ve probably already used technology secured by Anchorage’s founders, who engineered Docker’s containers that are used by Microsoft, and Square’s first encrypted card reader. Mónica was at Square when he met his future Anchorage co-founder Nathan McCauley, who’d been working on anti-reverse-engineering tech for the U.S. military. When a company that had lost the password to a $1 million cryptocurrency account asked for their help with security, they recognized the need for a more idiot-proof take on asset protection.

“Anchorage applies the best of modern security engineering for a more advanced approach: we generate and store private keys in secure hardware so they are never exposed at any point in their life cycle, and we eliminate human operations that expose assets to risk,” Mónica says. The startup competes with other crypto custody firms like Bitgo, Ledger, Coinbase and Gemini.

Last time we spoke, Anchorage was cagey about what I could reveal regarding how its transaction validation system worked. With the new funding, it’s feeling a little more secure about its market position and was willing to share more.

Last time we spoke, Anchorage was cagey about what I could reveal regarding how its transaction validation system worked. With the new funding, it’s feeling a little more secure about its market position and was willing to share more.

Anchorage ditches usernames, passwords, email addresses and phone numbers completely. That way a hacker can’t just dump your coins into their account by stealing your private key or SIM-porting your number to their phone. Instead, clients whitelist devices held by their employees, who use the Anchorage app to submit transactions. You’d propose selling $10 million worth of Bitcoin or transferring it to someone else as payment, and a minimum of two-thirds of your designated co-workers would need to concur to form a quorum that approves the transfer.

But first, Anchorage’s artificial intelligence and human staff would check for any suspicious signals that might indicate a hack in progress. It uses behavioral analysis (do you act like a real human and similar to how you have before), biometric signals (do you look like you) and network signals (is your device what and where it should be) to confirm the transaction is legitimate. The same process goes down if you try to add a new whitelisted device or change who has permission to do what.

The challenge will be scaling security to an ever-broadening range of digital assets, each with their own blockchain quirks and complex smart contracts. Even if Anchorage keeps coins safely in custody, those variables could expose assets to risk while in transit. Now with deeper pockets and the Visa vote of confidence, Anchorage could solve those problems as clients line up.

While most blockchain attention has focused on the cryptocurrencies themselves and the exchanges where you can buy and sell them, a second order of critical infrastructure startups is emerging. Companies like Anchorage could make Bitcoin, Ether, Libra and more not just objects of speculation or the domain of experts, but safely functioning elements of the new world economy.

Powered by WPeMatico

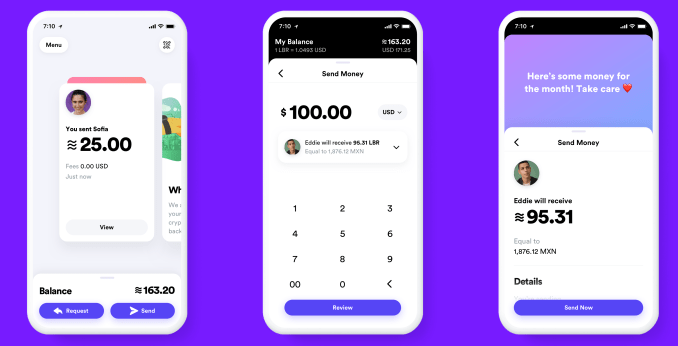

Facebook has finally revealed the details of its cryptocurrency, Libra, which will let you buy things or send money to people with nearly zero fees. You’ll pseudonymously buy or cash out your Libra online or at local exchange points like grocery stores, and spend it using interoperable third-party wallet apps or Facebook’s own Calibra wallet that will be built into WhatsApp, Messenger and its own app. Today Facebook released its white paper explaining Libra and its testnet for working out the kinks of its blockchain system before a public launch in the first half of 2020.

Facebook won’t fully control Libra, but instead get just a single vote in its governance like other founding members of the Libra Association, including Visa, Uber and Andreessen Horowitz, which have invested at least $10 million each into the project’s operations. The association will promote the open-sourced Libra Blockchain and developer platform with its own Move programming language, plus sign up businesses to accept Libra for payment and even give customers discounts or rewards.

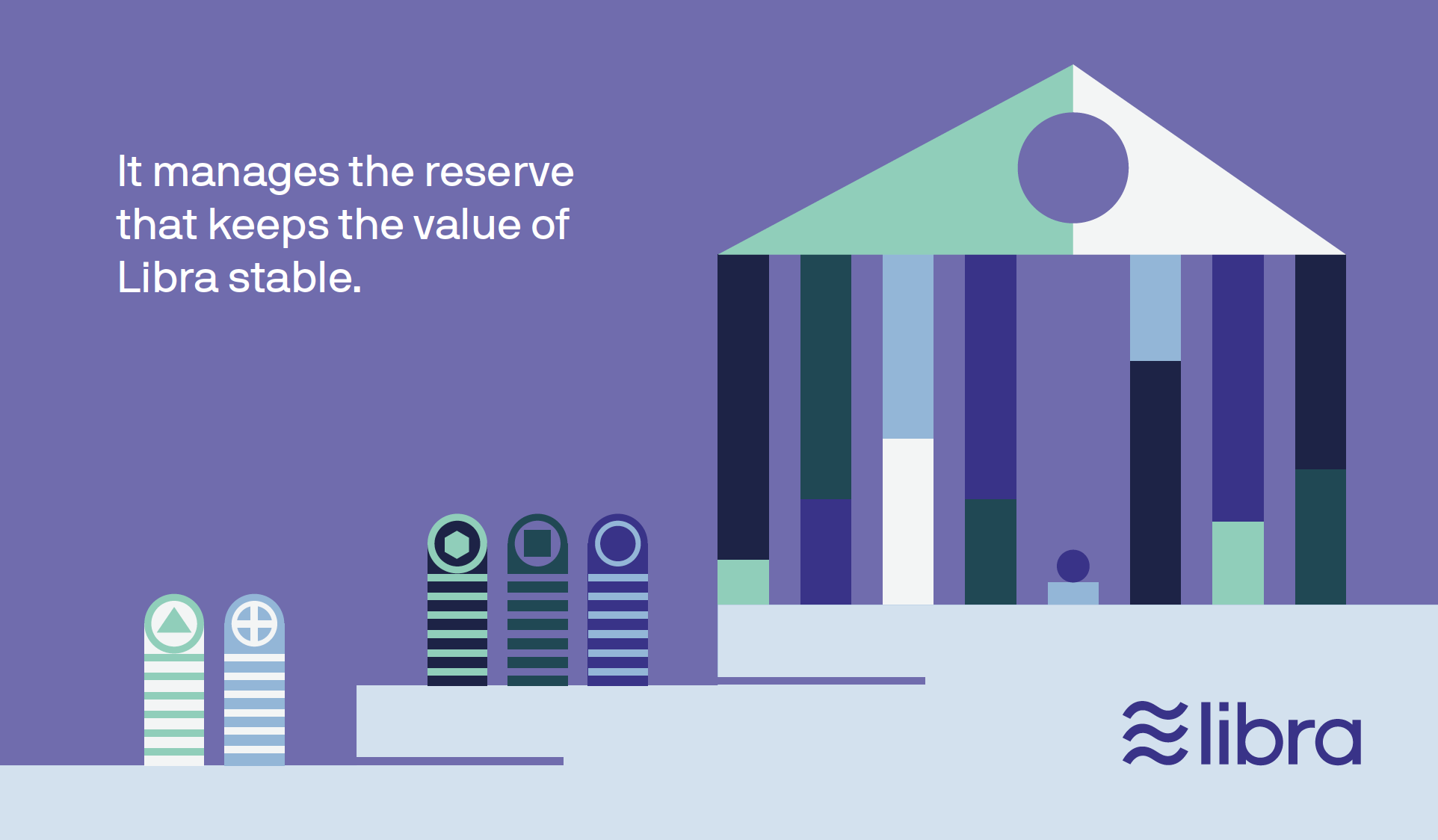

Facebook is launching a subsidiary company also called Calibra that handles its crypto dealings and protects users’ privacy by never mingling your Libra payments with your Facebook data so it can’t be used for ad targeting. Your real identity won’t be tied to your publicly visible transactions. But Facebook/Calibra and other founding members of the Libra Association will earn interest on the money users cash in that is held in reserve to keep the value of Libra stable.

Facebook’s audacious bid to create a global digital currency that promotes financial inclusion for the unbanked actually has more privacy and decentralization built in than many expected. Instead of trying to dominate Libra’s future or squeeze tons of cash out of it immediately, Facebook is instead playing the long-game by pulling payments into its online domain. Facebook’s VP of blockchain, David Marcus, explained the company’s motive and the tie-in with its core revenue source during a briefing at San Francisco’s historic Mint building. “If more commerce happens, then more small businesses will sell more on and off platform, and they’ll want to buy more ads on the platform so it will be good for our ads business.”

In cryptocurrencies, Facebook saw both a threat and an opportunity. They held the promise of disrupting how things are bought and sold by eliminating transaction fees common with credit cards. That comes dangerously close to Facebook’s ad business that influences what is bought and sold. If a competitor like Google or an upstart built a popular coin and could monitor the transactions, they’d learn what people buy and could muscle in on the billions spent on Facebook marketing. Meanwhile, the 1.7 billion people who lack a bank account might choose whoever offers them a financial services alternative as their online identity provider too. That’s another thing Facebook wants to be.

Yet existing cryptocurrencies like Bitcoin and Ethereum weren’t properly engineered to scale to be a medium of exchange. Their unanchored price was susceptible to huge and unpredictable swings, making it tough for merchants to accept as payment. And cryptocurrencies miss out on much of their potential beyond speculation unless there are enough places that will take them instead of dollars, and the experience of buying and spending them is easy enough for a mainstream audience. But with Facebook’s relationship with 7 million advertisers and 90 million small businesses plus its user experience prowess, it was well-poised to tackle this juggernaut of a problem.

Now Facebook wants to make Libra the evolution of PayPal . It’s hoping Libra will become simpler to set up, more ubiquitous as a payment method, more efficient with fewer fees, more accessible to the unbanked, more flexible thanks to developers and more long-lasting through decentralization.

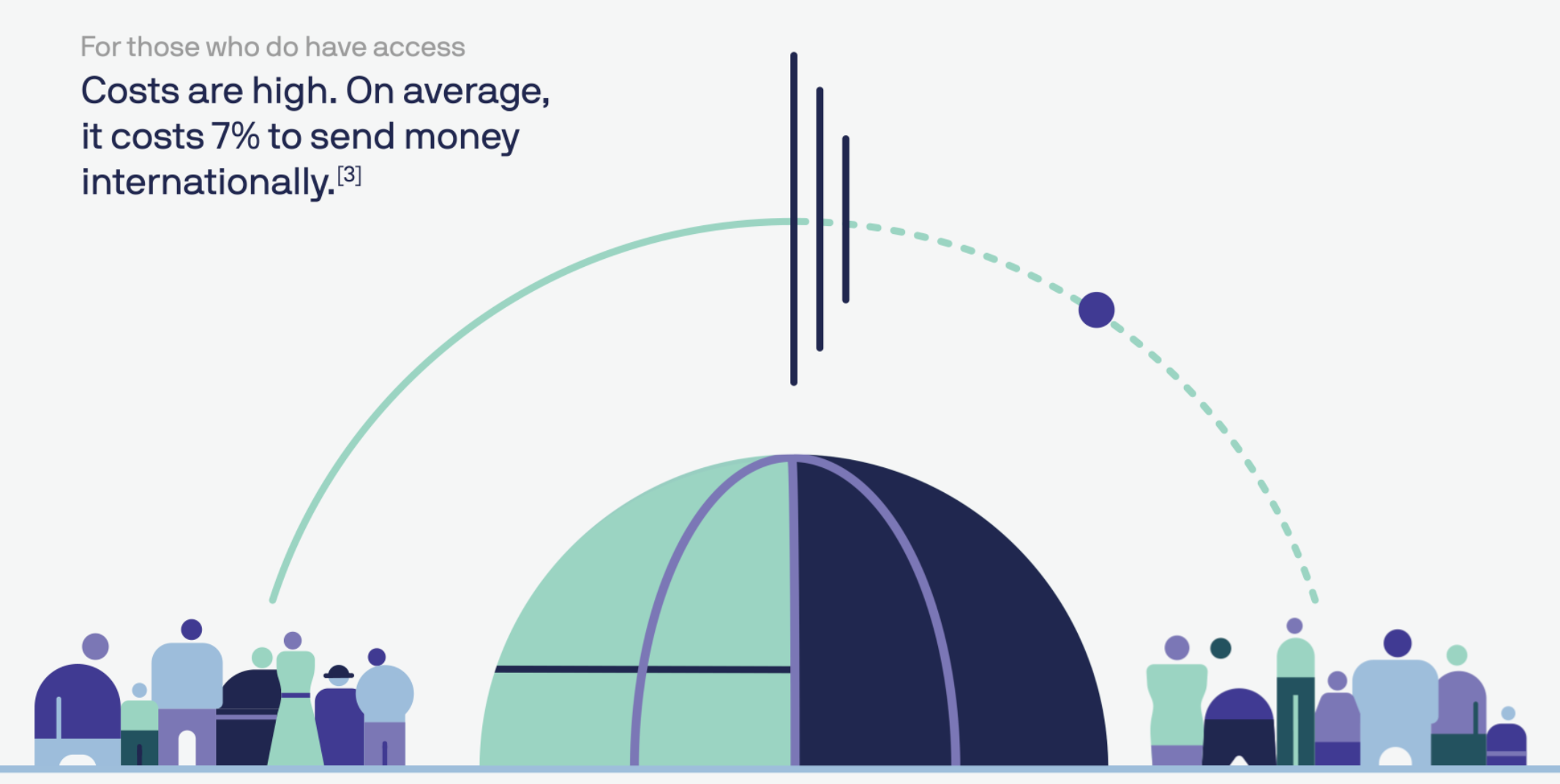

“Success will mean that a person working abroad has a fast and simple way to send money to family back home, and a college student can pay their rent as easily as they can buy a coffee,” Facebook writes in its Libra documentation. That would be a big improvement on today, when you’re stuck paying rent in insecure checks while exploitative remittance services charge an average of 7% to send money abroad, taking $50 billion from users annually. Libra could also power tiny microtransactions worth just a few cents that are infeasible with credit card fees attached, or replace your pre-paid transit pass.

…Or it could be globally ignored by consumers who see it as too much hassle for too little reward, or too unfamiliar and limited in use to pull them into the modern financial landscape. Facebook has built a reputation for over-engineered, underused products. It will need all the help it can get if wants to replace what’s already in our pockets.

By now you know the basics of Libra. Cash in a local currency, get Libra, spend them like dollars without big transaction fees or your real name attached, cash them out whenever you want. Feel free to stop reading and share this article if that’s all you care about. But the underlying technology, the association that governs it, the wallets you’ll use and the way payments work all have a huge amount of fascinating detail to them. Facebook has released more than 100 pages of documentation on Libra and Calibra, and we’ve pulled out the most important facts. Let’s dive in.

Facebook knew people wouldn’t trust it to wholly steer the cryptocurrency they use, and it also wanted help to spur adoption. So the social network recruited the founding members of the Libra Association, a not-for-profit which oversees the development of the token, the reserve of real-world assets that gives it value and the governance rules of the blockchain. “If we were controlling it, very few people would want to jump on and make it theirs,” says Marcus.

Each founding member paid a minimum of $10 million to join and optionally become a validator node operator (more on that later), gain one vote in the Libra Association council and be entitled to a share (proportionate to their investment) of the dividends from interest earned on the Libra reserve into which users pay fiat currency to receive Libra.

The 28 soon-to-be founding members of the association and their industries, previously reported by The Block’s Frank Chaparro, include:

Facebook says it hopes to reach 100 founding members before the official Libra launch and it’s open to anyone that meets the requirements, including direct competitors like Google or Twitter. The Libra Association is based in Geneva, Switzerland and will meet biannually. The country was chosen for its neutral status and strong support for financial innovation including blockchain technology.

To join the association, members must have a half rack of server space, a 100Mbps or above dedicated internet connection, a full-time site reliability engineer and enterprise-grade security. Businesses must hit two of three thresholds of a $1 billion USD market value or $500 million in customer balances, reach 20 million people a year and/or be recognized as a top 100 industry leader by a group like Interbrand Global or the S&P.

Crypto-focused investors must have more than $1 billion in assets under management, while Blockchain businesses must have been in business for a year, have enterprise-grade security and privacy and custody or staking greater than $100 million in assets. And only up to one-third of founding members can by crypto-related businesses or individually invited exceptions. Facebook also accepts research organizations like universities, and nonprofits fulfilling three of four qualities, including working on financial inclusion for more than five years, multi-national reach to lots of users, a top 100 designation by Charity Navigator or something like it and/or $50 million in budget.

The Libra Association will be responsible for recruiting more founding members to act as validator nodes for the blockchain, fundraising to jump-start the ecosystem, designing incentive programs to reward early adopters and doling out social impact grants. A council with a representative from each member will help choose the association’s managing director, who will appoint an executive team and elect a board of five to 19 top representatives.

Each member, including Facebook/Calibra, will only get up to one vote or 1% of the total vote (whichever is larger) in the Libra Association council. This provides a level of decentralization that protects against Facebook or any other player hijacking Libra for its own gain. By avoiding sole ownership and dominion over Libra, Facebook could avoid extra scrutiny from regulators who are already investigating it for a sea of privacy abuses as well as potentially anti-competitive behavior. In an attempt to preempt criticism from lawmakers, the Libra Association writes, “We welcome public inquiry and accountability. We are committed to a dialogue with regulators and policymakers. We share policymakers’ interest in the ongoing stability of national currencies.”

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

The name Libra comes from the word for a Roman unit of weight measure. It’s trying to invoke a sense of financial freedom by playing on the French stem “Lib,” meaning free.

The Libra Association is still hammering out the exact start value for the Libra, but it’s meant to be somewhere close to the value of a dollar, euro or pound so it’s easy to conceptualize. That way, a gallon of milk in the U.S. might cost 3 to 4 Libra, similar but not exactly the same as with dollars.

The idea is that you’ll cash in some money and keep a balance of Libra that you can spend at accepting merchants and online services. You’ll be able to trade in your local currency for Libra and vice versa through certain wallet apps, including Facebook’s Calibra, third-party wallet apps and local resellers like convenience or grocery stores where people already go to top-up their mobile data plan.

Each time someone cashes in a dollar or their respective local currency, that money goes into the Libra Reserve and an equivalent value of Libra is minted and doled out to that person. If someone cashes out from the Libra Association, the Libra they give back are destroyed/burned and they receive the equivalent value in their local currency back. That means there’s always 100% of the value of the Libra in circulation, collateralized with real-world assets in the Libra Reserve. It never runs fractional. And unliked “pegged” stable coins that are tied to a single currency like the USD, Libra maintains its own value — though that should cash out to roughly the same amount of a given currency over time.

When Libra Association members join and pay their $10 million minimum, they receive Libra Investment Tokens. Their share of the total tokens translates into the proportion of the dividend they earn off of interest on assets in the reserve. Those dividends are only paid out after Libra Association uses interest to pay for operating expenses, investments in the ecosystem, engineering research and grants to nonprofits and other organizations. This interest is part of what attracted the Libra Association’s members. If Libra becomes popular and many people carry a large balance of the currency, the reserve will grow huge and earn significant interest.

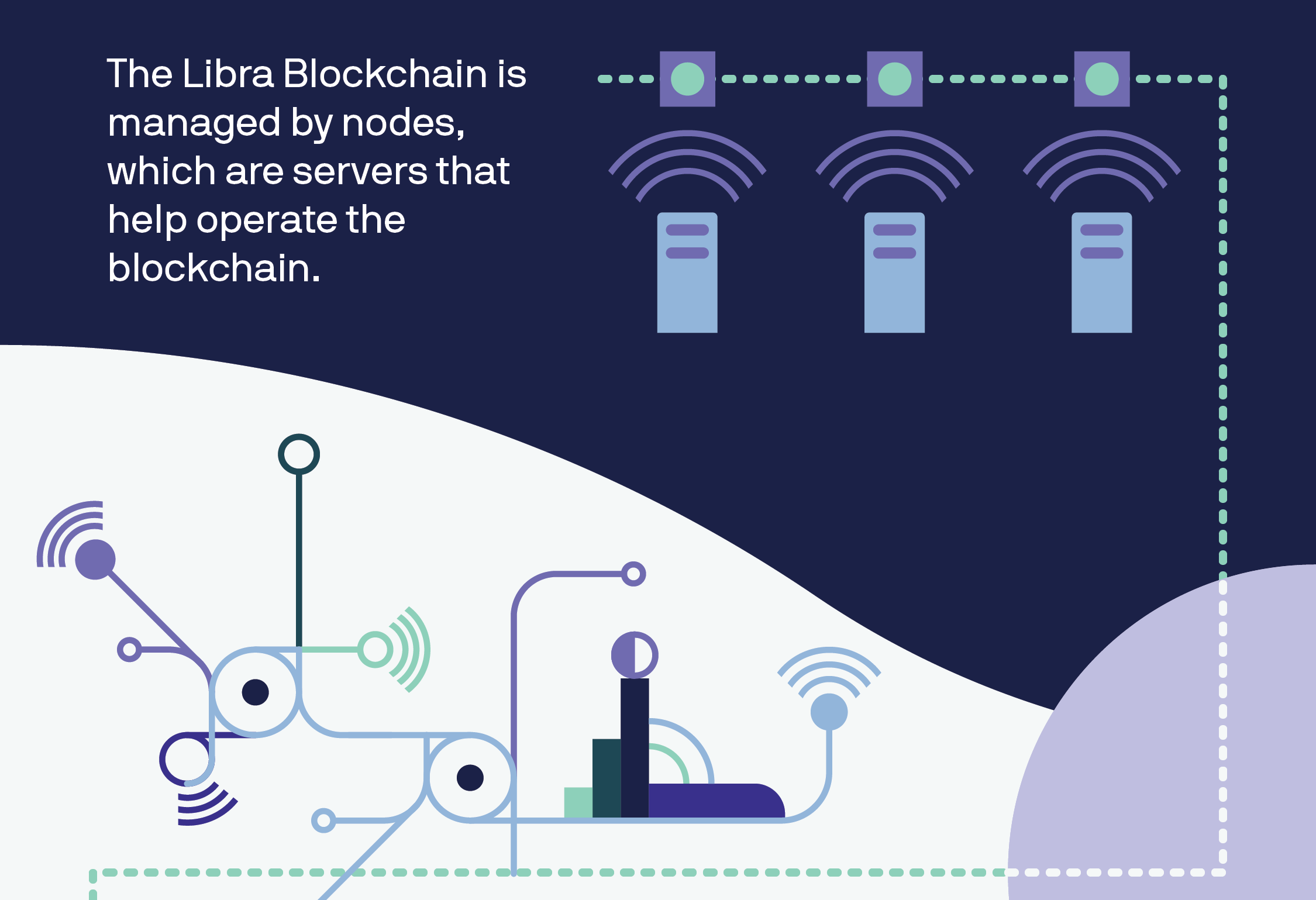

Every Libra payment is permanently written into the Libra Blockchain — a cryptographically authenticated database that acts as a public online ledger designed to handle 1,000 transactions per second. That would be much faster than Bitcoin’s 7 transactions per second or Ethereum’s 15. The blockchain is operated and constantly verified by founding members of the Libra Association, which each invested $10 million or more for a say in the cryptocurrency’s governance and the ability to operate a validator node.

When a transaction is submitted, each of the nodes runs a calculation based on the existing ledger of all transactions. Thanks to a Byzantine Fault Tolerance system, just two-thirds of the nodes must come to consensus that the transaction is legitimate for it to be executed and written to the blockchain. A structure of Merkle Trees in the code makes it simple to recognize changes made to the Libra Blockchain. With 5KB transactions, 1,000 verifications per second on commodity CPUs and up to 4 billion accounts, the Libra Blockchain should be able to operate at 1,000 transactions per second if nodes use at least 40Mbps connections and 16TB SSD hard drives.

Transactions on Libra cannot be reversed. If an attack compromises over one-third of the validator nodes causing a fork in the blockchain, the Libra Association says it will temporarily halt transactions, figure out the extent of the damage and recommend software updates to resolve the fork.

Transactions aren’t entirely free. They incur a tiny fraction of a cent fee to pay for “gas” that covers the cost of processing the transfer of funds similar to with Ethereum. This fee will be negligible to most consumers, but when they add up, the gas charges will deter bad actors from creating millions of transactions to power spam and denial-of-service attacks. “We’ve purposely tried not to innovate massively on the blockchain itself because we want it to be scalable and secure,” says Marcus of piggybacking on the best elements of existing cryptocurrencies.

Currently, the Libra Blockchain is what’s known as “permissioned,” where only entities that fulfill certain requirements are admitted to a special in-group that defines consensus and controls governance of the blockchain. The problem is this structure is more vulnerable to attacks and censorship because it’s not truly decentralized. But during Facebook’s research, it couldn’t find a reliable permissionless structure that could securely scale to the number of transactions Libra will need to handle. Adding more nodes slows things down, and no one has proven a way to avoid that without compromising security.

That’s why the Libra Association’s goal is to move to a permissionless system based on proof-of-stake that will protect against attacks by distributing control, encourage competition and lower the barrier to entry. It wants to have at least 20% of votes in the Libra Association council coming from node operators based on their total Libra holdings instead of their status as a founding member. That plan should help appease blockchain purists who won’t be satisfied until Libra is completely decentralized.

The Libra Blockchain is open source with an Apache 2.0 license, and any developer can build apps that work with it using the Move coding language. The blockchain’s prototype launches its testnet today, so it’s effectively in developer beta mode until it officially launches in the first half of 2020. The Libra Association is working with HackerOne to launch a bug bounty system later this year that will pay security researchers for safely identifying flaws and glitches. In the meantime, the Libra Association is implementing the Libra Core using the Rust programming language because it’s designed to prevent security vulnerabilities, and the Move language isn’t fully ready yet.

Move was created to make it easier to write blockchain code that follows an author’s intent without introducing bugs. It’s called Move because its primary function is to move Libra coins from one account to another, and never let those assets be accidentally duplicated. The core transaction code looks like: LibraAccount.pay_from_sender(recipient_address, amount) procedure.

Eventually, Move developers will be able to create smart contracts for programmatic interactions with the Libra Blockchain. Until Move is ready, developers can create modules and transaction scripts for Libra using Move IR, which is high-level enough to be human-readable but low-level enough to be translatable into real Move bytecode that’s written to the blockchain.

The Libra ecosystem and the Move language will be completely open to use and build, which presents a sizable risk. Crooked developers could prey on crypto novices, claiming their app works just the same as legitimate ones, and that it’s safe because it uses Libra. But if consumers get ripped off by these scammers, the anger will surely bubble up to Facebook. Yet still, Calibra’s head of product tells me, “There are no plans for the Libra Association to take a role in actively vetting [developers],” Calibra’s head of product Kevin Weil tells me.

Even though it’s tried to distance itself sufficiently via its subsidiary Libra and the association, many people will probably always think of Libra as Facebook’s cryptocurrency and blame it for their woes.

Read our full story on the dangers of Libra’s unvetted developer platform

The Libra Association wants to encourage more developers and merchants to work with its cryptocurrency. That’s why it plans to issue incentives, possibly Libra coins, to validator node operators who can get people signed up for and using Libra. Wallets that pull users through the Know Your Customer anti-fraud and money laundering process or that keep users sufficiently active for over a year will be rewarded. For each transaction they process, merchants will also receive a percentage of the transaction back.

Businesses that earn these incentives can keep them, or pass some or all of them along to users in the form of free Libra tokens or discounts on their purchases. This could create competition between wallets to see which can pass on the most rewards to their customers, and thereby attract the most users. You could imagine eBay or Spotify giving you a discount for paying in Libra, while wallet developers might offer you free tokens if you complete 100 transactions within a year.

“One challenge for Spotify and its users around the world has been the lack of easily accessible payment systems – especially for those in financially underserved markets,” Spotify’s Chief Premium Business Officer Alex Norström writes. “In joining the Libra Association, there is an opportunity to better reach Spotify’s total addressable market, eliminate friction and enable payments in mass scale.”

This savvy incentive system should massively help ratchet up Libra’s user count without dictating how businesses balance their margins versus growth. Facebook also has another plan to grow its developer ecosystem. By offering venture capital firms like Andreessen Horowitz and Union Square Ventures a portion of the reserve interest, they’re motivating to fund startups building Libra infrastructure.

So how do you actually own and spend Libra? Through Libra wallets like Facebook’s own Calibra and others that will be built by third-parties, potentially including Libra Association members like PayPal. The idea is to make sending money to a friend or paying for something as easy as sending a Facebook Message. You won’t be able to make or receive any real payments until the official launch next year, though, but you can sign up for early access when it’s ready here.

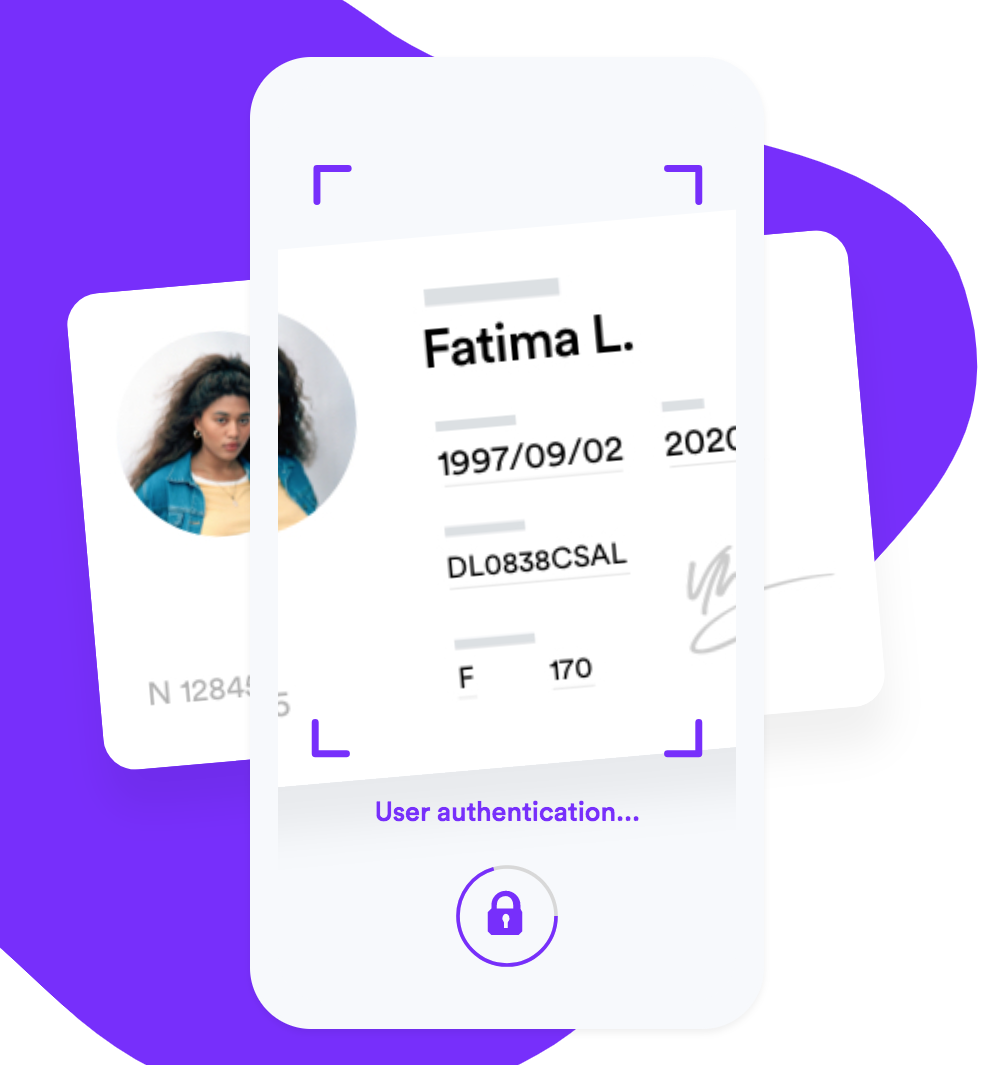

None of the Libra Association members agreed to provide details on what exactly they’ll build on the blockchain, but we can take Facebook’s Calibra wallet as an example of the basic experience. Calibra will launch alongside the Libra currency on iOS and Android within Facebook Messenger, WhatsApp and a standalone app. When users first sign up, they’ll be taken through a Know Your Customer anti-fraud process where they’ll have to provide a government-issued photo ID and other verification info. They’ll need to conduct due diligence on customers and report suspicious activity to the authorities.

From there you’ll be able to cash in to Libra, pick a friend or merchant, set an amount to send them and add a description and send them Libra. You’ll also be able to request Libra, and Calibra will offer an expedited way of paying merchants by scanning your or their QR code. Eventually it wants to offer in-store payments and integrations with point-of-sale systems like Square.

The Libra Association’s e-commerce members seem particularly excited about how the token could eliminate transaction fees and speed up checkout. “We believe blockchain will benefit the luxury industry by improving IP protection, transparency in the product life cycle and — as in the case of Libra — enable global frictionless e-commerce,” says FarFetch CEO Jose Neves.

Facebook CEO Mark Zuckerberg explained some of the philosophy behind Libra and Calibra in a post today. “It’s decentralized — meaning it’s run by many different organizations instead of just one, making the system fairer overall. It’s available to anyone with an internet connection and has low fees and costs. And it’s secured by cryptography which helps keep your money safe. This is an important part of our vision for a privacy-focused social platform — where you can interact in all the ways you’d want privately, from messaging to secure payments.”

By default, Facebook won’t import your contacts or any of your profile information, but may ask if you wish to do so. It also won’t share any of your transaction data back to Facebook, so it won’t be used to target you with ads, rank your News Feed, or otherwise earn Facebook money directly. Data will only be shared in specific instances in anonymized ways for research or adoption measurement, for hunting down fraudsters or due to a request from law enforcement. And you don’t even need a Facebook or WhatsApp account to sign up for Calibra or to use Libra.

“We realize people don’t want their social data and financial data commingled,” says Marcus, who’s now head of Calibra. “The reality is we’ll have plenty of wallets that will compete with us and many of them will not be in social, and if we want to successfully win people’s trust, we have to make sure the data will be separated.”

In case you are hacked, scammed or lose access to your account, Calibra will refund you for lost coins when possible through 24/7 chat support because it’s a custodial wallet. You also won’t have to remember any long, complex crypto passwords you could forget and get locked out from your money, as Calibra manages all your keys for you. Given Calibra will likely become the default wallet for many Libra users, this extra protection and smoother user experience is essential.

For now, Calibra won’t make money. But Calibra’s head of product Kevin Weil tells me that if it reaches scale, Facebook could launch other financial tools through Calibra that it could monetize, such as investing or lending. “In time, we hope to offer additional services for people and businesses, such as paying bills with the push of a button, buying a cup of coffee with the scan of a code or riding your local public transit without needing to carry cash or a metro pass,” the Calibra team writes. That makes it start to sound a lot like China’s everything app WeChat.

Facebook got one thing right for sure: Today’s money doesn’t work for everyone. Those of us living comfortably in developed nations likely don’t see the hardships that befall migrant workers or the unbanked abroad. Preyed on by greedy payday lenders and high-fee remittance services, targeted by muggers and left out of traditional financial services, the poor get poorer. Libra has the potential to get more money from working parents back to their families and help people retain credit even if they’re robbed of their physical possessions. That would do more to accomplish Facebook’s mission of making the world feel smaller than all the News Feed Likes combined.

If Facebook succeeds and legions of people cash in money for Libra, it and the other founding members of the Libra Association could earn big dividends on the interest. And if suddenly it becomes super quick to buy things through Facebook using Libra, businesses will boost their ad spend there. But if Libra gets hacked or proves unreliable, it could cost lots of people around the world money while souring them on cryptocurrencies. And by offering an open Libra platform, shady developers could build apps that snatch not just people’s personal info like Cambridge Analytica, but their hard-earned digital cash.

Facebook just tried to reinvent money. Next year, we’ll see if the Libra Association can pull it off. It took me 4,000 words to explain Libra, but at least now you can make up your own mind about whether to be scared of Facebook crypto.

Powered by WPeMatico

I’m not allowed to tell you exactly how Anchorage keeps rich institutions from being robbed of their cryptocurrency, but the off-the-record demo was damn impressive. Judging by the $17 million Series A this security startup raised last year led by Andreessen Horowitz and joined by Khosla Ventures, #Angels, Max Levchin, Elad Gil, Mark McCombe of Blackrock and AngelList’s Naval Ravikant, I’m not the only one who thinks so. In fact, crypto funds like Andreessen’s a16z crypto, Paradigm and Electric Capital are already using it.

They’re trusting in the guys who engineered Square’s first encrypted card reader and Docker’s security protocols. “It’s less about us choosing this space and more about this space choosing us. If you look at our backgrounds and you look at the problem, it’s like the universe handed us on a silver platter the Venn diagram of our skill set,” co-founder Diogo Monica tells me.

![]()

Today, Anchorage is coming out of stealth and launching its cryptocurrency custody service to the public. Anchorage holds and safeguards crypto assets for institutions like hedge funds and venture firms, and only allows transactions verified by an array of biometrics, behavioral analysis and human reviewers. And because it doesn’t use “buried in the backyard” cold storage, asset holders can actually earn rewards and advantages for participating in coin-holder votes without fear of getting their Bitcoin, Ethereum or other coins stolen.

The result is a crypto custody service that could finally lure big-time commercial banks, endowments, pensions, mutual funds and hedgies into the blockchain world. Whether they seek short-term gains off of crypto volatility or want to HODL long-term while participating in coin governance, Anchorage promises to protect them.

Anchorage’s story starts eight years ago when Monica and his co-founder Nathan McCauley met after joining Square the same week. Monica had been getting a PhD in distributed systems while McCauley designed anti-reverse engineering tech to keep U.S. military data from being extracted from abandoned tanks or jets. After four years of building systems that would eventually move more than $80 billion per year in credit card transactions, they packaged themselves as a “pre-product acqui-hire” Monica tells me, and they were snapped up by Docker.

As their reputation grew from work and conference keynotes, cryptocurrency funds started reaching out for help with custody of their private keys. One had lost a passphrase and the $1 million in currency it was protecting in a display of jaw-dropping ignorance. The pair realized there were no true standards in crypto custody, so they got to work on Anchorage.

“You look at the status quo and it was and still is cold storage. It’s the same technology used by pirates in the 1700s,” Monica explains. “You bury your crypto in a treasure chest and then you make a treasure map of where those gold coins are,” except with USB keys, security deposit boxes and checklists. “We started calling it Pirate Custody.” Anchorage set out to develop something better — a replacement for usernames and passwords or even phone numbers and two-factor authentication that could be misplaced or hijacked.

This led them to Andreessen Horowitz partner and a16z crypto leader Chris Dixon, who’s now on their board. “We’ve been buying crypto assets running back to Bitcoin for years now here at a16z crypto. [Once you’re holding crypto,] it’s hard to do it in a way that’s secure, regulatory compliant, and lets you access it. We felt this pain point directly.”

Andreessen Horowitz partner and Anchorage board member Chris Dixon

It’s at this point in the conversation when Monica and McCauley give me their off-the-record demo. While there are no screenshots to share, the enterprise security suite they’ve built has the polish of a consumer app like Robinhood. What I can say is that Anchorage works with clients to whitelist employees’ devices. It then uses multiple types of biometric signals and behavioral analytics about the person and device trying to log in to verify their identity.

But even once they have access, Anchorage is built around quorum-based approvals. Withdrawals, other transactions and even changing employee permissions requires approval from multiple users inside the client company. They could set up Anchorage so it requires five of seven executives’ approval to pull out assets. And finally, outlier detection algorithms and a human review the transaction to make sure it looks legit. A hacker or rogue employee can’t steal the funds even if they’re logged in because they need consensus of approval.

That kind of assurance means institutional investors can confidently start to invest in crypto assets. That swell of capital could help replace the retreating consumer investors who’ve fled the market this year, leading to massive price drops. The liquidity provided by these asset managers could keep the whole blockchain industry moving. “Institutional investing has had centuries to build up a set of market infrastructure. Custody was something that for other asset classes was solved hundreds of years ago, so it’s just now catching up [for crypto],” says McCauley. “We’re creating a bigger market in and of itself,” Monica adds.

With Anchorage steadfastly handling custody, the risk these co-founders admit worries them lies in the smart contracts that govern the cryptocurrencies themselves. “We need to be extremely wide in our level of support and extremely deep because each blockchain has details of implementation. This is inherently a very difficult problem,” McCauley explains. It doesn’t matter if the coins are safe in Anchorage’s custody if a janky smart contract can botch their transfer.

There are plenty of startups vying to offer crypto custody, ranging from Bitgo and Ledger to well-known names like Coinbase and Gemini. Yet Anchorage offers a rare combination of institutional-since-day-one security rigor with the ability to participate in votes and governance of crypto assets that’s impossible if they’re in cold storage. Down the line, Anchorage hints that it might serve clients recommendations for how to vote to maximize their yield and preserve the sanctity of their coin.

They’ll have crypto investment legend Chris Dixon on their board to guide them. “What you’ll see is in the same way that institutional investors want to buy stock in Facebook and Google and Netflix, they’ll want to buy the equivalent in the world 10 years from now and do that safely,” Dixon tells me. “Anchorage will be that layer for them.”

But why do the Anchorage founders care so much about the problem? McCauley concludes that, “When we look at what’s potentially possible with crypto, there a fundamentally more accessible economy. We view ourselves as a key component of bringing that future forward.”

Powered by WPeMatico