Amazon

Auto Added by WPeMatico

Auto Added by WPeMatico

Fifteen years ago this week on August 25, 2006, AWS turned on the very first beta instance of EC2, its cloud-based virtual computers. Today cloud computing, and more specifically infrastructure as a service, is a staple of how businesses use computing, but at that moment it wasn’t a well known or widely understood concept.

The EC in EC2 stands for Elastic Compute, and that name was chosen deliberately. The idea was to provide as much compute power as you needed to do a job, then shut it down when you no longer needed it — making it flexible like an elastic band. The launch of EC2 in beta was preceded by the beta release of S3 storage six months earlier, and both services marked the starting point in AWS’ cloud infrastructure journey.

You really can’t overstate what Amazon was able to accomplish with these moves. It was able to anticipate an entirely different way of computing and create a market and a substantial side business in the process. It took vision to recognize what was coming and the courage to forge ahead and invest the resources necessary to make it happen, something that every business could learn from.

The AWS origin story is complex, but it was about bringing the IT power of the Amazon business to others. Amazon at the time was not the business it is today, but it was still rather substantial and still had to deal with massive fluctuations in traffic such as Black Friday when its website would be flooded with traffic for a short but sustained period of time. While the goal of an e-commerce site, and indeed every business, is attracting as many customers as possible, keeping the site up under such stress takes some doing and Amazon was learning how to do that well.

Those lessons and a desire to bring the company’s internal development processes under control would eventually lead to what we know today as Amazon Web Services, and that side business would help fuel a whole generation of startups. We spoke to Dave Brown, who is VP of EC2 today, and who helped build the first versions of the tech, to find out how this technological shift went down.

The genesis of the idea behind AWS started in the 2000 timeframe when the company began looking at creating a set of services to simplify how they produced software internally. Eventually, they developed a set of foundational services — compute, storage and database — that every developer could tap into.

But the idea of selling that set of services really began to take shape at an executive offsite at Jeff Bezos’ house in 2003. A 2016 TechCrunch article on the origins AWS described how that started to come together:

As the team worked, Jassy recalled, they realized they had also become quite good at running infrastructure services like compute, storage and database (due to those previously articulated internal requirements). What’s more, they had become highly skilled at running reliable, scalable, cost-effective data centers out of need. As a low-margin business like Amazon, they had to be as lean and efficient as possible.

They realized that those skills and abilities could translate into a side business that would eventually become AWS. It would take a while to put these initial ideas into action, but by December 2004, they had opened an engineering office in South Africa to begin building what would become EC2. As Brown explains it, the company was looking to expand outside of Seattle at the time, and Chris Pinkham, who was director in those days, hailed from South Africa and wanted to return home.

Powered by WPeMatico

Facebook is a monopoly. Right?

Mark Zuckerberg appeared on national TV today to make a “special announcement.” The timing could not be more curious: Today is the day Lina Khan’s FTC refiled its case to dismantle Facebook’s monopoly.

To the average person, Facebook’s monopoly seems obvious. “After all,” as James E. Boasberg of the U.S. District Court for the District of Columbia put it in his recent decision, “No one who hears the title of the 2010 film ‘The Social Network’ wonders which company it is about.” But obviousness is not an antitrust standard. Monopoly has a clear legal meaning, and thus far Lina Khan’s FTC has failed to meet it. Today’s refiling is much more substantive than the FTC’s first foray. But it’s still lacking some critical arguments. Here are some ideas from the front lines.

To the average person, Facebook’s monopoly seems obvious. But obviousness is not an antitrust standard.

First, the FTC must define the market correctly: personal social networking, which includes messaging. Second, the FTC must establish that Facebook controls over 60% of the market — the correct metric to establish this is revenue.

Though consumer harm is a well-known test of monopoly determination, our courts do not require the FTC to prove that Facebook harms consumers to win the case. As an alternative pleading, though, the government can present a compelling case that Facebook harms consumers by suppressing wages in the creator economy. If the creator economy is real, then the value of ads on Facebook’s services is generated through the fruits of creators’ labor; no one would watch the ads before videos or in between posts if the user-generated content was not there. Facebook has harmed consumers by suppressing creator wages.

A note: This is the first of a series on the Facebook monopoly. I am inspired by Cloudflare’s recent post explaining the impact of Amazon’s monopoly in their industry. Perhaps it was a competitive tactic, but I genuinely believe it more a patriotic duty: guideposts for legislators and regulators on a complex issue. My generation has watched with a combination of sadness and trepidation as legislators who barely use email question the leading technologists of our time about products that have long pervaded our lives in ways we don’t yet understand. I, personally, and my company both stand to gain little from this — but as a participant in the latest generation of social media upstarts, and as an American concerned for the future of our democracy, I feel a duty to try.

According to the court, the FTC must meet a two-part test: First, the FTC must define the market in which Facebook has monopoly power, established by the D.C. Circuit in Neumann v. Reinforced Earth Co. (1986). This is the market for personal social networking services, which includes messaging.

Second, the FTC must establish that Facebook controls a dominant share of that market, which courts have defined as 60% or above, established by the 3rd U.S. Circuit Court of Appeals in FTC v. AbbVie (2020). The right metric for this market share analysis is unequivocally revenue — daily active users (DAU) x average revenue per user (ARPU). And Facebook controls over 90%.

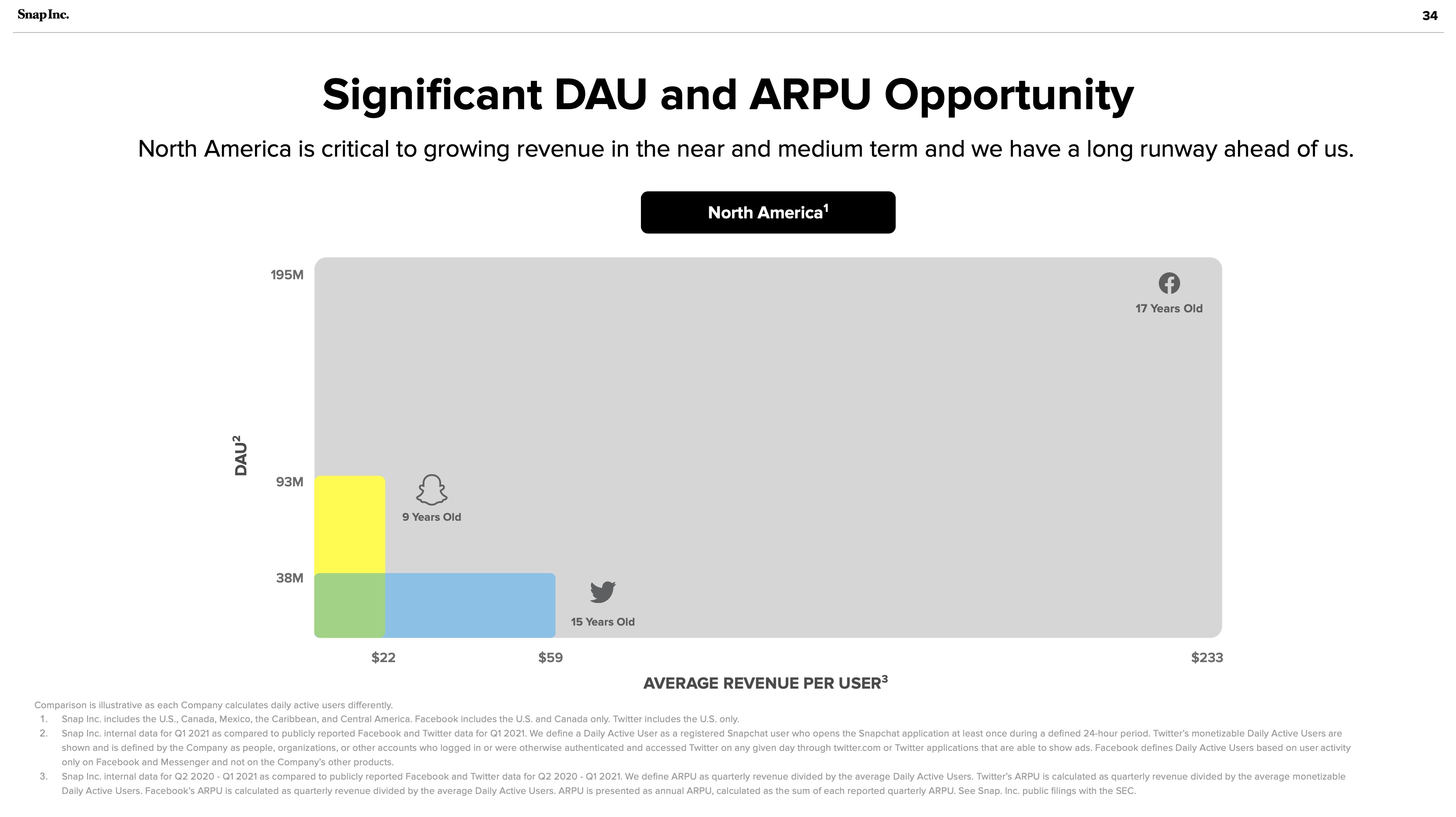

The answer to the FTC’s problem is hiding in plain sight: Snapchat’s investor presentations:

Snapchat July 2021 investor presentation: Significant DAU and ARPU Opportunity. Image Credits: Snapchat

This is a chart of Facebook’s monopoly — 91% of the personal social networking market. The gray blob looks awfully like a vast oil deposit, successfully drilled by Facebook’s Standard Oil operations. Snapchat and Twitter are the small wildcatters, nearly irrelevant compared to Facebook’s scale. It should not be lost on any market observers that Facebook once tried to acquire both companies.

The FTC initially claimed that Facebook has a monopoly of the “personal social networking services” market. The complaint excluded “mobile messaging” from Facebook’s market “because [messaging apps] (i) lack a ‘shared social space’ for interaction and (ii) do not employ a social graph to facilitate users’ finding and ‘friending’ other users they may know.”

This is incorrect because messaging is inextricable from Facebook’s power. Facebook demonstrated this with its WhatsApp acquisition, promotion of Messenger and prior attempts to buy Snapchat and Twitter. Any personal social networking service can expand its features — and Facebook’s moat is contingent on its control of messaging.

The more time in an ecosystem the more valuable it becomes. Value in social networks is calculated, depending on whom you ask, algorithmically (Metcalfe’s law) or logarithmically (Zipf’s law). Either way, in social networks, 1+1 is much more than 2.

Social networks become valuable based on the ever-increasing number of nodes, upon which companies can build more features. Zuckerberg coined the “social graph” to describe this relationship. The monopolies of Line, Kakao and WeChat in Japan, Korea and China prove this clearly. They began with messaging and expanded outward to become dominant personal social networking behemoths.

In today’s refiling, the FTC explains that Facebook, Instagram and Snapchat are all personal social networking services built on three key features:

Unfortunately, this is only partially right. In social media’s treacherous waters, as the FTC has struggled to articulate, feature sets are routinely copied and cross-promoted. How can we forget Instagram’s copying of Snapchat’s stories? Facebook has ruthlessly copied features from the most successful apps on the market from inception. Its launch of a Clubhouse competitor called Live Audio Rooms is only the most recent example. Twitter and Snapchat are absolutely competitors to Facebook.

Messaging must be included to demonstrate Facebook’s breadth and voracious appetite to copy and destroy. WhatsApp and Messenger have over 2 billion and 1.3 billion users respectively. Given the ease of feature copying, a messaging service of WhatsApp’s scale could become a full-scale social network in a matter of months. This is precisely why Facebook acquired the company. Facebook’s breadth in social media services is remarkable. But the FTC needs to understand that messaging is a part of the market. And this acknowledgement would not hurt their case.

Boasberg believes revenue is not an apt metric to calculate personal networking: “The overall revenues earned by PSN services cannot be the right metric for measuring market share here, as those revenues are all earned in a separate market — viz., the market for advertising.” He is confusing business model with market. Not all advertising is cut from the same cloth. In today’s refiling, the FTC correctly identifies “social advertising” as distinct from the “display advertising.”

But it goes off the deep end trying to avoid naming revenue as the distinguishing market share metric. Instead the FTC cites “time spent, daily active users (DAU), and monthly active users (MAU).” In a world where Facebook Blue and Instagram compete only with Snapchat, these metrics might bring Facebook Blue and Instagram combined over the 60% monopoly hurdle. But the FTC does not make a sufficiently convincing market definition argument to justify the choice of these metrics. Facebook should be compared to other personal social networking services such as Discord and Twitter — and their correct inclusion in the market would undermine the FTC’s choice of time spent or DAU/MAU.

Ultimately, cash is king. Revenue is what counts and what the FTC should emphasize. As Snapchat shows above, revenue in the personal social media industry is calculated by ARPU x DAU. The personal social media market is a different market from the entertainment social media market (where Facebook competes with YouTube, TikTok and Pinterest, among others). And this too is a separate market from the display search advertising market (Google). Not all advertising-based consumer technology is built the same. Again, advertising is a business model, not a market.

In the media world, for example, Netflix’s subscription revenue clearly competes in the same market as CBS’ advertising model. News Corp.’s acquisition of Facebook’s early competitor MySpace spoke volumes on the internet’s potential to disrupt and destroy traditional media advertising markets. Snapchat has chosen to pursue advertising, but incipient competitors like Discord are successfully growing using subscriptions. But their market share remains a pittance compared to Facebook.

The FTC has correctly argued for the smallest possible market for their monopoly definition. Personal social networking, of which Facebook controls at least 80%, should not (in their strongest argument) include entertainment. This is the narrowest argument to make with the highest chance of success.

But they could choose to make a broader argument in the alternative, one that takes a bigger swing. As Lina Khan famously noted about Amazon in her 2017 note that began the New Brandeis movement, the traditional economic consumer harm test does not adequately address the harms posed by Big Tech. The harms are too abstract. As White House advisor Tim Wu argues in “The Curse of Bigness,” and Judge Boasberg acknowledges in his opinion, antitrust law does not hinge solely upon price effects. Facebook can be broken up without proving the negative impact of price effects.

However, Facebook has hurt consumers. Consumers are the workers whose labor constitutes Facebook’s value, and they’ve been underpaid. If you define personal networking to include entertainment, then YouTube is an instructive example. On both YouTube and Facebook properties, influencers can capture value by charging brands directly. That’s not what we’re talking about here; what matters is the percent of advertising revenue that is paid out to creators.

YouTube’s traditional percentage is 55%. YouTube announced it has paid $30 billion to creators and rights holders over the last three years. Let’s conservatively say that half of the money goes to rights holders; that means creators on average have earned $15 billion, which would mean $5 billion annually, a meaningful slice of YouTube’s $46 billion in revenue over that time. So in other words, YouTube paid creators a third of its revenue (this admittedly ignores YouTube’s non-advertising revenue).

Facebook, by comparison, announced just weeks ago a paltry $1 billion program over a year and change. Sure, creators may make some money from interstitial ads, but Facebook does not announce the percentage of revenue they hand to creators because it would be insulting. Over the equivalent three-year period of YouTube’s declaration, Facebook has generated $210 billion in revenue. one-third of this revenue paid to creators would represent $70 billion, or $23 billion a year.

Why hasn’t Facebook paid creators before? Because it hasn’t needed to do so. Facebook’s social graph is so large that creators must post there anyway — the scale afforded by success on Facebook Blue and Instagram allows creators to monetize through directly selling to brands. Facebooks ads have value because of creators’ labor; if the users did not generate content, the social graph would not exist. Creators deserve more than the scraps they generate on their own. Facebook suppresses creators’ wages because it can. This is what monopolies do.

Facebook has long been the Standard Oil of social media, using its core monopoly to begin its march upstream and down. Zuckerberg announced in July and renewed his focus today on the metaverse, a market Roblox has pioneered. After achieving a monopoly in personal social media and competing ably in entertainment social media and virtual reality, Facebook’s drilling continues. Yes, Facebook may be free, but its monopoly harms Americans by stifling creator wages. The antitrust laws dictate that consumer harm is not a necessary condition for proving a monopoly under the Sherman Act; monopolies in and of themselves are illegal. By refiling the correct market definition and marketshare, the FTC stands more than a chance. It should win.

A prior version of this article originally appeared on Substack.

Powered by WPeMatico

Cart.com, a Houston-based company providing end-to-end e-commerce services, brought in its third funding round this year, this time a $98 million Series B round to bring its total funding to $143 million.

Oak HC/FT led the new round of funding and was joined by PayPal Ventures, Clearco, G9 Ventures, Mercury Fund, Valedor Partners and Arsenal Growth. Strategic investors in the Series B include Heyday CEO Sebastian Rymarz and Casper CEO Philip Krim. This new round follows a $25 million Series A round, led by Mercury and Arsenal in July, and a $20 million seed round from Bearing Ventures.

Cart.com CEO Omair Tariq, who was previously an executive at Home Depot and COO of Blinds.com, co-founded the company in September 2020 with Jim Jacobson, former CEO of RTIC Outdoors.

Tariq told TechCrunch that the company provides software, services and infrastructure to businesses so they can scale online. Cart.com is taking the best parts of selling direct-to-consumer on marketplaces like Amazon and Shopify to create value for brands. Tariq said he is pioneering the term “e-commerce-as-a-service” to bring together under one platform a suite of business tools like storefront software, marketing, fulfillment, payments and customer service.

“We see the power of having an interconnected platform,” Tariq said. “There also needs to be a hybrid between selling direct-to-consumer and on Amazon and Shopify for companies that don’t have the money to pay for a percentage of their sales and receive no access to customers or data, and needing 20 different plug-ins that are not connected.”

Cart.com went after the new funding after seeing validation of its idea: brands coming to them wanting more products and services, which led to acquisitions. The company has acquired seven companies so far, including — AmeriCommerce, Spacecraft Brands and, more recently, DuMont Project and Sauceda Industries. Tariq is planning for another three or four by the end of the year.

In addition, it received inbound interest from strategic investors, like Oak and PayPal, which Tariq said was going to enable the company “to be more successful faster.”

Allen Miller, principal at Oak HC/FT, said after spending time with Tariq to understand his vision about Cart.com’s software, payments and services, he felt that the company was doing something that didn’t exist in today’s commerce infrastructure.

He said that Cart.com is well positioned to help companies, like those with $1 million in sales, stay focused on growing the business while Cart.com stitches together all of the tools for them to operate in the background.

“It’s a unique offering to merchants that has a high value proposition,” Miller said. “The vision and drive that Omair and Jim have, along with an inspiring mission they want to achieve — to be brand-centric and help the next generation of merchants. These guys also have a good playbook on finding companies and teams to acquire, as well as handling the post M&A to have everyone on one platform.”

The new financing will enable Cart.com to further invest in technology development and to increase headcount by at least 15 times, with plans to go from fewer than two dozen employees to more than 300 team members by the end of the year. The company has nearly 70 jobs posted on its website for positions in engineering, technology, digital marketing and e-commerce. Tariq also expects half of the funds to go toward more acquisitions.

Cart.com currently serves over 2,000 e-commerce brands, including GNC, Haymaker Coffee and KeHE, and processes more than $700 million in gross merchandise value per year. The company saw revenue increase 400% since the platform’s launch in November.

In addition, the company has nine fulfillment centers across the country, and is increasing its access to reach 80% of the U.S. population with two-day shipping, Tariq added.

“We are giving the power back to brands by giving them what they need to operate e-commerce,” he said. “There are still a few pieces to fill in so brands have a unified experience, but with us, they can add fulfilment, marketing or customer conversion tools with the click of a couple of buttons.”

Powered by WPeMatico

Before you hire a marketing consultant who doesn’t understand your products or commit to a CMO who has several years of experience — but none in your sector — consider influencer marketing.

If the phrase evokes images of celebrities hawking hard seltzer, think again: An influencer can be as humble as an enthusiastic Reddit user who manages your Telegram channel.

According to Uber growth marketing manager Jonathan Martinez:

“ … You don’t need to find influencers with millions of followers. Instead, lean toward microinfluencers for testing, which will bring cost efficiency and the ability to sponsor a diverse range of people.”

If your startup has a clear brand pitch, “an enticing offer” and “clear next steps,” you’re ready to reach out to influencers, he says.

In a guest post, Martinez explains how to structure offers that will maximize conversions and keep your representatives motivated to promote your products and services.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Image Credits: Julian Shapiro

This morning, we published an interview with growth expert Julian Shapiro, a founder and angel investor who also advises startups on the best way to present themselves.

Marketing is data-driven, but good storytelling is an art, says Shapiro.

To connect with consumers on an emotional level, “you need a mix of goodwill, what-we-stand-for ideology, social prestige and customer delight — among other affinity-building ingredients.”

Thanks very much for reading Extra Crunch this week!

Walter Thompson

Senior Editor, TechCrunch

Image Credits: Nigel Sussman (opens in a new window)

“In celebration of Coinbase’s earnings report today, investors poured a mountain of cash into one of the company’s global competitors,” Alex Wilhelm writes in The Exchange.

Rolling up his sleeves, he dug into numbers from Coinbase, FalconX and FTX to give readers some perspective on the state of cryptocurrency exchanges.

Image Credits: tomertu (opens in a new window) / Getty Images

Companies that have reached $5 million to $10 million in annual revenue are more likely to assemble growth teams; it’s a smart investment for any startup that’s achieved product-market fit.

It can also be potentially disruptive: Early marketing and product managers may feel sidelined by new cross-functional teams that suddenly take a leadership role.

In a detailed walkthrough, senior director of growth at OpenView Sam Richard explains the core players needed to build a growth team and how to integrate them into the organization smoothly, and shares some useful experiments to run.

“Don’t expect a single hire to scratch the growth itch for you,” Richard warns.

“A brilliant hire is going to come up with ideas, but will absolutely need a team to support them, turn them into experiments and then make them a reality.”

Image Credits: Bryce Durbin

In an interview with Brian Heater, Indiegogo CEO Andy Yang spoke about how the pandemic has impacted the crowdfunding platform, the challenges of stepping into the role after the previous CEO departed, and how the company reached profitability.

The company wasn’t profitable when you joined?

We weren’t profitable. I joined and then we cut to profitability, or at least kind of a neutral state, and with any kind of change in leadership, some tenured folks opted out, and we basically became a new team overnight to kind of re-found the company, and we’ve been slowly adding people over the last couple years, but always with that eye on profitability and controlling our own destiny.

Image Credits: Bryce Durbin

Last week, Kickstarter announced that people have backed more than 200,000 projects with $6 billion in pledges since the company launched in 2009. Just 15 months ago, it crossed the $5 billion threshold.

Brian Heater spoke to CEO Aziz Hasan, who took over in 2019, about last year’s substantial of layoffs, the pandemic’s long-term impact on crowdfunding, and how he’s working to build a more resilient company:

I think for us some of the most important things are to really just understand how we’re operating the business, making sure that we are sufficient in the buffer that we have for the business to make sure that we’re operating in a way that we can feel confident that the team is going to have some stability, that they’re going to have this resilience.

We frequently run articles with advice for founders who are working on pitch decks. It’s a fundamental step in every startup’s journey, and there are myriad ways to approach the task.

Michelle Davey of telehealth staffing and services company Wheel and Jordan Nof of Tusk Venture Partners appeared on Extra Crunch Live recently to analyze Wheel’s Series A pitch.

Nof said entrepreneurs should candidly explain to potential investors what they’ll need to believe to back their startup.

” … It takes a lot of guesswork out of the equation for the investor and it reorients them to focus on the right problem set that you’re solving,” he said.

“You get this one shot to kind of influence what they think they need to believe to get an investment here … if you don’t do that … we could get pretty off base.”

Image Credits: TravelCouples (opens in a new window) / Getty Images

Going up against global e-commerce behemoth Amazon might seem futile, but smaller players can leverage value adds that give them a leg up when it comes to ensuring a loyal customer base, says Kenny Small, vice president SAP and Enterprise at Qualitest Group.

“The reality is that Amazon’s true unique selling proposition is its distribution network,” he writes in a guest post. “Online retailers will not be able to compete on this point because Amazon’s distribution network is so fast.

“Instead, it’s important to focus on areas where they can excel — without having to become a third-party seller on Amazon’s platform.”

Image Credits: Nigel Sussman (opens in a new window)

Edtech and fintech have been in the Chinese Communist Party crosshairs in recent weeks — now, chat apps and gaming are among the targets.

Beijing filed a civil suit against Tencent over claims that its WeChat Youth Mode flouts laws protecting minors, and state media criticized the gaming industry as the digital equivalent of passing out drugs to kids, Alex Wilhelm writes in The Exchange.

He writes that the “news appears to indicate that we should expect more of the same as we’ve seen in recent months from the Chinese government: More complaints about the impact of ‘excessive’ capital in its industries, more tumbling share prices and more held IPOs.”

Image Credits: Yuichiro Chino (opens in a new window) / Getty Images

In an increasingly on-demand world, shipping delays and disruptions are a major roadblock to customer happiness.

AI can help, says Ahmer Inam, chief artificial intelligence officer at Pactera EDGE, who offers five strategies for using AI that can help startups understand supply chain disruptions and prepare for a Plan B.

“While AI won’t protect startups, manufacturers and retailers from these types of disruptions in the future, it can help them sense, anticipate, reroute and respond to them more effectively.”

Powered by WPeMatico

Traditional MBA programs can be costly, lengthy and often lack the application of real-world skills. Meanwhile, big global brands and companies who need product managers to grow their businesses can’t sit around waiting for people to graduate. And the edtech space hasn’t traditionally catered to this sector.

This is perhaps why Product School says it has secured $25 million in growth equity investment from growth fund Leeds Illuminate (subject to regulatory approval) to accelerate its product and partnerships with client companies.

The growth funding for the company comes after bootstrapping since 2014, in large part because product managers (PMs) are no longer needed just inside tech companies but have become sought after across almost virtually all industries.

Product School provides certificates for individuals as well as team training, and says it has experienced an upwelling of business since COVID switched so many companies into digital ones. It also now counts Google, Facebook, Netflix, Airbnb, PayPal, Uber and Amazon amongst its customers.

“Product managers have an outsized role in driving digital transformation and innovation across all sectors,” said Susan Cates, managing partner of Leeds Illuminate. “Having built the largest community of PMs in the world validates Product School’s certification as the industry standard for the market and positions the company at the forefront of upskilling top-notch talent for global organizations.”

Carlos Gonzalez de Villaumbrosia, CEO and founder of Product School, who started the company after moving from Spain, said: “There has never been a better time in history to build digital products and Product School is excited to unlock value for product teams across the globe to help define the future. Our company was founded on the basis that traditional degrees and MBA programs simply don’t equip PMs with the real-world skills they require on the job.”

Product School has also produced the The Product Book, The Proddy Awards and ProductCon.

Its main competitor is MindTheProduct, a community and training platform, which has also boostrapped.

Powered by WPeMatico

Refurbed, a European marketplace for refurbished electronics which raised a $17 million Series A round of funding last year, has now raised a $54 million Series B funding led by Evli Growth Partners and Almaz Capital.

They are joined by existing investors such as Speedinvest, Bonsai Partners and All Iron Ventures, as well as a group of new backers — Hermes GPE, C4 Ventures, SevenVentures, Alpha Associates, Monkfish Equity (Trivago Founders), Kreos, Expon Capital, Isomer Capital and Creas Impact Fund.

Refurbed is an online marketplace for refurbished electronics that are tested and renewed. These then tend to be 40% cheaper than new, and come with a 12-month warranty. The company claims that in 2020, it grew by 3x and reached more than €100 million in GMV.

Operating in Germany, Austria, Ireland, France, Italy and Poland, the startup plans to expand to three other countries by the end of 2021.

Riku Asikainen at Evli Growth Partners said: “We see the huge potential behind the way Refurbed contributes to a sustainable, circular economy.”

Peter Windischhofer, co-founder of refurbed, told me: “We are cheaper and have a wider product range, with an emphasis on quality. We focus on selling products that look new, so we end up with happy customers who then recommend us to others. It makes people proud to buy refurbished products.”

The startup has 130 refurbishers selling through its marketplace.

Other players in this space include Back Market (raised €48 million), Swappa (U.S.) and Amazon Renew. Refurbed also competes with Rebuy in Germany and Swapbee in Finland.

Powered by WPeMatico

As more consumers embrace plant-based diets and sustainable food practices, Rise Gardens is giving anyone the ability to have a green thumb from the comfort of their own home.

The Chicago-based indoor, smart hydroponic company raised $9 million in an oversubscribed Series A round, led by TELUS Ventures, with existing investors True Ventures and Amazon Alexa Fund and new investor Listen Ventures joining in. The company has a total of $13 million in venture-backed investments since Rise was founded in 2017, founder and CEO Hank Adams told TechCrunch.

Though he began in 2017, Adams, who has a background in sports technology, said he spent a few years working on prototypes before launching the first products in 2019. Rise’s IoT-connected systems are designed to grow vegetables, herbs and microgreens year-round.

Customers can choose between three system levels and get started with their first garden for about $300.

There is a “kind of joyousness” in being able to grow something, but people are looking for assistance because they don’t want to get into a hobby that will become demanding or stressful, Adams said. As a result, Rise’s accompanying mobile app monitors water levels and plant progress, then alert users when it’s time to water, fertilize or care for their plants.

“People are paying attention to food, and they care about what they eat,” he added. “Then the global pandemic played a part in this, with people leaning into growing their own food.”

In fact, customers leaned into growing food so much that Rise Gardens saw its sales eclipse seven figures in 2020, and gardens sold out three times during the year. Customers purchased close to 100,000 plants and have harvested 50,000.

The company estimates it helped keep more than 2,000 pounds of food from being wasted and saved 250,000 gallons of water since launching in 2019.

The concept of an indoor farm is not new. Incumbents include AeroGarden, AeroGrow, which was acquired by Scotts-Miracle Gro last November, and Click & Grow. Rise is among a new crop of startups that have raised funds that include Gardyn.

However, Rise Gardens is differentiating itself from those competitors by making its gardens from powder-coated metals and glass and are designed to be a focal point in the room. It is also offering ways for people to experiment with their gardens.

“We wanted something that would be flexible because once you have mastered a hobby, you will get bored,” he added. “You can start at one level and they swap out tray lids to grow more densely. We have a microgreens kit you can add, or add plant supports for tomatoes and peppers. You can also build a trellis to vine snap peas.”

Adams will focus the Series A dollars into product development, inventory, manufacturing, expansion into new markets and building up the team, especially in the areas of customer service and marketing. Rise has about 25 employees and plans to bring on another eight this year.

In addition, Rise Gardens’ products will soon be available on Amazon — its first channel outside of its website. The company is also expanding into schools in what Adams calls “version 2.0” of the school garden.

When Rich Osborn, president and managing partner of TELUS Ventures, evaluated the indoor garden space, he told TechCrunch that Adams and his team rose to the top of the list because of their background, data experience and syndication with Amazon.

Not only was consumer demand there for these kinds of products, but the sustainability and social impact created from these kinds of investments couldn’t be overemphasized, he said.

Nishan Majarian, co-founder and CEO of TELUS Agriculture, said he sees a future where there is a spectrum of food growth, and crop management will be at the plant level.

“Ever since Climate Corp. was acquired by Monsanto, there has been a massive influx into agriculture to get to the next billion-dollar exit,” Majarian added. “Agrifood is the last segmented supply chain. Every crop is different, every market is different. That makes it local, complex and fertile soil — pun intended — for startups who get capital to solve those issues and scale.”

Powered by WPeMatico

There is an art to engineering, and sometimes engineering can transform art. For Spencer Kimball and Peter Mattis, those two worlds collided when they created the widely successful open-source graphics program, GIMP, as college students at Berkeley.

That project was so successful that when the two joined Google in 2002, Sergey Brin and Larry Page personally stopped by to tell the new hires how much they liked it and explained how they used the program to create the first Google logo.

Cockroach Labs was started by developers and stays true to its roots to this day.

In terms of good fortune in the corporate hierarchy, when you get this type of recognition in a company such as Google, there’s only one way you can go — up. They went from rising stars to stars at Google, becoming the go-to guys on the Infrastructure Team. They could easily have looked forward to a lifetime of lucrative employment.

But Kimball, Mattis and another Google employee, Ben Darnell, wanted more — a company of their own. To realize their ambitions, they created Cockroach Labs, the business entity behind their ambitious open-source database CockroachDB. Can some of the smartest former engineers in Google’s arsenal upend the world of databases in a market spotted with the gravesites of storage dreams past? That’s what we are here to find out.

Mattis and Kimball were roommates at Berkeley majoring in computer science in the early-to-mid-1990s. In addition to their usual studies, they also became involved with the eXperimental Computing Facility (XCF), an organization of undergraduates who have a keen, almost obsessive interest in CS.

Powered by WPeMatico

It’s not easy following a larger-than-life founder and CEO of an iconic company, but that’s what former AWS CEO Andy Jassy faces this week as he takes over for Jeff Bezos, who moves into the executive chairman role. Jassy must deal with myriad challenges as he becomes the head honcho at the No. 2 company on the Fortune 500.

How he handles these challenges will define his tenure at the helm of the online retail giant. We asked several analysts to identify the top problems he will have to address in his new role.

Handling that transition smoothly and showing investors and the rest of the world that it’s business as usual at Amazon is going to be a big priority for Jassy, said Robin Ody, an analyst at Canalys. He said it’s not unlike what Satya Nadella faced when he took over as CEO at Microsoft in 2014.

Handling the transition smoothly and showing investors and the rest of the world that it’s business as usual at Amazon is going to be a big priority for Jassy.

“The biggest task is that you’re following Jeff Bezos, so his overarching issue is going to be stability and continuity. … The eyes of the world are on that succession. So managing that I think is the overall issue and would be for anyone in the same position,” Ody said.

Forrester analyst Sucharita Kodali said Jassy’s biggest job is just to keep the revenue train rolling. “I think the biggest to-do is to just continue that momentum that the company has had for the last several years. He has to make sure that they don’t lose that. If he does that, I mean, he will win,” she said.

As an online retailer, the company has thrived during COVID, generating $386 billion in revenue in 2020, up more than $100 billion over the prior year. As Jassy takes over and things return to something closer to normal, will he be able to keep the revenue pedal to the metal?

Powered by WPeMatico

When the Pentagon killed the JEDI cloud program yesterday, it was the end of a long and bitter road for a project that never seemed to have a chance. The question is why it didn’t work out in the end, and ultimately I think you can blame the DoD’s stubborn adherence to a single vendor requirement, a condition that never made sense to anyone, even the vendor that ostensibly won the deal.

In March 2018, the Pentagon announced a mega $10 billion, decade-long cloud contract to build the next generation of cloud infrastructure for the Department of Defense. It was dubbed JEDI, which aside from the Star Wars reference, was short for Joint Enterprise Defense Infrastructure.

The idea was a 10-year contract with a single vendor that started with an initial two-year option. If all was going well, a five-year option would kick in and finally a three-year option would close things out with earnings of $1 billion a year.

While the total value of the contract had it been completed was quite large, a billion a year for companies the size of Amazon, Oracle or Microsoft is not a ton of money in the scheme of things. It was more about the prestige of winning such a high-profile contract and what it would mean for sales bragging rights. After all, if you passed muster with the DoD, you could probably handle just about anyone’s sensitive data, right?

Regardless, the idea of a single-vendor contract went against conventional wisdom that the cloud gives you the option of working with the best-in-class vendors. Microsoft, the eventual winner of the ill-fated deal acknowledged that the single vendor approach was flawed in an interview in April 2018:

Leigh Madden, who heads up Microsoft’s defense effort, says he believes Microsoft can win such a contract, but it isn’t necessarily the best approach for the DoD. “If the DoD goes with a single award path, we are in it to win, but having said that, it’s counter to what we are seeing across the globe where 80% of customers are adopting a multicloud solution,” Madden told TechCrunch.

Perhaps it was doomed from the start because of that. Yet even before the requirements were fully known there were complaints that it would favor Amazon, the market share leader in the cloud infrastructure market. Oracle was particularly vocal, taking its complaints directly to the former president before the RFP was even published. It would later file a complaint with the Government Accountability Office and file a couple of lawsuits alleging that the entire process was unfair and designed to favor Amazon. It lost every time — and of course, Amazon wasn’t ultimately the winner.

While there was a lot of drama along the way, in April 2019 the Pentagon named two finalists, and it was probably not too surprising that they were the two cloud infrastructure market leaders: Microsoft and Amazon. Game on.

The former president interjected himself directly in the process in August that year, when he ordered the Defense Secretary to review the matter over concerns that the process favored Amazon, a complaint which to that point had been refuted several times over by the DoD, the Government Accountability Office and the courts. To further complicate matters, a book by former defense secretary Jim Mattis claimed the president told him to “screw Amazon out of the $10 billion contract.” His goal appeared to be to get back at Bezos, who also owns the Washington Post newspaper.

In spite of all these claims that the process favored Amazon, when the winner was finally announced in October 2019, late on a Friday afternoon no less, the winner was not in fact Amazon. Instead, Microsoft won the deal, or at least it seemed that way. It wouldn’t be long before Amazon would dispute the decision in court.

By the time AWS re:Invent hit a couple of months after the announcement, former AWS CEO Andy Jassy was already pushing the idea that the president had unduly influenced the process.

“I think that we ended up with a situation where there was political interference. When you have a sitting president, who has shared openly his disdain for a company, and the leader of that company, it makes it really difficult for government agencies, including the DoD, to make objective decisions without fear of reprisal,” Jassy said at that time.

Then came the litigation. In November the company indicated it would be challenging the decision to choose Microsoft charging that it was was driven by politics and not technical merit. In January 2020, Amazon filed a request with the court that the project should stop until the legal challenges were settled. In February, a federal judge agreed with Amazon and stopped the project. It would never restart.

In April the DoD completed its own internal investigation of the contract procurement process and found no wrongdoing. As I wrote at the time:

While controversy has dogged the $10-billion, decade-long JEDI contract since its earliest days, a report by the DoD’s inspector general’s office concluded today that, while there were some funky bits and potential conflicts, overall the contract procurement process was fair and legal and the president did not unduly influence the process in spite of public comments.

Last September the DoD completed a review of the selection process and it once again concluded that Microsoft was the winner, but it didn’t really matter as the litigation was still in motion and the project remained stalled.

The legal wrangling continued into this year, and yesterday the Pentagon finally pulled the plug on the project once and for all, saying it was time to move on as times have changed since 2018 when it announced its vision for JEDI.

The DoD finally came to the conclusion that a single-vendor approach wasn’t the best way to go, and not because it could never get the project off the ground, but because it makes more sense from a technology and business perspective to work with multiple vendors and not get locked into any particular one.

“JEDI was developed at a time when the Department’s needs were different and both the CSPs’ (cloud service providers) technology and our cloud conversancy was less mature. In light of new initiatives like JADC2 (the Pentagon’s initiative to build a network of connected sensors) and AI and Data Acceleration (ADA), the evolution of the cloud ecosystem within DoD, and changes in user requirements to leverage multiple cloud environments to execute mission, our landscape has advanced and a new way ahead is warranted to achieve dominance in both traditional and nontraditional warfighting domains,” said John Sherman, acting DoD chief information officer in a statement.

In other words, the DoD would benefit more from adopting a multicloud, multivendor approach like pretty much the rest of the world. That said, the department also indicated it would limit the vendor selection to Microsoft and Amazon.

“The Department intends to seek proposals from a limited number of sources, namely the Microsoft Corporation (Microsoft) and Amazon Web Services (AWS), as available market research indicates that these two vendors are the only Cloud Service Providers (CSPs) capable of meeting the Department’s requirements,” the department said in a statement.

That’s not going to sit well with Google, Oracle or IBM, but the department further indicated it would continue to monitor the market to see if other CSPs had the chops to handle their requirements in the future.

In the end, the single vendor requirement contributed greatly to an overly competitive and politically charged atmosphere that resulted in the project never coming to fruition. Now the DoD has to play technology catch-up, having lost three years to the histrionics of the entire JEDI procurement process and that could be the most lamentable part of this long, sordid technology tale.

Powered by WPeMatico