Alphabet

Auto Added by WPeMatico

Auto Added by WPeMatico

“It is our contention that the investment industry may be experiencing a peak of its own, in this case the point of the maximum rate at which it extracts value from its clients’ assets. Let’s call it Peak Gravy.” That’s a recent quote from Tom Coutts, who is one of a few dozen partners at Baillie Gifford (See Arman Tabatabai’s profile here). It’s also typical of the provocative sentiments offered by this band of fund managers who are based in Edinburgh, but scour the world looking for opportunities.

In an effort to distinguish its world view, the firm has introduced the somewhat eyebrow-raising tagline, “We’re actual investors.” For many US technology observers, though, Baillie Gifford is known for its investments in unicorns. But as Extra Crunch’s executive editor Danny Crichton and I found out in a recent conversation with Charles Plowden (one of two senior partners and the overseer of the firm’s investment departments), there’s a lot more to the story and motivations behind this unique 110-year-old partnership that’s still going strong.

Powered by WPeMatico

Ouster has raised $60 million as the San Francisco-based lidar startup opens a new facility that will have the capacity to assemble and ship several thousand sensors a month by the end of 2019.

The new factory, which will have a grand opening ceremony March 28, currently produces hundreds of sensors per month. Ouster says at full capacity, the factory will produce $25 million to $50 million in inventory per month.

Lidar measures distance using laser light to generate highly accurate 3D maps of the world around the car. It’s considered by most in the self-driving car industry a key piece of technology required to safely deploy robotaxis and other autonomous vehicles (although not everyone agrees). However, the sensors are also useful in other industries — and this is where Ouster’s business model is targeted.

Ouster has cast a wider net for customers than some of its rivals. Unlike others vying solely for automotive customers working on the development of autonomous vehicles, Ouster is selling sensors to other industries. Ouster is selling its light detection and ranging radar sensors to robotics, drones, mapping, defense, building security, mining and agriculture companies.

The strategy has appeared to pay off. Ouster says it has 400 customers from 15 industries.

The $60 million in additional funding follows a Series A raise of $27 million announced back in 2017 as Ouster came out of stealth mode. In the years since, the company led by Angus Pacala has grown to more than 100 employees and announced four lidar sensors, with resolutions from 16 to 128 channels, and two product lines, the OS-1 and OS-2. The startup expects to nearly double its headcount in the coming year to support further product line development.

The $60 million in equity and debt funding includes investments from Runway Growth Capital and Silicon Valley Bank, as well as additional funding from Series A participants Cox Enterprises, Constellation Tech Ventures, Fontinalis Partners, Carthona and others.

Ouster said the additional investment has helped to develop Ouster’s product lines, including the launch of the OS-1 128 lidar sensor, and fund the expansion of its production facilities.

The company also announced the appointment of Susan Heystee, senior VP for OEM business at Verizon Connect, to its board of directors.

Waymo, the self-driving car company under Google’s Alphabet, could be a new competitor to the company. Waymo announced this month it will start selling its custom lidar sensors to companies outside of self-driving cars. Waymo will initially target robotics, security and agricultural technology. The sales will help the company scale its autonomous technology faster, making each sensor more affordable through economies of scale, Simon Verghese, head of Waymo’s lidar team, wrote in a Medium post at the time.

Powered by WPeMatico

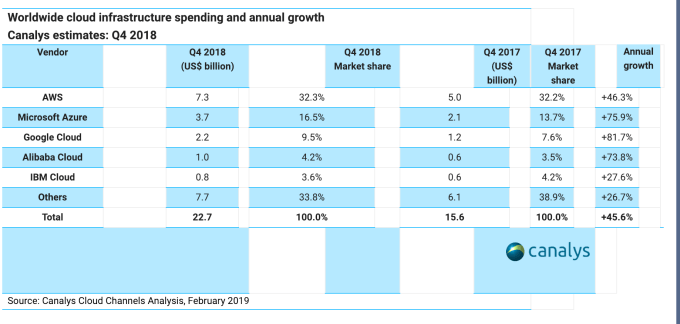

Google has shared its cloud revenue exactly once over the last several years. Silence tends to lead to speculation to fill the information vacuum. Luckily there are some analyst firms who try to fill the void, and it looks like Google’s cloud business is actually trending in the right direction, even if they aren’t willing to tell us an exact number.

When Google last reported its cloud revenue, last year about this time, they indicated they had earned $1 billion in revenue for the quarter, which included Google Cloud Platform and G Suite combined. Diane Greene, who was head of Google Cloud at the time, called it an “elite business.” but in reality it was pretty small potatoes compared to Microsoft’s and Amazon’s cloud numbers, which were pulling in $4-$5 billion a quarter between them at the time. Google was looking at a $4 billion run rate for the entire year.

Google apparently didn’t like the reaction it got from that disclosure so it stopped talking about cloud revenue. Yesterday when Google’s parent company, Alphabet, issued its quarterly earnings report, to nobody’s surprise, it failed to report cloud revenue yet again, at least not directly.

Google CEO Sundar Pichai gave some hints, but never revealed an exact number. Instead he talked in vague terms calling Google Cloud “a fast-growing multibillion-dollar business.” The only time he came close to talking about actual revenue was when he said, “Last year, we more than doubled both the number of Google Cloud Platform deals over $1 million as well as the number of multiyear contracts signed. We also ended the year with another milestone, passing 5 million paying customers for our cloud collaboration and productivity solution, G Suite.”

OK, it’s not an actual dollar figure, but it’s a sense that the company is actually moving the needle in the cloud business. A bit later in the call, CFO Ruth Porat threw in this cloud revenue nugget. “We are also seeing a really nice uptick in the number of deals that are greater than $100 million and really pleased with the success and penetration there. At this point, not updating further.” She is not updating further. Got it.

That brings us to a company that guessed for us, Canalys. While the firm didn’t share its methodology, it did come up with a figure of $2.2 billion for the quarter. Given that the company is closing larger deals and was at a billion last year, this figure feels like it’s probably in the right ballpark, but of course it’s not from the horse’s mouth, so we can’t know for certain. It’s worth noting that Canalys told TechCrunch that this is for GCP revenue only, and does not include G Suite, so that would suggest that it could be gaining some momentum.

Frankly, I’m a little baffled why Alphabet’s shareholders actually let the company get away with this complete lack of transparency. It seems like people would want to know exactly what they are making on that crucial part of the business, wouldn’t you? As a cloud market watcher, I know I would, and if the company is truly beginning to pick up steam, as Canalys data suggests, the lack of openness is even more surprising. Maybe next quarter.

Powered by WPeMatico

Despite a number of well-publicized hiccups, venture capitalists are betting another $500 million on health insurance provider Clover Health, TechCrunch has learned.

Existing investor Greenoaks Capital led the round, according to the startup, which confirmed it was closing a new round of capital in the coming weeks. Clover Health has raised a total of $925 million to date, garnering a valuation of $1.2 billion with a $130 million Series D funding in 2017. The company, backed by Alphabet’s venture arm GV, Sequoia Capital, Floodgate, Bracket Capital, First Round Capital and more, declined to disclose its latest valuation.

San Francisco-based Clover Health was founded in 2012 by chief executive officer Vivek Garipalli, the former founder of New Jersey healthcare system CarePoint Health; and Kris Gale, who served as the startup’s chief technology officer until transitioning into an adviser role in December 2017. As part of its latest funding round, the company told TechCrunch it’s promoting Andrew Toy, its chief technology officer since early 2018, to the role of president and CTO. He will also join its board of directors.

Varsha Rao, Airbnb’s former chief operating officer, joined the company in September 2017 as COO.

The tech-enabled health insurer differentiates itself from incumbents by collecting and analyzing health and behavioral data to lower costs and improve medical outcomes for its members. It’s part of a new cohort of heavily funded insurtech startups, including Devoted Health and Bright Health, both of which similarly provide Medicare Advantage plans. Devoted Health, backed by Andreessen Horowitz, raised a $300 million Series B funding round three months ago. Bright Health, for its part, brought in a $200 million Series C in late November at a $950 million valuation. It’s backed by Bessemer Venture Partners, Greycroft, NEA and Redpoint Ventures, among others.

Founded in 2012, Clover Health is years older than its aforementioned counterparts. The business, though supported by top-tier investors and plenty of capital, has struggled in the past to shrink its losses. In 2015, Clover Health posted a net loss of $4.9 million only to increase it 7x the following year to $34.6 million, according to financial documents obtained by Axios. At the time, Clover Health had 20,600 Medicare Advantage members, earning it $184 million in taxpayer revenue. According to reporting from CNBC, the company had initially planned to double its membership base each year but was only able to expand from 20,000 in 2016 to 27,000 in September 2017.

Clover Health currently has 40,000 members in Georgia, New Jersey, Arizona, Pennsylvania, South Carolina, Tennessee and Texas. The business earns roughly $10,000 in revenue per member from the Centers for Medicare and Medicaid Services, or currently about $400 million in annual revenue. As a Medicare Advantage plan, Clover Health makes a majority of its cash from the government.

“Clover’s continuously improving economic fundamentals have allowed us to build sustainably, thoughtfully enter new markets and increase our overall membership by 35 percent during the last 12 months, compared with nationwide growth of 8 percent for Medicare Advantage overall,” the company said in a statement provided to TechCrunch. “This has made Clover one of the fastest growing insurers in [Medicare Advantage] over the past three years. That said, there is much more to accomplish, which is why I am so excited about entering this next phase in our company’s history.”

Powered by WPeMatico

Mobile licensing changes made by Google this fall, when it tweaked terms for OEMs wanting to license its Android smartphone platform on devices destined for the European market, don’t appear to be offering succour to search rivals — despite being triggered by an antitrust ruling intended to reset the competitive playing field.

The European Commission found the search giant guilty of anti-competitive practices related to its Android platform this summer, slapping the company with a $5BN fine. The decision required Google cease practices judged to be illegally skewing the market and do so within 90 days.

It was the second such major EC antitrust finding against Google, after last year’s Google Shopping ruling, when the company was warned that having been found dominant in search it had a “special responsibility” to avoid breaching antitrust rules in any market it plays in.

Google disputes the Commission’s findings of competitive abuse in both cases, and has lodged legal appeals.

But the nature of competition law demands action in the meanwhile, given the threat of punitive penalties for any continued breach. So in October Google responded to the Commission’s Android ruling by updating its regional compatibility agreement to provide a route for OEMs to unbundle key services from the Android OS — rather than requiring its suite of Google apps be pre-loaded for devices to get the Play Store.

However it also incorporated licensing fees for some unbundled configurations (e.g. Android + Play Store). At the same time it said it would not charge any fee to include search or Chrome. And it said it was offering incentives for OEMs to place its eponymous, market dominating search engine (and/or browser) prominently on their devices — despite one of the behaviors the Commission judged illegal being payments Google had made to certain large manufacturers and mobile carriers to exclusively pre-install Google Search.

The Commission did not prescribe specific remedies for the anticompetitive behaviours it pegged to Android — saying it’s “Google’s sole responsibility to make sure that it changes its conduct in a way that brings the infringements to an effective end”.

Though it warned it would closely monitor the company’s conduct, noting that any finding of continued non-compliance would risk fresh fines — of up to 5% of the average daily turnover of Alphabet for each day of non-compliance.

The key word there is “effective” — in terms of what the Commission is watching for.

Meanwhile Google’s dominant position in search naturally makes it the smartphone consumer’s go-to choice — which in turn means there’s a natural incentive for device makers not to ditch Google as the search default. At least for mainstream devices.

But Google’s new European licensing terms for Android appear to be piling additional pressure on OEMs not to switch even for more experimental and/or regional device launches, according to privacy-focused search engine Qwant.

The suggestion is Google’s licensing changes have essentially blocked the launch of an Android device with Qwant search rather than Google as the default.

Its experience suggests Google’s initial ‘remedy’ — far from delivering an “effective end” to the competitive infringements the Commission found — is actively steering OEMs away from search alternatives and rival companies.

Qwant, a French startup, launched its non-tracking search offering back in 2013, and has been on a growth tear on its home turf in recent months — winning over high profile users in the public sector as concern has risen about Silicon Valley’s intrusive grip on user data.

The French National Assembly and the French Ministry of the Armed Forces Minister announced this fall they’d switch to Qwant instead of Google as their default.

Of course the startup is still a minnow compared to Google. But it’s growing: Qwant tracks queries rather than users (given it doesn’t track people), and it says it generated 2.6BN queries in 2016; which grew to 9BN last year; and is now on track to end this year with around 18BN queries.

“So if we think about it that means that last year we were three days of Google; this year six days of Google — not so bad!” says co-founder Eric Leandri.

“In France we have now more than 6% of the market,” he continues. “In Germany something like 2%. And we are still growing. We do growth of 20% by month for the last four months. The growth in our revenue is two digit too, by month.”

Earlier this year it had been hoping to make additional regional marketshare gains by securing a deal to be pre-loaded on Android smartphones destined for European markets. A spokesman tells us it has a framework agreement with Huawei. (The Chinese Android OEM is second only to Samsung in global marketshare terms, according to analysts.)

The Commission’s antitrust ruling opened the door to this possibility, given it banned Google from prohibiting OEMs from launching non-Google approved Android forks. So after the ruling things were looking good for Qwant, with the startup on the cusp of securing a device deal for a few European countries, as Leandri tells it.

He blames Google’s licensing changes for putting the kibosh on a launch they’d been expecting to be able to announce in November. Early that month the startup pinged us to trail forthcoming news — of “a major partnership that will allow us to accelerate in the smartphone market” — only to go silent.

A few weeks later it got in touch again to say it had had to postpone the announcement.

“We are very near to one or two deals to be by default or in the list of search engines in some Android cell phone made by a very large Asian manufacturer… Just for Europe, and just for some countries in Europe but we are talking about 10 million or 20 million of cell phones,” says Leandri now.

“And when we have won the bid against Google in October then Google start to say that in Europe you have to pay $40 for Android. So now if you install Qwant you have to pay $40 and if you install Google they give you some cash.”

“Before it was impossible to bid against Google because Google was blocking everything. Now you can — but now the solution of Google is you have to pay $40 if you don’t install Google by default with Chrome just on the bar. You know the bar that is fixed on Android. And this is again an abuse of their dominant position,” he adds.

“Because if I want, for example, 10 million smartphones, the guy has to pay $400M to Google. Do you really think they will pay $400M to Google just to install Qwant?”

Google’s rebuttal of the Commission’s antitrust finding for Android has focused on claims that its approach of free licensing combined with a bundle of Google services has generally enabled competition to thrive in the mobile app ecosystem, as well as claiming lower prices are a “classic hallmark… of robust competition”.

Yet Qwant’s experience offers a clear counterpoint, underlining how challenging it remains to try to compete with Google’s core search business when the same company also dominates the smartphone market and can just throw the levers of Android’s licensing terms to configure how much ‘appetite’ OEMs have for investing in alternative search defaults (given tiny hardware profit margins in the Android space).

After Qwant won over Huawei to building a device with its search engine in prime position, Leandri says it was Google’s changes to the licensing terms for Android that threw a spanner in the works.

“After that pressure then the manufacturer doesn’t know how to react now,” he says, confirming he believes there’s currently no chance for the device to be launched. Not without further changes to how Android operates in the market — i.e. further regulatory intervention.

“So we will work a lot with the European Commission to stop that,” he adds. “But again, again my question is why Google goes that way?”

We reached out to Google to ask about the fees it would charge an OEM wanting to launch an Android device with Google Play but without Google search as the default in Europe.

We also asked how charging a fee for Android if OEMs don’t also bundle Google services can help increase competition, per the Commission’s intention.

At the time of writing Google had not responded to our questions.

We also reached out to Huawei for comment and will update this story with any response.

Even if Qwant and Huawei get their way, and European buyers in a handful of countries are able to choose to buy an Android device with a little search localization as its differentiating out-of-the-box twist, Leandri isn’t under any illusions that a majority of consumers will still switch back to Google of their own accord — given its dominance of search.

He reckons those who’d stick with a non-Google search choice might be as low as a third or 40%.

But his point is that, as it stands, Qwant doesn’t even have the chance to try competing against the Google Goliath on its own terms. And he argues that’s simply not fair.

“Google has billions to make advertisement to ask people to switch, right. And they can even do advertisement on the Play Store for zero because they control the Play Store. Why they don’t come back to a normal market where we are all on the same line and they just compete with advertisement, with pushing their products, with a better proposition of value. It’s crazy, it’s crazy!” he says.

“They have 95% of the market, and on that market they expect that if they don’t have the search by default there then they don’t do money with the Play Store. This is bullshit. They do billions of euros with the app on the Play Store each year. With the 30% that they take on the apps. So this is not true. This is not true, sorry.

“So right now this is our goal and my main work actually is just to obtain the right to have a fair competition — a simple, fair competition.”

“I don’t want to dismantle Google. I don’t want Google to be fined 10BN. I don’t care. The only thing I want is to have the right to have a fair competition,” he adds.

We asked the European Commission to respond to Qwant’s experience, and for an update on its monitoring of Google’s compliance with the Android antitrust ruling.

A spokeswoman declined to comment on an individual case but we understand the Commission has been sending questionnaires to market players as part of its compliance monitoring.

It’s clear the regulator’s intention with the Android decision was to expand consumer choice by creating opportunities for competition that didn’t exist before — including for rival search and browser providers to be able to compete on the merits with Google when it comes to pre-loading their products on Android devices.

So if the Commission’s monitoring efforts confirm instances where competition is being blocked, as appears the case here with Qwant, further interventions will surely follow.

Leandri also points out that Google made much the same arguments vis-a-vis ‘fair competition’ more than a decade ago — when it called for the then computing incumbent, Microsoft, not to stand in the way of Internet upstarts by bundling MSN search into its Internet Explorer web browser.

“The market favors open choice for search, and companies should compete for users based on the quality of their search services,” said Marissa Mayer in 2006, then Google’s vice president for search products. “We don’t think it’s right for Microsoft to just set the default to MSN. We believe users should choose.”

“I totally agree with what they say in 2006! Just exchange Microsoft for Google and that’s it!” he says now, adding: “We have to fight because there is not a lot of other way. But I stop fighting tomorrow as soon as I have a fair competition.

“I’m not waiting for the Commission to make the competition. Right now the percentage of growth that I have in France it’s not based on the Commission who has won or not. It’s based on our value proposition.”

Leandri is also president of the Open Internet Project, a European organization whose members lobby for regulatory action to rein in what they view as Google’s abusive dominance of digital markets, and which was also involved in the Google Shopping complaints — though he points out that in the Android case three of the five complainants are American.

“We are the only European. So the problem is not only for a small startup in Europe. Who, y’know, complained because ‘Google is so cool’. And we are so dumb. And so ridiculous. But the problem is for Oracle, it’s for the Fair Search. It’s not for kids.”

Powered by WPeMatico

A flurry of digital-first insurers are betting they can surpass industry incumbents with a little help from technology and a lot of help from venture capitalists.

The latest to land a massive check is Bright Health, a Minneapolis-headquartered provider of affordable individual, family and Medicare Advantage healthcare plans in Alabama, Arizona, Colorado, New York City, Ohio and Tennessee. The company, founded by the former chief executive officer of UnitedHealthcare Bob Sheehy; Kyle Rolfing, the former CEO of UnitedHealth-acquired Definity Health; and Tom Valdivia, another former Definity Health executive, has brought in a $200 million Series C.

The funding values Bright Health at $950 million, according to PitchBook — more than double the $400 million valuation it garnered with its $160 million Series B in June 2017. Sheehy, Bright Health’s CEO, declined to comment on the valuation. New investors Declaration Partners and Meritech Capital participated in the round, with backing from Bessemer Venture Partners, Greycroft, NEA, Redpoint Ventures and others. Bright Health has raised a total of $440 million since early 2016.

VCs have deployed significantly more capital to the insurance technology (insurtech) space in recent years. Startups in the industry, long-known for a serious dearth of innovation, have raked in nearly $3 billion in private capital this year. U.S.-based insurtech startups have raised $2 billion in 2018, a record year for the sector and more than double last year’s total.

Deal count, meanwhile, is swelling. In 2016, there were 72 deals conducted in the space, followed by 86 in 2017 and 94 so far this year, again, according to PitchBook’s data.

Oscar Health, the health insurance provider led by Josh Kushner, is responsible for about 25 percent of the capital invested in U.S. insurtech startups this year. The company has raised a total of $540 million across two notable deals in 2018. The first saw Oscar pulling in $165 million at a $3 billion valuation and the second, announced in August, had Alphabet investing a whopping $375 million. Devoted Health, a Waltham, Mass.-based Medicare Advantage startup, followed up with a massive round of its own. The company nabbed $300 million and announced that it would begin enrolling members to its Medicare Advantage plan in eight Florida counties. Devoted is led by Todd Park, the co-founder of Athenahealth and Castlight Health.

Bright Health co-founders Bob Sheehy, CEO; Tom Valdivia, chief medical officer; and Kyle Rolfing, president

VC’s interest in insurtech isn’t limited to healthcare.

Hippo, which sells home insurance plans at lower premiums, officially launched in 2017 and has brought in $109 million to date. Earlier this month the company announced a $70 million Series C funding round led by Felicis Ventures and Lennar Corporation. Lemonade, which is similarly an insurer focused on homeowners, raised $120 million in a SoftBank-led round late last year. And Root Insurance, an app-based car insurance company founded in 2015, itself raised a $100 million Series D led by Tiger Global Management in August. The financing valued the company at $1 billion.

Together, these companies have raised well over $1 billion this year alone. Why? Because building a health insurance platform is incredibly cash-intensive and particularly difficult given the breadth of incumbents like Aetna or UnitedHealth. Sheehy, considering his 20-year tenure at UnitedHealthcare, may be especially well-positioned to disrupt the industry.

The opportunity here for investors and startups alike is huge; the health insurance market alone is forecasted to be worth more than $1 trillion by 2023. Companies that can leverage technology to create consumer-friendly, efficient and, most importantly, reasonably priced insurance options stand to win big.

As for Bright Health, the company plans to use its $200 million infusion to rapidly expand into new markets, planning to triple its geographic footprint in 2019.

“Bright Health has continued to execute at a fast pace towards our goal of disrupting the old health care model that places insurers at odds with providers,” Sheehy said in a statement. “[Its] current high re-enrollment rate shows that consumers are ready for this improved healthcare experience – especially when it is priced competitively.”

Powered by WPeMatico

With its latest $34 billion acquisition of Red Hat, IBM may have found something more elementary than “Watson” to save its flagging business.

Though the acquisition of Red Hat is by no means a guaranteed victory for the Armonk, N.Y.-based computing company that has had more downs than ups over the five years, it seems to be a better bet for “Big Blue” than an artificial intelligence program that was always more hype than reality.

Indeed, commentators are already noting that this may be a case where IBM finally hangs up the Watson hat and returns to the enterprise software and services business that has always been its core competency (albeit one that has been weighted far more heavily on consulting services — to the detriment of the company’s business).

Also read as IBM taps out on Watson as its growth engine and returns to basics ie financial engineering and distribution https://t.co/nD7gHyYhQf

— Sunil Rawat (@_sunilrawat) October 28, 2018

Watson, the business division focused on artificial intelligence whose public claims were always more marketing than actually market-driven, has not performed as well as IBM had hoped and investors were losing their patience.

Critics — including analysts at the investment bank Jefferies (as early as one year ago) — were skeptical of Watson’s ability to deliver IBM from its business woes.

As we wrote at the time:

Jefferies pulls from an audit of a partnership between IBM Watson and MD Anderson as a case study for IBM’s broader problems scaling Watson. MD Anderson cut its ties with IBM after wasting $60 million on a Watson project that was ultimately deemed, “not ready for human investigational or clinical use.”

The MD Anderson nightmare doesn’t stand on its own. I regularly hear from startup founders in the AI space that their own financial services and biotech clients have had similar experiences working with IBM.

The narrative isn’t the product of any single malfunction, but rather the result of overhyped marketing, deficiencies in operating with deep learning and GPUs and intensive data preparation demands.

That’s not the only trouble IBM has had with Watson’s healthcare results. Earlier this year, the online medical journal Stat reported that Watson was giving clinicians recommendations for cancer treatments that were “unsafe and incorrect” — based on the training data it had received from the company’s own engineers and doctors at Sloan-Kettering who were working with the technology.

All of these woes were reflected in the company’s latest earnings call where it reported falling revenues primarily from the Cognitive Solutions business, which includes Watson’s artificial intelligence and supercomputing services. Though IBM chief financial officer pointed to “mid-to-high” single digit growth from Watson’s health business in the quarter, transaction processing software business fell by 8% and the company’s suite of hosted software services is basically an afterthought for business gravitating to Microsoft, Alphabet, and Amazon for cloud services.

To be sure, Watson is only one of the segments that IBM had been hoping to tap for its future growth; and while it was a huge investment area for the company, the company always had its eyes partly fixed on the cloud computing environment as it looked for areas of growth.

It’s this area of cloud computing where IBM hopes that Red Hat can help it gain ground.

“The acquisition of Red Hat is a game-changer. It changes everything about the cloud market,” said Ginni Rometty, IBM Chairman, President and Chief Executive Officer, in a statement announcing the acquisition. “IBM will become the world’s number-one hybrid cloud provider, offering companies the only open cloud solution that will unlock the full value of the cloud for their businesses.”

The acquisition also puts an incredible amount of marketing power behind Red Hat’s various open source services business — giving all of those IBM project managers and consultants new projects to pitch and maybe juicing open source software adoption a bit more aggressively in the enterprise.

As Red Hat chief executive Jim Whitehurst told TheStreet in September, “The big secular driver of Linux is that big data workloads run on Linux. AI workloads run on Linux. DevOps and those platforms, almost exclusively Linux,” he said. “So much of the net new workloads that are being built have an affinity for Linux.”

Powered by WPeMatico

VirusTotal, the virus- and malware-scanning service owned by Alphabet’s Chronicle, launched an enterprise-grade version of its service today.

VirusTotal Enterprise offers significantly faster and more customizable malware search, as well as a new feature called Private Graph, which allows enterprises to create their own private visualizations of their infrastructure and malware that affects their machines.

The Private Graph makes it easier for enterprises to create an inventory of their internal infrastructure and users to help security teams investigate incidents (and where they started). In the process of building this graph, VirtusTotal also looks are commonalities between different nodes to be able to detect changes that could signal potential issues.

The company stresses that these graphs are obviously kept private. That’s worth noting because VirusTotal already offered a similar tool for its premium users — the VirusTotal Graph. All of the information there, however, was public.

As for the faster and more advanced search tools, VirusTotal notes that its service benefits from Alphabet’s massive infrastructure and search expertise. This allows VirusTotal Enterprise to offer a 100x speed increase, as well as better search accuracy. Using the advanced search, the company notes, a security team could now extract the icon from a fake application, for example, and then return all malware samples that share the same file.

VirusTotal says that it plans to “continue to leverage the power of Google infrastructure” and expand this enterprise service over time.

Google acquired VirusTotal back in 2012. For the longest time, the service didn’t see too many changes, but earlier this year, Google’s parent company Alphabet moved VirusTotal under the Chronicle brand and the development pace seems to have picked up since.

Powered by WPeMatico

Let’s talk a bit about security.

Most internet users around the world are pretty crap at it, but there are basic tools that companies have, and users can enable, to make their accounts, and lives, a little bit more hacker-proof.

One of these — two-factor authentication — just got a big boost from Epic Games, the maker of what is currently The Most Popular Game In The World: Fortnite.

Epic is already getting a ton of great press for what amounts to very little effort.

Son: Do you know what two-factor authentication is?

Me: Uh, yeah?

Son: I get a free dance on @Fortnitegame if I enable two factor. Can we do that?Incentives matter.

— Dennis (@DennisF) August 23, 2018

The company is giving users a new emote (the victory dance you’ve seen emulated in airports, playgrounds and parks by kids and tweens around the world) to anyone who turns on two-factor authentication. It’s one small (dance) step for Epic, but one giant leap for securing their users’ accounts.

The thing is any big company could do this (looking at you Microsoft, Apple, Alphabet and any other company with a huge user base).

Apparently the perk of not getting hacked isn’t enough for most users, but if you give anyone the equivalent of a free dance, they’ll likely flock to turn on the feature.

It’s not that two-factor authentication is a panacea for all security woes, but it does make life harder for hackers. Two-factor authentication works on codes, basically tokens, that are either sent via text or through an over-the-air authenticator (OTA). Text messaging is a pretty crap way to secure things, because the codes can be intercepted, but OTAs — like Google Authenticator or Authy — are sent via https (pretty much bulletproof, but requiring an app to use).

So using SMS-based two-factor authentication is better than nothing, but it’s not Fort Knox (however, these days, even Fort Knox probably isn’t Fort Knox when it comes to security).

Still, anything that makes things harder for crimes of opportunity can help ease the security burden for companies large and small, and the consumers and customers that love them (or at least are forced to pay and use them).

I’m not sure what form the perk could or should take. Maybe it’s the promise of a free e-book or a free download or an opportunity to have a live chat with the celebrity, influencer or athlete of a user’s choice. Whatever it is, there’re clearly something that businesses could do to encourage greater adoption.

Self-preservation isn’t cutting it. Maybe an emote will do the trick.

Powered by WPeMatico

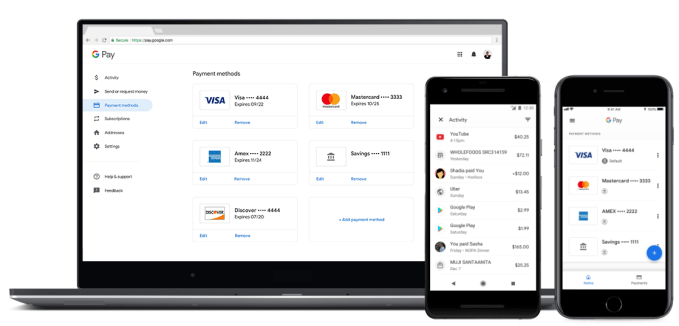

Google is making several updates to Google Pay, its recently-rebranded service for all its different payments tools. Most of these updates were announced earlier this year, but now, Google says they’re actually going live in the app.

One of the additions is peer-to-peer payments. You could already pay or request money from a friend through Google Pay Send, but as of today, you can also do it into the main Google Pay app.

Gerardo Capiel, Director of Product Management at Google Pay, noted that this makes it easier to split the bill with your friends — if you bought something with Google Pay, you can tap on the purchase and then request payment from up to five people.

Since Google is basically combining two apps, it sounds like Google Pay Send isn’t long for this world — as Capiel put it, “We want to basically bring everything into Google Pay,” but he said the timing is “TBD” on when Pay Send might be shut down.

The Google Pay app is also gaining the ability to save mobile tickets and boarding passes, to be found in a new Passes tab that will also include loyalty cards and gift cards. Ticketmaster and Southwest are supported at launch, and Google says it has plans to add Eventbrite, Singapore Airlines and Vueling.

While some of Google Pay’s functionality (like the new Passes Tab) is limited to Android, Capiel said the goal is to support users on any platform. So you can also access Google Pay on the web and on an iOS app. Now Google says it’s making it easier to manage all your payment information across platforms, allowing users (for example) to update their payment info on the web and see it reflected in their app.

Looking ahead, Capiel said his team plans to add support for more ticketing partners, and also to launch the Google Pay app in more countries — particularly the ones where the service is already being used for online payments.

“We’re working to bring everything into the app,” he added. “Some things are a little trickier than others, for a number of reasons, but we will continue to make the experience as complete as possible.”

Powered by WPeMatico