alipay

Auto Added by WPeMatico

Auto Added by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Welcome back to This Week in Apps, the weekly TechCrunch series that recaps the latest in mobile OS news, mobile applications and the overall app economy.

The app industry is as hot as ever, with a record 218 billion downloads and $143 billion in global consumer spend in 2020.

Consumers last year also spent 3.5 trillion minutes using apps on Android devices alone. And in the U.S., app usage surged ahead of the time spent watching live TV. Currently, the average American watches 3.7 hours of live TV per day, but now spends four hours per day on their mobile devices.

Apps aren’t just a way to pass idle hours — they’re also a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus. In 2020, investors poured $73 billion in capital into mobile companies — a figure that’s up 27% year-over-year.

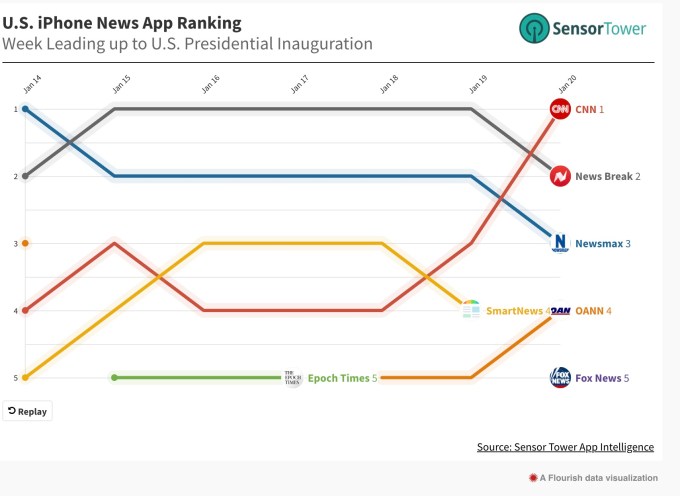

This week, we’re looking into how President Biden’s inauguration impacted news apps, the latest in the Parler lawsuit, and how TikTok’s app continues to shape culture, among other things.

Logos for AWS (Amazon Web Services) and Parler. Image Credits: TechCrunch

U.S. District Judge Barbara Rothstein in Seattle this week ruled that Amazon won’t be required to restore access to web services to Parler. As you may recall, Parler sued Amazon for booting it from AWS’ infrastructure, effectively forcing it offline. Like Apple and Google before it, Amazon had decided that the calls for violence that were being spread on Parler violated its terms of service. It also said that Parler showed an “unwillingness and inability” to remove dangerous posts that called for the rape, torture and assassination of politicians, tech executives and many others, the AP reported.

Amazon’s decision shouldn’t have been a surprise for Parler. Amazon had reported 98 examples of Parler posts that incited violence over the past several weeks before its decision. It told Parler these were clear violations of the terms of service.

Parler’s lawsuit against Amazon, however, went on to claim breach of contract and even made antitrust allegations.

The judge shot down Parler’s claims that Amazon and Twitter were colluding over the decision to kick the app off AWS. Parler’s claims over breach of contract were denied, too, as the contract had never said Amazon had to give Parler 30 days to fix things. (Not to mention the fact that Parler breached the contract on its side, too.) It also said Parler had fallen short in demonstrating the need for an injunction to restore access to Amazon’s web services.

The ruling only blocks Parler from forcing Amazon to again host it as the lawsuit proceeds, but is not the final ruling in the overall case, which is continuing.

@livbedumb♬ drivers license – Olivia Rodrigo

We already knew TikTok was playing a large role in influencing music charts and listening behavior. For example, Billboard last year noted how TikTok drove hits from Sony artists like Doja Cat (“Say So”) and 24kGoldn (“Mood”), and helped Sony discover new talent. Columbia also signed viral TikTok artists like Lil Nas X, Powfu, StaySolidRocky, Jawsh 685, Arizona Zervas and 24kGoldn. Meanwhile, Nielsen has said that no other app had helped break more songs in 2020 than TikTok.

This month, we’ve witnessed yet another example of this phenomenon. Olivia Rodrigo, the 17-year-old star of Disney+’s “High School Musical: The Musical: the Series” released her latest song, “Drivers License” on January 8. The pop ballad and breakup anthem is believed to be referencing the actress’ relationship with co-star Joshua Bassett, which gave the song even more appeal to fans.

Upon its release the song was heavily streamed by TikTok users, which helped make it an overnight sensation of sorts. According to a report by The WSJ, Billboard counted 76.1 million streams and 38,000 downloads in the U.S. during the week of its release. It also made a historic debut at No. 1 on the Hot 100, becoming the first smash hit of 2021.

On January 11, “Drivers License” broke Spotify’s record for most streams per day (for a non-holiday song) with 15.17 million global streams. On TikTok, meanwhile, the number of videos featuring the song and the views they received doubled every day, The WSJ said.

Charli D’Amelio’s dance to it on the app has now generated 5 million “Likes” across nearly 33 million views, as of the time of writing.

@charlidamelio♬ drivers license – Olivia Rodrigo

Of course, other TikTok hits have broken out in the past, too — even reaching No. 1 like “Blinding Lights” (The Weeknd) and “Mood” (24kGoldn). But the success of “Drivers License” may be in part due to the way it focuses on a subject that’s more relevant to TikTok’s young, teenage user base. It talks about first loves and being dumped for the other girl. And its title and opening refer to a time many adults have forgotten: the momentous day when you get your driver’s license. It’s highly relatable to the TikTok crowd who fully embraced it and made it a hit.

Image Credits: Bodyguard

A French content moderation app called Bodyguard, detailed here by TechCrunch, has brought its service to the English-speaking market. The app allows you to choose the level of content moderation you want to see on top social networks, like Twitter, YouTube, Instagram and Twitch. You can choose to hide toxic content across a range of categories, like insults, body shaming, moral harassment, sexual harassment, racism and homophobia and indicate whether the content is a low or high priority to block.

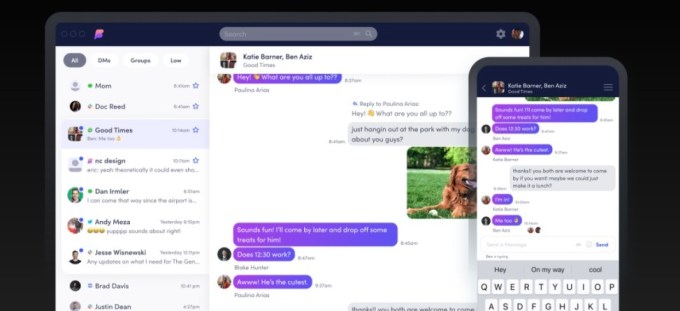

Image Credits: Beeper

Pebble’s founder and current YC Partner Eric Migicovsky has launched a new app, Beeper, that aims to centralize in one interface 15 different chat apps, including iMessage. The app relies on an open-source federated, encrypted messaging protocol called Matrix that uses “bridges” to connect to the various networks to move the messages. However, iMessage support is more wonky, as the company actually ships you an old iPhone to make the connection to the network. But this system allows you to access Beeper on non-Apple devices, the company says. The app is slowly onboarding new users due to initial demand. The app works across MacOS, Windows, Linux, iOS and Android and charges $10/mo for the service.

Powered by WPeMatico

The long-anticipated IPO of Alibaba-affiliated Chinese fintech giant Ant Group could raise tens of billions of dollars in a dual-listing on both the Shanghai and Hong Kong exchanges.

Shares for the company formerly known as Ant Financial are expected to price at around HK$80, or roughly 68 to 69 Chinese Yuan. The company is selling around 134 million shares in the Hong Kong portion of its debut, worth around $17.25 billion American dollars at HK$80 apiece.

Given that the share sale is expected to raise a similar amount of money from its Shanghai listing, the company’s IPO could raise as much as $34.5 billion. That tally would make the debut the largest in history, besting the recent Aramco IPO that raised around $29.4 billion.

Alibaba owns a 33% stake in Ant Group. At its currently expected share price, Ant Group would be worth as much as $310 billion, according to The New York Times, or $313 billion per CNBC.

Ant Group’s huge IPO fits its own epic scale. As TechCrunch reported in July, Ant had around 1.3 billion annual active users in March of this year, a number that could have risen in recent quarters. Ant’s Alipay competes with Tencent’s WeChat Pay in the huge and lucrative Chinese market.

The Ant Group IPO could be viewed as a moment in which the United States stock markets showed weakness. When Alibaba went public back in 2014, it did so via the New York Stock Exchange. The Chinese tech giant later dual-listed on the Hong Kong exchange. To see Ant Group dual-list on the Hong Kong and Shanghai indices without a float in New York shows what is possible outside of the United States when it comes to capital financing.

Fintech startups have broadly seen their fortunes rise during 2020 as the global pandemic changed consumer behavior and moved more commerce and payments into the digital realm. And IPOs have generally performed strongly as well, meaning that Ant Group could find a few tailwinds for its equity when it begins to trade.

Ant has not been content to stick to its knitting, keeping itself busy by investing in other startups. The company took a small stake in installment-payment service Klarna earlier this year, for example.

At a valuation of more than $310 billion, Ant Group would be worth about as much as JPMorgan Chase, the most valuable American bank today. It would also best U.S.-based digital payments leader PayPal, which is currently valued at $236 billion, as well as Square, which is valued at $77 billion.

Powered by WPeMatico

This has been a long time coming, but the OpenStack Foundation today announced that it is changing its name to “Open Infrastructure Foundation,” starting in 2021.

The announcement, which the foundation made at its virtual developer conference, doesn’t exactly come as a surprise. Over the course of the last few years, the organization started adding new projects that went well beyond the core OpenStack project, and renamed its conference to the “Open Infrastructure Summit.” The organization actually filed for the “Open Infrastructure Foundation” trademark back in April.

Image Credits: OpenStack Foundation

After years of hype, the open-source OpenStack project hit a bit of a wall in 2016, as the market started to consolidate. The project itself, which helps enterprises run their private cloud, found its niche in the telecom space, though, and continues to thrive as one of the world’s most active open-source projects. Indeed, I regularly hear from OpenStack vendors that they are now seeing record sales numbers — despite the lack of hype. With the project being stable, though, the Foundation started casting a wider net and added additional projects like the popular Kata Containers runtime and CI/CD platform Zuul.

“We are officially transitioning and becoming the Open Infrastructure Foundation,” long-term OpenStack Foundation executive president Jonathan Bryce told me. “That is something that I think is an awesome step that’s built on the success that our community has spawned both within projects like OpenStack, but also as a movement […], which is [about] how do you give people choice and control as they build out digital infrastructure? And that is, I think, an awesome mission to have. And that’s what we are recognizing and acknowledging and setting up for another decade of doing that together with our great community.”

In many ways, it’s been more of a surprise that the organization waited as long as it did. As the foundation’s COO Mark Collier told me, the team waited because it wanted to be sure that it did this right.

“We really just wanted to make sure that all the stuff we learned when we were building the OpenStack community and with the community — that started with a simple idea of ‘open source should be part of cloud, for infrastructure.’ That idea has just spawned so much more open source than we could have imagined. Of course, OpenStack itself has gotten bigger and more diverse than we could have imagined,” Collier said.

As part of today’s announcement, the group also announced that its board approved four new members at its Platinum tier, its highest membership level: Ant Group, the Alibaba affiliate behind Alipay, embedded systems specialist Wind River, China’s FiberHome (which was previously a Gold member) and Facebook Connectivity. These companies will join the new foundation in January. To become a Platinum member, companies must contribute $350,000 per year to the foundation and have at least two full-time employees contributing to its projects.

“If you look at those companies that we have as Platinum members, it’s a pretty broad set of organizations,” Bryce noted. “AT&T, the largest carrier in the world. And then you also have a company Ant, who’s the largest payment processor in the world and a massive financial services company overall — over to Ericsson, that does telco, Wind River, that does defense and manufacturing. And I think that speaks to that everybody needs infrastructure. If we build a community — and we successfully structure these communities to write software with a goal of getting all of that software out into production, I think that creates so much value for so many people: for an ecosystem of vendors and for a great group of users and a lot of developers love working in open source because we work with smart people from all over the world.”

The OpenStack Foundation’s existing members are also on board and Bryce and Collier hinted at several new members who will join soon but didn’t quite get everything in place for today’s announcement.

We can probably expect the new foundation to start adding new projects next year, but it’s worth noting that the OpenStack project continues apace. The latest of the project’s bi-annual releases, dubbed “Victoria,” launched last week, with additional Kubernetes integrations, improved support for various accelerators and more. Nothing will really change for the project now that the foundation is changing its name — though it may end up benefitting from a reenergized and more diverse community that will build out projects at its periphery.

Powered by WPeMatico

“Animal Crossing: New Horizons” is a bonafide wonder. The game has been setting new records for Nintendo, is adored by players and critics alike and provides millions of players a peaceful escape during these unprecedented times.

But there’s been something even more extraordinary happening on the fringe: Players are finding ways to augment the game experience through community-organized activities and tools. These include free weed-pulling services (tips welcome!) from virtual Samaritans, and custom-designed items for sale — for real-world money, via WeChat Pay and AliPay.

Well-known personalities and companies are also contributing, with “Rogue One: A Star Wars Story” scribe Gary Whitta hosting an A-list celebrity talk show using the game, and luxury fashion brand Marc Jacobs providing some of its popular clothing designs to players. 100 Thieves, the white-hot esports and apparel company, even created and gave away digital versions of its entire collection of impossible-to-find clothes.

This community-based phenomenon gives us a pithy glimpse into not only where games are inevitably going, but what their true potential is as a form of creative, technical and economic expression. It also exemplifies what we at Forte call “community economics,” a system that lies at the heart of our aim in bringing new creative and economic opportunities to billions of people around the world.

Formally, community economics is the synthesis of economic activity that takes place inside, and emerges outside, virtual game worlds. It is rooted in a cooperative economic relationship between all participants in a game’s network, and characterized by an economic pluralism that is unified by open technology owned by no single party. And notably, it results in increased autonomy for players, better business models for game creators, and new economic and creative opportunities for both.

The fundamental shift that underlies community economics is the evolution of games from centralized entertainment experiences to open economic platforms. We believe this is where things are heading.

Powered by WPeMatico

Zhihu may not be as well known outside of China as WeChat or ByteDance’s Douyin, but over the past eight years, it has cultivated a reputation for being one of the country’s most trustworthy social media platforms. Originally launched as a question-and-answer site similar to Quora, Zhihu has grown to be a central hub for professional knowledge, allowing users to interact with experts and companies in a wide range of industries.

Headquartered in Beijing, Zhihu recently raised a $434 million Series F, its biggest round since 2011. The funding also brought Zhihu two important new partners: video and live-streaming app Beijing Kuaishou, which led the round, and Baidu, owner of China’s largest search engine (other participants in the round included Tencent and CapitalToday).

Launched in 2011, Zhihu (the name means “do you know”) is most frequently compared to Quora and Yahoo Answers. While it resembled those Q&A platforms at first, it has grown in scope. Now it would be more accurate to say that the platform is like a combination of Quora, LinkedIn and Medium’s subscription program.

For example, Zhihu has an invitation-only blogging platform for verified experts and since launching official accounts, it has become a channel for companies and organizations to communicate with users. A representative for Zhihu told TechCrunch that the platform had 220 million users and 30,000 official accounts as of January 2019 (for context, there are currently about 800 million Internet users in China), who have posted a total of 130 million answers so far.

The company’s growth will be closely watched since Zhihu is reportedly preparing for an initial public offering. Last November, the company hired its first chief financial officer, Sun Wei, heightening speculation. A representative for the company told TechCrunch the position was created because of Zhihu’s business development needs and that there is currently no timeline for a public listing.

At the same time, the company has also dealt with reports that its growth has slowed.

Powered by WPeMatico

China’s war on garbage is as digitally savvy as the country itself. Think QR codes attached to trash bags that allow a municipal government to trace exactly where its trash comes from.

On July 1, the world’s most populated city (Shanghai) began a compulsory garbage-sorting program. Under the new regulations (in Chinese), households and companies must classify their wastes into four categories and dump them in designated places at certain times. Noncompliance can lead to fines. Companies and properties that don’t comply risk having their credit rating lowered.

The strict regime became the talk of the city’s more than 24 million residents, who criticized the program’s inflexibility and confusing waste categorization. Gratefully, China’s tech startups are here to help.

For instance, China’s biggest internet companies responded with new search features that help people identify which wastes are “wet” (compostable), “dry,, “toxic,” or “recyclable.” Not even the most environmentally conscious person can get all the answers right. Like, which bin does the newspaper you just used to pick up dog poop belong to? Simply pull up a mini app on WeChat, Baidu or Alipay and enter the keyword. The tech firms will give you the answer and why.

A WeChat mini program that lets users learn the category of cash

Alipay, Alibaba’s electronics payment affiliate, claims its garbage-sorting mini app added one million users in just three days. The lite app, which is available without download inside the e-wallet with one billion users, has so far indexed more than 4,000 types of rubbish. Its database is still growing, and soon it will save people from typing by using image recognition to classify trash when they snap a photo of it. Alibaba’s answer to Alexa Tmall Genie can already answer (in Chinese) the question “what kind of trash is a wet wipe?” and more.

If people are too busy or lazy to hit the collection schedule, well, startups are offering valet trash service at the doorstep. A third-party developer helped Alipay build a recycling mini app (“垃圾分类回收平台”) and is now collecting garbage from 8,000 apartment complexes across 11 cities. To date, two million people have sold recyclable material through its platform.

Ele.me, Alibaba’s food delivery arm, added trash pickup to its list of valet services its fleets offer on top of “apologize to the girlfriend” and dog walking.

Alibaba’s food delivery & local service platform https://t.co/Yh95Bt0DPG just rolled out a “throw out the trash” service for $2. The delivery guy can also “apologize to the girlfriend” on your behalf among other things #DigitalEconomyinChina $BABA pic.twitter.com/C2ey1ePDvJ

— Krystal Hu (@readkrystalhu) June 24, 2019

Besides helping households, companies are also building software to make property managers’ lives easier. Some residential complexes in Shanghai began using QR codes to trace the origin of garbage, state-owned media outlet Xinhua reported. Each household is asked to attach a unique QR code to their trash bags, which will be scanned for sources and classification when they arrive at the waste management station.

Workers at a waste management station in Shanghai scan codes on trash bags to check their source (Screenshot from Xinhua feature)

This way, regulators in the region know exactly which family has produced the trash — although the city’s current garbage regulations do not require real-name tracking — and those who correctly categorized receive a small reward of 0.1 yuan, or 1.45 cents, per day, according to another report (in Chinese) from Xinhua.

Powered by WPeMatico

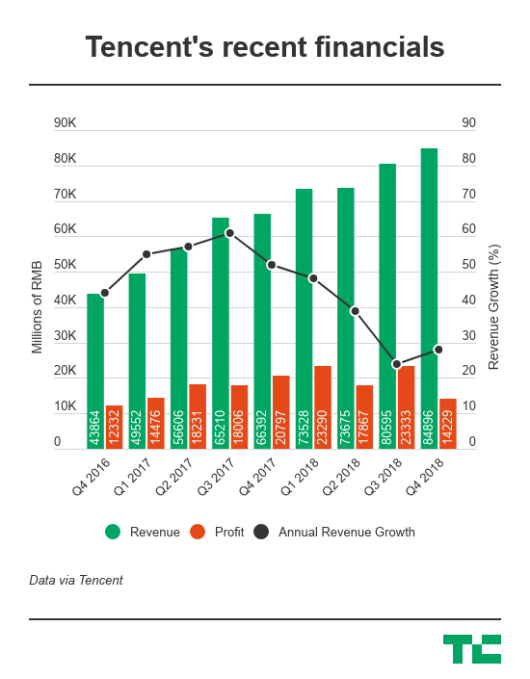

China’s Tencent reported disappointing profits in the fourth quarter on the back of surging costs but saw emerging businesses pick up steam as it plots to diversify amid slackening gaming revenues.

Net profit for the quarter slid 32 percent to 14.2 billion yuan ($2.1 billion), behind analysts’ forecast of 18.3 billion yuan. The decrease was due to one-off expenses related to its portfolio companies and investments in non-gaming segments like video content and financial technology.

Excluding non-cash items and M&A deals, Tencent’s net profit from the period rose 13 percent to 19.7 billion yuan ($2.88 billion). The company has to date invested in more than 700 companies, 100 of which are valued over $1 billion each and 60 of which have gone public.

Quarterly revenue edged up 28 percent to 84.9 billion yuan ($12.4 billion) beating expectations.

The Hong Kong-listed company is best known for its billion-user WeChat messenger but had for years relied heavily on a high-margin gaming business. That was until a months-long freeze on games approvals last year that delayed monetization for new titles, spurring a major reorg in the firm to put more focus on enterprise services, including cloud computing and financial technology.

Tencent has received approvals for eight games since China resumed the licensing process, although its blockbusters PlayerUnknown Battlegrounds and Fortnite have yet to get the green light. The firm also warned of a “sizeable backlog” for license applications in the industry, which means its “scheduled game releases will initially be slower than in some prior years.”

Video games for the quarter contributed 28.5 percent of Tencent’s total revenues, compared to 36.7 percent in the year-earlier period. Despite the domestic fiasco, Tencent remains as the world’s largest games publisher by revenue, according to data compiled by NewZoo. The firm has also gotten more aggressive in taking its titles global.

Social network revenues rose 25 percent on account of growth in live streaming and video subscriptions. The segment made up 22.9 percent of total revenues. Tencent has in recent years spent heavily on making original content and licensing programs as it competes with Baidu’s iQiyi video streaming site. Tencent claimed 89 million subscribers in the latest quarter, compared with iQiyi’s 87.4 million.

Tencent has been relatively slow to monetize WeChat in contrast to its western counterpart Facebook, though it’s under more pressure to step up its game. Tencent’s advertising revenue from the quarter grew 38 percent thanks to expanding advertising inventory on WeChat. Ads accounted for 20 percent of the firm’s quarterly revenues.

All told, WeChat and its local version Weixin reached nearly 1.1 billion monthly active users; 750 million of them checked their friends’ WeChat feeds, and Tencent recently introduced a Snap Story-like feature to lock users in as it vies for eyeball time with challenger TikTok.

The “others” category, composed of financial technology and cloud computing, grew 71.8 percent to generate 28.5 percent of total revenues. WeChat’s e-wallet, which is going neck-and-neck with Alibaba affiliate Alipay, saw daily transaction volume exceed 1 billion last year. During the fourth quarter, merchants who used WeChat Pay monthly grew more than 80 percent year-over-year.

Meanwhile, cloud revenues doubled to 9.1 billion yuan in 2018, thanks to Tencent’s dominance in the gaming sector as its cloud infrastructure now powers over half of the China-based games companies and is following these clients overseas. Tencent meets Alibaba head-on again in the cloud sector. For comparison, Alibaba’s most recent quarterly cloud revenue was 6.6 billion yuan. Just yesterday, the e-commerce leader claimed that its cloud business is larger than the second to eight players in China combined.

Powered by WPeMatico