alibaba group

Auto Added by WPeMatico

Auto Added by WPeMatico

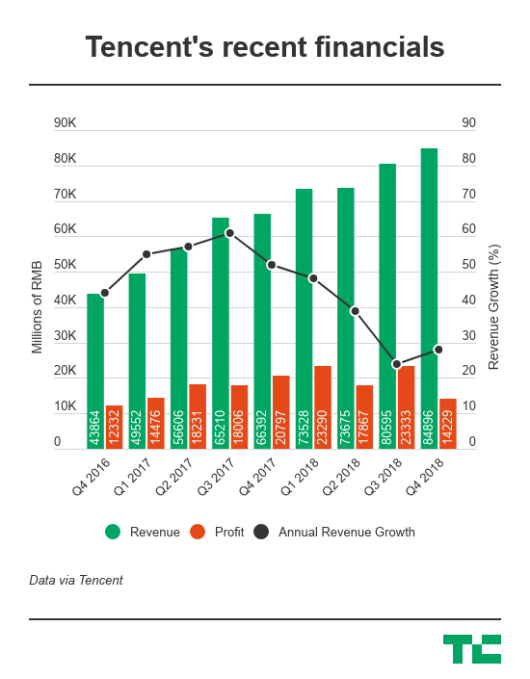

China’s Tencent reported disappointing profits in the fourth quarter on the back of surging costs but saw emerging businesses pick up steam as it plots to diversify amid slackening gaming revenues.

Net profit for the quarter slid 32 percent to 14.2 billion yuan ($2.1 billion), behind analysts’ forecast of 18.3 billion yuan. The decrease was due to one-off expenses related to its portfolio companies and investments in non-gaming segments like video content and financial technology.

Excluding non-cash items and M&A deals, Tencent’s net profit from the period rose 13 percent to 19.7 billion yuan ($2.88 billion). The company has to date invested in more than 700 companies, 100 of which are valued over $1 billion each and 60 of which have gone public.

Quarterly revenue edged up 28 percent to 84.9 billion yuan ($12.4 billion) beating expectations.

The Hong Kong-listed company is best known for its billion-user WeChat messenger but had for years relied heavily on a high-margin gaming business. That was until a months-long freeze on games approvals last year that delayed monetization for new titles, spurring a major reorg in the firm to put more focus on enterprise services, including cloud computing and financial technology.

Tencent has received approvals for eight games since China resumed the licensing process, although its blockbusters PlayerUnknown Battlegrounds and Fortnite have yet to get the green light. The firm also warned of a “sizeable backlog” for license applications in the industry, which means its “scheduled game releases will initially be slower than in some prior years.”

Video games for the quarter contributed 28.5 percent of Tencent’s total revenues, compared to 36.7 percent in the year-earlier period. Despite the domestic fiasco, Tencent remains as the world’s largest games publisher by revenue, according to data compiled by NewZoo. The firm has also gotten more aggressive in taking its titles global.

Social network revenues rose 25 percent on account of growth in live streaming and video subscriptions. The segment made up 22.9 percent of total revenues. Tencent has in recent years spent heavily on making original content and licensing programs as it competes with Baidu’s iQiyi video streaming site. Tencent claimed 89 million subscribers in the latest quarter, compared with iQiyi’s 87.4 million.

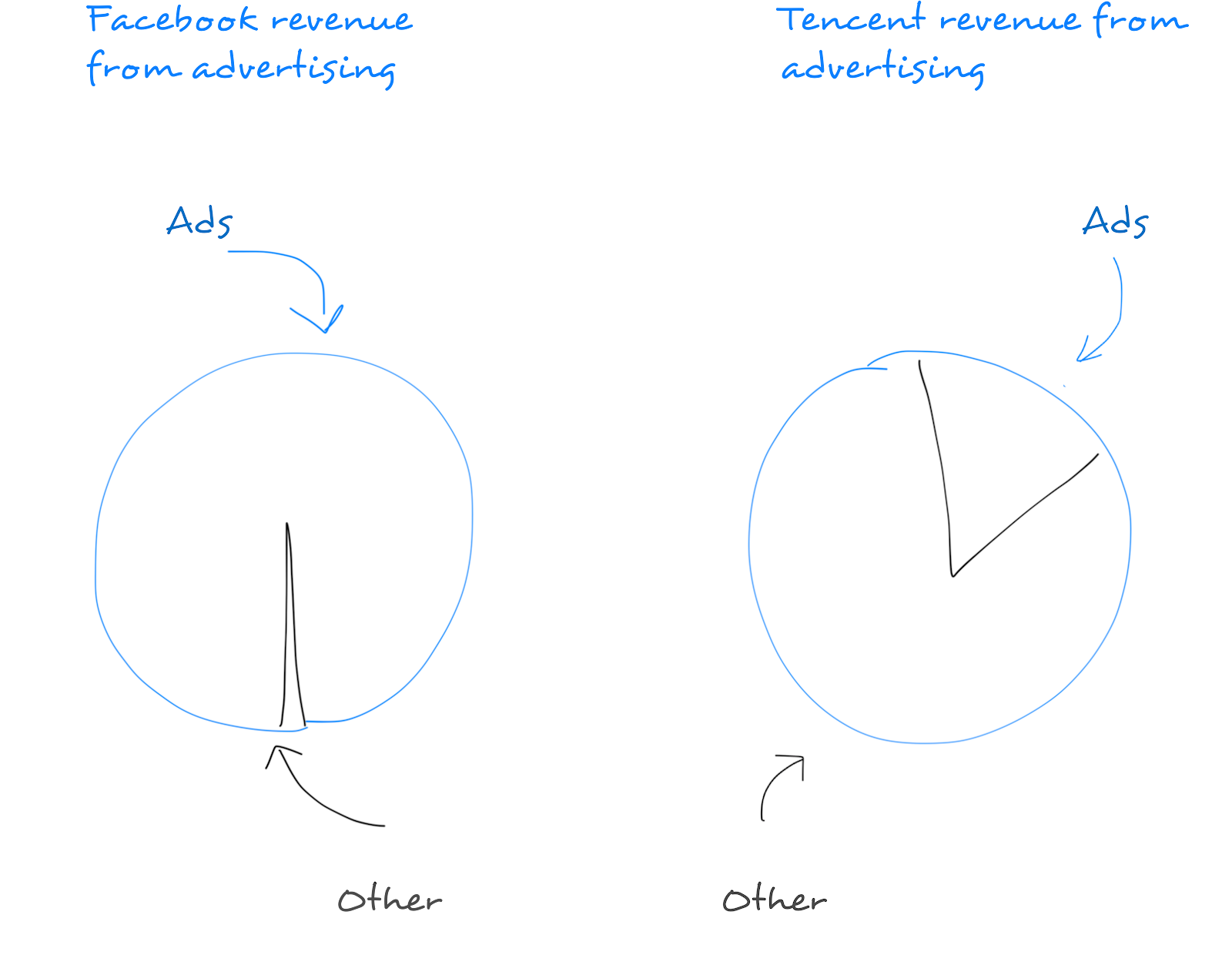

Tencent has been relatively slow to monetize WeChat in contrast to its western counterpart Facebook, though it’s under more pressure to step up its game. Tencent’s advertising revenue from the quarter grew 38 percent thanks to expanding advertising inventory on WeChat. Ads accounted for 20 percent of the firm’s quarterly revenues.

All told, WeChat and its local version Weixin reached nearly 1.1 billion monthly active users; 750 million of them checked their friends’ WeChat feeds, and Tencent recently introduced a Snap Story-like feature to lock users in as it vies for eyeball time with challenger TikTok.

The “others” category, composed of financial technology and cloud computing, grew 71.8 percent to generate 28.5 percent of total revenues. WeChat’s e-wallet, which is going neck-and-neck with Alibaba affiliate Alipay, saw daily transaction volume exceed 1 billion last year. During the fourth quarter, merchants who used WeChat Pay monthly grew more than 80 percent year-over-year.

Meanwhile, cloud revenues doubled to 9.1 billion yuan in 2018, thanks to Tencent’s dominance in the gaming sector as its cloud infrastructure now powers over half of the China-based games companies and is following these clients overseas. Tencent meets Alibaba head-on again in the cloud sector. For comparison, Alibaba’s most recent quarterly cloud revenue was 6.6 billion yuan. Just yesterday, the e-commerce leader claimed that its cloud business is larger than the second to eight players in China combined.

Powered by WPeMatico

Chinese AI startup Tianrang has raised a $26 million (RMB180 million) funding round from China’s Gaorong Capital and co-lead CMB International Capital. Other investors included Ziniu Fund and Chinese fintech company Wacai. In 2016, the company raised an angel round led by Gaorong Capital and participated in by Shanghai Jindi Investment Management Ltd.

Based on deep learning and other AI technology, Tianrang provides data analysis and smart solutions for enterprises. It was founded by in 2016 by Xu Guirong, former director of Alibaba’s Ali Cloud and chief scientist at Alibaba’s cloud platform Alimama. So no slouch on the AI front.

Tianrang claims to be able to automatically collect and analyze marketing trends and purchase-related information on Alibaba’s e-commerce platform, allowing vendors to make better marketing decisions.

Wang Hongbo, chief investment officer at CMB International Capital says: “With algorithm and AI, Tianrang lowers the requirement of complex machine decision-making and makes it accessible and scalable for commercial use.”

Tianrang also plans to set up a project to apply machine learning to the urban development of cities, led by Jessie Li, a professor at the College of Information Sciences and Technology of Pennsylvania State University.

Powered by WPeMatico

Airwallex, a three-year-old fintech startup focused on international payments for SMEs and businesses, is putting itself on the map after it raised an $80 million Series B round.

Based out of Melbourne, but with six offices in Asia and other parts of the world, Airwallex’s new funding round is the second-largest financing deal for an Australian startup in history. The round was led by existing investors Tencent, the $500 billion Chinese internet giant, and Sequoia China. Other participants included China’s Hillhouse, Horizons Ventures — the fund from Hong Kong’s richest man, Li Ka-Shing — Indonesia-based Central Capital Ventura (BCA) and Australia’s Square Peg, a firm from Paul Bassat, who took recruitment firm Seek to IPO and is one of Australia’s highest-profile founders.

The financing takes Airwallex to $102 million raised. Tencent led a $13 million Series A in May 2017, while Square Peg added $6 million more via a Series A+ in December. Mastercard is also a backer; the finance giant uses Airwallex to handle its “Send” product, while Tencent uses the service to power an overseas remittance service for its WeChat app.

Airwallex handles cross-border transactions for companies that do business in multiple countries using international currencies. So it’s not unlike a TransferWise-style service for SMEs that lack the capital to develop a sophisticated (and expensive) international banking system of their own.

The service uses wholesale FX rates to route overseas payments back to a client’s domestic bank and is capable of processing “thousands of transactions per second,” according to the company. A use case example might include helping a China-based seller return money earned in the U.S. or Europe via Amazon or other e-commerce services, or route sales revenue back directly from their own website.

Airwallex CEO Jack Zhang (far right) onstage at TechCrunch Shenzhen in 2017

China is a key market for Airwallex — which was started by four Australian-Chinese founders — as well as the wider Asian region, and in particular Australia, Hong Kong and Southeast Asia. With this new capital, Airwallex co-founder and CEO Jack Zhang said the company will increase its focus on Hong Kong and Southeast Asia, whilst also extending its business in Europe (where it has a London-based office) and pushing into North America.

Product R&D is shared across Melbourne and Shanghai, while Hong Kong accounts for business development, compliance and more, Zhang explained. However, Airwallex’s locations in London and San Francisco are likely to account for most of the upcoming headcount growth planned following this funding. Right now, Airwallex has around 100 staff, according to Zhang.

The company is also aiming to expand its product range.

The firm is in the process of applying for a virtual banking license in Hong Kong, a third-party payment license in mainland China and a cross-border Chinese yuan license. One goal, Zhang revealed, is to offer working capital loans to SMEs to help them scale their businesses to the next level. Airwallex is working with an undisclosed partner to underwrite deals in the future. Zhang explained that the company sees a gap in the market since banks don’t have access to critical data on clients for loan assessments.

More generally, he’s bullish for the future, despite Brexit and the ongoing trade war between the U.S. and China.

“The trade war gives the Chinese yuan a lot of vitality, and we’ve seen more demand in the market. China’s belt road initiative has really taken off, too, and we’re seeing the impact in many, many of our payment corridors,” he explained. “Business has been booming, especially as traditional offline SMEs start to move online and go from domestic to global.”

“We want to be the backbone to support these new opportunities for businesses,” Zhang added.

Powered by WPeMatico

Since the dawn of the internet, the titans of this industry have fought to win the “starting point” — the place that users start their online experiences. In other words, the place where they begin “browsing.” The advent of the dial-up era had America Online mailing a CD to every home in America, which passed the baton to Yahoo’s categorical listings, which was swallowed by Google’s indexing of the world’s information — winning the “starting point” was everything.

As the mobile revolution continues to explode across the world, the battle for the starting point has intensified. For a period of time, people believed it would be the hardware, then it became clear that the software mattered most. Then conversation shifted to a debate between operating systems (Android or iOS) and moved on to social properties and messaging apps, where people were spending most of their time. Today, my belief is we’re hovering somewhere between apps and operating systems. That being said, the interface layer will always be evolving.

The starting point, just like a rocket’s launchpad, is only important because of what comes after. The battle to win that coveted position, although often disguised as many other things, is really a battle to become the starting point of commerce.

Google’s philosophy includes a commitment to get users “off their page” as quickly as possible…to get that user to form a habit and come back to their starting point. The real (yet somewhat veiled) goal, in my opinion, is to get users to search and find the things they want to buy.

Of course, Google “does no evil” while aggregating the world’s information, but they pay their bills by sending purchases to Priceline, Expedia, Amazon and the rest of the digital economy.

Facebook, on the other hand, has become a starting point through its monopolization of users’ time, attention and data. Through this effort, it’s developed an advertising business that shatters records quarter after quarter.

Google and Facebook, this famed duopoly, represent 89 percent of new advertising spending in 2017. Their dominance is unrivaled… for now.

Change is urgently being demanded by market forces — shifts in consumer habits, intolerable rising costs to advertisers and through a nearly universal dissatisfaction with the advertising models that have dominated (plagued) the U.S. digital economy. All of which is being accelerated by mobile. Terrible experiences for users still persist in our online experiences, deliver low efficacy for advertisers and fraud is rampant. The march away from the glut of advertising excess may be most symbolically seen in the explosion of ad blockers. Further evidence of the “need for a correction of this broken industry” is Oracle’s willingness to pay $850 million for a company that polices ads (probably the best entrepreneurs I know ran this company, so no surprise).

As an entrepreneur, my job is to predict the future. When reflecting on what I’ve learned thus far in my journey, it’s become clear that two truths can guide us in making smarter decisions about our digital future:

Every day, retailers, advertisers, brands and marketers get smarter. This means that every day, they will push the platforms, their partners and the places they rely on for users to be more “performance driven.” More transactional.

Paying for views, bots (Russian or otherwise) or anything other than “dollars” will become less and less popular over time. It’s no secret that Amazon, the world’s most powerful company (imho), relies so heavily on its Associates Program (its home-built partnership and affiliate platform). This channel is the highest performing form of paid acquisition that retailers have, and in fact, it’s rumored that the success of Amazon’s affiliate program led to the development of AWS due to large spikes in partner traffic.

Chinese flag overlooking The Bund, Shanghai, China (Photo: Rolf Bruderer/Getty Images)

When thinking about our digital future, look down and look east. Look down and admire your phone — this will serve as your portal to the digital world for the next decade, and our dependence will only continue to grow. The explosive adoption of this form factor is continuing to outpace any technological trend in history.

Now, look east and recognize that what happens in China will happen here, in the West, eventually. The Chinese market skipped the PC-driven digital revolution — and adopted the digital era via the smartphone. Some really smart investors have built strategies around this thesis and have quietly been reaping rewards due to their clairvoyance.

China has historically been categorized as a market full of knock-offs and copycats — but times have changed. Some of the world’s largest and most innovative companies have come out of China over the past decade. The entrepreneurial work ethic in China (as praised recently by arguably the world’s greatest investor, Michael Moritz), the speed of innovation and the ability to quickly scale and reach meaningful populations have caused Chinese companies to leapfrog the market cap of many of their U.S. counterparts.

The most interesting component of the Chinese digital economy’s growth is that it is fundamentally more “pure” than the U.S. market’s. I say this because the Chinese market is inherently “transactional.” As Andreessen Horowitz writes, WeChat, China’s most valuable company, has become the “starting point” and hub for all user actions. Their revenue diversity is much more “Amazon” than “Google” or “Facebook” — it’s much more pure. They make money off the transactions driven from their platform, and advertising is far less important in their strategy.

The obsession with replicating WeChat took the tech industry by storm two years ago — and for some misplaced reason, everyone thought we needed to build messaging bots to compete.

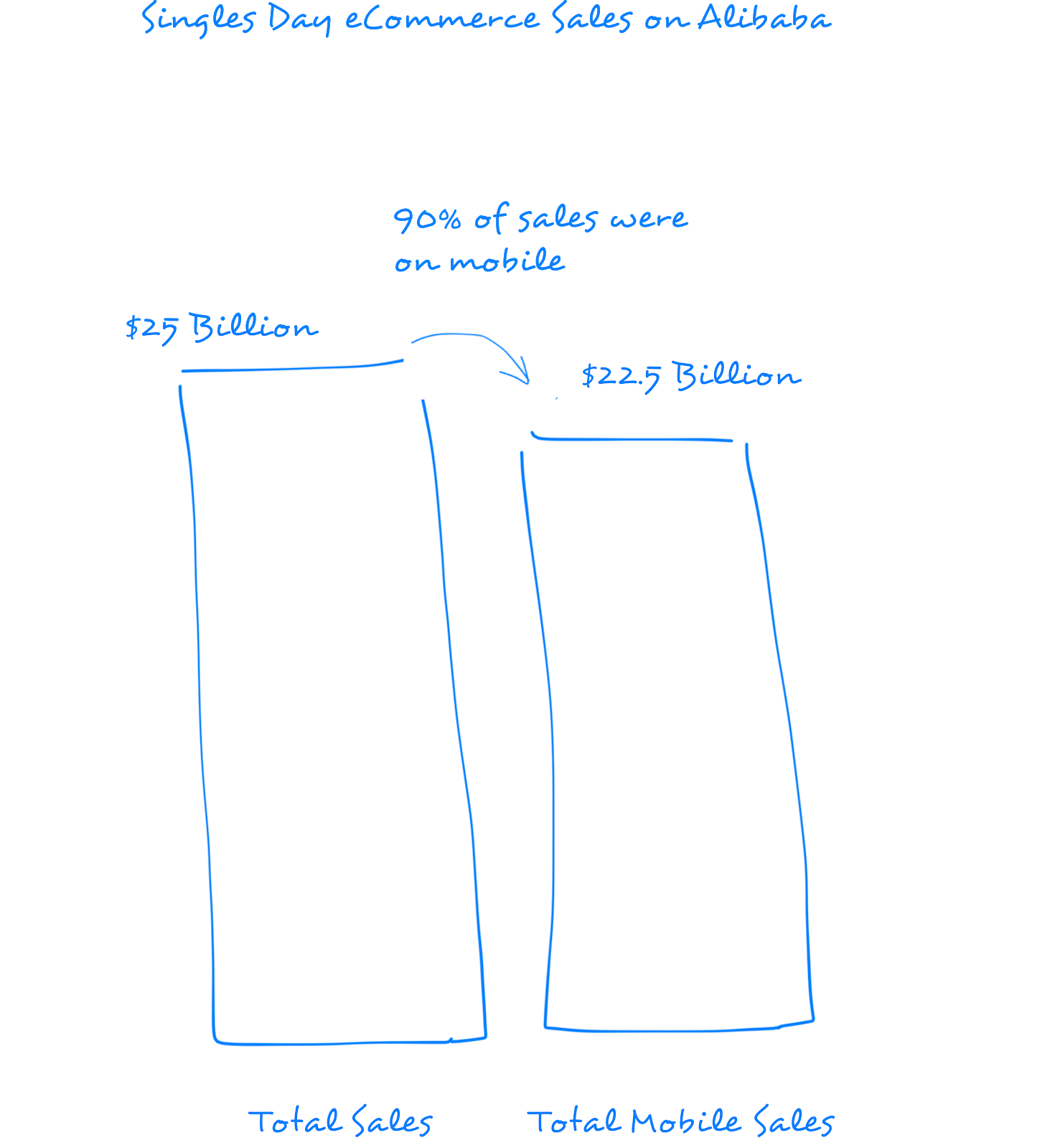

What shouldn’t be lost is our obsession with the purity and power of the business models being created in China. The fabric that binds the Chinese digital economy and has fostered its seemingly boundless growth is the magic combination of commerce and mobile. Singles Day, the Chinese version of Black Friday, drove $25 billion in sales on Alibaba — 90 percent of which were on mobile.

The lesson we’ve learned thus far in both the U.S. and in China is that “consumers spending money” creates the most durable consumer businesses. Google, putting aside all its moonshots and heroic mission statements, is a “starting point” powered by a shopping engine. If you disagree, look at where their revenue comes from…

Google’s recent announcement of Shopping Actions and their movement to a “pay per transaction model” signals a turning point that could forever change the landscape of the digital economy.

Google’s multi-front battle against Apple, Facebook and Amazon is weighted. Amazon is the most threatening. It’s the most durable business of the four — and its model is unbounded on two fronts that almost everyone I know would bet their future on, 1) people buying more online, where Amazon makes a disproportionate amount of every dollar spent, and 2) companies needing more cloud computing power (more servers), where Amazon makes a disproportionate amount of every dollar spent.

To add insult to injury, Amazon is threatening Google by becoming a starting point itself — 55 percent of product searches now originate at Amazon, up from 30 percent just a year ago.

Google, recognizing consumer behavior was changing in mobile (less searching) and the inferiority of their model when compared to the durability and growth prospects of Amazon, needed to respond. Google needed a model that supported boundless growth and one that created a “win-win” for its advertising partners — one that resembled Amazon’s relationship with its merchants — not one that continued to increase costs to retailers while capitalizing on their monopolization of search traffic.

Google knows that with its position as the starting point — with Google.com, Google Apps and Android — it has to become a part of the transaction to prevail in the long term. With users in mobile demanding fewer ads and more utility (demanding experiences that look and feel a lot more like what has prevailed in China), Google has every reason in the world to look down and to look east — to become a part of the transaction — to take its piece.

A collision course for Google and the retailers it relies upon for revenue was on the horizon. Search activity per user was declining in mobile and user acquisition costs were growing quarter over quarter. Businesses are repeatedly failing to compete with Amazon, and unless Google could create an economically viable growth model for retailers, no one would stand a chance against the commerce juggernaut — not the retailers nor Google itself.

As I’ve believed for a long time, becoming a part of the transaction is the most favorable business model for all parties; sources of traffic make money when retailers sell things, and, most importantly, this only happens when users find the things they want.

Shopping Actions is Google’s first ambitious step to satisfy all three parties — businesses and business models all over the world will feel this impact.

Good work, Sundar.

Powered by WPeMatico

Beijing-based bike-sharing startup Ofo has raised $866 million in new financing led by Alibaba Group to fuel its expensive competition with Mobike, which is backed by Tencent, one of Alibaba’s biggest rivals. Ofo and Mobike are the two largest bike-sharing companies in China. Read More

Beijing-based bike-sharing startup Ofo has raised $866 million in new financing led by Alibaba Group to fuel its expensive competition with Mobike, which is backed by Tencent, one of Alibaba’s biggest rivals. Ofo and Mobike are the two largest bike-sharing companies in China. Read More

Powered by WPeMatico

Despite hiccups, Yahoo’s planned sale to Verizon appears to be moving forward — but some portions of the company will be left behind and renamed Altaba Inc.

Despite hiccups, Yahoo’s planned sale to Verizon appears to be moving forward — but some portions of the company will be left behind and renamed Altaba Inc.

Yahoo is hanging on to its 15 percent stake in Alibaba and its 35.5 percent stake in Yahoo Japan, and those assets will survive as an investment company under the new name Altaba Inc., as the rest of Yahoo integrates with Verizon. Read More

Powered by WPeMatico

One of the saddest scenes in the Lord Of The Rings trilogy is watching the slow-moving Ents – the massive tree shepherds that took days to decide whether or not to react Sauron’s onslaught – are cut down by the wily Orcs. Only a few fall in the battle but when they do the giants of the forests that at first seemed so powerful are exposed to be easily vanquished. They won… Read More

One of the saddest scenes in the Lord Of The Rings trilogy is watching the slow-moving Ents – the massive tree shepherds that took days to decide whether or not to react Sauron’s onslaught – are cut down by the wily Orcs. Only a few fall in the battle but when they do the giants of the forests that at first seemed so powerful are exposed to be easily vanquished. They won… Read More

Powered by WPeMatico

Aliyun, the cloud computing unit of Alibaba Group, is launching an artificial intelligence service that it claims is the first in China. Called DT PAI, the platform combines algorithms used by Alibaba with machine and deep learning techniques and presents them in a simple drag-and-drop interface. Aliyun says developers can use DT PAI to predict user behavior without having to write new code. Read More

Aliyun, the cloud computing unit of Alibaba Group, is launching an artificial intelligence service that it claims is the first in China. Called DT PAI, the platform combines algorithms used by Alibaba with machine and deep learning techniques and presents them in a simple drag-and-drop interface. Aliyun says developers can use DT PAI to predict user behavior without having to write new code. Read More

Powered by WPeMatico

Alibaba will reportedly invest $1.25 billion in Ele.me, a food delivery service based in Shanghai, says financial news site Caixin (link via Google Translate). The deal would Alibaba the startup’s biggest shareholder, with a 27.7 percent stake.

Alibaba will reportedly invest $1.25 billion in Ele.me, a food delivery service based in Shanghai, says financial news site Caixin (link via Google Translate). The deal would Alibaba the startup’s biggest shareholder, with a 27.7 percent stake.