Alabama

Auto Added by WPeMatico

Auto Added by WPeMatico

Zack Parisa and Max Nova, the co-founders of the carbon offset company SilviaTerra, have spent the last decade working on a way to democratize access to revenue-generating carbon offsets.

As forestry credits become a big, booming business on the back of multibillion-dollar commitments from some of the world’s biggest companies to decarbonize their businesses, the kinds of technologies that the two founders have dedicated 10 years of their lives to building are only going to become more valuable.

That’s why their company, already a profitable business, has raised $4.4 million in outside funding led by Union Square Ventures and Version One Ventures, along with Salesforce founder and the driving force between the One Trillion Trees Initiative, Marc Benioff .

“Key to addressing the climate crisis is changing the balance in the so-called carbon cycle. At present, every year we are adding roughly 5 gigatons of carbon to the atmosphere. Since atmospheric carbon acts as a greenhouse gas this increases the energy that’s retained rather than radiated back into space which causes the earth to heat up,” writes Union Square Ventures managing partner Albert Wenger in a blog post. “There will be many ways such drawdown occurs and we will write about different approaches in the coming weeks (such as direct air capture and growing kelp in the oceans). One way that we understand well today and can act upon immediately are forests. The world’s forests today absorb a bit more than one gigatons of CO2 per year out of the atmosphere and turn it into biomass. We need to stop cutting and burning down existing forests (including preventing large scale forest fires) and we have to start planting more new trees. If we do that, the total potential for forests is around 4 to 5 gigatons per year (with some estimates as high as 9 gigatons).”

For the two founders, the new funding is the latest step in a long journey that began in the woods of Northern Alabama, where Parisa grew up.

After attending Mississippi State for forestry, Parisa went to graduate school at Yale, where he met Louisville, Kentucky native Max Nova, a computer science student who joined with Parisa to set up the company that would become SilviaTerra.

SilviaTerra co-founders Max Nova and Zack Parisa. Image Credit: SilviaTerra

The two men developed a way to combine satellite imagery with field measurements to determine the size and species of trees in every acre of forest.

While the first step was to create a map of every forest in the U.S., the ultimate goal for both men was to find a way to put a carbon market on equal footing with the timber industry. Instead of cutting trees for cash, potentially landowners could find out how much it would be worth to maintain their forestland. As the company notes, forest management had previously been driven by the economics of timber harvesting, with over $10 billion spent in the U.S. each year.

The founders at SilviaTerra thought that the carbon market could be equally as large, but it’s hard for most landowners to access. Carbon offset projects can cost as much as $200,000 to put together, which is more than the value of the smaller offset projects for landowners like Parisa’s own family and the 40 acres they own in the Alabama forests.

There had to be a better way for smaller landowners to benefit from carbon markets too, Parisa and Nova thought.

To create this carbon economy, there needed to be a single source of record for every tree in the U.S. and while SilviaTerra had the technology to make that map, they lacked the compute power, machine learning capabilities and resources to build the map.

That’s where Microsoft’s AI for Earth program came in.

Working with AI for Earth, SilviaTierra created their first product, Basemap, to process terabytes of satellite imagery to determine the sizes and species of trees on every acre of America’s forestland. The company also worked with the U.S. Forestry Service to access their data, which was used in creating this holistic view of the forest assets in the U.S.

With the data from Basemap in hand, the company has created what it calls the Natural Capital Exchange. This program uses SilviaTerra’s unparalleled access to information about local forests, and the knowledge of how those forests are currently used to supply projects that actually represent land that would have been forested were it not for the offset money coming in.

Currently, many forestry projects are being passed off to offset buyers as legitimate offsets on land that would never have been forested in the first place — rendering the project meaningless and useless in any real way as an offset for carbon dioxide emissions.

“It’s a bloodbath out there,” said Nova of the scale of the problem with fraudulent offsets in the industry. “We’re not repackaging existing forest carbon projects and trying to connect the demand side with projects that already exist. Use technology to unlock a new supply of forest carbon offset.”

The first Natural Capital Exchange project was actually launched and funded by Microsoft back in 2019. In it, 20 Western Pennsylvania land owners originated forest carbon credits through the program, showing that the offsets could work for landowners with 40 acres, or, as the company said, 40,000.

Landowners involved in SilviaTerra’s pilot carbon offset program paid for by Microsoft. Image Credit: SilviaTerra

“We’re just trying to get inside every landowners annual economic planning cycle,” said Nova. “There’s a whole field of timber economics… and we’re helping answer the question of given the price of timber, given the price of carbon does it make sense to reduce your planned timber harvests?”

Ultimately, the two founders believe that they’ve found a way to pay for the total land value through the creation of data around the potential carbon offset value of these forests.

It’s more than just carbon markets, as well. The tools that SilviaTerra have created can be used for wildfire mitigation as well. “We’re at the right place at the right time with the right data and the right tools,” said Nova. “It’s about connecting that data to the decision and the economics of all this.”

The launch of the SilviaTerra exchange gives large buyers a vetted source to offset carbon. In some ways it’s an enterprise corollary to the work being done by startups like Wren, another Union Square Ventures investment, that focuses on offsetting the carbon footprint of everyday consumers. It’s also a competitor to companies like Pachama, which are trying to provide similar forest offsets at scale, or 3Degrees Inc. or South Pole.

Under a Biden administration there’s even more of an opportunity for these offset companies, the founders said, given discussions underway to establish a Carbon Bank. Established through the existing Commodity Credit Corp. run by the Department of Agriculture, the Carbon Bank would pay farmers and landowners across the U.S. for forestry and agricultural carbon offset projects.

“Everybody knows that there’s more value in these systems than just the product that we harvest off of it,” said Parisa. “Until we put those benefits in the same footing as the things we cut off and send to market…. As the value of these things goes up… absolutely it is going to influence these decisions and it is a cash crop… It’s a money pump from coastal America into middle America to create these things that they need.”

Powered by WPeMatico

During the days when Snapchat’s popularity was booming, investors thought the company would become the anchor for a new Los Angeles technology scene.

Snapchat, they hoped, would spin-off entrepreneurs and angel investors who would reinvest in the local ecosystem and create new companies that would in turn foster more wealth, establishing LA as a hub for tech talent and venture dollars on par with New York and Boston.

In the ensuing years, Los Angeles and its entrepreneurial talent pool has captured more attention from local and national investors, but it’s not Snap that’s been the source for the next generation of local founders. Instead, several former SpaceX employees have launched a raft of new companies, capturing the imagination and dollars of some of the biggest names in venture capital.

“There was a buzz, but it doesn’t quite have the depth of bench of people that investors wanted it to become,” says one longtime VC based in the City of Angels. “It was a company in LA more than it was an LA company.”

Perhaps the most successful SpaceX offshoot is Relativity Space, founded by Jordan Noone and Tim Ellis. Since Noone, a former SpaceX engineer, and Ellis, a former Blue Origin engineer, founded their company, the business has been (forgive the expression) a rocket ship. Over the past four years, Relativity href=”https://techcrunch.com/2019/10/01/relativity-a-new-star-in-the-space-race-raises-160-million-for-its-3-d-printed-rockets/”> has raised $185.7 million, received special dispensations from NASA to test its rockets at a facility in Alabama, will launch vehicles from Cape Canaveral and has signed up an early customer in Momentus, which provides satellite tug services in orbit.

Powered by WPeMatico

While most of the world agrees that carbon dioxide emissions from human activity are creating a climate crisis, there’s little consensus regarding how to address it.

One of the solutions that’s both the most obvious and, seemingly, the most difficult for the international community to agree on is establishing a market that would put a price on carbon emissions. Making the cost of emissions palpable for industries would encourage companies to curb their polluting activities or pay to offset them.

The holy grail of a global carbon market — or a collection of regional ones — has been on the agenda for climate activists and regulators since the Kyoto Protocols were ratified in 1997, but enacting the policy has proven elusive.

Now, as the results of climate inaction become more apparent, there appears to be some movement on the regulatory front and concurrent activity from early-stage technology investors to make carbon offsets more of a reality.

It’s still early days, but startups like Project Wren, Pachama and Cloverly prove that investors and utilities are willing to take a flyer on companies that are trying to enable carbon offsets for consumers and corporations alike.

These small bets for investors are complemented by the potential for outsized returns given the size and scope that’s possible should these markets actually develop.

After years of languishing in relative obscurity, global carbon markets rebounded with vigor in 2017 and into 2018, according to data from the World Bank.

Countries raised about $44 billion in revenues from carbon pricing in 2018, an increase of $11 billion, with more than half coming from carbon taxes. In 2017, the $33 billion raised by governments from carbon pricing was an increase of 50% over 2016 numbers.

However large that number may seem, it’s dwarfed by the figure required to make any real changes in industry emissions, according to the World Bank. The current pricing schemes that exist cover a small percentage of global emissions at a cost that’s consistent with achieving the goals of the Paris Agreement, the latest international treaty around climate change and greenhouse gas emissions. Prices need to rise to between $40 per ton of carbon dioxide and $80 per ton by 2020 and between $50 per ton and $100 per ton by 2030.

Powered by WPeMatico

Eleven million women in the U.S. live more than an hour from an abortion clinic, a number expected to increase as facilities close up shop following new restrictions on women’s healthcare in several states.

Planned Parenthood and other leading nonprofits continue to put up a good fight while private “mission-driven” companies in the burgeoning women’s health tech sector are all talk and little action. But a new effort from The Pill Club, an Alphabet-backed birth control and prescription delivery startup, may lead to change in the nascent sector.

The Pill Club has partnered with Power To Decide, a nonprofit campaign to prevent unplanned pregnancies, to dole out free emergency contraception to women in need. Together they’ll distribute 5,000 units of a generic form of Plan B, a pill taken after sex to stop a pregnancy before it starts. For the next three months The Pill Club will also match all donations up to $10,000 made to Power To Decide’s Contraceptive Access Fund, which helps low-income women access contraception. Anyone can sign up now to receive free units.

The Pill Club’s decision to share resources with a nonprofit comes as several states this year have imposed new laws restricting or outlawing abortion procedures. Alabama, for example, earlier this year passed a Senate bill banning abortion in the state. Arkansas, Indiana, Kentucky and others have also OK’d new restrictions on abortion.

This is The Pill Club’s first effort to donate emergency contraception to populations in need, as well as its first partnership with a not-for-profit entity. Co-founder and chief executive officer Nick Chang says the startup thought long and hard about how it could be most helpful to women in this political climate.

“We thought, what can we do to support women in these states in ways that other companies may not be able to?,” Chang tells TechCrunch. “This is the moment where private companies can really go out and benefit women in ways that may not be supported in other avenues. Since we have the means and ability to do it in ways that are more convenient and private, it’s our opportunity to drive access and support.”

Founded in 2014 and backed with more than $60 million in venture capital funding, one might argue The Pill Club should have forged partnerships like this from the get-go. Curious what efforts other well-funded birth control startups were making to support women in 2019, especially women in contraceptive deserts who are likely unfamiliar with the new line of consumer birth control brands, I reached out to The Pill Club’s competitors Nurx, a fellow birth control delivery company, and Hers, a line of women’s healthcare products owned by the billion-dollar startup Hims.

Both companies emphasized the fact that many of their customers live in Southern states, or the region most impacted by new limitations to abortion care, but didn’t mention any new efforts to increase access, like partnerships with nonprofits or donations. Hers provided this quote from the company’s co-founder Hilary Coles, which didn’t answer my question but did make clear the company is thinking about serving contraceptive deserts:

“At Hers, our mission is to provide women with more convenient and affordable access to the healthcare system,” Hers co-founders Hilary Coles said in a statement. “Approximately 3.5 million patients go without care because they cannot access transportation to their providers and 19.5 million women have reported not having access to a clinic that provides birth control specifically. That’s simply unacceptable. Closing the gaps caused by geographic barriers between patients and their doctors was one of the primary challenges we set out to address when founding Hers. We’re proud to be a resource for women nationwide, including those who live in contraceptive deserts who may not otherwise have access to the care they need. It’s crucial to Hers to be part of the solution in alleviating the pain points women experience within the healthcare system.”

It’s not the responsibility of these companies to improve the political landscape of the U.S., but with $340 million in private capital shared between them, the trio does have a unique opportunity to innovate, share, collaborate and influence. After all, that’s what’s so great about healthtech; it brings new, innovative solutions to an industry characterized by antiquated systems and slow movers. For once, Silicon Valley’s “move fast and break things” mantra may be appropriately applied to a facet of healthcare. Women need sustained access to contraception and abortion care. Fast.

“This is the time when private companies can step in,” Chang concluded. “We can come in and help out and it’s our responsibility to do that.”

Powered by WPeMatico

The American South may not be the first region that comes to mind when you hear the phrase “hotbed of tech entrepreneurship,” but, slightly misguided perceptions aside, it’s home to a diverse and growing collection of startups.

Here, we’re going to take a deep dive into the startup funding data for the region.

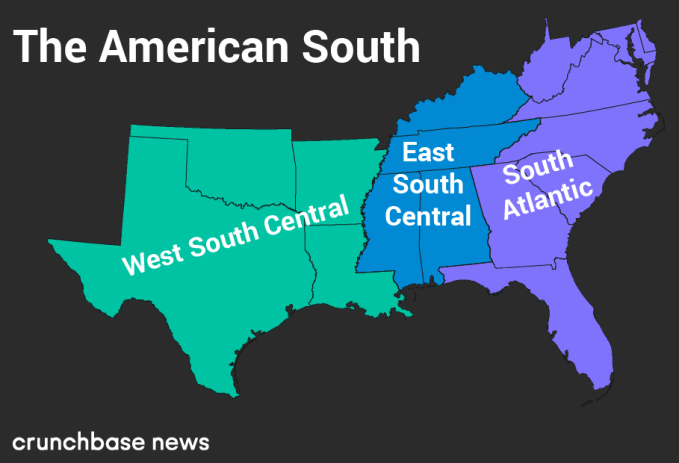

Just like it’s a common pastime for many city dwellers to argue about the precise boundaries of neighborhoods, there’s often some disagreement about the exact contours of the U.S.’s various regions. To quash rabble-rousing from the get-go, we’re using the U.S. Census Bureau’s definition of “the South” on its official map of the United States. Below, we display a map of the states we’re going to look at today.

Much like barbecue, the South is not a monolithic concept. So to incorporate some regional flavor into the following analysis, we’re also going to use the same regional divisions that the U.S. Census Bureau uses.

By doing this, we’ll be able to get a better idea of the relative contribution states from each sub-region make to startup activity in the South overall.

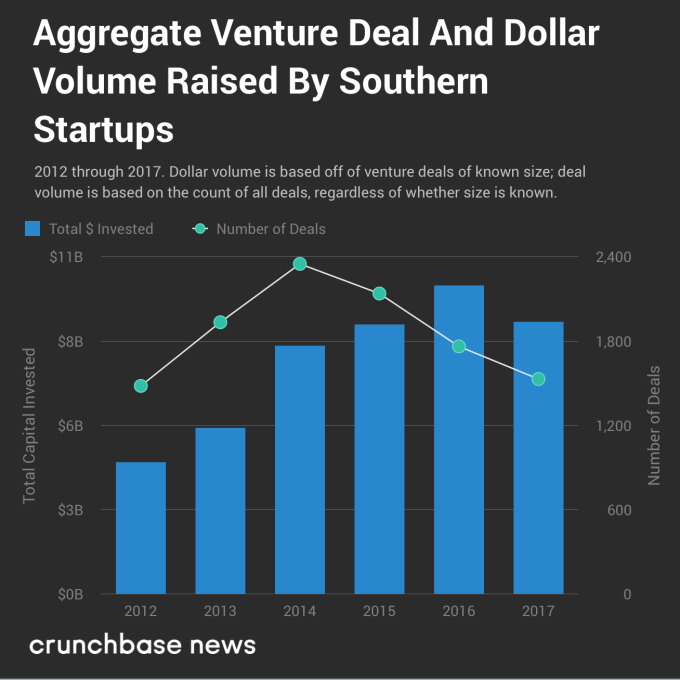

As is the case with most of the country, the South appears to be experiencing a shift in startup funding as we move toward the latter half of a bull run in entrepreneurial activity. The chart below shows a divergence in overall deal and dollar volume over time.

Much like in the rest of the U.S., reported deal and dollar volume are heading in different directions. Part of this may be due to reporting delays — it can sometimes take a few years for seed and early-stage rounds to get added to databases like Crunchbase’s . Nonetheless, there is a slow and generally upward creep in round sizes at most stages of funding. And that’s not just a Southern thing; it’s a country-wide trend.

Let’s disaggregate these figures a bit. We’ll start with deal counts and move on to dollar volume from there.

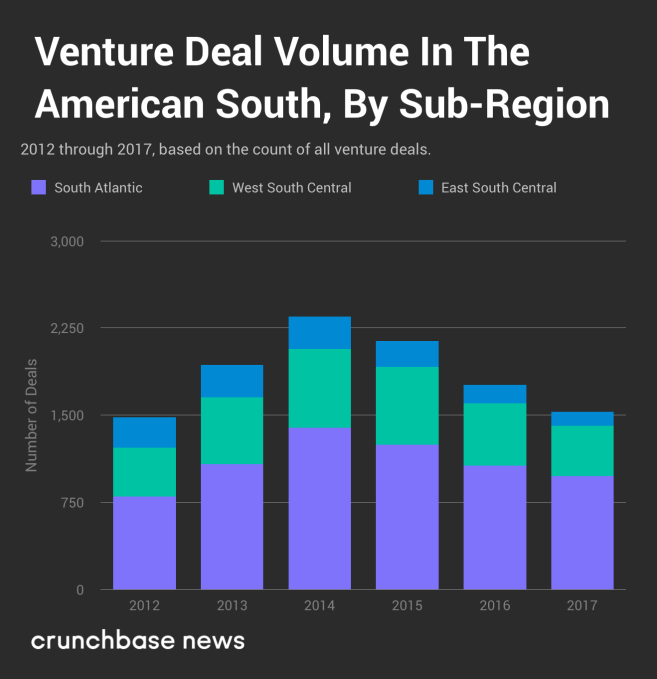

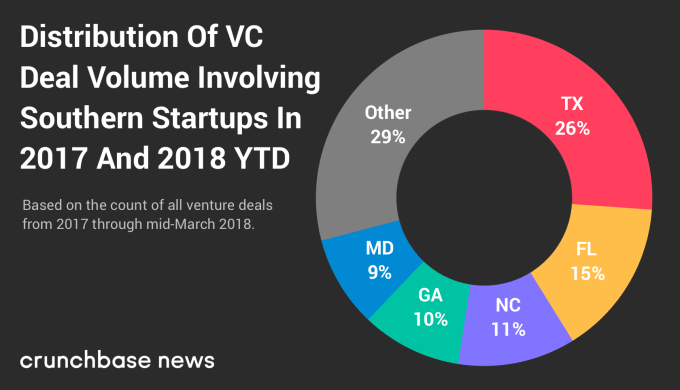

In the chart below, you’ll see venture deal volume broken out by sub-region.

Over the past several years, reported venture deal volume has been on the downswing. From a local maximum in 2014 through the end of 2017, it’s down almost 35 percent overall. But that’s not the whole picture. The relative share of deal volume has changed, as well.

Although it’s not immediately clear just by looking at the chart above, startups in the South Atlantic sub-region have accounted for an increasingly large share of the funding rounds. For example, in 2012, South Atlantic startups attracted 54 percent of the deal volume. In 2017, that grows to 64 percent. Startups in the West South Central sub-region have pretty consistently pulled in between 28 and 30 percent of the deals, so where’s the loss coming from? Startups headquartered in Kentucky, Tennessee, Mississippi and Alabama pulled in just 8 percent of deals in 2017, compared to 18 percent in 2012.

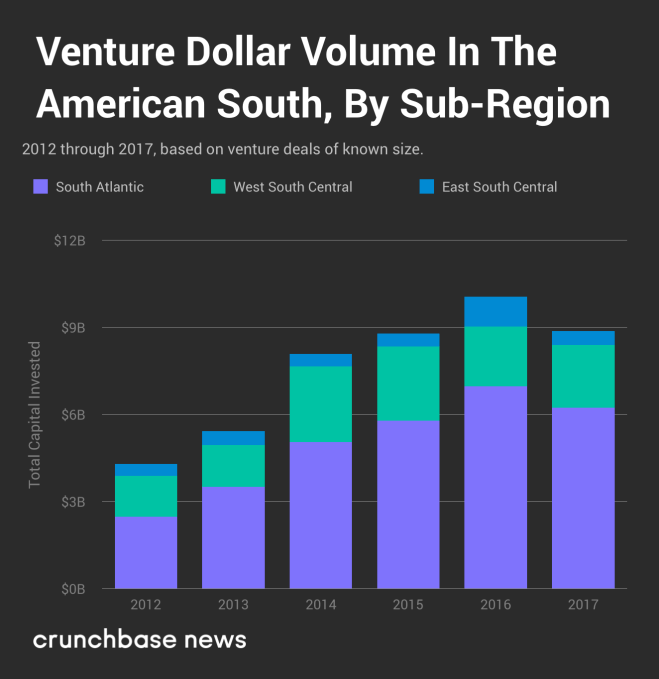

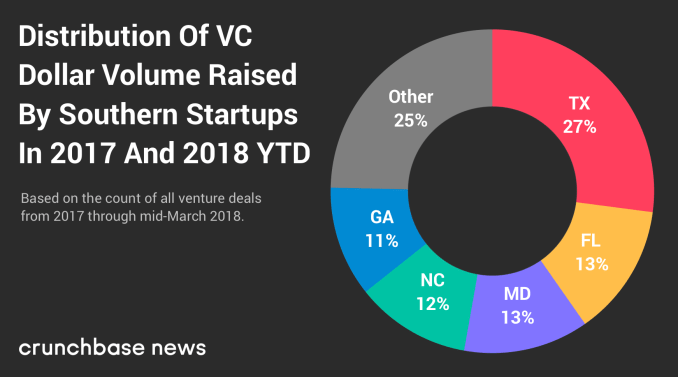

It’s a similar story with dollar volume.

In general, dollar volume follows the same pattern, albeit with a bit more variability. Regardless, startups in the South Atlantic sub-region are hoovering up an ever-larger share of venture dollars, and there’s little to indicate that trend will reverse itself any time soon.

Let’s see which states accounted for most of the deal volume. The chart below shows the geographic distribution of deal-making activity by startups in each Southern state from the beginning of 2017 through time of writing. It should come as no surprise that much of the activity is concentrated in states with higher populations.

And here’s the distribution of dollar volume among southern states.

Despite some variation in which states are at the top of the ranks, the share of deal and dollar volume raised by startups in the top three states is remarkably similar, coming in at between 52 and 53 percent for both metrics.

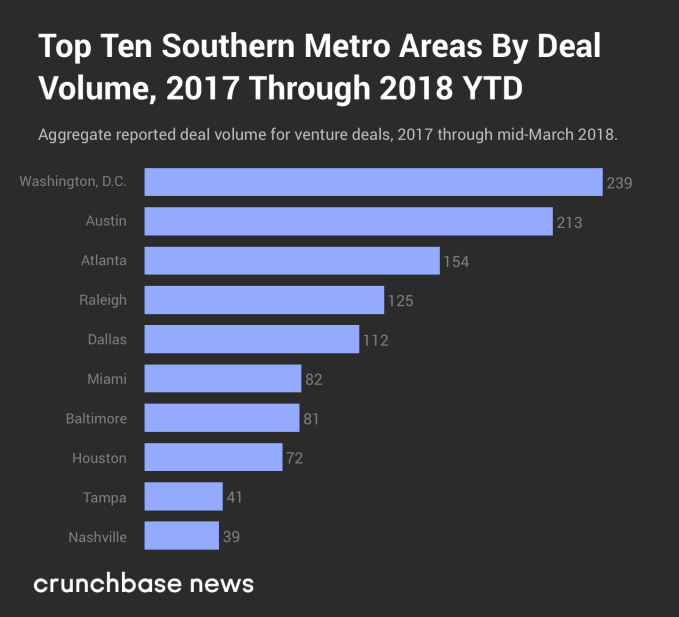

We started by looking at the South as a whole and then drilled into its sub regions and states. But there’s one layer deeper we can go here, and that’s to rank the top startup cities in the South.

In the interest of keeping our rankings fresh and timely, we’re covering activity from the past 15 months or so, from the start of 2017 through mid-March 2018. But before highlighting some of the more notable hubs, let’s take a look at the numbers.

In the chart below, you’ll find the top 10 metropolitan areas where Southern startups closed the most funding rounds.

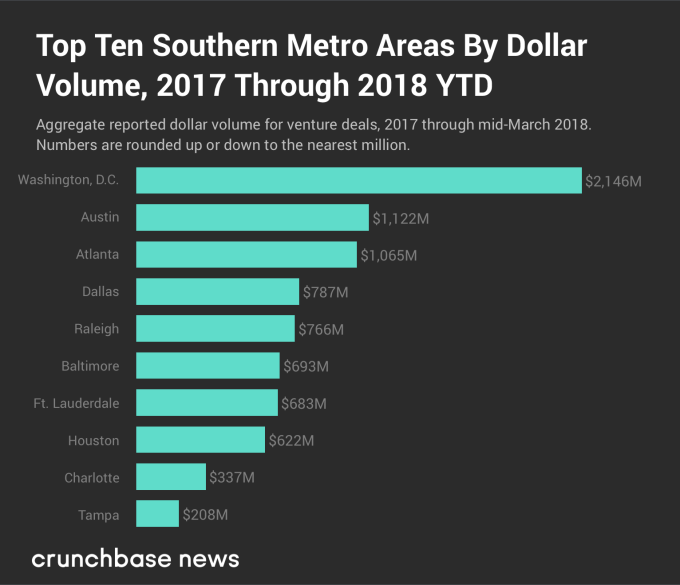

The chart below shows reported dollar volume over the same period of time.

Much like we saw at the state level, the top five startup cities — ranked by both deal and dollar volume — are the same, although there’s some variation between where each one ranks. In order, the D.C., Austin and Atlanta metro areas rank in the top three for each metric, while Dallas and Raleigh, NC switch off between fourth and fifth place.

To be frank, Washington, D.C.’s top-shelf ranking was a bit of a surprise. It may be the fact that Austin, TX plays host to South By Southwest, a somewhat more relaxed culture and/or a preponderance of excellent breakfast taco and barbecue joints, but to many — ourselves included — the city feels like it would have a more active startup scene than the nation’s capital. But that’s not exactly the case. The D.C. metro area had more venture deal and dollar volume than Austin for seven out of the last 10 years, and startups based in the nation’s capital have raised more than twice as much money so far in 2018.

D.C.-area startups have recently raised some notable rounds. Just a couple of weeks prior to the time of writing, Viela Bio raised $250 million in a Series A round (in late February 2018) to continue funding research and testing of its treatments for severe inflammation and autoimmune diseases. And on the later-stage end of things, education technology company Everfi raised $190 million in a Series D round that had participation from Amazon founder and CEO Jeff Bezos, former Alphabet executive Eric Schmidt and Medium CEO Ev Williams. Other D.C. companies, including Mapbox, Upside.com, Afiniti and ThreatQuotient, have all raised late-stage rounds within the past 15 months.

Startup ecosystems in Southern cities may pale in comparison to places like New York and San Francisco, but it wouldn’t be wise to discount the region entirely. A large number of interesting companies call the lower half of the Lower 48 home, and as the cost of living continues to rise on the east and west coasts, don’t be surprised if many current and would-be founders opt to stay down home in the South.

Powered by WPeMatico