Airbnb

Auto Added by WPeMatico

Auto Added by WPeMatico

The WSJ is reporting that Airbnb is expected to price its IPO at either $67 or $68 per share. The American hospitality unicorn raised its IPO price target earlier this week, from $44 to $50 to $56 to $60.

While we’re still waiting for official pricing, Airbnb is worth $41 billion at its IPO price, using the upper pricing estimate and the company’s share count of 602,448,251 from its most recent S-1/A filing. That figure rises sharply if we included more than 50 million shares that could be added to the mix upon the exercise of vested employee options. The company’s fully diluted valuation at its IPO price was calculated to be $47 billion.

Axios reports that Airbnb raised $3.5 billion at its fully diluted valuation.

Regardless of how you prefer to value the company, its worth has risen sharply from an early pandemic nadir of $18 billion. After COVID-19 ravaged the company’s business, it laid off staff and took on external capital.

Since the end of Q1 and the first months of Q2, Airbnb has recovered, allowing it to file to go public and earn its highest valuation to date.

The company’s pricing comes after both DoorDash and C3.ai each priced above their own raised ranges, and saw their shares skyrocket in the first day’s trading. Some exuberance was therefore not unexpected.

Airbnb starts trading tomorrow morning. More then.

Powered by WPeMatico

It’s a special day; we’re hosting the year’s final episode of Extra Crunch Live with General Catalyst’s Peter Boyce and Katherine Boyle at 4 p.m. EST/1 p.m. PST.

Extra Crunch members can join the live conversation (details below) or catch it on demand. Questions from the audience are not just allowed, they’re highly encouraged, so if you’re not yet an Extra Crunch member, sign up here and join the fun!

General Catalyst is widely recognized as one of the top venture capital firms, with portfolio companies that include Snap, Kayak, Airbnb, Stripe, HubSpot and GitLab.

Boyce has been with General Catalyst since 2013, leading investments in companies like Ro, Macro, towerIQ and Atom. He also supported some big deals, including investments in Giphy, Jet.com and Circle. He also co-founded Rough Draft Ventures, an investment arm of General Catalyst focused on funding first-time CEOs out of university.

Boyle was previously a business reporter at The Washington Post before joining General Catalyst, which gives her a unique perspective on the entrepreneurial landscape. She’s invested in several companies, including AirMap, Origin and Nova Credit and has joined us for previous events to lay out some advice for startups navigating governmental rules.

We’re amped to discuss which opportunities are exciting them these days, how tech, innovation and venture has changed amid the pandemic, what they look for in a pitch, and much, much more.

You really won’t want to miss it.

Oh, and if this is of interest, I highly suggest you check out our library of ECL episodes right here. We’ve spoken to big names like Roelof Botha, Jason Green, Alexa von Tobel, Aileen Lee, Charles Hudson and many others.

Catch the details for today’s call below.

Powered by WPeMatico

When a friend forwarded this tweet from Paul Graham, it hit close to home:

Startups are subject to something like infant mortality: before they’re established, one thing going wrong can kill the company. Hardware companies seem to be subject to infant mortality their whole lives.

I think the reason is that the evolution of the product is so discontinuous. The company has to keep shipping, and customers to keep buying, new products. Which in practice is like relaunching the company each time.

I don’t know if there is an answer to this, but if there were a way for hardware companies to evolve more the way software companies do, they’d be a lot more resilient.

Looking back on our startup journey at Minut, I remember several moments when we could have died. However, surviving several near misses we learned to tackle these challenges and have become more resilient over time. While there will never be one fully exhaustive answer, here are some of the lessons we learned over the years:

While you can sell hardware with a margin and make important early revenue, it’s not a sustainable business model for a company that requires both software and hardware. You can’t cover an indefinite commitment with a finite amount of money.

Many hardware companies don’t consider subscriptions early enough. While it can be hard to command a subscription from the start (if you can, you might have waited too long to launch), it needs to be in the plan from the beginning. Look for markets where paying subscriptions is the norm rather than markets that operate on a one-time sale model.

It’s tempting to set low prices for hardware to attract customers, but in the beginning you should do the opposite. Margins allow for mistakes to be rectified. A missed deadline might mean you have to opt for freight by air rather than boat. You might have to scrap components or buy them expensively in a supply crunch. Surprises are seldom positive, and you don’t want to use your venture capital to pay for them.

Healthy margins can also be used to cover marketing costs while you learn what kind of messaging works and what channels you can sell through. If that wasn’t enough reason, starting with relatively high prices will help you avoid another common mistake, selling too much at launch.

This might seem counterintuitive — why wouldn’t you want great success out of the gate? The reason is that you will inevitably make mistakes with your early launches, and the bigger the launch, the bigger the blow. There are plenty of companies who achieved amazing crowdfunding success and then failed to deliver even the first units. Startups tend to chase growth at all costs, but for hardware startups in the first few years there is such a thing as too much of a good thing.

Powered by WPeMatico

This morning Airbnb released an S-1/A filing that details its initial IPO price range. The home-sharing unicorn intends to price its shares between $44 and $50 in its debut.

Per the company’s own accounting, it will have 596,399,007 or 601,399,007 shares outstanding, depending on whether its underwriters exercise their option. That gives the company a valuation range of $26.2 billion to $30.1 billion at the extremes.

The company’s simple share count does not include a host of other shares that have vested but not yet been exercised. Including those shares, the company’s fully diluted valuation stretches to $35 billion, by CNBC’s arithmetic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The top end of Airbnb’s simple valuation places it near its Series F valuation set in 2017. Its fully diluted valuation exceeds that $30.5 billion valuation and is far superior to the $18 billion, post-money valuation that it raised at during its troubled period early in the COVID-19 pandemic.

For those investors, Silver Lake and Sixth Street, the company’s initial IPO price range is a win. For the company’s preceding investors, to see the company appear ready to at least match its preceding private valuation is a win as well, given how much damage Airbnb’s business sustained early in the pandemic.

For those investors, Silver Lake and Sixth Street, the company’s initial IPO price range is a win. For the company’s preceding investors, to see the company appear ready to at least match its preceding private valuation is a win as well, given how much damage Airbnb’s business sustained early in the pandemic.

But how do those Airbnb valuation numbers match up against its revenues, and will public market investors value the company based on its current results, or expectations for a return-to-form once a vaccine comes to market? And if so, is Airbnb expensive or not?

Shares of Booking Holdings, which owns travel services like Kayak, Priceline, OpenTable and others, have almost doubled in value since its pandemic lows and is within spitting distance of its all-time highs. This despite its revenues falling 48% in its most recent quarter. There’s optimism in the market that travel companies are on the cusp of a return to form, buoyed — we presume — by good news regarding effective coronavirus vaccines.

My expectation is that Airbnb is enjoying a similar bump, as investors intend to buy its shares not to bask in awe of its Q4 2020 results, but instead to enjoy what happens in the back half of 2021 as vaccines roll out and the travel industry recovers.

But what happens if we stack Airbnb’s revenues against its valuation today?

Powered by WPeMatico

DoorDash, Affirm, Roblox, Airbnb, C3.ai and Wish all filed to go public in recent days, which means some venture capitalists are having the best week of their lives.

Tech companies that go public capture our imagination because they are literal happy endings. An Initial Public Offering is the promised land for startup pilgrims who may wander the desert for years seeking product-market fit. After all, the “I” in “ISO” stands for “incentive.”

A flurry of new S-1s in a single week forced me to rearrange our editorial calendar, but I didn’t mind; our 360-degree coverage let some of the air out of various hype balloons and uncovered several unique angles.

For example: I was familiar with Affirm, the service that lets consumers finance purchases, but I had no idea Peloton accounted for 30% of its total revenue in the last quarter.

“What happens if Peloton puts on the brakes?” I asked Alex Wilhelm as I edited his breakdown of Affirm’s S-1. We decided to use that as the subhead for his analysis.

The stories that follow are an overview of Extra Crunch from the last five days. Full articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Thank you very much for reading Extra Crunch this week; I hope you have a relaxing weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

Gaming company Roblox filed to go public yesterday afternoon, so Alex Wilhelm brought out a scalpel and dissected its S-1. Using his patented mathmagic, he analyzed Roblox’s fundraising history and reported revenue to estimate where its valuation might land.

Noting that “the public markets appear to be even more risk-on than the private world in 2020,” Alex pegged the number at “just a hair under $10 billion.”

HANGZHOU, CHINA – JULY 31: An employee uses face recognition system on a self-service check-out machine to pay for her meals in a canteen at the headquarters of Alibaba Group on July 31, 2018 in Hangzhou, Zhejiang Province of China. The self-service check-out machine can calculate the price of meals quickly to save employees’ queuing time. (Photo by Visual China Group via Getty Images)

For all the hype about new forms of payment, the way I transact hasn’t been radically transformed in recent years — even in tech-centric San Francisco.

Sure, I use NFC card readers to tap and pay and tipped a street musician using Venmo last weekend. But my landlord still demands paper checks and there’s a tattered “CASH ONLY” taped to the register at my closest coffee shop.

In China, it’s a different story: Alibaba’s employee cafeteria uses facial recognition and AI to determine which foods a worker has selected and who to charge. Many consumers there use the same app to pay for utility bills, movie tickets and hamburgers.

“Today, nobody except Chinese people outside of China uses Alipay or WeChat Pay to pay for anything,” says finance researcher Martin Chorzempa. “So that’s a big unexplored side that I think is going to come into a lot of geopolitical risks.”

Image Credits: Nigel Sussman (opens in a new window)

Consumer lending service Affirm filed to go public on Wednesday evening, so Alex used Thursday’s column to unpack the company’s financials.

After reviewing Affirm’s profitability, revenue and the impact of COVID-19 on its bottom line, he asked (and answered) three questions:

Image Credits: XiXinXing (opens in a new window) / Getty Images

“The only thing more rare than a unicorn is an exited unicorn,” observes Managing Editor Danny Crichton, who looked back at Exitpalooza 2020 to answer “a simple question — who made the money?”

Covering each exit from the perspective of founders and investors, Danny makes it clear who’ll take home the largest slice of each pie. TL;DR? “Some really colossal winners among founders, and several venture firms walking home with billions of dollars in capital.

Image Credits: Nigel Sussman (opens in a new window)

The S-1 Airbnb released at the start of the week provided insight into the home-rental platform’s core financials, but it also raised several questions about the company’s health and long-term viability, according to Alex Wilhelm:

Andrew Anagnost, president and CEO, Autodesk.

Earlier this week, Autodesk announced its purchase of Spacemaker, a Norwegian firm that develops AI-supported software for urban development.

TechCrunch reporter Steve O’Hear interviewed Autodesk CEO Andrew Anagnost to learn more about the acquisition and asked why Autodesk paid $240 million for Spacemaker’s 115-person team and IP — especially when there were other startups closer to its Bay Area HQ.

“They’ve built a real, practical, usable application that helps a segment of our population use machine learning to really create better outcomes in a critical area, which is urban redevelopment and development,” said Anagnost.

“So it’s totally aligned with what we’re trying to do.”

Image Credits: Nigel Sussman (opens in a new window)

On Monday, Alex dove into the IPO filing for enterprise artificial intelligence company C3.ai.

After poring over its ownership structure, service offerings and its last two years of revenue, he asks and answers the question: “is the business itself any damn good?”

Image Credits: jayk7 / Getty Images

In his new book, “Subprime Attention Crisis,” writer/researcher Tim Hwang attempts to answer a question I’ve wondered about for years: does advertising actually work?

Managing Editor Danny Crichton interviewed Hwang to learn more about his thesis that there are parallels between today’s ad industry and the subprime mortgage crisis that helped spur the Great Recession.

So, are online ads effective?

“I think the companies are very reticent to give up the data that would allow you to find a really definitive answer to that question,” says Hwang.

Image Credits: Zoom

Even after much of the population has been vaccinated against COVID-19, we will still be using Zoom’s video-conferencing platform in great numbers.

That’s because Zoom isn’t just an app: it’s also a platform play for startups that add functionality using APIs, an SDK or chatbots that behave like smart assistants.

Enterprise reporter Ron Miller spoke to entrepreneurs and investors who are leveraging Zoom’s platform to build new applications with an eye on the future.

“By offering a platform to build applications that take advantage of the meeting software, it’s possible it could be a valuable new ecosystem for startups,” says Ron.

Image Credits: Bryce Durbin

Without an on-campus experience, many students (and their parents) are wondering how much value there is in attending classes via a laptop in a dormitory.

Even worse: Declining enrollment is leading many institutions to eliminate majors and find other ways to cut costs, like furloughing staff and cutting athletic programs.

Edtech solutions could fill the gap, but there’s no real consensus in higher education over which tools work best. Many colleges and universities are using a number of “third-party solutions to keep operations afloat,” reports Natasha Mascarenhas.

“It’s a stress test that could lead to a reckoning among edtech startups.”

3D rendering of TNT dynamite sticks in carton box on blue background. Explosive supplies. Dangerous cargo. Plotting terrorist attack. Image Credits: Gearstd / Getty Images.

I look for guest-written Extra Crunch stories that will help other entrepreneurs be more successful, which is why I routinely turn down submissions that seem overly promotional.

However, Henrik Torstensson (CEO and co-founder of Lifesum) submitted a post about the techniques he’s used to scale his nutrition app over the last three years. “It’s a strategy any startup can use, regardless of size or budget,” he writes.

According to Sensor Tower, Lifesum is growing almost twice as fast as Noon and Weight Watchers, so putting his company at the center of the story made sense.

Image via Getty Images / Alexander Spatari

Every year, we ask TechCrunch reporters, VCs and our Extra Crunch readers to recommend their favorite books.

Have you read a book this year that you want to recommend? Send an email with the title and a brief explanation of why you enjoyed it to bookclub@techcrunch.com.

We’ll compile the suggestions and publish the list as we get closer to the holidays. These books don’t have to be published this calendar year — any book you read this year qualifies.

Please share your submissions by November 30.

Image Credits: Sophie Alcorn

Dear Sophie:

My VC partner and I are working with 50/50 co-founders on their startup — let’s call it “NewCo.” We’re exploring pre-seed terms.

One founder is on a green card and already works there. The other founder is from India and is working on an H-1B at a large tech company.

Can the H-1B co-founder lead this company? What’s the timing to get everything squared away? If we make the investment we want them to hit the ground running.

— Diligent in Daly City

Powered by WPeMatico

The only thing more rare than a unicorn is an exited unicorn.

At TechCrunch, we cover a lot of startup financings, but we rarely get the opportunity to cover exits. This week was an exception though, as it was exitpalooza as Affirm, Roblox, Airbnb and Wish all filed to go public. With DoorDash’s IPO filing last week, this is upwards of $100 billion in potential float heading to the public markets as we make our way to the end of a tumultuous 2020.

All those exits raise a simple question — who made the money? Which VCs got in early on some of the biggest startups of the decade? Who is going to be buying a new yacht for the family for the holidays (or, like, a fancy yurt for when Burning Man restarts)? The good news is that the wealth is being spread around at least a couple of VC firms, although there are definitely a handful of partners who are looking at a very, very nice check in the mail compared to others.

So let’s dive in.

I’ve covered DoorDash’s and Airbnb’s investor returns in-depth, so if you want to know more about those individual returns, feel free to check out those analyses. But let’s take a more panoramic perspective of the returns of these five companies as a whole.

First, let’s take a look at the founders. These are among the very best startups ever built, and therefore, unsurprisingly, the founders all did pretty well for themselves. But there are pretty wide variations that are interesting to note.

First, Airbnb — by far — has the best return profile for its founders. Brian Chesky, Nathan Blecharczyk and Joe Gebbia together own nearly 42% of their company at IPO, and that’s after raising billions in venture capital. The reason for their success is simple: Airbnb may have had some tough early innings when it was just getting started, but once it did, its valuation just skyrocketed. That helped to limit dilution in its earlier growth rounds, and ultimately protected their ownership in the company.

David Baszucki of Roblox and Peter Szulczewski of Wish both did well: they own 12% and about 19% of their companies, respectively. Szulczewski’s co-founder Sheng “Danny” Zhang, who is Wish’s CTO, owns 4.9%. Eric Cassel, the co-founder of Roblox, did not disclose ownership in the company’s S-1 filing, indicating that he doesn’t own greater than 5% (the SEC’s reporting threshold).

DoorDash’s founders own a bit less of their company, mostly owing to the money-gobbling nature of that business and the sheer number of co-founders of the company. CEO Tony Xu owns 5.2% while his two co-founders Andy Fang and Stanley Tang each have 4.7%. A fourth co-founder, Evan Moore, didn’t disclose his share totals in the company’s filing.

Finally, we have Affirm . Affirm didn’t provide total share counts for the company, so it’s hard right now to get a full ownership picture. It’s also particularly hard because Max Levchin, who founded Affirm, was a well-known, multi-time entrepreneur who had a unique shareholder structure from the beginning (many of the venture firms on the cap table actually have equal proportions of common and preferred shares). Levchin has more shares all together than any of his individual VC investors — 27.5 million shares, compared to the second largest investor, Jasmine Ventures (a unit of Singapore’s GIC) at 22 million shares.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

Today we have an Equity Shot for you about Airbnb’s S-1 filing, as it looks to go public before the year is out.

All that, and our trusty other host Danny Crichton was busy filing a post about the winners and losers of the Airbnb IPO. Ownership, you quiet, billionaire beast. There’s more coming from TechCrunch on the company’s IPO, and from the Equity crew on everything else we ferret out on Thursday. Stay tuned!

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Airbnb filed to go public today, bringing the well-known unicorn one step closer to being a public company.

The financial results show a company on the rebound, but smaller than it was. Its more granular financial results also make clear how hard the pandemic was on the travel-reliant unicorn. Regarding Airbnb’s worth, investors will have to balance how they value recovery and recent profits over the company’s disrupted historical growth arc.

The home-sharing startup had a tumultuous year, with the COVID-19 pandemic harming its business in the first and second quarters of the year, and Airbnb later recovering on the strength of more local bookings.

Its filing comes mere days after fellow unicorns DoorDash and C3.ai themselves filed to go public in what could be a rush to the public markets by richly valued startups.

Airbnb’s S-1 filing was expected to come last week, but was delayed due to purported election concerns, a concept that TechCrunch staff did not find entirely convincing.

We’ve scraped together quite a lot about Airbnb’s recent financial performance, but its S-1 is the real treasure trove. What follows is a dive into the company’s high-level numbers. From there, TechCrunch will dig into the company’s financial nuances and ownership stakes.

What we want to know is how the pandemic impacted Airbnb’s business; its year-to-date results, and what we can suss out from its quarterly trends.

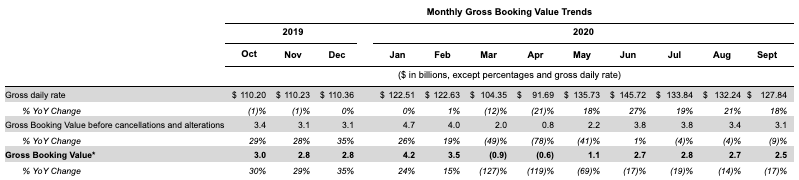

Up top in Airbnb’s S-1 is a chart that shows monthly bookings on its platform. The implication is somewhat simple; namely that Airbnb knows what we want to know and wanted to share. Here are those numbers:

Image Credits: Airbnb S-1

As expected, Airbnb took a huge hit in March. But by May things were back to year-over-year growth, where they stayed.

Now, the company has seen precious little bookings growth since June — indeed it has seen bookings fall in the months since. And, worse, the company’s gross bookings after removing cancellations are down on a year-over-year basis. (Update: We misread this table at first, and have updated our notes on it.)

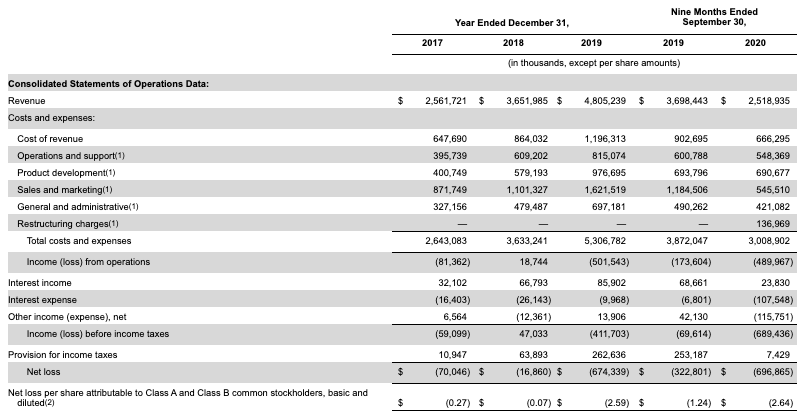

So, what does all of that look like in more traditional accounting figures? Here’s Airbnb’s reported income statement:

Image Credits: Airbnb S-1

As expected, Airbnb’s year has not been tremendous. Indeed, the company is on track to match its 2018 size, if we have our math correct.

What changed from the first three quarters of 2019 to the first three quarters of 2020? The biggest thing, apart from expected lower revenue costs — less revenue costs less — is the huge decline in sales and marketing spend at the company. Airbnb slashed S&M outlays from $1.18 billion in the first three quarters of 2019 to just $545.5 million in the same period of 2020.

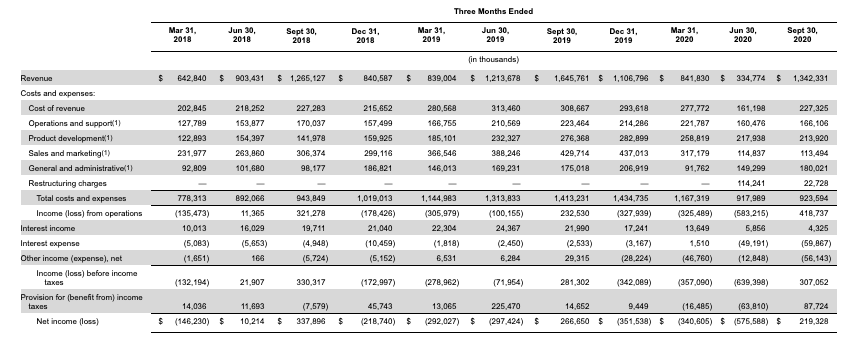

So, where will Airbnb wind up in 2020 once it’s all done? We’ll need to peek at its quarterly results for that. Here they are:

Image Credits: Airbnb S-1

Airbnb’s growth continues in year-over-year terms right until the March 31, 2020 quarter, when it was effectively flat compared to Q1 2019. Or, the company would have grown sans COVID-19. In the June 30, 2020 quarter we see the real damage, with Airbnb’s revenue falling from $1.2 billion in the year-ago quarter to just $334.8 million. That’s a shocking decline.

But, looking ahead to Q3 2020 we see a large return to form. Yes, Airbnb’s third quarter was smaller than its Q3 2019, with $1.34 billion in top line instead of $1.65 billion in 2019, but the company effectively quadrupled from its preceding quarter. If the company manages another Q3 worth of revenue in Q4, it would be larger than it was in 2018 by a few hundred million.

Critically, Airbnb managed to swing from a number of unprofitable quarters to a profit in Q3, akin to its 2019 Q3 when it was also in the black. Of course, Airbnb’s $219.3 million in GAAP net income during the third quarter pales compared to its losses tallied earlier in the year. The company will not break even in 2020.

Airbnb also reported adjusted profit metrics. Its adjusted EBITDA results are based on the following definition:

Adjusted EBITDA is defined as net income or loss adjusted for (i) provision for income taxes; (ii) interest income, interest expense, and other income (expense), net; (iii) depreciation and amortization; (iv) stock-based compensation expense; (v) net changes to the reserves for lodging taxes for which we may be held jointly liable with hosts for collecting and remitting such taxes; and (vi) restructuring charges.

The decision to remove restructuring costs raised eyebrows, with Amy Cheetham, an investor at Costanoa Ventures, saying that “it feels like leaving out restructuring costs is a little aggressive?” We agree, as it gives the company too much flexibility to count the good in its results, like lower operating costs, while discounting what it took to get those results, like restructuring its business operations.

That’s having your cake and eating it as well and not counting the calories.

Still, who are we to withhold numbers from you? Here is the very adjusted EBITDA that Airbnb claims:

Image Credits: Airbnb S-1

The numbers are still not good even after ripping out so very any costs. Worse, perhaps is the company’s cash burn in the year. That deficit helps explain why Airbnb took on more capital when it did earlier this year.

It’s hard to put a firm grade on this S-1. It contains what we expected, but how investors weigh the company’s year-over-year revenue declines in Q3 2020 against its rapid comeback from Q2 2020 should help decide its eventual value. On the whole Airbnb has managed something incredibly impressive — bouncing back from so low a low.

But, now that it’s going public we can’t merely say “good job”; it wants to price itself well and trade strongly. So, all eyes on its first IPO range as that should tell us what investors just might be willing to pay for the famous company’s equity.

Powered by WPeMatico

During yesterday’s tense voting and this morning, shares of American-listed technology companies are shooting higher.

The tech-heavy Nasdaq composite is up around 3.35% this morning, more than double what the broad S&P 500 index is currently managing. SaaS and cloud stocks kicked off the day up a staggering 4.98%, a sharp rally in the value of smaller, more growth-oriented technology companies.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

For technology companies on the wings of the IPO market, it’s great news.

In 2020 it can be easy to forget, but tech stocks do not have to rise. They merely have in recent months, perhaps warming the waters for more technology debuts as the fourth quarter races toward its midpoint. The Exchange has heard whispers from several folks that the late-November/early-December period could be active for new filings, bringing rising stocks and pent-up demand together for a possible IPO run.

We’ll see. Today’s rally — and ballot measure results in California — could be the push companies like Airbnb and DoorDash needed to stop faffing around with private filings.

We’ll see. Today’s rally — and ballot measure results in California — could be the push companies like Airbnb and DoorDash needed to stop faffing around with private filings.

In pedestrian terms, the getting is good right now for public tech companies, so if you are going to go public, go get got while the getting stays good.

Today, let’s examine recent market gains for tech stocks and remind ourselves who is expected to go public next. Then, of course, chat about all the unicorns on the unofficial IPO list who could find a greased path ahead of them toward a flotation.

Big tech stocks are gaining, small stocks are up and software companies are hot. The NASDAQ is now less than 5% away from its all-time highs, and the Bessemer Cloud Index is now just 9% down from its own, a rebound from its prior status in correction territory. (A correction occurs when an index falls 10% or more from highs.)

So, who does the rally help? Let’s rock through a list:

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest big news, chats about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here — and don’t forget to check out last Friday’s episode that includes some high-quality Quibi jokes, if I recall correctly.

Shout-out to Lewis Hamilton and that G2 series. OK, chat Thursday!

Equity drops every Monday at 7:00 a.m. PT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico