Aileen Lee

Auto Added by WPeMatico

Auto Added by WPeMatico

Earlier this week, we kicked off our Extra Crunch Live series with an interesting chat with Cowboy’s Aileen Lee and Ted Wang. Today, we will be back at 3 p.m. PST/6 p.m. EST/10 p.m. GMT with a new guest: Charles Hudson, the general partner of Precursor Ventures.

Extra Crunch members will find an AddEvent link below to drop the details directly into their calendar and folks who want to participate directly can hit up the Zoom link (also below). We’ll ask as many audience questions as we can, so please make them sharp — no pitches, please.

Charles Hudson founded Precursor Ventures to invest in pre-seed and seed-stage companies. Earlier this year, the firm filed paperwork to put together a $40 million third fund after previously raising two main funds and one $10 million “opportunity” fund.

As we await hard and accurate numbers on how COVID-19 is impacting fundraising, we’ll ask Hudson to walk us through the changes he has seen and will cover some basics: The best way to pitch him, what his to-do list looks like these days and if the pandemic has made Precursor newly bullish or bearish on certain sectors.

Then, we’ll get much nerdier: Will we see the number of party rounds fall further now that it’s harder to gather investors in real life? Do you think we’ll see pre-seed raises ask for more ownership terms? And what is the latest with the wacky world of early-stage valuations?

There’s a lot to talk about. And we haven’t even mentioned YC’s pro rata change yet.

After Hudson, we have a stacked lineup of Extra Crunch live guests, including Mitch and Freada Kapor, Mark Cuban, Roelof Botha and Kirsten Green, with more to be announced soon.

You can find information below with details for joining today’s discussion, as well as an AddEvent link to put the details directly onto your calendar.

Sign up for Extra Crunch to get access to all these episodes where you can view the talks live, participate in the Q&A with industry leaders and watch later on-demand if you can’t make the live timing. You can also see the chat via YouTube below. Talk soon!

Powered by WPeMatico

The tech industry (and the world at large) is not experiencing temporary anxiety — the uncertainty we’re all coping with is the new normal.

Sudden shifts in behavior have made some startups targeting slow-moving, old-school industries more relevant than they could have imagined, such as those in telehealth, distance learning and remote work. Most, however are seeing massive decreases in revenue, forcing them to cut costs and even lay off teams to slash burn rates. Other startups simply won’t be here in three to six months.

Cowboy Ventures founder and managing partner Aileen Lee, who coined the term “unicorn,” says tech companies going through scenario planning need to begin thinking long-term.

“We’ve spent the last month scenario planning with our portfolio companies, and in most cases, we’ll have conversations about what these scenarios can include,” said Lee. “And when we look at the planning around those scenarios, they often don’t feel conservative enough. Most entrepreneurs are optimists, and we are, too! But it seems safer to have more conservative plans [and start expecting] that this is going to impact us for longer and be worse than we expected.”

Lee and Cowboy Ventures partner Ted Wang joined TechCrunch on Tuesday for our first episode of Extra Crunch Live, a virtual speaker series for Extra Crunch members. In a live Q&A that included questions from myself and the Extra Crunch audience, Wang and Lee covered a wide range of topics, including PPP loans, advice for business leaders around layoffs, the right time to seek funding and the right firms from which to seek that funding, how to pitch during a downturn and which sectors in particular Cowboy is interested in financing right now.

You can check out the best insights from the call, or catch up on the full conversation via the YouTube embed below.

We have several outstanding guests, including Charles Hudson, Mitch and Freada Kapor, Mark Cuban, Roelof Botha, Hunter Walk and Kirsten Green, joining us on Extra Crunch Live over the next few weeks. Sign up for Extra Crunch to get access to all of them.

Powered by WPeMatico

Early-stage founders: Don’t miss your chance to follow in the footsteps of tech giants. We know COVID-19 has created challenges for startup founders, but fear not. Disrupt SF is still proceeding as scheduled, with a Disrupt Digital Pass Virtual option. Launch your startup in the world’s most famous pitch competition, Startup Battlefield. The smackdown goes down live on the Main Stage at Disrupt San Francisco 2020 on September 14-16. Want a shot at $100,000 and the Disrupt Cup? Fill out your application to compete right here.

Companies such as Fitbit, Cloudflare, Mint.com, Dropbox, Vurb, Yammer and Getaround — to name but a few — trace their origins to the Battlefield competition. The Startup Battlefield Alumni Community — 902 companies strong and counting — has collectively raised $9 billion and produced more than 115 successful exits (IPOs or acquisitions). That’s some impressive company to keep. Why not join their ranks?

Here’s how Startup Battlefield works. First, you apply. (Pro tip: Applying and competing in the Battlefield is free and TechCrunch does not take any equity). Next, TechCrunch’s Battlefield-savvy editorial team pours over every application looking for approximately 20 startups to pitch on the Main Stage.

The TechCrunch team will put all participants through rigorous, weeks-long training to hone pitches, business models, presentation skills and any other startup issues that require tightening. You’ll be in fighting trim and ready to step out onto the Main Stage.

Teams have just six minutes to pitch and present a live demo to a panel of expert judges. After each pitch, the judges (we’re talking folks like Cyan Banister, Kirsten Green, Aileen Lee, Alfred Lin and Roelof Botha) will put each team through a Q&A. No flop-sweat here, thanks to all those weeks of pitch coaching.

The judges will select anywhere from four to six teams to advance to the finals. And that means another pitch and Q&A in front of a fresh set of judges. The winning team takes home $100,000, the coveted Disrupt Cup and they bask in a spotlight of media and investor attention. Startup Battlefield can be a life-changing experience for all competitors — not just the ultimate winner.

The action takes place in front of an enthusiastic audience of thousands. Plus, we live-stream the entire event on TechCrunch.com, once you sign up for the digital pass. If all that’s not enough, consider this. Startup Battlefield competitors receive a VIP Disrupt experience.

You’ll have access to private VIP events like the Startup Battlefield Reception, and each team receives four complimentary event tickets. You get to exhibit at the show for all three days, and you’ll have access to CrunchMatch, TC’s investor-founder networking platform. And you also get a complimentary ticket to all future TC events and free subscriptions to Extra Crunch.

Whew. That’s a whole lot of opportunity and exposure. So, what are you waiting for? Disrupt San Francisco 2020 takes place on September 14-16. Apply to compete in Startup Battlefield for a shot at launching your dream to the world.

TechCrunch is mindful of the COVID-19 issue and its impact on live events. You can follow our updates here.

Is your company interested in sponsoring or exhibiting at Disrupt San Francisco 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a newsletter published every Saturday that dives into the week’s noteworthy venture capital deals, funds and trends. Before I dive into this week’s topic, let’s catch up a bit. Last week, I wrote about the sudden uptick in beverage startup rounds. Before that, I noted an alternative to venture capital fundraising called revenue-based financing. Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets.

Here’s what I’ve been thinking about this week: Unicorn scarcity, or lack thereof. I’ve written about this concept before, as has my Equity co-host, Crunchbase News editor-in-chief Alex Wilhelm. I apologize if the two of us are broken records, but I think we’re equally perplexed by the pace at which companies are garnering $1 billion valuations.

Here’s the latest data, according to Crunchbase: “2018 outstripped all previous years in terms of the number of unicorns created and venture dollars invested. Indeed, 151 new unicorns joined the list in 2018 (compared to 96 in 2017), and investors poured more than $135 billion into those companies, a 52% increase year-over-year and the biggest sum invested in unicorns in any one year since unicorns became a thing.”

2019 has already coined 42 new unicorns, like Glossier, Calm and Hims, a number that grows each and every week. For context, a total of 19 companies joined the unicorn club in 2013 when Aileen Lee, an established investor, coined the term. Today, there are some 450 companies around the globe that qualify as unicorns, representing a cumulative valuation of $1.6 trillion.

We’ve clung to this fantastical terminology for so many years because it helps us classify startups, singling out those that boast valuations so high, they’ve gained entry to a special, elite club. In 2019, however, $100 million-plus rounds are the norm and billion-dollar-plus funds are standard. Unicorns aren’t rare anymore; it’s time to rethink the unicorn framework.

Petition to stop using the term “unicorn” unless the company is valued at more than $1 billion *and* profitable.

— Kate Clark (@KateClarkTweets) May 22, 2019

Last week, I suggested we only refer to profitable companies with a valuation larger than $1 billion as unicorns. Understandably, not everyone was too keen on that idea. Why? Because startups in different sectors face barriers of varying proportions. A SaaS company, for example, is likely to achieve profitability a lot quicker than a moonshot bet on autonomous vehicles or virtual reality. Refusing startups that aren’t yet profitable access to the unicorn club would unfairly favor certain industries.

So what can we do? Perhaps we increase the valuation minimum necessary to be called a unicorn to $10 billion? Initialized Capital’s Garry Tan’s idea was to require a startup have 50% annual growth to be considered a unicorn, though that would be near-impossible to get them to disclose…

While I’m here, let me share a few of the other eclectic responses I received following the above tweet. Joseph Flaherty said we should call profitable billion-dollar companies Pegasus “since [they’ve] taken flight.” Reagan Pollack thinks profitable startups oughta be referred to as leprechauns. Hmmmm.

The suggestions didn’t stop there. Though I’m not so sure adopting monikers like Pegasus and leprechaun will really solve the unicorn overpopulation problem. Let me know what you think. Onto other news.

Image by Rafael Henrique/SOPA Images/LightRocket via Getty Images

CrowdStrike has set its IPO terms. The company has inked plans to sell 18 million shares at between $19 and $23 apiece. At a midpoint price, CrowdStrike will raise $378 million at a valuation north of $4 billion.

Slack inches closer to direct listing. The company released updated first-quarter financials on Friday, posting revenues of $134.8 million on losses of $31.8 million. That represents a 67% increase in revenues from the same period last year when the company lost $24.8 million on $80.9 million in revenue.

Online lender SoFi has quietly raised $500M led by Qatar

Groupon co-founder Eric Lefkofsky just-raised another $200M for his new company Tempus

Less than 1 year after launching, Brex eyes $2B valuation

Password manager Dashlane raises $110M Series D

Enterprise cybersecurity startup BlueVoyant raises $82.5M at a $430M valuation

Talkspace picks up $50M Series D

TaniGroup raises $10M to help Indonesia’s farmers grow

Stripe and Precursor lead $4.5M seed into media CRM startup Pico

Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, has closed on another $180 million to invest in early-stage consumer startups. The capital represents the firm’s seventh fundraise and largest since 2000. To keep the fund from reaching mammoth proportions, the firm’s general partners said they turned away more than $70 million amid high demand for the effort. There’s more where that came from, here’s a quick look at the other VCs to announce funds this week:

This week, I penned a deep dive on Slack, formerly known as Tiny Speck, for our premium subscription service Extra Crunch. The story kicks off in 2009 when Stewart Butterfield began building a startup called Tiny Speck that would later come out with Glitch, an online game that was neither fun nor successful. The story ends in 2019, weeks before Slack is set to begin trading on the NYSE. Come for the history lesson, stay for the investor drama. Here are the other standout EC pieces of the week.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I debate whether the tech press is too negative or too positive in its coverage of tech startups. Plus, we dive into Brex’s upcoming round, SoFi’s massive raise and CrowdStrike’s imminent IPO.

Powered by WPeMatico

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

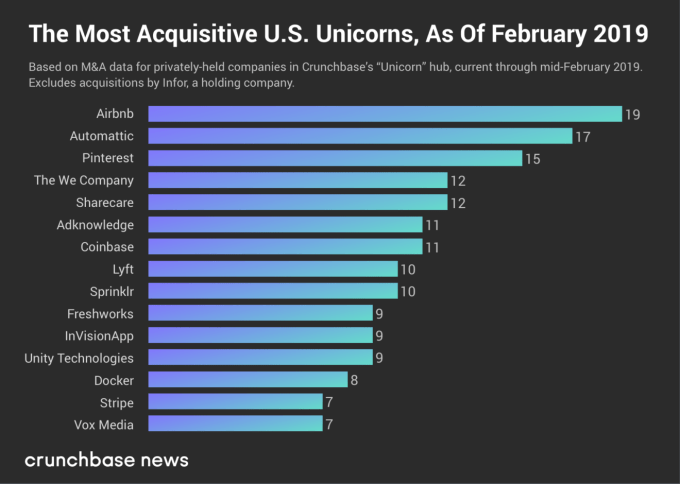

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

Tom Griffiths has founded four companies, two of which “weren’t much to write home about,” he jokes. The third captured the world’s attention: FanDuel, the fantasy sports company that was routinely in the press — not always for desirable reasons — from nearly the day it launched, to its near merger with rival DraftKings, to its ultimate sale last May to the European betting giant Paddy Power Betfair in a deal that reportedly saw FanDuel’s founders, along with its employees, walk away with almost nothing at the end of their roller coaster ride.

Little wonder that Griffith’s new, fourth company, Hone, is targeting the comparatively undramatic world of workforce training. Specifically, Hone and his small team have built a platform for modern and distributed teams, inspired largely by FanDuel’s experience of becoming a unicorn at one point in just six years’ time, and growing its team from 5 to 500 people in the process. Looking back, says Griffiths, “We really didn’t have the manager training we wanted or needed.”

In fact, Griffiths had already left the company by the time it was acquired, around his 10th anniversary last year, to “go back to the start.” It was time, he says. FanDuel had grown like a weed. He was exhausted by the many regulators wrestling with whether FanDuel provided a legally acceptable form of gambling. He knew he wanted to work in education, too. “My mom was a teacher,” he offers simply.

Enter Griffith’s newest act, which is just 10 months old at this point. The goal of the San Francisco-based company is to improve people’s skills around leadership management and people management, specifically at companies that already have hundreds of employees and that are dealing with increasingly distributed and diverse teams.

Hone is obviously not the first company tackling the remote management training or team building. The market already attracts tens of billions of dollars each year. But he insists it will be one of the best, including because it’s unlike a lot of what’s available currently. For one thing, Hone is very anti-traditional workshop. Hone also eschews pre-recorded video, working instead with qualified professional coaches who have to audition for Hone and who are already teaching a growing number of customers 12 different modules, typically in online class sizes of eight to a dozen people.

A company simply signs up, chooses from the programs (these include an intensive manager bootcamp, for example, as well as a manager 101 program), then embarks on what are 60- to 90-minute sessions each week for seven weeks.

The idea, in part, is for the learnings to stick. According to Griffiths, trainees forget 70 percent of what they are taught within 24 hours of a training experience. Instilling new lessons and reiterating old ones produces a greater return on investment for Hone’s customers, he suggests.

Hone’s underlying platform is also a differentiator, he says. It contains a reporting interface, so companies can not only see who is in attendance, but they can measure learner feedback through students who are asked afterward to provide the company with details about what they’ve learned. Hone’s software can also track how many questions were asked to assess engagement.

The self-learning platform gives Hone an easier way to assess how successful, or not, a particular module proves to be, and it allows Hone to continue sharpening its products. In fact, Griffiths says that by working with early, paying customers that include WeWork, Clear, App Annie, Dashlane, Omada Health, SoulCycle and others, Hone has already learned much that it intends to bake into future products,.

“We were in pilot mode last year to get product-market fit.” Now, the company is ready for its close-up, he suggests.

Some new funding should help. In addition to taking the wraps off Hone and opening more widely for business, the company just raised $3.6 million in seed funding led by Cowboy Ventures and Harrison Metal. Other participants in the round include Slack Fund, Reach Capital, Rethink Education, Day One Ventures, Entangled Ventures and numerous relevant angel investors, like Masterclass CEO David Rogier and Guild Education CEO Rachel Carlson.

What the 10-month-old company isn’t sharing publicly just yet is its pricing, which may remain flexible in any case. Says Griffiths, “We work with customers to diagnose their needs, then we create a package, one that’s far more reasonable than classroom training. There’s no travel. No instructor having to come to you.”

Griffiths is more forthcoming when it comes to lessons learned at FanDuel. Among these is aligning one’s self with investors who share a company’s values. He points to Cowboy Ventures founder Aileen Lee, calling her a “towering pillar of progressive values, equality, inclusion and diversity.” What he saw at FanDuel, he says, is that “investors can influence culture. So from the board down, you want people who share your same values.”

Griffiths also stresses the “importance of establishing a strong culture and a vision from the start, and to live that every day as you grow.

“It’s something we did well at FanDuel at some times,” he says, “and not so well at other times.”

Hone founders, left to right: Savina Perez, who was formerly a VP of marketing at CultureIQ, a platform that aims to helps companies strengthen their culture; Tom Griffiths; and Jeremy Hamel, who was formerly the head of product at CultureIQ.

Powered by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

San Francisco-based Tally Technologies raised $15 million in Series A venture funding to launch an app that promises to help people maintain good credit while avoiding fees, charges and other credit card affiliated pains. Shasta Ventures led the Series A and was joined by the company’s earlier backers — Cowboy Ventures and AITV. Silicon Valley Bank also invested. Read More

San Francisco-based Tally Technologies raised $15 million in Series A venture funding to launch an app that promises to help people maintain good credit while avoiding fees, charges and other credit card affiliated pains. Shasta Ventures led the Series A and was joined by the company’s earlier backers — Cowboy Ventures and AITV. Silicon Valley Bank also invested. Read More

Powered by WPeMatico