affirm

Auto Added by WPeMatico

Auto Added by WPeMatico

Shares of Square are up this morning after the company announced its second-quarter earnings and that it will buy Afterpay, an Australian buy now, pay later (BNPL) player in a $29 billion deal. As TechCrunch reported this morning, Afterpay shareholders will receive 0.375 shares of Square in exchange for their existing equity.

Shares of Afterpay are sharply higher after the deal was announced thanks to its implied premium, while shares of Square are up 7% in early-morning trading.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Over the past year, we’ve written extensively about the BNPL market, usually from the perspective of earnings from companies in the space. Afterpay has been a key data source, along with the yet-private Klarna and U.S. public BNPL outfit Affirm. Recall that each company has posted strong growth in recent periods, with the United States arising as a prime competitive market.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

From that landscape, let’s explore the Square-Afterpay deal. We want to know what Afterpay brings to Square in terms of revenue, growth and reach. We also want to do some math on the price Square is willing to pay for the company — and what that might tell us about the value of BNPL and fintech revenues more broadly. Then we’ll eyeball the numbers and try to decide if Square is overpaying for Afterpay.

As with most major deals these days, Square and Afterpay released an investor presentation detailing their argument in favor of their combination. Let’s dig through it.

Square is a two-part company. It has a large consumer business via Cash App, and it has a large business division that offers payments tech and other fintech services to corporate customers. Recall that Square is also building out banking services for its business customers and that Cash App also serves some banking and investing functionality for consumers.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week had the whole crew aboard to record: Grace and Chris making us sound good, Danny to provide levity, Natasha to actually recall facts and Alex to divert us from staying on topic. It’s teamwork, people — and our transitions are proof of it.

And it’s good that we had everyone around the virtual table, as there was quite a lot to get through:

Thanks for hanging out this week, Equity is back on Tuesday with our usual weekly kickoff, thanks to the American holiday on Monday. Chat then, unless you want to follow us on Twitter and get a first-look at all of Chris’ meme work.

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday morning at 7:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

“Most of the startups I give advice to about how to raise venture capital shouldn’t be raising venture capital,” an investor recently told me. While the idea that every startup isn’t venture-backable might run counter to the narrative to the barrage of funding news each week, I think it’s important to double click on the topic. Plus, it keeps coming up, off the record, on phone calls with investors!

As venture grows as an asset class, the access to capital has broadened from a dollar perspective, but I do think the difficulties that remain is an important dynamic to call out (and something no one talks about during an upmarket). Beyond the fact that only a small subset of startups truly can pull off scaling to the point of venture-level returns, it is still hard for even qualified founders to raise venture capital. Venture capital is still a heavily white, male-led industry, and as a result contains bias that disproportionately limits access for underrepresented founders.

Eniac founding partner Hadley Harris applied this dynamic to the current market boom in a recent tweet: A lot of people are misunderstanding this VC funding market. More money is flowing into the market but the increase is not evenly distributed. The market believes winners can be much bigger but not necessary that there will be more winners. It’s still very hard for most to raise a VC.

To say otherwise is to gaslight the early-stage or first-time founders that have spent months and months trying to raise their first institutional dollars and failed. So ask yourself: Seed rounds have indeed grown bigger, but for who? What comes at the cost of the $30 million seed round? Are the founders that can raise overnight from diverse backgrounds? Are investors backing first-time founders as much as they are backing second- or third-time entrepreneurs?

The answers might leave you debating about the boundaries, and limitations, of the upcoming hot-deal summer.

A few weeks ago, I wrote about the disconnect between due diligence and fundraising right now. Now we’ve moved onto the disconnect, and bifurcation, within first-check fundraising itself. There is so much more we can get into about the fallacy of “democratization” in venture capital, from who gets to start a rolling fund to the lack of assurance within equity crowdfunding campaigns.

We’ll get through it all together, and in the meantime make sure to follow me on Twitter @nmasc_ for more hot takes throughout the week.

In the rest of this newsletter, we will talk about fintech politics, the Affirm model with a twist, and sneakers-as-a-service.

The inimitable Mary Ann Azevedo has been dominating the fintech beat for us, covering everything from the latest Uruguayan unicorn to Acorn’s scoop of a debt management startup. But the story I want to focus on this week is her interview with ex-Coinbase counsel & former Treasury official, Brian Brooks.

Here’s what to know: Coinbase CEO Brian Armstrong notoriously released a memo last year denouncing political activism at work, calling it a distraction. In this exclusive interview, Brooks spoke about how blockchain is the answer to financial inclusion, and argued why politics needs to be taken out of tech.

We don’t want bank CEOs making those decisions for us as a society, in terms of who they choose to lend money to, or not. We need to take the politics out of tech. All of us do a lot of different things, and we have no idea on a given day, whether what we’re doing is popular with our neighbors or popular with our bank president or not. I don’t want the fact that I sometimes feel Republican to be a reason why my local bank president can deny me a mortgage.

Image Credits: Bryce Durbin/TechCrunch

While Affirm may have popularized the “buy now, pay later” model, the consumer-friendly business strategy still has room to be niched down into specific subsectors. I ran into one such startup when covering Plaid’s inaugural cohort of startups in its accelerator program.

Here’s what to know: Walnut is a new seed-stage startup that is a point-of-sale loan company with a healthcare twist. Unlike Affirm, it doesn’t make money off of fees charged to consumers.

Image Credits: Bryce Durbin/TechCrunch

Everything you could ever want to know about StockX

In our latest EC-1, reporter Rae Witte has covered a startup that leads one of the most complex and culturally relevant marketplaces in the world: sneakers.

Here’s what to know: StockX, in her words, has built a stock market of hype, and her series goes into its origin story, authentication processes and a market map.

Image Credits: Nigel Sussman

Found, a new podcast joining the TechCrunch network, has officially launched! The Equity team got a behind-the-scenes look at what triggered the new podcast, the first guests and goals of the show. Make sure to tune into the first episode.

Also, if you run into any paywalls while browsing today’s newsletter, make sure to use discount code STARTUPSWEEKLY to get 25% off an annual or two-year Extra Crunch subscription.

Seen on TechCrunch

Okta launches a new free developer plan

New Jersey announces $10M seed fund aimed at Black and Latinx founders

Education nonprofit Edraak ignored a student data leak for two months

6 VCs talk the future of Austin’s exploding startup ecosystem

Dear Sophie: Help! My H-1B wasn’t chosen!

Seen on Extra Crunch

5 machine learning essentials nontechnical leaders need to understand

How we dodged risks and raised millions for our open-source machine language startup

Giving EV batteries a second life for sustainability and profit

And that’s a wrap! Thanks for making it this far, and now I dare you to go make the most out of the rest of your day. And by make the most, I mean listen to Taylor’s Version.

Warmly,

Powered by WPeMatico

Healthcare insurance, if you’re lucky to have it, only covers a subset of conditions in the United States. As a result, patients can often get burdened with horror story charges, like huge deductibles, out-of-network costs and expensive co-pays. So for the uninsured and insured alike, innovative ways of managing big bills are in high demand — especially as uncertainty remains around how COVID-19 and long-haul symptoms will be handled by patients and payers.

Walnut, founded by Roshan Patel, is a point-of-sale lending company with a healthcare twist. Walnut uses a “buy now, pay later” model, popularized by Affirm and Klarna, to help patients pay for healthcare over a period of time, instead of in one $3,000 chunk. Walnut works with healthcare providers so that a patient’s bill can be paid back through $100-a-month increments for 30 months, instead of one aggressive credit card swipe.

A patient using Walnut to pay healthcare bills. Image Credits: Walnut

It’s a sweet deal, but Patel added one more detail that he thinks makes Walnut stand out: The startup doesn’t charge any interest or fees to consumers.

“Almost every ‘buy now, pay later’ company in e-commerce charges interest or fees, and every personal loan provider charges interest or fees, but we do not,” he said. “And that’s really important to me, not making healthcare any more expensive than it already is. It’s a very patient-friendly product.”

Companies that use the buy now, pay later model with zero interest or fees need to make revenue somehow, and in Walnut’s case it is by charging healthcare providers a percentage of each sale or transaction.

If a provider’s collection rate for an out-of-pocket is 50%, Walnut would go to them and say “give us a 40% discount, and we’ll guarantee the cash for you upfront.” The startup will take the risk, and then the provider is able to make 60% of the collection rate.

Now, ideally, a provider would want to get 100% of payments they are owed, but that is wishful thinking. Patel explained that a large number of bills go unpaid due to bankruptcies or a default on payments (the average collections rate for hospitals out of pocket is less than 20%). Because of this, a company like Walnut has room to offer at least some stable upfront cash to hospitals, even if it ends up being 60% of overall bills versus 100%.

The company uses “extensive underwriting models” to figure out if a patient should qualify for a loan. Patel says that the startup goes beyond using credit score, which he describes as an “outdated metric”, and instead looks at thousands of data points from different providers, from side hustle income to spending habits on things like groceries and bills.

Image Credits: Lightspring (opens in a new window) / Shutterstock (opens in a new window)

Walnut’s biggest challenge, says Patel, is to underwrite the population and pay the healthcare provider upfront in cash. It then collects from the patient on the back end, which comes with its own amount of risk.

“To be able to take on that risk for patients that are less credit-worthy is a very challenging problem, and I don’t think it’s really solved yet in healthcare,” he said.

The startup is starting by working with small private practices of one to five physicians that focus on specialties like dentistry, dermatology and fertility.

A big part of Walnut’s success will be determined by if it can attract people that truly need flexible financing options. For example, the company doesn’t have any hospitals as a partner yet, which would tap a larger group of patients that likely need flexible financing options the most. Right now, “the people who get elective-care surgery are the ones that can afford it.”

But Patel doesn’t see this as a disconnect; instead, he sees it as an opportunity to widen access to elective medical care to more people.

“I talked to a person last week who has no teeth and wants dentures but it costs $6,000,” he said. “That person should be able to afford it, and we enabled them to pay $100 a month for it.”

Walnut’s two biggest customer groups are the uninsured (people who have lost their jobs from COVID-19), and consumers who have high deductible plans.

Walnut isn’t the first. PrimaHealth Credit, Walnut’s closest competitor, offers point-of-sale lending procedures for elective medical procedures. Think surgeries like cataract work or dental work. The company said the service is currently available in Arizona, California, Florida, Oklahoma and Texas, and will be expanded to all 50 states this year. Walnut, comparatively, is mostly focused on the East Coast and plans to expand nationwide by the end of this year.

PrimaHealth’s average loan size is $1,800, and Walnut’s average loan size is $5,000.

The company is currently piloting with a handful of healthcare providers in dermatology, dentistry and fertility. It has had more than 500 patient loan applications, totaling over $4.6 million in application volume year-to-date. Patel says that Walnut only accepted a fraction of these applications, but declined to share what percent of money it has lent so far. As Walnut refines its model, it might be able to cover other categories.

Up until this point, Walnut has been lending off of its own balance sheet. In order to truly scale, it will need to get a new source of capital — either a credit line, debt financing round or venture capital — to offer more loans. Patel says that the startup is in talks with banks, and turned down a debt offer due to size and rate.

Venture capital seems to be the solution for now: The startup announced that it has raised a $3.6 million seed round from investors including Gradient Ventures, Afore Capital, 2048 Ventures, Supernode Ventures, TA Ventures, Polymath Capital, Tack Ventures, Awesome People Ventures, Newark Ventures and NKM Capital. Angels include the CEOs of Giphy and PillPack, and the CTO of Rampm Financial as well as an NFL coach. The company is also a part of Plaid’s inaugural accelerator.

“I don’t want to be yet another startup trying to offer you an undifferentiated insurance plan,” Patel said.

Powered by WPeMatico

This morning Wisetack, a startup that provides buy-now-pay-later services to in-person business transactions, announced that is has closed a total of $19 million across two rounds, a seed investment and a Series A.

Greylock led both rounds, with the seed round clocking in at $4 million and the Series A at $15 million. Bain Capital Ventures also took part in the company’s fundraising.

Notably both rounds were closed in 2019, making these amongst the more aged rounds that we’ve heard of in recent quarters. However, as much venture reporting was delayed last year due to the pandemic and political unsettlement, I am still willing to cover the occasional antique deal.

Wisetack caught our eye not only due to its fundraising activity, but also thanks the buy-now-pay-later (BNPL) space becoming all the more interesting in the wake of Affirm’s direct listing. Affirm is perhaps the best-known service of its type, making its liquidity moment — and post-IPO performance — impactful for its broader business category.

But while Affirm wants to offer point-of-sale BNPL services to online merchants, Wisetack is taking a different approach. It focuses on the in-person business world, helping finance consumer transactions involving things like home improvement and car repair; the sort of big transactions that your average family might not have the cash to cover but also doesn’t want to put on a credit card.

Wisetack partners with vertical SaaS players in different areas. Say, plumbing. This allows users of those vertical SaaS applications — the plumbers, sticking to the same example — to offer Wisetack’s BNPL service to their customers.

It’s well known that vertical SaaS has wide application. A favorite recent example is SingleOps, which provides software for the so-called “green industry,” the world of lawns and landscaping. There’s SaaS for all sorts of IRL work, which could mean that Wisetack has a good number of software providers to sell into.

The model appears to be working, at least thus far. Wisetack shared with TechCrunch that its loan volume rose 20x between January of 2020 and January of 2021. As the company generates revenues from merchants (loan processing costs), and consumer interest, it’s likely that its revenue scales with loan volume. If the relationship is even closer to direct, Wisetack grew quite a lot last year.

The startup also said that the number of businesses using Wisetack grew 25-fold last year to a number in the “thousands.”

Wisetack fits neatly into a number of recent trends. The first is its work with vertical SaaS, a notable slice of the software market. The second is that Wisetack is another example of an API-led business, offering its service as a tech-powered add-on to other bits of code. And, third, that Wisetack had the same lead investor twice in sequential rounds. This sort of doubling-down from the venture community has become common in recent quarters as the signaling risk of having the lead twice in a row has been zeroed out by general investor enthusiasm for more equity in what appear to be winning startups.

Finally, the Wisetack round is interesting as it is nearly a sort of vertical BNPL, or at least a vertically focused BNPL. The company was reticent to share notes on how it comes to credit decisions, but we presume that all BNPL players that do focus on a particular niche or segment.

Powered by WPeMatico

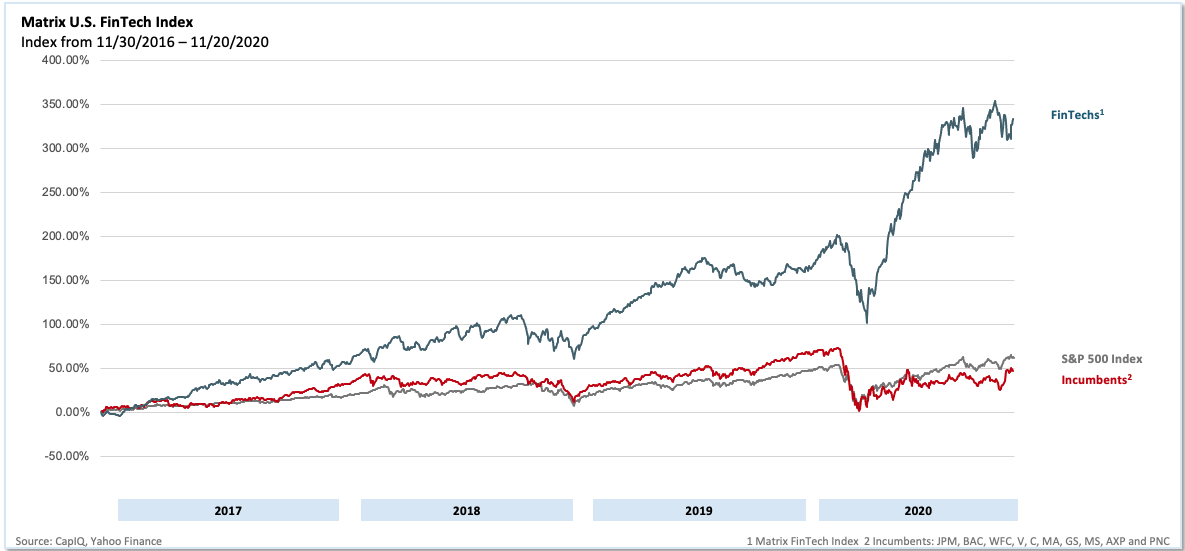

Three years ago, we released the first edition of the Matrix Fintech Index. We believed then, as we do now, that fintech represents one of the most exciting major innovation cycles of this decade. In 2020, all the long-term trends forcing change in this sector continued and even accelerated.

The broad movement away from credit toward debit, particularly among younger consumers, represents one such macro shift. However, the pandemic also created new, unforeseen drivers. Among them, millennials decamped from their rentals in crowded cities to accelerate their first home purchases to the benefit of proptech companies and challenger mortgage players alike.

E-commerce saw an enormous acceleration in growth rates, furthering adoption of online payments platforms. Lastly, low interest rates and looming inflation helped pave the way for the price of Bitcoin to charge toward $30,000. In short, multiple tailwinds combined to produce a blockbuster year for the category.

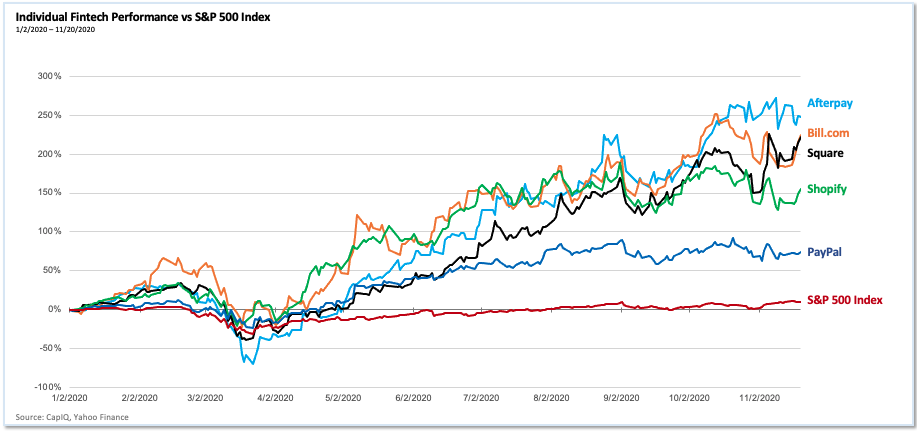

In this year’s refresh of the Matrix Fintech Index, we’ll divide our attention into three parts. First, a look at the public stocks’ performance. Second, liquidity. Third, we highlight one major trend in the sector: Buy Now Pay Later, or BNPL.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index. While the underlying performance of these companies was strong, the pandemic further bolstered results as consumers avoided appearing in-person for both shopping and banking. Instead, they sought — and found — digital alternatives.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index.

Our own representation of the public fintechs’ performance is the Matrix Fintech Index — a market cap-weighted index that tracks the progress of a portfolio of 25 leading public fintech companies. The Matrix fintech Index rose 97% in 2020, compared to a 14% rise in the S&P 500 and a 10% drop for the incumbent financial service companies over the same time period.

2020 performance of individual fintech companies vs. SPX Image Credits: CapiQ, Yahoo Finance

Matrix U.S. Fintech Index, 2016 -2020 Image Credits: CapiQ, Yahoo Finance

E-commerce undoubtedly stood out as a major driver. As a category, retail e-commerce grew 35% YoY as of Q3, propelling PayPal and Shopify to add over $160 billion of market capitalization over the year. For its part, PayPal in the third quarter signed up 15 million net new active accounts (its highest ever).

Powered by WPeMatico

As expected, shares of Poshmark exploded this morning, blasting over 130% higher in afternoon trading from the company’s above-range IPO price of $42. The enormous and noisy debut of Poshmark comes a day after Affirm, another IPO, was treated similarly by the public markets.

Both explosive debuts were preceded by huge December debuts from C3.ai, Doordash and Airbnb. It seems today that any venture-backed company that can claim some sort of tech mantle is being treated to a strong IPO pricing run and a huge first-day result.

This is, of course, annoying to some people. Namely, certain elements of the venture capital community who would prefer to keep all outsized gains in their own pockets. But, no matter. You might be wondering what is going on. Let’s talk about it.

TechCrunch has covered the IPO window as closely as we can over the last few years. And the late-stage venture capital markets, along with the changing value of tech stocks and the huge boom in consumer (retail) investing.

Based on my participation in as much of that reporting as I could take part in here’s how you get a 130% first-day IPO pop in a company that has actually been around long enough for investors to math-out reasonable growth and profit expectations for the future:

Powered by WPeMatico

And we’re off to the races!

Last night, Affirm priced its IPO above its raised range at $49 per share, a sign that the public markets remain hungry for new listings. Provided that Affirm today trades similarly to how it priced, we could be looking at a 2021 IPO market that resembles last year’s heated results.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

That’s good news for a host of companies looking to follow in the financial technology unicorn’s footsteps.

Poshmark prices tonight and trades tomorrow. With Qualtrics in the wings along with Coinbase, Roblox set to direct list, and Bumble said to file as well, we’re heading into another busy IPO quarter. Affirm’s first-day trading results will therefore hold extra importance, even if its pricing augurs well for IPOs more generally.

Affirm first targeted $33 to $38 per share before raising its range to $41 to $44 per share. Pricing at $49 is a victory. Briefly, why, and then a thought about what’s next for the IPO market.

Affirm first targeted $33 to $38 per share before raising its range to $41 to $44 per share. Pricing at $49 is a victory. Briefly, why, and then a thought about what’s next for the IPO market.

What does Affirm sell? First, per its S-1 filings, it charges merchants a fee to “convert a sale and power a payment.” That sounds like software revenues, albeit not in the recurring manner of a SaaS company.

Second, Affirm earns from “interest income [from] the simple interest loans that we purchase from our originating bank partners.” And, it offers virtual cards to consumers via its app, allowing it to generate interchange revenues.

We care about all of that as it’s important to realize that Affirm is not a software company in the context that we usually think about them, namely software as a service, or SaaS.

This matters when we consider how the market values Affirm; the more richly Affirm is valued in revenue-multiple terms by its new, $49 per-share IPO price, the more bullish we can presume the IPO market is.

What are Affirm’s gross margins? A great question, and one that is surprisingly hard to answer. If you read its final S-1 filing, you’ll find that all its chatter concerning “contribution profit” has been removed. This is a shame to some degree as contribution profit — and margin — were Affirm’s closest shared cognate to gross margin.

Powered by WPeMatico

Today Bumble, a popular dating-focused startup, was reported by Bloomberg to have filed IPO documents, albeit privately.

The news that Bumble is pursuing an IPO is not a surprise. TechCrunch covered the story in September, noting the huge revenues that its rival Tinder has managed to accrete, possibly indicative of a sufficiently large market to support two public dating players.

That Bumble has privately filed puts it, along with the crypto-focused Coinbase, as far along the IPO path before we can see their numbers. When they make their S-1 filings public the two companies will provide the market a look into their financial results.

Bumble and Coinbase are preceded in making such disclosures by Roblox, Affirm and Poshmark. The five companies will join others in seeking IPOs over the next few months.

According to a recent interview with GGV’s Hans Tung — an investor in Affirm and Airbnb and other unicorns — TechCrunch understands that quarters one, three and four in 2021 could prove to be active IPO periods. Bumble joining the fray in the final weeks of 2020 underscores how active the start of the year could be for highly priced private companies seeking liquidity while public markets trade near all-time highs.

TechCrunch reached out to Bumble for comment on the IPO report. The company declined to comment.

Bloomberg reports that Bumble could target a valuation of between $6 and $8 billion. This squares with prior reporting. How much revenue the market will require of Bumble to reach those prices, and at what pace of growth, is not clear.

But with the company reaching 100 million users earlier this year, perhaps all the math will pencil out.

Powered by WPeMatico

Amount, a new service that helps traditional banks compete in a digital world, has raised $81 million from none other than Goldman Sachs as it looks to help legacy fintech players compete with their more nimble digital counterparts.

The company, which spun out from the startup lending company Avant in January of this year, has already inked deals with Banco Popular, HSBC, Regions Bank and TD Bank to power their digital banking services and offer products like point-of-sale lending to compete with challenger banks like Chime and lenders like Affirm or Klarna.

“Most banks are looking for resources and infrastructure to accelerate their digital strategy and meet the demands of today’s consumer,” said Jade Mandel, a vice president in Goldman Sachs’ growth equity platform, GS Growth, who will be joining the board of directors at Amount, in a statement. “Amount enables banks to navigate digital transformation through its modular and mobile-first platform for financial products. We’re excited to partner with the team as they take on this compelling market opportunity.”

Complementing those customer-facing services is a deep expertise in fraud prevention on the back-end to help banks provide more loans with less risk than competitors, according to chief executive Adam Hughes.

It’s the combination of these three services that led Goldman to take point on a new $81 million investment in the company, with participation from previous investors August Capital, Invus Opportunities and Hanaco Ventures — giving Amount a post-money valuation of $681 million and bringing the company’s total capital raised in 2020 to a whopping $140 million.

Think of Amount as a white-labeled digital banking service provider for Luddite banks that hadn’t upgraded their services to keep pace with demands of a new generation of customers or the COVID-19 era of digital-first services for everything.

Banks pay a pretty penny for access to Amount’s services. On top of a percentage for any loans that a bank processes through Amount’s services, there’s an up-front implementation fee that typically averages at $1 million.

The hefty price tag is a sign of how concerned banks are about their digital challengers. Hughes said that they’ve seen a big uptick in adoption since the launch of their buy-now-pay-later product designed to compete with the fast growing startups like Affirm and Klarna .

Indeed, by offering banks these services, Amount gives Klarna and Affirm something to worry about. That’s because banks conceivably have a lower cost of capital than the startups and can offer better rates to borrowers. They also have the balance sheet capacity to approve more loans than either of the two upstart lenders.

“Amount has the wind at its back and the industry is taking notice,” said Nigel Morris, the co-founder of Capital One and an investor in Amount through the firm QED Investors. “The latest round brings Amount’s total capital raised in 2020 to nearly $140 million, which will provide for additional investments in platform research and development while accelerating the company’s go-to-market strategy. QED is thrilled to be a part of Amount’s story and we look forward to the company’s future success as it plays a vital role in the digitization of financial services.”

FT Partners served as advisor to Amount on this transaction.

Powered by WPeMatico