Adyen

Auto Added by WPeMatico

Auto Added by WPeMatico

The payments space — amazingly — remains up for grabs for startups. Yes, dear reader, despite the success of Stripe, there seems to be a new payments startup virtually every other day. It’s a mess out there! The accelerated growth of e-commerce due to the pandemic means payments are now a booming space. And here comes another one, with a twist.

WhenThen has built a no-code payment operations platform that, they claim, streamlines the payment processes “of merchants of any kind”. It says its platform can autonomously orchestrate, monitor, improve and manage all customer payments and payments ops.

The startup’s opportunity has arisen because service providers across different verticals increasingly want to get into open banking and provide their own payment solutions and financial services.

Founded six months ago, WhenThen has now raised $6 million, backed by European VCs Stride and Cavalry.

The founders, Kirk Donohoe, Eamon Doyle and Dave Brown, are three former Mastercard Payment veterans.

Based out of Dublin, CEO Donohoe told me: “We see traditional businesses embracing e-comm, and e-comm merchants now operating multiple business models such as trade supply, marketplace, subscription, and more. There is no platform that makes it easy for such businesses to create and operate multiple payment flows to support multiple business models in one place — that’s where we step in.”

He added: “WhenThen is helping e-commerce digital platforms build advanced payment flows and payment automation, in minutes as opposed to months. When you start to integrate different payment methods, different payment gateways, how you want the payment to move from collection through to payout gets very, very complex. I’ve been doing this for over a decade now, as an entrepreneur building different businesses that had to accept, collect and pay payments.”

He said his founding team “had to build very complex payment flows for large merchants, airlines, hotels, issuers, and we just found it was ridiculous that you have to continue to do the same thing over and over again. So we decided to come up with WhenThen as a better way to be able to help you build those flows in minutes.”

Claude Ritter, managing partner at Cavalry, said: “Basic payment orchestration platforms have been around for some time, focusing mostly on maximizing payment acceptance by optimizing routing. WhenThen provides the first end-to-end payment flow platform to equip businesses with the opportunity to control every stage of the payment flow from payment intent to payout.”

WhenThen supports a wide range of popular payment providers such as Stripe, Braintree, Adyen, Authorize.net, Checkout.com, etc., and a variety of alternative and locally preferred payment methods such as Klarna Affirm, PayPal and BitPay.

“For brave merchants considering global reach and operating multiple business models concurrently, I believe choosing the right payment ops platform will become as important as choosing the right e-commerce platform. Building your entire e-comm experience tightly coupled to a single payment processor is a hard correction to make down the line — you need a payment flow platform like WhenThen”, added Fred Destin, founder of Stride.VC.

Powered by WPeMatico

It’s a big morning for fintech startups today: Flywire, a Boston-based magnet for venture capital, has filed to go public.

Flywire is a global payments company that attracted more than $300 million as a startup, according to Crunchbase, most recently raising a $60 million Series F last month. We don’t have its most recent valuation, but PitchBook data indicates that the company’s February 2020, $120 million round valued Flywire at $1 billion on a post-money basis.

So what we’re looking at here is a fintech unicorn IPO. A great way to kick off the week, to be honest, though I’d thought that Robinhood would be the next such debut.

Fintech venture capital activity has been hot lately, which makes the Flywire IPO interesting. Its success or failure could dictate the pace of fintech exits and fintech startup valuations in general, so we have to care about it.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Regardless, we’re doing our regular work this morning. First, what does Flywire do and with whom does it compete? Then, a closer look at its financial results as we hope to get our hands around its revenue quality, aggregate economics and growth prospects.

After that, we’ll discuss valuations and which venture capital groups are set to do well in its flotation. The company had a number of backers, but Spark Capital, Temasek, F-Prime Capital and Bain Capital Ventures made the major shareholder list, along with Goldman Sachs. So, a number of firms and funds are hoping for a big Flywire exit. Let’s dig in.

Flywire is a global payments company. Or, as it states in its S-1 filing, it’s “a leading global payments enablement and software company.” And it thinks that its market, and by extension itself, has lots of room to grow. While “substantial strides [have been] made in payments technology in the retail and e-commerce industries,” the company wrote, “massive sectors of our global economy—including education, healthcare, travel, and business-to-business, or B2B, payments—are still in the early stages of digital transformation.”

That’s the same logic behind Stripe’s epic valuation and the rising value of payments-focused companies like Finix.

Powered by WPeMatico

YL Ventures, the Israel-focused cybersecurity seed fund, today announced that it has sold its stake in cybersecurity asset management startup Axonius, which only a week ago announced a $100 million Series D funding round that now values it at around $1.2 billion.

ICONIQ Growth, Alkeon Capital Management, DTCP and Harmony Partners acquired YL Venture’s stake for $270 million. This marks YL’s first return from its third $75 million fund, which it raised in 2017, and the largest return in the firm’s history.

With this sale, the company’s third fund still has six portfolio companies remaining. It closed its fourth fund with $120 million in committed capital in the middle of 2019.

Unlike YL, which focuses on early-stage companies — though it also tends to participate in some later-stage rounds — the investors that are buying its stake specialize in later-stage companies that are often on an IPO path. ICONIQ Growth has invested in the likes of Adyen, CrowdStrike, Datadog and Zoom, for example, and has also regularly partnered with YL Ventures on its later-stage investments.

“The transition from early-stage to late-stage investors just makes sense as we drive toward IPO, and it allows each investor to focus on what they do best,” said Dean Sysman, co-founder and CEO of Axonius. “We appreciate the guidance and support the YL Ventures team has provided during the early stages of our company and we congratulate them on this successful journey.”

To put this sale into perspective for the Silicon Valley and Tel Aviv-based YL Ventures, it’s worth noting that it currently manages about $300 million. Its current portfolio includes the likes of Orca Security, Hunters and Cycode. This sale is a huge win for the firm.

Its most headline-grabbing exit so far was Twistlock, which was acquired by Palo Alto Networks for $410 million in 2019, but it has also seen exits of its portfolio companies to Microsoft, Proofpoint, CA Technologies and Walmart, among others. The fund participated in Axonius’ $4 million seed round in 2017 up to its $58 million Series C round a year ago.

It seems like YL Ventures is taking a very pragmatic approach here. It doesn’t specialize in late-stage firms — and until recently, Israeli startups always tended to sell long before they got to a late-stage round anyway. And it can generate a nice — and guaranteed — return for its own investors, too.

“This exit netted $270 million in cash directly to our third fund, which had $75 million total in capital commitments, and this fund still has six outstanding portfolio companies remaining,” Yoav Leitersdorf, YL Ventures’ founder and managing partner, told me. “Returning multiple times that fund now with a single exit, with the rest of the portfolio companies still there for the upside is the most responsible — yet highly profitable path — we could have taken for our fund at this time. And all this while diverting our energies and means more towards our seed-stage companies (where our help is more impactful), and at the same time supporting Axonius by enabling it to bring aboard such excellent late-stage investors as ICONIQ and Alkeon — a true win-win-win situation for everyone involved!”

He also noted that this sale achieved a top-decile return for the firm’s limited partners and allows it to focus its resources and attention toward the younger companies in its portfolio.

Powered by WPeMatico

Silverflow, a Dutch startup founded by Adyen alumni, is breaking cover and announcing seed funding.

The pre-launch company has spent the last two years building what it describes as a “cloud-native” online card processor that directly connects to card networks. The aim is to offer a modern replacement for the 20 to 40-year-old payments card processing tech that is mostly in use today.

Backing Silverflow’s €2.6 million seed round is U.K.-based VC Crane Venture Partners, with participation from Inkef Capital and unnamed angel investors and industry leaders from Pay.On, First Data, Booking.com and Adyen. It brings the fintech startup’s total funding to date to ~€3 million.

Bootstrapped while in development and launching in 2021, Silverflow’s founders are CEO Anne-Willem de Vries (who was focused on card acquiring and processing at Adyen), CBDO Robert Kraal (former Adyen COO and EVP global card acquiring & processing of Adyen) and CTO Paul Buying (founder of acquired translation startup Livewords).

“The payments tech stack needs an upgrade,” Kraal tells me. “Today’s card payment infrastructure based on 30 to 40-year-old technology is still in use across the global payment landscape. This legacy infrastructure is costing everyone time and money: consumers, merchants, payment-service-providers and banks. The legacy platforms require a lengthy on-boarding process and are expensive to maintain, [and] they also aren’t fit for purpose today because they don’t support data use”.

In addition, Kraal says that adding new functionality is a lengthy and expensive process, requiring the effort of specialised engineers which ultimately slows down innovation “for the whole card payments system”.

“Finally, every acquirer provides its customer with a different processing platform, which for a typical payment service provider (PSP) means they have to deal with multiple legacy platforms — and all the costs and specialised support each entails,” adds de Vries.

To solve this, Silverflow claims it has built the first payments processor with a “cloud-native platform” built for today’s technology stack. This includes offering simple APIs and “streamlined data flows” directly integrated into the card networks.

Continues de Vries: “Instead of managing a complex network of acquirers across markets with dozens of bank and card network connections to maintain, Silverflow provides card-acquiring processing as a service that connects to card networks directly through a simple API”.

Target customers are PSPs, acquirers and “global top-market merchants” that are seeing €500 million to 10 billion in annual transactions.

“As a managed service, Silverflow provides the maintenance for connections and new product innovation that users have typically had to support in-house or work on long-term product road maps with suppliers,” explains Kraal. “Based in the cloud, Silverflow is infinitely scalable for peak flows and also provides robust data insights that users haven’t previously been able to access”.

With regards to competitors, Kraal says there are no other companies at the moment doing something similar, “as far as we are aware”. Currently, acquirers use traditional third-party processors, such as SIA, Omnipay, Cybersource or MIGS. Some companies, like Adyen, have built their own in-house processing platform.

So, why hasn’t a cloud-native card processing platform like Silverflow been done before and why now? A lack of awareness of the problem might be one reason, says de Vries.

“Unless you have built several integrations to acquirers during your career, you are not aware that the 30 to 40-years-old infrastructure is still in use. This is not typically a problem some bright college graduates would tackle,” he posits.

“Second, to build this successfully, you need to have prior knowledge of the card payments industry to navigate all the legal, regulatory and technical requirements.

“Thirdly, any large corporate currently active in card payment processing will be aware of the problem and have the relevant industry knowledge. However, building a new processing platform would require them to allocate their most talented staff to this project for two-three years, taking away resources from their existing projects. In addition, they would also need to manage a complex migration project to move their existing customers from their current system to the new one and risk losing some of the customers along the way”.

Powered by WPeMatico

The other week TechCrunch’s Extra Crunch Live series sat down with Accel VCs Sonali De Rycker and Andrew Braccia to chat about the state of the global startup investing ecosystem. Given their firm’s broad geographic footprint, we wanted to know what was going on in different startup markets, and inside a number of business-model varietals that we are tracking, like API-focused startups and low-code work.

As with all Extra Crunch Live episodes, we’ve included the full video below, along with a number of favorite quotes from the conversation.

Above the paywall, I wanted to share what De Rycker said about the European startup ecosystem: It’s been stuck in my head for the last day, because her comments points to a future where there is no single center of startup gravity.

Instead, considering her bullishness on her local scene, we’re going to see at least three major hubs, namely North America with a locus in the United States, Asia with a possible capital in India, and Europe, with a somewhat distributed layout.

Here’s De Rycker from our chat, responding to my question about how active the European venture and startup scene is today (transcript has been lightly edited for clarity):

What has surprised me even more [than change in the European startup scene over time] is the acceleration in the last couple of years. And I think it’s continued in the last few months, despite the COVID environment.

And that’s really because Europe isn’t just one location, right? It’s a collection of different ecosystems, different locations, different hubs. At any point in time there are 15 to 20 cities that are relevant, and they’ve all sort of reached this tipping point. And together, Europe is at this inflection point, in terms of the quality of entrepreneurs, [and] the number of opportunities. And it feels like it’s all come together with the digitization that’s going on that we’re all, you know, very much believing in right now. And the fact that there’s a ton of capital around. So I would say that we’re seeing a pretty frenetic pace, more than, candidly, pre-COVID, which is not something we expected. […]

But I would say that overall, Europe is incredibly active [regarding] deal pace, deal count, I wouldn’t say it’s very different from what I understand to be the situation in the U.S.

Undergirding what De Rycker said above, TechCrunch recently reported on the financial results of TransferWise, a European fintech unicorn that grew 70% in the last year, to £302.6 million in revenue. Toss in Adyen’s epic run as a public European tech company and there’s lots to celebrate from the continent, even if we don’t read enough about here in the States.

Extra Crunch Live continues with some really damn fun stuff coming up (including a few more that I am hosting). So, make sure you’re in and ready for the next edition as we dig deeper into season two.

Hit the jump for the full chat and some further bits from the transcript.

Here’s the full video:

Powered by WPeMatico

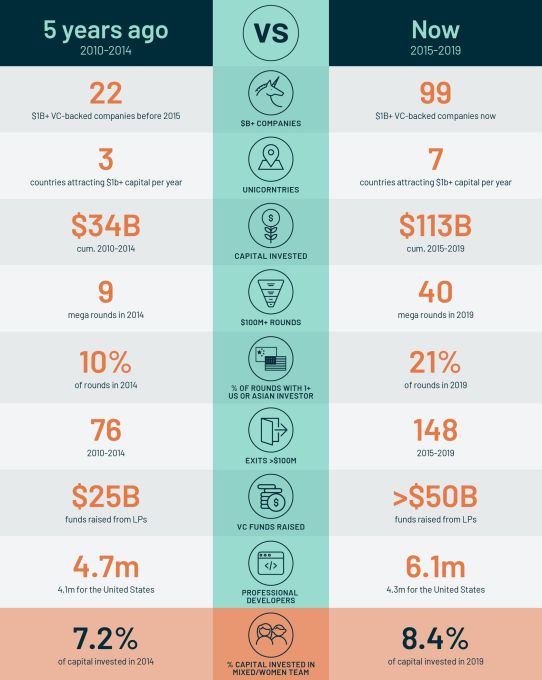

Atomico, the European venture capital firm founded by Skype’s Niklas Zennström, has released its latest annual The State of European Tech report, published in partnership with Slush and Orrick.

As part of the report, the authors surveyed 5,000 members of the ecosystem — including 1,000 founders — as well as pulling in robust data from other sources, such as Dealroom and the London Stock Exchange .

This year, the report reveals that the European tech ecosystem continues to mature and shows no sign of slowing — particularly highlighting the contrast from five years ago when the The State of European Tech report made its debut. Almost every key indicator is up and to the right, except, rather depressingly, diversity.

The data shows, for example, that competition for talent and access to the best founders has increased ferociously. And from a funding perspective, European founders have more choice than ever, especially with U.S. and Asian VC firms investing more and more in the region. Progress with gender diversity stalled, however, such as 92% of funding going to all-male teams.

I caught up with the report’s author Tom Wehmeier, Partner and Head of Insights at Atomico (also sometimes jokingly referred to as the “Mary Meeker of Europe”), where we discuss in more detail some of the key findings and why, it seems, that the rest of the world has finally woken up to Europe’s tech potential.

But first, a few headlines from the report:

Extra Crunch: It is 5 years since Atomico published the first The State of European Tech report, which really attempted to capture a data-driven snapshot of the entire ecosystem. What are some of the biggest changes you’ve seen within European tech in the intertwining years or in this year in particular?

Tom Wehmeier: If I think back to when we did the first report, people who believe that Europe could actually be an interesting player in global technology, were largely limited to people who were in the tech industry in Europe itself. If you then fast forward to today, what has clearly happened — and I think 2019 was the year where this really materialized and became part of the narrative — was that belief translating from people on the inside to a bunch of people that were on the outside.

Most obviously has been the strength of interest from from the U.S. and the number of top-tier U.S. funds that are not just increasing their level of investment activity but committing to spending more and more time here on the ground, hiring people, building teams, building a network, and getting to know companies. I think it probably surprises people to know that 19% of all rounds this year will involve at least one U.S. investor in Europe, which is more than double since since the first year we did the report.

I think the other thing, where I come back to this idea that now we have finally convinced a certain group of people about the role that Europe can play, is mainstream institutional investors. I know it is not going to be lost on you, [but] this is going to be another record year for VC fund raising from Europe. And whilst the headline numbers might not be a surprise, I think what should catch people’s attention is that the composition of the LP base here in Europe is now shifting. And finally, there’s an unlocking of institutional investors, [by which] I mean pension funds, funds of funds, insurance companies, sovereign wealth funds, who are committing to European VC at levels that are significantly increased and elevated from where they had been in the past. So, if you just take pension funds, we’re going to see close to a billion dollars invested which is up nearly three fold.

It’s a validation of what’s happening around European tech to see that now coming through and I think is ultimately something that helps to build a foundation for the next five years of success. As much as this is a report that’s looking back, it’s also about trying to understand where things go from here.

With regards to the pension funds, do you think that is driven by the general bullishness towards European tech, or do you think it’s more the macro economic reality that maybe other places where they could put their money aren’t very attractive at the moment?

I think it’s really a reflection that there’s a strong level of belief that European venture as an asset class is an attractive investment opportunity. And that is reflected by the numbers. One of the charts that we’ve got in the report is from Cambridge Associates who do the benchmarking for the VC indices… And when you look back over a 1, 3, 5, or even a 10 year horizon, the performance from European VC is demonstrating that this is a place where for anyone building a diversified portfolio, they should have some allocation. I think it’s fundamentally the strength of the investment opportunity. That is the single biggest driver for why you’re seeing this happen.

I think the biggest thing that Europe has been able to prove is that it can take a great idea and turn it into a great company and that company can scale to not just a billion dollar outcome but to a multi-billion dollar outcome and go all the way through into an IPO or into a large scale acquisition. What you’ve seen happen in 2019 is in part A reflection of what happened last year where it was obviously this record year with Spotify, Adyen, Farfetch, Elastic and others that really showed you can go full cycle from start all the way to finish. And that the magnitude of those outcomes can be at a scale that makes them globally relevant.

Are the pension funds shifting their allocation of VC away from other geographies or are they just doing more VC as a whole?

Powered by WPeMatico