advisors

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I noted some challenges plaguing mental health tech startups. Before that, I wrote about Zoom and Superhuman’s PR disasters.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

Anyway, onto the subject on everyone’s mind this week: SoftBank’s second Vision Fund.

Well into the evening on Thursday, SoftBank announced a target of $108 billion for the Vision Fund 2. Yes, you read that correctly, $108 billion. SoftBank indeed plans to raise even more capital for its sophomore vehicle than it did for the record-breaking debut vision fund of $98 billion, which was majority-backed by the government funds of Saudi Arabia and Abu Dhabi, as well as Apple, Foxconn and several other limited partners.

Its upcoming fund, to which SoftBank itself has committed $38 billion, has attracted investment from the National Investment Corporation of National Bank of Kazakhstan, Apple, Foxconn, Goldman Sachs, Microsoft and more. Microsoft, a new LP for SoftBank, reportedly hopped on board with the Japanese telecom giant as part of a grand scheme to convince the massive fund’s portfolio companies to transition to Microsoft Azure, the company’s cloud platform that competes with Amazon Web Services . Here’s more on that and some analysis from TechCrunch editor Jonathan Shieber.

News of the second Vision Fund comes as somewhat of a surprise. We’d heard SoftBank was having some trouble landing commitments for the effort. Why? Well, because SoftBank’s investments have included a wide-range of upstarts, including some uncertain bets. Brandless, a company into which SoftBank injected a lot of money, has struggled in recent months, for example. Wag is said to be going downhill fast. And WeWork, backed with billions from SoftBank, still has a lot to prove.

Here’s everything else we know about The Vision Fund 2:

On to other news…

WeWork is planning a September listing

The company made headlines again this week after word slipped it was accelerating its IPO plans and targeting a September listing. We don’t know much about its IPO plans yet as we are still waiting on the co-working business to unveil its S-1 filing. Whether WeWork can match or exceed its current private market valuation of $47 billion is unlikely. I expect it will pull an Uber and struggle, for quite some time, to earn a market cap larger than what VCs imagined it was worth months earlier.

The consumer financial app made headlines twice this week. The first time because it raised a whopping $323 million at a $7.6 billion valuation. That is a whole lot of money for a business that just raised a similarly sized monster round one year ago. In fact, it left us wondering, why the hell is Robinhood worth $7.6 billion? Then, in a major security faux pas, the company revealed it has been storing user passwords in plaintext. So, go change your Robinhood password and don’t trust any business to value your security. Sigh.

Another day, another huge fintech round

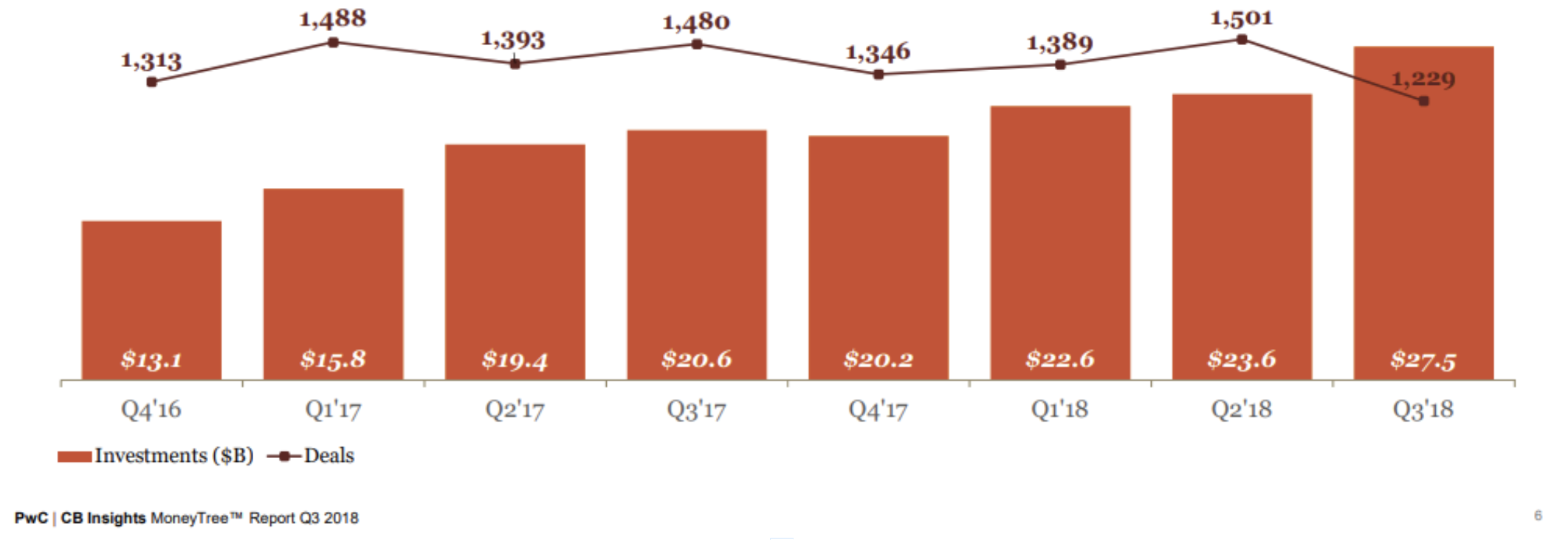

While we’re on the subject on fintech, TechCrunch editor Danny Crichton noted this week the rise of mega-rounds in the fintech space. This week, it was personalized banking app MoneyLion, which raised $100 million at a near unicorn valuation. Last week, it was N26, which raised another $170 million on top of its $300 million round earlier this year. Brex raised another $100 million last month on top of its $125 million Series C from late last year. Meanwhile, companies like payments platform Stripe, savings and investment platform Raisin, traveler lender Uplift, mortgage backers Blend and Better and savings depositor Acorns have also raised massive new rounds this year. Naturally, VC investment in fintech is poised to reach record levels this year, according to PitchBook.

Arianna Huffington, the CEO of Thrive Global, stepped down from Uber’s board of directors this week, a team she had been apart of since 2016. She addressed the news in a tweet, explaining that there were no disagreements between her and the company, rather, she was busy and had other things to focus on. Fair. Benchmark’s Matt Cohler also stepped down from the board this week, which leads us to believe the ride-hailing giant’s advisors are in a period of transition. If you remember, Uber’s first employee and longtime board member Ryan Graves stepped down from the board in May, just after the company’s IPO.

Today I told my fellow @Uber board members that given @Thrive‘s growth, I will no longer be able to give my board duties the attention they deserve, so I will be stepping down. I look forward to watching Uber go from strength to strength! Here is the email I sent to the board: pic.twitter.com/sck0CPLwAV

— Arianna Huffington (@ariannahuff) July 24, 2019

Unity, now valued at $6B, raising up to $525M

Bird is raising a Sequoia-led Series D at $2.5B valuation

SMB payroll startup Gusto raises $200M Series D

Elon Musk’s Boring Company snags $120M

a16z values camping business HipCamp at $127M

An inside look at the startup behind Ashton Kutcher’s weird tweets

Dataplor raises $2M to digitize small businesses in Latin America

While we’re on the subject of amazing TechCrunch #content, it’s probably time for a reminder for all of you to sign up for Extra Crunch. For a low price, you can learn more about the startups and venture capital ecosystem through exclusive deep dives, Q&As, newsletters, resources and recommendations and fundamental startup how-to guides. Here are some of my current favorite EC posts:

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Equity co-host Alex Wilhelm, TechCrunch editor Danny Crichton and I unpack Robinhood’s valuation and argue about scooter startups. Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast and Spotify.

That’s all, folks.

Powered by WPeMatico

Amid calls for a dozen different global cities to replace Silicon Valley — Austin, Beijing, London, New York — nobody has yet nominated “nowhere.” But it’s now a possibility.

There are two trends to unpack here. The first is startups that are fully, or almost fully, remote, with employees distributed around the world. There’s a growing list of significant companies in this category: Automattic, Buffer, GitLab, Invision, Toptal and Zapier all have from 100 to nearly 1,000 remote employees.

The second trend is nomadic founders with no fixed location. For a generation of founders, moving to Silicon Valley was de rigueur. Later, the emergence of accelerators and investors worldwide allowed a wider range of potential home bases. But now there’s a third wave: a culture of traveling with its own, growing support networks and best practices.

You don’t have to look far to find startup gurus and VCs who strongly advise against being remote, much less a nomad. The basic reasoning is simple: Not having a location doesn’t add anything, so why do it? Startups are fragile, so it’s best to avoid any work practice that could disrupt delicate growth cycles.

Powered by WPeMatico

Many founders believe in the myth that the first steps of starting a business are the hardest: Attracting the first investment, the first hires, proving the technology, launching the first product and landing the first customer. Although those critical first steps are difficult, they are certainly not the most difficult on the arduous path of building an iconic company. As early and late-stage funding becomes more abundant, founders and their early VC backers need to get smarter about how to position their companies for a looming valley of death in-between. As we’ll learn below, it’s only going to get much, much harder before it gets easier.

Money will have the look, and heft, of dumbbells as the economic cycle turns. Expect an abundance of small, seed checks at one end, an abundance of massive checks for clear, breakout companies at the other, and a dearth of capital for expanding companies with early proof points and market traction. Read more on how to best prepare for this inevitable future. (Image courtesy Flickr/CircaSassy)

There will be an abundance of capital at the two ends of the startup spectrum. At one end, hundreds of seed and micro VCs, each armed with dozens of $250,000-$1 million checks to write every year, are on the prowl for visionary founders with pedigrees and resumes. At the other end, behemoths like SoftBank, sovereigns, as well “early-stage” firms raising larger funds are seeking breakout companies ready for checks that are in the mid-tens to hundreds of millions. There will be a dearth of capital to grow companies from a kernel of a business, to becoming the clear market-defining leader. In fact, we’re already seeing deal volume decreasing significantly as dollars increase, likely evidence of larger checks going into fewer companies.

Even as the overall number of deals decrease below 2012 levels, the overall dollars invested into startups continue to soar. The 200+ “seed-stage” funds formed since 2012 will continue to chase nascent companies. Meanwhile, the increasing number of mega-funds will seek breakout companies into which to make $100 million+ investments. Companies with early traction seeking ~$20 million to grow will be abundant and have difficulty accessing capital.

Founders should no longer assume that their all-star seed and Series A syndicates will guarantee a successful follow-on financing. Progress on recruiting and product development, though necessary, are no longer sufficient for B-rounds and beyond. Founders should be mindful that investors that specialize in leading $20-50 million rounds will have a plethora of well-funded, well-mentored, well-staffed startups with slick presentations, big visions and some early market traction from which to choose.

Today, there is far more capital chasing fewer quality companies. Fewer breakout companies and fear of missing out is making it easy to raise growth rounds with revenue growth, which may not be scalable or even reflective of an attractive business. This is creating false realities and prompting founders to raise big rounds at high prices — which is fine when there is an over-abundance of capital, but can cripple them when capital later becomes scarce. For example, not long ago, cleantech companies, armed with very preliminary sales, raised massive financings from VCs eager to back winners toward scaling into what they characterized as infinite demand. The reality is that the capital required to meet target economics was far greater and demand far smaller. As the private markets turned, access to cash became difficult and most faltered or were acquired for pennies on the dollar.

There is a likely future where capital grows scarce, and investors take a harder look at the underpinnings of revenue, growth and (dis)economies of scale.

What should startup leadership teams emphasize in an inevitable future where the $30 million rounds will be orders of magnitude harder than their $5 million rounds?

Leadership teams put lots of emphasis on revenue. Unfortunately, revenue that’s not representative of the big vision is probably worse than no revenue at all. Companies are initially seeded with the expectation that the founding team can build and sell something. What needs to be proven is the hypothesis that the company can a) build a special product that b) is inexpensive to convince customers to pay for, and c) that those customers represent a massive market. It should be proven that it is unattractive for customers to switch to the inevitable copycats. It should be clear that over time, customers will pay more for additional features, and the cost of acquiring new customers will go down. Simply selling a product to customers that don’t represent that model is worse than not selling anything at all.

Early founding teams are cognitively diverse individuals that can convince early investors that they can overcome the incredible odds of building a company that until now, shouldn’t have existed. They build a unique product, leveraging unique tools satisfying an unmet need. The early teams need to demonstrate the big vision, and that they can recruit the people that can make that vision a reality. Unfortunately, more founders struggle when it comes to recruiting people that have real experience reducing a technology to practice, executing on a product that customers want and charting the path to expand their market with improving unit economics. There are always exceptions of people that do the above for the first time at startups; however, most of today’s iconic startups knew what kind of talent they needed to execute and succeeded in bringing them on board. Who’s on your team?

The attractive SaaS valuation multiples behoove all founders to apply its metrics to their businesses even if they aren’t really SaaS businesses. Sophisticated later-stage investors see right past that and dismiss numbers associated with metrics that are not representative. Semiconductors are about winning dedicated sockets in growing markets. Design tools are about winning and upselling seats in an industry that’s going to be hooked on those tools. Develop a clear understanding of how your business will be measured. Don’t inundate your investor with numbers; present a concise hypothesis for your unfair advantage in a growing market with your current traction being evidence to back it.

“Pouring fuel on the fire” is a misleading metaphor that leads some into believing that capital can grow any business. That’s just as true as watering a plant with a fire hose or putting TNT in your Corolla’s gas tank: most business models and markets simply are not native to the much-sought-after venture growth profile. In fact, most later-stage startups that fail after raising large amounts of capital fail for this reason. Most markets are conducive to businesses with DIS-economies of scale, implying dwindling margins with scale, which is why many businesses are small, serving local, fragmented markets that technology alone cannot consolidate. How do your unit economics improve over time? What are the efficiencies generated by economies of scale? Is there a real network effect that drives these economies?

Image courtesy Getty Images

I expect today’s resourceful founders to seek partners, whether it’s employees, advisors or investors, to help them answer these questions. Together, these cognitively diverse teams will work together to accelerate past any metaphoric valley and build the iconic companies taking humanity to its fantastic future.

Powered by WPeMatico

Zocdoc founder Cyrus Massoumi and Indiegogo founder Slava Rubin have created a new $30 million fund called Humbition aimed at early stage, founder-led companies in New York.

“The fund is focused on connecting startups with investors and advisors experienced in building and growing successful businesses,” said Rubin.

“We are seeking to fill a void in NYC, where the vast majority of early stage investors have no significant experience building and scaling businesses,” he said. “The fund’s main areas of investment include marketplaces, consumer and health tech. But the primary criteria for investments is high quality founders. The fund is also seeking out mission-driven businesses because the companies that are socially responsible will be the most successful in the coming decades.”

The fund has brought on ClassPass founder Payal Kadakia, Warby Parker founder Neil Blumenthal, Charity: Water CEO and founder Scott Harrison, and Casper founder and CEO Philip Krim as advisors. They have already invested some of the $30 million raise in Burrow, a couch-on-demand service.

“New York City is home to a tremendous number of mission-driven startups that are simply not receiving the same level of support as their peers in the Bay Area. This void presents a unique opportunity for humbition to reach the incredible local talent who need the funding and guidance to build and grow their businesses in New York City,” said Rubin.

Powered by WPeMatico

As his new company, The Players’ Tribune, plots its course toward dominance in the sports media market after its official launch on Tuesday, Derek Jeter gives us his thoughts on his company and the transition from iconic athlete to startup entrepreneur in the email interview below. Since Jeter took his final bow in Yankee pinstripes, the former shortstop has been working to reinvent… Read More

As his new company, The Players’ Tribune, plots its course toward dominance in the sports media market after its official launch on Tuesday, Derek Jeter gives us his thoughts on his company and the transition from iconic athlete to startup entrepreneur in the email interview below. Since Jeter took his final bow in Yankee pinstripes, the former shortstop has been working to reinvent… Read More

Powered by WPeMatico