Accel

Auto Added by WPeMatico

Auto Added by WPeMatico

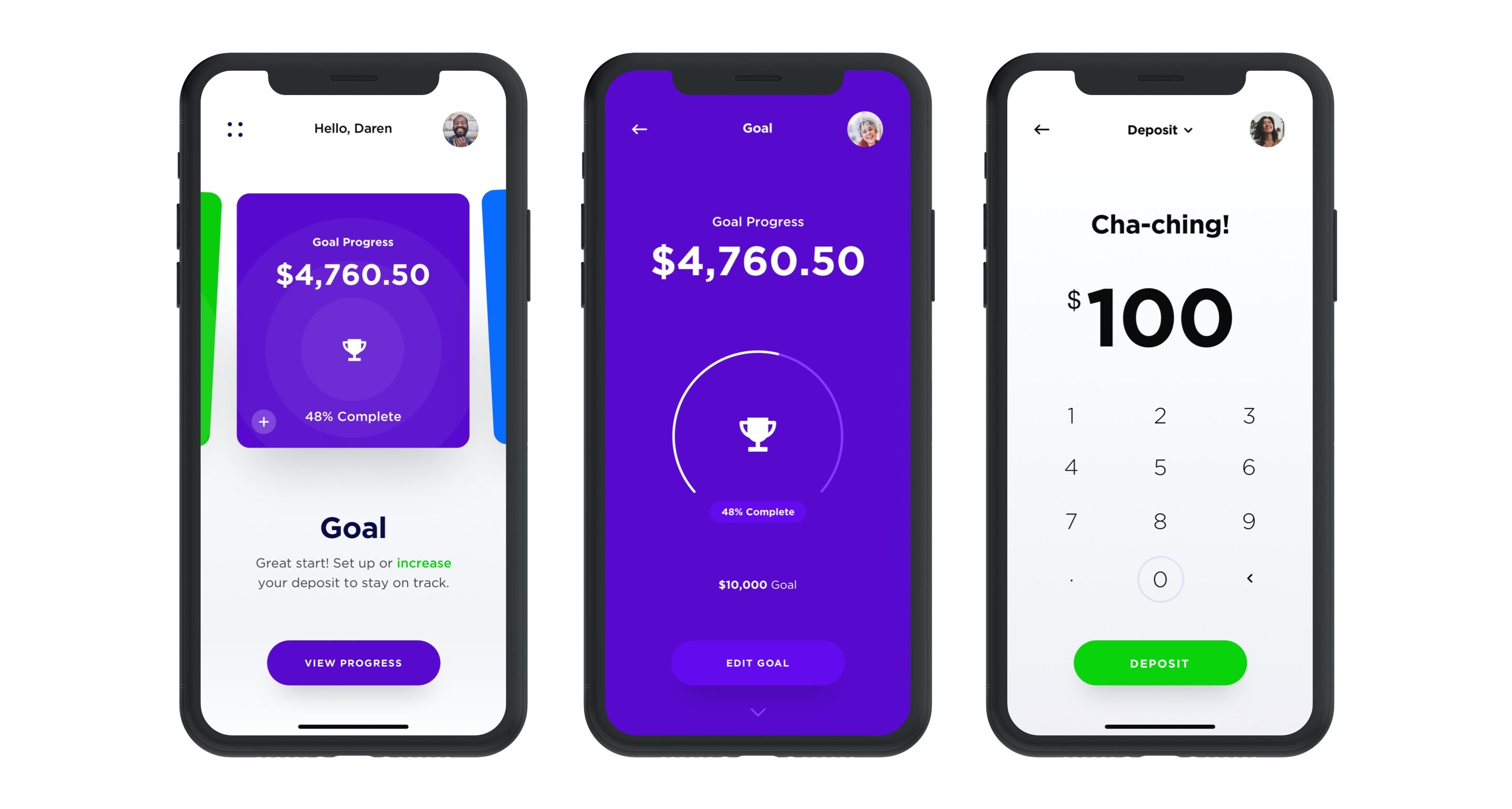

Lower, an Ohio-based home finance platform, announced today it has raised $100 million in a Series A funding round led by Accel.

This round is notable for a number of reasons. First off, it’s a large Series A even by today’s standards. The financing also marks the previously bootstrapped Lower’s first external round of funding in its seven-year history. Lower is also something that is kind of rare these days in the startup world: profitable. Silicon Valley-based Accel has a history of backing profitable, bootstrapped companies, having also led large Series A rounds for the likes of 1Password, Atlassian, Qualtrics, Webflow, Tenable and Galileo (which went on to be acquired by SoFi).

In fact, Galileo founder Clay Wilkes introduced the VC firm to Dan Snyder, Lower’s founder and CEO. The two companies have a few things in common besides being profitable: they were both bootstrapped for years before taking institutional capital and both have headquarters outside of Silicon Valley.

“We were immediately intrigued because Ohio-based Lower echoes both of these themes,” said Accel partner John Locke, who led the firm’s investment in Lower and is taking a seat on the company’s board as part of the investment. “Like Galileo, Lower will be one of the most successful bootstrapped fintech companies globally. The combination of a company built in a nontraditional region across the globe and a bootstrapped company reminds us of [other] companies we have partnered with for a large Series A.”

There were other unnamed participants in the round, but Accel provided the “majority” of the investment, according to Lower.

Snyder co-founded Lower in 2014 with the goal of making the home-buying process simpler for consumers. The company launched with Homeside, its retail brand that Snyder describes as “a tech-leveraged retail mortgage bank” that works with realtors and builders, among others.

In 2018, the company launched the website for Lower, its direct-to-consumer digital lending brand with the mission of making its platform a one-stop shop where consumers can go online to save for a home, obtain or refinance a mortgage and get insurance through its marketplace. This year, it launched the Lower mobile app with a savings account.

Sitting (L to R): Co-founders Dan Snyder, Grayson Hanes

Standing (L to R): Co-founders Mike Baynes, Chris Miller

Not pictured: Robert Tyson; Image credit: Lower

Over the years, Lower has funded billions of dollars in loans and notched an impressive $300 million in revenue in 2020 after doubling revenue every year, according to Snyder.

“Our history is maybe a little atypical of fintech companies today,” he told TechCrunch. “We’ve had a view going back to the start of the company that we wanted to run it profitably. That’s been one of our pillars, so that’s what we’ve done. Also, we all grew up in the mortgage industry, so we saw firsthand the size of the market, but also how broken it was, so we wanted to change it.”

In launching the direct-to-consumer digital lending brand, the company was working to make the homebuying process more “digital, transparent and easier for consumers to access,” Snyder said.

At the same time, the company didn’t want to lose the human touch.

“We tried to design the app flow in a way where you can get as far along as you can in the application but if you want, at any point in time, to talk or chat with someone, we’re available,” Snyder added.

Image Credits: Lower

Lower’s typical customer is the millennial and now Gen Z who’s aspiring to own their first home, according to Snyder.

“They might be thinking, ‘OK, I might be living in an apartment now, but in the next few years I’m going to meet someone and/or have a child and I want to unlock the investment that is a home,’” he told TechCrunch. “And we’ll help them on that journey.”

Lower’s recently launched new app offers a deposit account it’s dubbed “HomeFund.” The interest-bearing, FDIC-insured deposit account offers a 0.75% Annual Percentage Yield and is designed to help consumers save for a home with a “dollar-for-dollar match in rewards” up to the first $1,000 saved, Snyder said.

Lower works with more than 35 major insurance carriers nationally, including Nationwide, Liberty Mutual and Allstate. It has more than 1,600 employees, about half of which are based in Lower’s home state. That’s up from about 650 employees in June of 2020.

Looking ahead, the company plans to add more services and has an “aggressive roadmap” for adding new features to its platform. Today, for example, Lower sells primarily to Fannie Mae and Freddie Mac. And while it services the majority of its loans, like many large lenders, it uses a subservicer. That will change, however, in early 2022, when Lower intends to launch its own native servicing platform.

And while the company intends to continue to run profitably, Snyder said he and his co-founders “think the time is now to gain share.”

“We want to become a global brand, raise money and gain market share,” he added. “We’re going to continue to double down on product and build out our capabilities. We are the best-kept secret in fintech and plan to change that with smart branding, advertising and sponsorships.”

And last but not least, Lower is eyeing the public markets as part of its longer-term roadmap.

“Ultimately, we know we can build a great public company,” Snyder told TechCrunch. “We’re of the scale to be a public company right now, but we’re going to keep our heads down and we’re going to keep building for the next few years and then I think we can be in a spot to be a strong public business.”

Accel’s Locke points out that in the U.S., mortgage and home finance are among the largest financial service markets, and they have primarily been handled by large banks.

“For most consumers, getting a mortgage through these banks continues to be an overly complex, slow-moving process,” Locke told TechCrunch. “We believe by providing consumers a great mobile experience, Lower will gain share from incumbent banks, in the same way that companies like Monzo have in banking or Venmo in payments or Trade Republic and Robinhood in stock trading.”

Powered by WPeMatico

Productivity analytics startup Time is Ltd. wants to be the Google Analytics for company time. Or perhaps a sort of “Apple Screen Time” for companies. Whatever the case, the founders reckon that if you can map how time is spent in a company, enormous productivity gains can be unlocked and money better spent.

It’s now raised a $5.6 million late-seed funding round led by Mike Chalfen, of London-based Chalfen Ventures, with participation from Illuminate Financial Management and existing investor Accel. Acequia Capital and former Seal Software chairman Paul Sallaberry are also contributing to the new round, as is former Seal board member Clark Golestani. Furthermore, Ulf Zetterberg, founder and former CEO of contract discovery and analytics company Seal Software, is joining as president and co-founder.

The venture is the latest from serial entrepreneur Jan Rezab, better known for founding SocialBakers, which was acquired last year.

We are all familiar with inefficient meetings, pestering notifications chat, video conferencing tools and the deluge of emails. Time is Ltd. says it plans to address this by acquiring insights and data platforms such as Microsoft 365, Google Workspace, Zoom, Webex, MS Teams, Slack and more. The data and insights gathered would then help managers to understand and take a new approach to measure productivity, engagement and collaboration, the startup says.

The startup says it has now gathered 400 indicators that companies can choose from. For example, a task set by The Wall Street Journal for Time is Ltd. found the average response time for Slack users versus email was 16.3 minutes, comparing to emails which was 72 minutes.

Chalfen commented: “Measuring hybrid and distributed work patterns is critical for every business. Time Is Ltd.’s platform makes such measurement easily available and actionable for so many different types of organizations that I believe it could make work better for every business in the world.”

Rezab said: “The opportunity to analyze these kinds of collaboration and communication data in a privacy-compliant way alongside existing business metrics is the future of understanding the heartbeat of every company — I believe in 10 years time we will be looking at how we could have ignored insights from these platforms.”

Tomas Cupr, founder and Group CEO of Rohlik Group, the European leader of e-grocery, said: “Alongside our traditional BI approaches using performance data, we use Time is Ltd. to help improve the way we collaborate in our teams and improve the way we work both internally and with our vendors — data that Time is Ltd. provides is a must-have for business leaders.”

Powered by WPeMatico

TechCrunch Disrupt has a long history of bringing leading venture capitalists to the stage to yammer about their industry. Our impending TC Disrupt conference happening on September 21-23 is no different. This time around one of our investor guests is Arun Mathew of Accel, a venture capitalist that you might recall from his recent participation in Webflow’s huge $140 million Series B.

But we aren’t merely asking Mathew out to the event to chat low-code, or SaaS, or simply current intra-venture capital investing dynamics. Instead, he’ll be taking part in our panel on alternative financing (alt-finance) with a few folks that aren’t venture capitalists, but still deploy capital into startups.

Having an Accel partner take part in the panel makes good sense, as the venture firm has an interesting way of approaching bootstrapped companies. Namely that it is willing to show up to pretty large companies and write huge checks. That’s how Accel got into Qualtrics, for example, a deal that worked out pretty well.

But Accel invests from seed through super-late stage, making Mathew the perfect person to bring the venture perspective to the conversation.

The chat should hit on revenue-based financing, other more exotic forms of alt-finance and where the venture world may see capital partnerships, and funding rivalries. Our goal won’t be to incite an argument, but instead to unfold the private capital markets in a manner that helps fans of traditional VC — if there is still such a thing in today’s Tiger Global-led world — and believers in newer methods of capital deployment learn from each other. And so that founders can carve the most reasonable path for themselves as they seek to grow their businesses.

All told it should be a bop and I will see you there!

Powered by WPeMatico

Mental health, and how it is getting addressed, has been one of the major leitmotifs of the past year of pandemic living. COVID-19 not only has led to a lot of people getting ill or worse; it has increased isolation, economic uncertainty and led to a lot of other kinds of disappointments, and that all has had a knock-on effect on our collective and individual state of mind.

Today a startup called Headway, which has been working on building a better way for people to attend to themselves — by way of a three-sided marketplace of sorts, by helping a person to find and afford a therapist via a free-to-use portal, by making it possible for those therapists to accept a wider range of insurance plans and by helping those insurance plans facilitate more therapy appointments for their patient networks — is announcing a major round of funding on the heels of strong growth.

The startup has raised $70 million, money that it will be using to continue expanding its platform with more partnerships, more hiring for its team (it wants to have 300 people this year) and opening in new regions, aiming to be nationwide this year in the U.S. This round, a Series B, has a number of big names attached to it: It is being led by Andreessen Horowitz, with Thrive, GV and Accel also participating. (The latter three are repeat investors: Thrive and GV led its Series A, while Accel led its seed.) This Series B is coming in at a $750 million valuation.

The rapid pace of funding, the backers and that valuation all underscore the timeliness of the concept, and also the traction that Headway is getting for its approach.

When we last covered Headway — it raised $26 million just last November, six months ago — it said it had registered some 1,800 therapists on its platform in the New York metro area, where it is based. Now that number is up to more than 3,000 with its network now covering not just NYC, but also New Jersey, Florida, North Carolina, Texas, Georgia, Michigan, Virginia, Washington, Illinois and Colorado. It has more than 2,000 patients joining the platform each month and has so far helped facilitate 300,000 appointments, with a current average of 30,000 appointments each month. Revenues have in the last year, meanwhile, grown nine-fold.

The approach that Headway is taking — creating not just a vertical search portal for therapists, but building a back-end system to help those therapists grow their business by making it easier for them to accept insurance coverage — comes directly out of the experiences faced by one of the startup’s co-founders.

Andrew Adams, the CEO of Headway, told me last year he came up with the idea after he moved to New York from California several years ago to take a job. In seeking a therapist, he found most unwilling to accept his insurance plan as payment, making getting therapy unaffordable.

This is a very typical problem, he said. Some 70% of therapists do not accept insurance today because it’s too complicated for them to integrate, since about 85% of all therapists happen to be solo practitioners. So something that should be accessible to everyone becomes something typically only used by those who can afford it, or have entered into social care programs that might provide it. But that leaves a massive gap in the middle.

“This is the defining problem in the space,” he said at the time. “Health insurance is built around a medical world dominated by billers and admins, but therapists are small practitioners and don’t have the bandwidth to handle that, so they don’t. So we thought if we could make it easier for them to, they would, and they have.”

And indeed, if you are needing to see a therapist, the very last thing you need or want to be doing is spending your time trying to work out the economics of doing so: You need to be focused on finding someone you feel you can talk to; someone who can help you.

The problem is a huge one. In the U.S. alone it’s estimated that there are some 82 million people who have treatable health conditions. Headway was founded on the premise that most of them currently do not seek that treatment because of cost or accessibility.

A lot of therapy has traditionally been about seeing people in person — and arguably the fact that we’ve had so much reduced contact with people has contributed to mental health issues this past year — but in the event, Headway has definitely adapted to the current climate.

The company says that some 89% of its appointments at the moment are being carried out remotely. This is down from 97% at the peak of the pandemic in the U.S., and has been slowly starting to taper off, the company said. Some of the increased volume, meanwhile, is a direct result of therapists working remotely — they can fit more people in to a daily schedule as a result.

In terms of insurers, the company currently works with Aetna, Cigna, United Healthcare, Oscar and Oxford and says the list will be growing. One interesting detail is that Headway has not only built out a bigger funnel for these insurers in terms of the practitioners they work with and individuals who can subsequently use insurance to pay for therapy, but conversely has served to be a conduit for those insurance groups in bringing more patients through to those therapists, who are now a part of their networks, by way of Headway’s platform.

Headway says that using its system can help a patient get an appointment within five days, versus the the 30-day average you typically face when using an insurance directory.

It’s the kind of scale and “software eating the world” efficiency that has attracted Andreessen Horowitz to backing companies before, with the added detail of this being particularly relevant to the time we are living in.

“By getting the mental health provider community on the same page with insurance companies for the first time, Headway unlocks affordable mental healthcare for millions of Americans,” said Scott Kupor, managing partner at Andreessen Horowitz. “We’re incredibly excited to work alongside the Headway team.” Kupor is also joining Headway’s board with this round.

Cherry Miao, a former partner at Accel and Headway’s lead seed investor, is also joining as head of Finance & Data.

“I’ve been fortunate to work with some of the world’s most influential startups, and know that being part of Headway’s meaningful mission, robust business model, and incredibly talented team is a once-in-a-lifetime opportunity,” she said. “I’m thrilled to be helping rebuild America’s mental healthcare system for access and affordability.”

Powered by WPeMatico

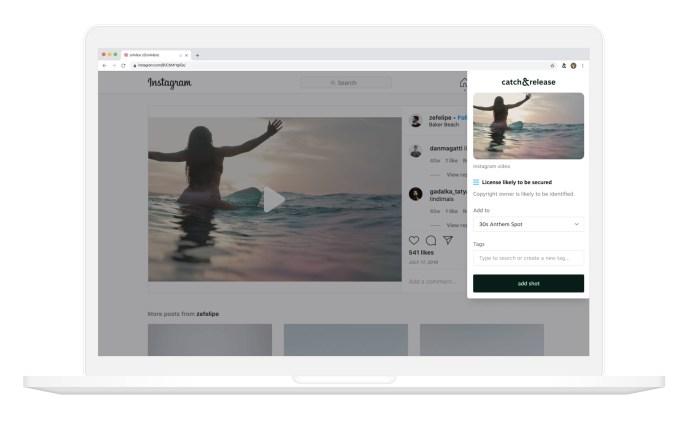

Catch&Release founder and CEO Analisa Goodin told me that she wants to help brands break free from the limitations of stock photography — and that her startup has raised $14 million in Series A funding to achieve that goal.

Goodin explained that the company started out as an image research firm before becoming a product-focused, venture-backed startup in 2015. The Series A was led by Accel (with participation from Cervin Ventures and other existing investors), and it brings Catch&Release’s total funding to $26 million.

Stock media and video services are moving in this direction themselves, for example by introducing their own libraries of user-generated content. Goodin applauded this, and she said Catch&Release isn’t opposed to the use of stock photos — it integrates with these stock marketplaces. At the same time, she suggested that she has a much bigger vision.

“This isn’t just about UGC, this is about tapping into the creative potential of the internet,” she said.

After all, you can now find pretty much any kind of content you can imagine somewhere online, but “a lot of advertising agencies and brands have been trained that if a piece of content comes from the internet, avoid it,” because it’s just “too hard” to figure out how to license it. (And indeed, that’s why I went with a stock photo for the lead image of this post.)

Image Credits: Catch&Release

Catch&Release aims to make that process as simple as possible, first with a browser extension that allows marketers to save any media that they find on the web, anytime they think they might want to use it in their own campaigns (this is the “catch” part of the process). It even presents a “licensability score,” which is a rating based on factors like the person who posted the content, the description and the comments, indicating how likely it is that a marketer will actually be able to license this content.

Then, when someone from a brand or advertising agency decides that they want to use a piece of content, they can send a licensing request with a push of a button (this is the “release”). Catch&Releases also analyzes the content for anything else that needs to be cleared or obscured, such as a company logo.

While we’ve written about other tools for licensing online content, Goodin emphasized that Catch&Release isn’t just about finding photos for a social media campaign. Part of the goal, she said, is to erase the “stigma” around UGC, which now “represents the entire spectrum of culturally relevant content.”

For example, she showed me a Red Lobster commercial that looks like a normal TV ad, but was in fact assembled entirely from footage found online — something that’s been even more useful in the past year, with pandemic-related safety concerns around large shoots. (Catch&Release has also been used to license content for ads promoting TechCrunch’s parent company Verizon.)

Goodin added that the new funding will allow Catch&Release to continue investing in product, engineering and marketing.

“No one has defined the commercial licensing layer for the web,” she said. “What’s got me really excited to build this product is being that layer for the internet, not just for photos and videos, but for writing, art, graphics and building the commercial licensing engine of the web.”

Powered by WPeMatico

Few companies have done better than Scale at spotting a need in the AI gold rush early on and filling that gap. The startup rightly identified that one of the tasks most important to building effective AI at scale — the laborious exercise of tagging data sets to make them usable in properly training new AI agents — was one that companies focused on that area of tech would also be most willing to outsource. CEO and co-founder Alex Wang credits their success since founding, which includes raising over $277 million and achieving break-even status in terms of revenue, to early support from investors including Accel’s Dan Levine.

Accel haș participated in four of Scale’s financing rounds, which is all of them unless you include the funding from YC the company secured as part of a cohort in 2016. In fact, Levine wrote one of the company’s very first checks. So on this past week’s episode of Extra Crunch Live, we spoke with Levine and Wang about how that first deal came together, and what their working relationship has been like in the years since.

Scale’s story starts with a pivot, and with a bit of rule-breaking, too — Wang went off the typical YC book by speaking to investors prior to demo day when Levine cold-emailed him after seeing Scale on Product Hunt. The Product Hunt spot wasn’t planned, either — Wang was as surprised to see his company there as anyone else. But Levine saw the kernel of something with huge potential, and despite being a relative unknown in VC at the time, didn’t want to let the opportunity pass him, or Wang, by.

Both Wang and Levine were also able to provide some great feedback on decks submitted to our regular Pitch Deck Teardown segment, despite the fact that Levine actually never saw a pitch deck from Wang before investing (more on that later). If you’d like your pitch deck reviewed by experienced founders and investors on a future episode, you can submit your deck here.

As mentioned, Levine and Accel’s initial investment in Scale came from a cold email sent after the company appeared on Product Hunt. Wang said the team had just put out an early version of Scale, and then noticed that it was up on Product Hunt — it was submitted by someone else. The community response was encouraging, and it also led to Levine reaching out via email.

“One of the side effects of that, one of the outcomes, was that we got this cold email from Dan,” he said. “We really knew nothing about Dan until his cold email. So like many great stories that started with a bold, cold email. And we were pretty stressed about it at the time, because in YC, they tell you pretty definitively, ‘Hey, don’t talk to a VC during the batch,’ and we were squarely in the middle of the batch.”

Wang and the team were so nervous that they even considered “ghosting” Dan despite his obvious interest and the prestige of Accel as an investment firm. In the end, they decided to “go rogue” and respond, which led to a meeting at the Accel offices in Palo Alto.

Powered by WPeMatico

CaptivateIQ, which has developed a no-code platform to help companies design customized sales commission plans, has raised $46 million in a Series B round led by Accel.

Existing backers Amity, S28 Capital, Sequoia and Y Combinator also participated in the financing, which brings the San Francisco-based company’s total raised to $63 million since its 2017 inception.

CaptivateIQ must be doing something right. While it is not yet profitable, the startup’s revenue has grown 600% year-over-year. To date, it has processed more than $2 billion in commissions on its platform across hundreds of enterprise customers, including Affirm, TripActions, Udemy, Intercom, Newfront Insurance and JMAC Lending.

“A big part of our growth is that we can help any company that offers a performance-based compensation plan, so we don’t have any restrictions with the types of businesses we work with,” said co-CEO Mark Schopmeyer. “We typically see conversations start with teams that have a minimum of 25 sales people, though we easily serve enterprises and public companies as well.”

The number of payees — defined as someone receiving a payout in CapitvateIQ’s system — was up four times in December 2020 from the year prior. Plus, the company had “back-to-back record months” from September through the end of the year in 2020, according to Schopmeyer.

He, co-CEO Conway Teng and CTO Hubert Wong founded CaptivateIQ after coming out of Y Combinator’s Winter 2017 cohort.

Left to right: CaptivateIQ co-founders Hubert Wong, Mark Schopmeyer and Conway Teng. Image Credits: CaptivateIQ

The company touts its SaaS platform as a combination of the familiarity of spreadsheets with the scalability and performance of software, so that users can configure any commission plan “entirely on their own,” according to Teng.

“Calculating commissions is really complicated and mission-critical — think of it like a very complicated form of payroll — each company has a unique commission plan that involves a lot more calculations and data than your typical salary payroll math,” Teng said. “Also, in recent years, companies have access to more data than ever, giving them room to incentive employees on more performance metrics.”

Today, CaptivateIQ has 90 employees, more than triple what it did one year ago.

In 2020, the startup saw a bump in the number of non-high-technology companies buying its software, and as a result, CaptivateIQ is going to increase its efforts into those other verticals, according to Teng. So far, it has found success in particular in financial services, manufacturing and business services, among other sectors.

The pandemic served as a tailwind to its business. Sales teams generally rely on in-person interactions to stay productive, Schopmeyer points out. Without those activities over the past year, “having the right incentives in place became ever more critical as companies required new ways to motivate teams during the shift to remote work.”

“We saw our product usage skyrocket at the beginning of the pandemic as businesses quickly adjusted incentives, team quotas, SPIFs and other components of their comp plans to stay competitive,” he said.

The company plans to use its new capital to improve upon the user experience. Specifically, Teng said, it plans to introduce “more powerful data transformations, a richer set of formulas and off-the-shelf templates.”

Another goal is to automate and streamline the commissions process from beginning to end, he added. The startup is expanding its data integrations to support “all major data systems” and introducing new dashboarding capabilities. It’s also enhancing existing collaboration workflows around approvals, inquiries and contracts.

Looking ahead, CaptivateIQ is exploring the potential of applying its technology to solve for use cases outside the world of commissions — something that it says its customers are already doing.

“It’s exciting to see what people have been building, and we’re looking forward to enabling new solutions as we continue to release more of our core technology platform,” Teng said.

Accel Partner Ben Fletcher said the pain point of calculating and reporting sales commissions kept coming up among portfolio companies, with CaptivateIQ frequently referenced. Those companies, he said, tried more enterprise-grade solutions — “spending hundreds of thousands on implementation to ultimately find that their products did not work.” They also tried other newer tools that also just didn’t work well.

“As we dug in and talked with more and more customers, it was abundantly clear — CaptivateIQ was the best product in the space,” Fletcher said.

Besides ease of use, the fact that CaptivateIQ is a no-code tool, is a big deal to Accel.

“Similar to UIPath, Webflow, and Ada, CaptivateIQ is able to bring the power of customer development and automation to an easy to use, drag-and-drop product,” Fletcher said.

Powered by WPeMatico

Over the course of their careers, Alex Bovee and Paul Querna realized that while the use of SaaS apps and cloud infrastructure was exploding, the process to give employees permission to use them was not keeping up.

The pair led Zero Trust strategies and products at Okta, and could see the problem firsthand. For the unacquainted, Zero Trust is a security concept based on the premise that organizations should not automatically trust anything inside or outside its perimeters and, instead must verify anything and everything trying to connect to its systems before granting access.

Bovee and Querna realized that while more organizations were adopting Zero Trust strategies, they were not enacting privilege controls. This was resulting in delayed employee access to apps, or to the over-permissioning employees from day one.

Last summer, Bovee left Okta to be the first virtual entrepreneur-in-residence at VC firm Accel. There, he and Accel partner Ping Li got to talking and realized they both had an interest in addressing the challenge of granting permissions to users of cloud apps quicker and more securely.

Recalls Li: “It was actually kind of fortuitous. We were looking at this problem and I was like ‘Who can we talk to about the space?’ And we realized we had an expert in Alex.”

At that point, Bovee told Li he was actually thinking of starting a company to solve the problem. And so he did. Months later, Querna left Okta to join him in getting the startup off the ground. And today, ConductorOne announced that it raised $5 million in seed funding in a round led by Accel, with participation from Fuel Capital, Fathom Capital and Active Capital.

ConductorOne plans to use its new capital to build what the company describes as “the first-ever identity orchestration and automation platform.” Its goal is to give IT and identity admins the ability to automate and delegate employee access to cloud apps and infrastructure, while preserving least-privilege permissions.

“The crux of the problem is that you’ve got these identities — you’ve got employees and contractors on one side and then on the other side you’ve got all this SaaS infrastructure and they all have sort of infinite permutations of roles and permissions and what people can do within the context of those infrastructure environments,” Bovee said.

Companies of all sizes often have hundreds of apps and infrastructure providers they’re managing. It’s not unusual for an IT helpdesk queue to be more than 20% access requests, with people needing urgent access to resources like Salesforce, AWS or GitHub, according to Bovee. Yet each request is manually reviewed to make sure people get the right level of permissions.

“But that access is never revoked, even if it’s unused,” Bovee said. “Without a central layer to orchestrate and automate authorization, it’s impossible to handle all the permissions, entitlements and on- and off-boarding, not to mention auditing and analytics.”

ConductorOne aims to build “the world’s best access request experience,” with automation at its core.

“Automation that solves privilege management and governance is the next major pillar of cloud identity,” Accel’s Li said.

Bovee and Querna have deep expertise in the space. Prior to Okta, Bovee led enterprise mobile security product development at Lookout. Querna was the co-founder and CTO of ScaleFT, which was acquired by Okta in 2018. He also led technology and strategy teams at Rackspace and Cloudkick, and is a vocal and active open-source software advocate.

While the company’s headquarters are in Portland, Oregon, ConductorOne is a remote-first company with 10 employees.

“We’re deep in building the product right now, and just doing a lot of customer development to understand the problems deeply,” Bovee said. “Then we’ll focus on getting early customers.”

Powered by WPeMatico

Swiggy has raised about $800 million in a new financing round, the Indian food delivery startup told employees on Monday, as it looks to expand its business in the country quarters after the startup cut its workforce to navigate the pandemic.

In an email to employees, first reported by Times of India journalist Digbijay Mishra, Swiggy co-founder and chief executive Sriharsha Majety said the startup had raised about $800 million from new investors, including Falcon Edge Capital, Goldman Sachs, Think Capital, Amansa Capital and Carmignac, and existing investors Prosus Ventures and Accel.

“This fundraise gives us a lot more firepower than the planned investments for our current business lines. Given our unfettered ambition though, we will continue to seed/experiment new offerings for the future that may be ready for investment later. We will just need to now relentlessly invent and execute over the next few years to build an enduring iconic company out of India,” wrote Majety in the email obtained by TechCrunch.

Majety didn’t disclose the new valuation of Swiggy, but said the new financing round was “heavily subscribed given the very positive investor sentiments towards Swiggy.” According to a person familiar with the matter, the new round valued Swiggy at over $4.8 billion $4.9 billion. The startup has now raised about $2.2 billion to date.

Swiggy had raised $157 million last year at about $3.7 billion valuation. That investment is not part of the new round, a person familiar with the matter told TechCrunch.

He said the long-term goal for the startup, which competes with heavily-backed Zomato and new entrant Amazon, is to serve 500 million users in the next 10-15 years, pointing to Chinese food giant Meituan, which had 500 million transacting users last year and is valued at over $100 billion.

“We’re coming out of a very hard phase during the last year given Covid and have weathered the storm, but everything we do from here on needs to maximise the chances of our succeeding in the long-term,” wrote Majety.

Swiggy last year eliminated some jobs — so did Zomato — and scaled down its cloud kitchen efforts as it attempted to stay afloat during the pandemic, which had prompted New Delhi to enforce a months-long lockdown.

Monday’s reveal comes amid Zomato raising $910 million in recent months as the Gurgaon-headquartered firm prepares for an IPO this year. The last tranche of investment valued Zomato at $5.4 billion. During its fundraise, Zomato said it was raising money partially to fight off “any mischief or price wars from our competition in various areas of our business.”

A third player, Amazon, also entered the food delivery market in India last year, though its operations are still limited to parts of Bangalore.

At stake is India’s food delivery market, which analysts at Bernstein expect to balloon to be worth $12 billion by 2022, they wrote in a report to clients earlier this year. Zomato currently leads the market with about 50% market share, Bernstein analysts wrote.

“We find the food-tech industry in India to be well positioned to sustained [sic] growth with improving unit economics. Take-rates are one of the highest in India at 20-25% and consumer traction is increasing. Market is largely a duopoly between Zomato and Swiggy with 80%+ share,” wrote analysts at Bank of America in a recent report, reviewed by TechCrunch.

“The food delivery business is the strongest it’s ever been, and we’re now well on our way to drive continued growth over the next decade. In addition, some of our new bets like Instamart [grocery delivery business] are showing amazing promise while we’ve also made strides in setting up some of our other adjacencies for liftoff very soon.”

Powered by WPeMatico

You might expect that a startup that makes community building software would be thriving during a pandemic when it’s so difficult for us to be together. And Bevy, a company whose product powers community sites like Salesforce Trailblazers and Google Developers announced it has raised a $40 million Series C this morning, at least partly due to the growth related to that dynamic.

The round was led by Accel with participation from Upfront Ventures, Qualtrics co-founder Ryan Smith and LinkedIn, but what makes this investment remarkable is that it included 25 Black investors representing 20% of the investment.

One of those investors, James Lowery, who is a management consultant and entrepreneur, and was the first Black employee hired at McKinsey in 1968, sees the opportunity for this approach to be a model to attract investment from other under-represented groups.

“I know for a fact because of my friendship and my network that there are a lot of people, if they had the opportunity to invest in opportunities like this, they will do it, and they have the money to do it. And I think we can be the model for the nation,” Lowery said.

Unfortunately, there has been a dearth of Black VC investment in startups like Bevy. In fact, only around 3% of venture capitalists are Black and 81% of VC firms don’t have a single Black investor.

Kobie Fuller, who is general partner at investor Upfront Ventures, a Bevy board member and runs his own community called Valence, says that investments like this can lead to a flywheel effect that can lead to increasing Black investment in startups.

“So for me, it’s about how do we get more Black investors on cap tables of companies early in their lifecycle before they go public, where wealth can be created. How do we get key members of executive teams being Black executives who have the ability to create wealth through options and equity. And how do we also make sure that we have proper representation on the boards of these companies, so that we can make sure that the CEOs and the C suite is held accountable towards the diversity goals,” Fuller said.

He sees a software platform like Bevy that facilitates community as a logical starting point for this approach, and the company needs to look like the broader communities it serves. “Making sure that our workforce is appropriately represented from a perspective of having appropriate level of Black employees to the board to the actual investors is just good business sense,” he said.

But the diversity angle doesn’t stop with the investor group. Bevy CEO and co-founder Derek Anderson says that last May when George Floyd was killed, his firm didn’t have a single person of color among the company’s 27 employees and not a single Black investor in his cap table. He wanted to change that, and he found that in diversifying, it not only was the right thing to do from a human perspective, it was also from a business one.

“We realized that if we really started including people from the Black and brown communities inside of Bevy that the collective bar of a talent was going to go up. We were going to look from a broader pool of candidates, and what we found as we’ve done this is that as the culture has started to change, the customer satisfaction is going up, our profits and our revenues — the trajectory is going up — and I see this thing is completely correlated,” Anderson said.

Last summer the company set a two year goal to get to 20% of employees being Black. While the number of employees is small, Bevy went from zero to 5% in June, and 10% by September. Today it is just under 15% and expects to hit the 20% goal by summer, a year ahead of the goal it set last year.

Bevy grew out of a community called Startup Grind that Anderson started several years ago. Unable to find software to run and manage the community, he decided to build it himself. In 2017, he spun that product into a separate company that became Bevy, and he has raised $60 million, according to the company.

In addition to Salesforce and Google, other large enterprises are using Bevy to power their communities and events, including Adobe, Atlassian, Twilio, Slack and Zendesk.

Today, the startup is valued at $325 million, which is 4x the amount it was valued at when it raised its $15 million Series B in May 2019. It expects to reach $30 million in ARR by the end of this year.

Powered by WPeMatico