500 startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Servicing one’s car personally is a time-consuming, expensive and painstaking process. It’s a cycle that can lead to more expensive repairs and safety issues down the line, and no car owner likes that.

Egypt and Dubai-based auto tech startup Odiggo is a platform addressing this problem. It allows car owners to get the help they need by finding car services and parts suppliers from providers around them. Then for the suppliers, it increases their sales and reaches more customers without necessarily spending on marketing.

Odiggo is part of the current YC Summer batch and has secured a $2.2 million seed round before Demo Day. The rosters of existing investors participating in the round are Y Combinator, 500 Startups, and Plug and Play Ventures. Regional VCs like Seedra Ventures, LoftyInc Capital, and Essa Al-Saleh (CEO of Volta-Tucks) also took part.

Ahmed Omar and Ahmed Nasser launched Odiggo in December 2019. The company operates a marketplace that connects car owners with service providers who can solve their problems, from servicing and repair to washing and maintenance. A commission-based model is used and Odiggo charges the car suppliers 20% commission on every transaction.

Over 50,000 car owners across three markets — Egypt, the UAE and Saudi Arabia — use Odiggo. The company also works directly with over 300 merchants. It claims merchant numbers have grown 40% month-on-month while its user base has increased 200% since the start of the pandemic.

“We believe we are at a watershed moment. It is incredible that since COVID hit, Odiggo has experienced over 10 times growth in the last year,” said co-founder Omar.

CEO Omar said with this new round, Odiggo’s priority will be to attain consistent growth while expanding its team across the UEA, Saudi Arabia and Egypt.

L-R: Ahmed Nassir (co-founder) & Ahmed Omar (co-founder and CEO)

He adds that since Odiggo taps into a mix of data sources — including car metrics and internal software, it will use that same information to provide more product offerings.

Odiggo will use part of the funding to continue developing its tech and dashboard software, he said.

“For example, the platform would be hooked up to the car owner’s vehicle and link the vehicle to the marketplace and provide frequent updates of your vehicle condition so you’ll be informed if the tires are low, the oil needs changing, or if a service is required.”

The pandemic has upended the mobility and logistics sectors, especially in MENA, making players like Odiggo gain much visibility from investors. In an industry today worth over $61 billion in the Middle East and Africa alone, Odiggo is looking to become a market leader. It has even more lofty plans to go public in the next three years.

“We are also aiming to be fully focused on spending more on our product and technology, as building an ecosystem to monetize requires more capital. Our target is to go for IPO by 2024 and achieve one billion services booked, and this requires a lot of network effects, infrastructure and technology,” the CEO said.

“We aim to be the first $100 billion company coming out of the region,” added Nasser.

Some of its investors, Idris Ayodeji Bello, managing partner at LoftyInc, and Essa Al-Saleh, are onboard with the startup’s plan despite early days.

“We are excited to back Odiggo through our Afropreneurs Funds in its quest to transform the automotive parts market and provide superior service to clients, starting from MENA. The leadership team of Omar and Nasser, supported by the rest of the employees, have been a joy to work with and we are on a countdown to the IPO,” said Bello in a statement.

Powered by WPeMatico

Canopy Servicing announced this morning it recently closed a $15 million Series A. The startup sells software to fintechs and others, allowing customers to create loan programs and service the resulting products.

The company raised a $3.5 million seed round in 2020. Canaan led its Series A, with participation from Homebrew, Foundation and BoxGroup, among others. Per Canopy, its valuation grew by 5x from its seed round to its Series A.

The company has raised $18.5 million to date.

So far this reads much like any other post announcing a new startup funding round, kicking off with an array of information concerning the round and who chipped into the transaction. Next, we’d probably note the competitors, growth and what investors in the company in question have to say about their recent purchase. This morning, however, I want to riff a bit on the future of fintech and how the financial tech stack of the future may be built.

TechCrunch chatted with Canopy CEO Matt Bivons last week. He has an interesting take on where fintech is headed. Let’s discuss it and work through what Canopy does.

As with many startups, Canopy was built to scratch an itch. Bivons had run into issues regarding loan servicing in prior jobs. He went on to found a startup that aimed to build a student credit card. But after working on that project, Bivons and co-founder Will Hanson pivoted the company to a B2B-focused concern building loan servicing technology.

Behind the decision was market research undertaken by the Canopy crew that uncovered that a great number of fintech startups wanted to get into the credit market. That makes sense; credit products can provide far more attractive economics to fintech startups than, say, checking and savings accounts. Knowing that loan servicing was a bear and a half to manage, Canopy decided to focus on it.

Bivons framed Canopy as a modern API for loan servicing that can be used to create and manage loans at any point in their lifecycle. He noted that what the startup is doing is akin to what several successful fintech companies have done, namely taking a piece of the fintech world and making it better for developers.

This is where Bivons’ view of the future of fintech products comes into play. According to the CEO, in the future, companies will not buy a monolithic financial technology stack. Instead, he thinks, they will buy the best API for each slice of the fintech world that they need to implement. This matters because we could argue that Canopy is targeting too small a product space. Not that its market isn’t large — debt and its servicing are massive problem spaces — but seeing a company find a niche to focus on makes more sense when its leaders expect focused fintech products to win out over large bundles of services.

Bivons added that much of the fintech focus of the last five years has been on debit, citing Chime, Step and Greenlight as examples. The next decade, he said, is going to focus on credit products. That would be good news for Canopy.

Canopy co-founders via the company. CTO Will Hanson (left) and CEO Matt Bivons (right).

Critically, and for the finance nerds out there, Bivons told TechCrunch that its loan servicing technology does not require the company to take on any credit risk, and that it has gross margins of around 90%. I never trust a too-round number, but the figure indicates that what Canopy has built could grow into an attractive business.

Today, Canopy is a traditional SaaS, though Bivons said that it wants to move toward usage-based pricing in time. Its service costs around 50 cents per account per month, or around $6 per year in its current form. Today, around 40% of Canopy’s customers are seed and Series A-scale startups, though Bivons noted that it is moving up the customer size chart over time.

The resulting growth is impressive. Canopy’s customer count grew 4.5x from February to May of 2021. Of course, Canopy is a young company, so its overall customer base could not have been massive at the start of the year. Still, that’s the sort of growth that makes investors sit up and pay attention, making the Canopy Series A somewhat unsurprising.

Fintech growth doesn’t seem to be slackening much, meaning that the market for what Canopy is selling should expand. Provided that its view that best-of-breed, more particular fintech products will beat larger stacks in the market, it could have an interesting trajectory ahead of it. And now that it has raised its Series A, we can start to annoy it with more concrete questions about its growth from here on out.

Powered by WPeMatico

Una Brands’ co-founders (from left to right): Tobias Heusch, Kiren Tanna and Kushal Patel. Image Credits: Una Brands

One of the biggest funding trends of the past year is companies that consolidate small e-commerce brands. Many of the most notable startups in the space, like Thrasio, Berlin Brands Group and Branded Group, focus on consolidating Amazon Marketplace sellers. But the e-commerce landscape is more fragmented in the Asia-Pacific region, where sellers use platforms like Tokopedia, Lazada, Shopee, Rakuten or eBay, depending on where they are. That is where Una Brands comes in. Co-founder Kiren Tanna, former chief executive officer of Rocket Internet Asia, said the startup is “platform agnostic,” searching across marketplaces (and platforms like Shopify, Magento or WooCommerce) for potential acquisitions.

Una announced today that it has raised a $40 million equity and debt round. Investors include 500 Startups, Kingsway Capital, 468 Capital, Presight Capital, Global Founders Capital and Maximilian Bitner, the former CEO of Lazada who currently holds the same role at secondhand fashion platform Vestiaire Collective.

Una did not disclose the ratio of equity and debt in the round. Like many other e-commerce aggregators, including Thrasio, Una raised debt financing to buy brands because it is non-dilutive. The round will also be used to hire aggressively in order to evaluate brands in its pipeline. Una currently has teams in Singapore, Malaysia and Australia and plans to expand in Southeast Asia before entering Taiwan, Japan and South Korea.

Tanna, who also founded Foodpanda and ZEN Rooms, launched Una along with Adrian Johnston, Kushal Patel, Tobias Heusch and Srinivasan Shridharan. He estimates that there are more than 10 million third-party sellers spread across different platforms in the Asia-Pacific.

“Every single seller in Asia is looking at multiple platforms and not just Amazon,” Tanna told TechCrunch. “We saw a big gap in the market where e-commerce is growing very quickly, but players in the West are not able to look at every platform, so that is why we decided to focus on APAC, launch the business there and acquire sellers who are selling on multiple platforms.”

Una looks for brands with annual revenue between $300,000 to $20 million and is open to many categories, as long as they have strong SKUs and low seasonality (for example, it avoids fast fashion). Its offering prices range from about $600,000 to $3 million.

Tanna said Una will maintain acquisitions as individual brands “because what’s working, we don’t change it.” How it adds value is by doing things that are difficult for small brands to execute, especially those run by just one or two people, like expanding into more distribution channels and countries.

“For example, in Indonesia there are at least five or six important platforms that you should be on, and many times the sellers aren’t doing that, so that’s something we do,” Tanna explained. “The second is cross-border in Southeast Asia, which sellers often can’t do themselves because of regulations around customs, import restrictions and duties. That’s something our team has experience in and want to bring to all brands.”

Amazon FBA roll-up players have the advantage of Amazon Marketplace analytics that allow them to quickly measure the performance of brands in their pipeline of potential acquisitions. Since it deals with different marketplaces and platforms, Una works with much more fragmented sources of data for revenue, costs, rankings and customer reviews. To scale up, the company is currently building technology to automate its valuation process and will also have local teams in each of its markets. Despite working with multiple e-commerce platforms, Tanna said Una is able to complete a deal within five weeks, with an offer usually happening within two or three days.

In countries where Amazon is the dominant e-commerce player, like the United States, many entrepreneurs launch FBA brands with the goal of flipping them for a profit within a few years, a trend that Thrasio and other Amazon roll-up startups are tapping into. But that concept is less common in Una’s markets, so it offers different team deals to appeal to potential sellers. Though Una acquires 100% of brands, it also does profit-sharing models with sellers, so they get a lump sum payment for the majority of their business first, then collect more money as Una scales up the brand. Tanna said Una usually continues working with sellers on a consulting basis for about three to six months after a sale.

“Something that Amazon players know very well is that they can find a product, sell it for four to five years, and then ideally make a multi-million deal exit and build another product or go on holiday,” said Tanna. “That’s something Asian sellers are not as familiar with, so we see this as an education phase to explain how the process works, and why it makes sense to sell to us.”

Powered by WPeMatico

In a year marred by the coronavirus pandemic, it seems that early-stage startups on the African continent are continuing to see some notable growth, both in terms of their business and from investors looking to back them.

Microtraction, an early-stage venture capital firm based in Lagos, Nigeria, saw funding nearly quadruple for its portfolio.

In a review of the year published last week, the firm noted that 21 companies in its portfolio have raised more than $33 million in funding. This represents nearly four-fold growth over a year ago, when its portfolio raised $6 million (and just $3 million in 2018). The companies’ combined valuation stands at more than $147 million, according to the firm.

Founded by Yele Bademosi in 2017, Microtraction arrived on the continent’s early-stage investment scene with all intent to be “the most accessible and preferred source of pre-seed funding for African tech entrepreneurs.”

Bademosi, who returned to Nigeria from the U.K. in 2015, worked as the general manager for Starta Africa, an online community for African tech entrepreneurs. After his stint there, he saw the need to plug the gap of early-stage funding in Nigeria and the continent at large with Microtraction.

Microtraction does not specify the size of its fund, but what is more clear is that it has attracted a great deal of attention and has built a strong network in part because of who backs it.

Michael Seibel, the CEO of Y Combinator, is a global advisor and an investor in the firm, and so is Andy Volk, the head of ecosystem for Google Sub-Saharan Africa. Other investors include Pave Investments and U.S.-based angel investor Chris Schultz.

Being entrepreneurs in the past, some of these investors know what it takes to build a startup in the U.S. But it’s completely different in Africa. With no on the ground knowledge as to which startups to fund but an interest to do so, for portfolio diversification and other personal reasons, Microtraction and a few other early-stage investors present the best bets to accomplish this goal.

At first, Microtraction’s standard deal was to offer portfolio startups $15,000 in exchange for a 7.5% equity. But as a sign of how the market is firming up, that changed last year, and now the firm invests $25,000 for 7% equity.

Microtraction revealed that it accepted more than 500 applications from startups in Nigeria, Ghana, Zambia and Mauritius in its first full year of operation (though, just eight of those companies got investments).

The introductory batch was all Nigerian: four fintech startups — Cowrywise, Riby, Wallets Africa and ThankUCash; a crypto-exchange startup, BuyCoins; a SaaS platform, Accounteer; an edtech startup, Schoolable; and healthtech startup, 54gene.

2019 saw the local VC firm invest in six companies. This time there was a representative outside Nigeria — Ghanaian fintech startup Bitsika. The Nigerian startups included social commerce startup Sendbox; events startup Festival Coins; and communications-as-a-service platform Termii. The rest were unannounced.

Last year (the one this latest review covers), Microtraction announced seven startups. The latest selection includes Nigerian fintech startups Evolve Credit and Chaka; edtech startup Gradely; bus-hailing platform PlentyWaka; and Kenyan credit data marketplace CARMA.

Of the total investments raised in 2019 and 2020, 54gene contributed more than half of those numbers by raising $4.5 million in seed and a $15 million Series A investment. With an ingenious solution to solve the underrepresentation of African genomics data in global genomics research, 54gene got accepted into the winter batch in January 2019, the same month it officially launched.

Excluding 54gene, there were six other African-focused startups in the YC W19 batch. Two out of the six, Schoolable and Wallets Africa, were Microtraction portfolio companies. Others accepted into YC before and after include BuyCoins, Cowrywise, Termii and two unannounced startups.

Microtraction-backed ThankUCash and a second unannounced startup have also joined cohorts at 500 Startups. On the other hand, Festival Coins is the only startup to be selected into Google for Startups Accelerator. With all accounted for, 11 out of the 21 startups are either backed by Y Combinator, 500 Startups or Google for Startups.

The Microtraction team with founding partner, Yele Bademosi (far right). Image Credits: Microtraction

Getting into these global accelerators is a surefire way to receive follow-up investment, ranging from $125,000 to $150,000. From the outside in, startups see Microtraction and other early-stage VC firms like Ventures Platform as a means to that end. There have also been arguments that these firms build startups to be “YC or any global accelerator ready.”

However, Dayo Koleowo, a partner at Microtraction alongside Chidinma Iwueke, debunks it saying there’s no formula behind the numbers we see. He believes YC and other accelerators share the same fundamentals with Microtraction, which revolves around the team, the market and traction.

“We love super technical teams that understand the industry they are in and are likely to succeed without us. We are always looking for companies that are solving huge problems that a lot of people face,” he told TechCrunch. “Also, the tech and startup world moves fast, so we like teams who understand that and can show in real-time that they can execute. I believe that these global accelerators look for these same things.”

Typically, YC and other accelerators may perform extended due diligence and risk assessments before cutting cheques for any African startup without a local backer. Koleowo points out that this might be why Microtraction portfolio companies get accepted quicker. “The icing on the cake is that there is a level of de-risking that has been done by Microtraction and other local investors on the ground before these global accelerators step in,” he added.

That said, there’s no denying the significance of Microtraction’s advisory board in playing a part as to why half the firm’s portfolio are in global accelerators. Besides the names mentioned earlier, some of its past advisors included Lexi Novitske, former PIO at Singularity Investments; Dotun Olowoporoku, VC at Novastar Ventures; and Monique Woodward, ex-venture partner at 500 Startups.

And with the growing trends of globalization, plus the acceptance of a more decentralised approach to building and operations in the tech industry because of COVID-19, it’s a trend that might continue for a while.

Powered by WPeMatico

Today 500 Startups hosted a virtual demo day for its 26th batch of startups, a group of companies that TechCrunch covered back in February.

500 is not the only accelerator that moved its traditional investor pitch event online; Y Combinator made a similar move after efforts to flatten the spread of COVID-19 required changes that made its traditional demo day setup temporarily impossible.

In addition to hosting a few dozen startup pitches today, 500 also explained changes to its own format and provided notes on the current state of the venture market.

Regarding how 500 Startups is shaking up how it handles its accelerator, the group intends to pivot to a rolling-admissions setup that will give participants more flexibility; the group will still hold two demo days each year — TechCrunch has more on the changes here.

Regarding the venture market, 500 Startups said venture capital’s investment pace could slow for several months. This seems likely, given how the economy has taken body blows in recent weeks as huge swaths of the world’s economy shut down. What advice did 500 have in the face of the new world? What you’d expect: startups should cut burn and focus on customers.

Got all that? OK, let’s talk about our favorite companies from the current 500 cohort.

Powered by WPeMatico

The founders of Seattle-based Modus cold-emailed Pete Flint, the founder of Trulia and a current managing partner at the venture capital firm NFX, for months, to no avail. In a last-ditch effort, Alex Day, Jai Sim and Abbas Guvenilir sent one more message to the investor whose real estate listings tool sold to Zillow in 2014 for $3.5 billion. They were at a coffee shop below his San Francisco office, was he interested in meeting?

Fortunately for them, he was.

Modus co-founders Abbas Guvenilir (left), Jai Sim, Alex Day (right)

Modus, a real estate startup focused on title and escrow services, is today announcing a $12.5 million Series A financing co-led by NFX’s Flint and Niki Pezeshki of Felicis Ventures. Liquid 2 Ventures and existing backers, including Mucker Capital, Hustle Fund, 500 Startups, Rambleside and Cascadia Ventures, also participated in the round.

“The first revolution in online real estate was transforming the research experience, the next revolution in the industry is transforming the transaction,” Flint said in a statement.

Modus launched in 2018 with a focus on Washington (state) real estate opportunities. The startup, led by former employees of a nearly defunct lunch delivery company, Peach, has developed software to help both agents and home buyers navigate the home closing process, which, unlike many other real estate experiences, has yet to receive a boost of innovation from startups building in the sector. That’s why Modus started with an emphasis on escrow services, though the team’s long-term vision, they explain, is to power all real estate transactions.

“When you think about communication, you think of Gmail; when you think of traveling, you think of Uber. We want to be synonymous with home closing,” Sim, the company’s executive chairman, tells TechCrunch.

Day, Modus’ chief executive officer and former head of expansion at Peach, says Modus has ambitions of becoming a sort of operating system for real estate, or “like what Stripe is for payment processing, we want to become for real estate transactions.”

Since closing its Series A financing in May — the team waited until now to make its financing information public — Modus has increased its headcount to 50 employees across product, engineering and operations. Their goal now is to provide their software to home buyers in 15 to 20 states over the next two years. To support expansion efforts, Modus plans to raise a Series B in the second or third quarter of next year.

Modus previously raised $1.8 million in seed funding.

Powered by WPeMatico

San Francisco-based accelerator 500 Startups is expanding its executive team with the hiring of Tony Wang.

Wang is joining the early-stage firm from Color Genomics, a venture-backed developer of genetic testing kits where he had served as chief operating officer since 2014. Prior to Color, Wang was the vice president of global partnerships and development at Twitter and managing counsel for Google’s international operations.

“The venture capital world is undergoing a dramatic shift towards globalization where 500 Startups has been the leader and investing for the past decade,” Wang said in a statement. “There’s no question there are talented founders around the world, as proven by the number of unicorn companies in the 500 family.”

500 Startups, led by chief executive officer Christine Tsai, is an early investor in TalkDesk, Twilio, GitLab, Canva and several others.

Through its four-month seed program, the 500 Startups seed fund invests $150,000 in participating companies in exchange for 6% equity. Here’s a closer look at all the startups to finish 500 Startups’ latest program.

Powered by WPeMatico

It’s that time of year again. When startup founders fret for weeks on end as the long-awaited Demo Day approaches. Investors pore through lists of startups participating in various accelerator programs and have their associates ping dozens of founders for coffee meetings.

Demo Day season is upon us. Soon Y Combinator’s latest cohort of startups will pitch to investors for two days, beginning August 19, and 500 Startups, another San Francisco-based accelerator program for early-stage companies, will host its own Demo Day on August 22.

We’ll report live from YC’s Demo Day next month. For now, here’s a closer look at all the startups finishing out 500 Startups’ latest program. As a reminder, through its four-month seed program, the 500 Startups seed fund invests $150,000 in participating companies in exchange for 6% equity. The companies below include a mix of fintech, digital health, edtech and e-commerce businesses, 33% of which 500 Startups says are women-led and 40% have Black or Latinx founders.

Powered by WPeMatico

Jumia may be the first startup you’ve heard of from Africa. But the e-commerce venture that recently listed on the NYSE is definitely not the first or last word in African tech.

The continent has an expansive digital innovation scene, the components of which are intersecting rapidly across Africa’s 54 countries and 1.2 billion people.

When measured by monetary values, Africa’s tech ecosystem is tiny by Shenzen or Silicon Valley standards.

But when you look at volumes and year over year expansion in VC, startup formation, and tech hubs, it’s one of the fastest growing tech markets in the world. In 2017, the continent also saw the largest global increase in internet users—20 percent.

If you’re a VC or founder in London, Bangalore, or San Francisco, you’ll likely interact with some part of Africa’s tech landscape for the first time—or more—in the near future.

That’s why TechCrunch put together this Extra-Crunch deep-dive on Africa’s technology sector.

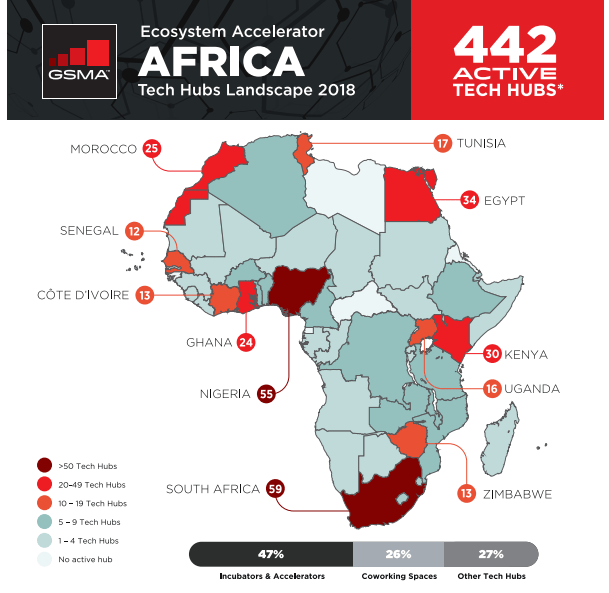

A foundation for African tech is the continent’s 442 active hubs, accelerators, and incubators (as tallied by GSMA). These spaces have become focal points for startup formation, digital skills building, events, and IT activity on the continent.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Blue-chip companies such as Google and Microsoft are also providing money and support. In 2018 Facebook opened its own Hub_NG in Lagos with partner CcHub, to foster startups using AI and machine learning.

Powered by WPeMatico

For a long time, it was the norm for founders to haul their hardware to the 3000 block of Sand Hill Road, where the venture capitalists of “Silicon Valley” would be awaiting their pitches. Today, many of the investors that touted the exclusivity of “The Valley” have moved north to San Francisco, where they have better access to top entrepreneurs.

Y Combinator, a Silicon Valley institution and to many the lifeblood of the startups and venture capital ecosystem, is the latest to pack up shop. YC, which invests $150,000 for 7 percent equity in a few hundred startups per year, is currently searching for a space in SF to operate its accelerator program, sources close to YC confirm to TechCrunch, because the majority of YC’s employees and its portfolio founders reside in the city.

Founded in 2005, YC’s roots are in Mountain View, California. In its first four years, YC offered programs in Cambridge, Massachusetts and Mountain View before opting in 2009 to focus exclusively on The Valley. In late 2013, as more and more of its partners and portfolio companies were establishing themselves in SF, YC opened a satellite office in the city in what would be the beginning of its journey northbound.

The small satellite office, used to support SF-based staff and provide portfolio companies resources and workspace, is located in Union Square. The fate of YC’s Mountain View office is unclear.

YC’s move north will be the latest in a series of small changes that, together, point to a new era for the accelerator. Approaching its 15th birthday, YC announced in September it was changing up the way it invests. No longer would it seed startups with $120,000 for 7 percent equity, it would give startups an additional 30,000 to cover the expenses of getting a business off the ground and it would admit a whole lot more companies.

YC began mentoring its largest cohort of companies to date in late 2018. The astonishing 200-plus group in its winter 2019 batch is more than 50 percent larger than the 132-team cohort that graduated in spring 2018. To accommodate the truly gigantic group at YC Demo Days later this month (March 18 and 19), YC has moved to a new venue, SF’s Pier 48. Historically, YC Demo Days were hosted at the Computer History Museum near its home in Mountain View.

YC has also ditched “Investor Day,” which is typically an opportunity for investors to schedule meetings with startups that just completed the accelerator program. YC writes that the decision came “after analyzing its effectiveness.” On top of that, rumors suggest YC is planning to put an end to Demo Days. Other accelerators, AngelPad for example, put a stop to the tradition last year after realizing demo day was more of a stress to startup founders than a resource. Sources close to YC, however, tell TechCrunch these rumors are categorically false.

YC isn’t the first accelerator to ditch its Silicon Valley digs. 500 Startups, a smaller yet still prolific accelerator, opened an SF satellite office the same year as YC, and in 2018, the nine-year-old program made the decision to permanently relocate to SF. Venture capital firms, too, have realized the opportunities are larger in SF than on Sand Hill Road.

The transition from the peninsula to the city began around 2012, when VC heavyweights like Uber and Twitter-backer Benchmark opened an office in SF’s mid-market neighborhood. Months later, 47-year-old Kleiner Perkins, an investor in Stripe and DoorDash, opened the doors to its new workplace in SF’s South Park neighborhood.

Around that same time a whole bunch of firms followed suit: Shasta Ventures, Norwest Venture Partners, Accel, GV, General Catalyst and NEA opened SF shops, to name a few. Many of these firms, Benchmark, Kleiner and Accel, for example, held onto their Silicon Valley locations. Firms like True Ventures and Peter Thiel’s Founders Fund planted stakes in SF years prior. Both firms have operated SF offices since 2005; True Ventures, for its part, has managed a Palo Alto office from the get-go, as well.

“When we first started, it was [expected] that it would be maybe 60-40 Peninsula to the city; it’s actually turned out to be 80-20 SF to The Valley,” True Ventures co-founder Phil Black told TechCrunch. “For us, it was important to be near our customer: the founder. It’s important for us to be in and around where founders are doing their things.”

The transition out of The Valley is ongoing. Other VC funds are still in the process of opening their first SF offices as more partners beg for shorter commutes. Khosla Ventures, for example, is currently searching for an SF headquarters.

Silicon Valley real estate will likely remain a hot — or warm, at least — commodity, however. Why? Because long-time investors have lives established in that part of the bay, where they’ve built homes in well-kept, affluent cities like Woodside, Atherton and Los Altos.

Still, Y Combinator’s move highlights an increasingly adopted mantra: Silicon Valley isn’t the goldmine it used to be. For the best deals and greatest access to entrepreneurs, SF takes the cake — for now, that is. But with rising rents and a changing attitude toward geographically diverse founders, how long SF will remain the destination for top talent is an entirely different question.

Powered by WPeMatico