2U

Auto Added by WPeMatico

Auto Added by WPeMatico

Reports on November 9 that a COVID-19 vaccine looks incredibly effective moved the market. Software stocks sold off and long-suffering industries hammered by the pandemic saw their fortunes rise. It was odd to see airlines soaring and 2020 high-fliers like Zoom taking blows.

But amidst all that noise, another sector that has great import for startups was also taking lumps: edtech.

Looking at how a number of edtech companies traded in the aftermath of the vaccine news helps us understand how public investors view the companies and assess their long-term growth prospects.

Simply put, selling edtech on the vaccine news — as investors did — was a bet that growth in the sector would be constrained by a return to normalcy, something a solid vaccine could hasten. This is a related concept to what TechCrunch discussed regarding software’s own November 9 selloff — that investors were betting that future growth for those companies, boosted in 2020 by the pandemic shaking up how and where people worked, would be limited by a quick return to regular life.

The vaccine’s reported efficacy changed how investors see the future. But how much did it change investor expectations for the future of edtech? Let’s examine the public market results before asking our own edtech expert Natasha Mascarenhas on what she’s seeing in the numbers and hearing from investors.

There aren’t many public edtech companies, but TechCrunch surveyed those that we knew about. Here’s where three stood after the closing bell rang on Friday, November 3:

Powered by WPeMatico

Before the coronavirus made edtech more relevant, companies in the sector were historically likely to see slow, low exits. Despite successful IPOs by 2U, Chegg and Instructure in the United States, public markets are not crowded with edtech companies.

Some of the largest exits in the space include LinkedIn’s scoop of Lynda for a $1.5 billion in cash and stock and TPG’s purchase of Ellucian for $3.5 billion.

But both of those deals happened in 2015. Five years later, edtech is cooler and surging — but is it seeing exits? Are Lynda and Ellucian one-off success stories?

2U’s co-founder and CEO, Chip Paucek, said he is optimistic.

“We are a rare edtech IPO,” he told TechCrunch last week. “For a long time in edtech it was either ‘sell to Pearson or not.’”

Despite the sector’s slow past, Paucek said now is a good time to start an edtech company because the sector “is finally starting to hit its stride” with more back-end infrastructure and demand for online education.

This morning, let’s use some data to paint a picture of the landscape of edtech exits and bring some balance to this stodgy stereotype.

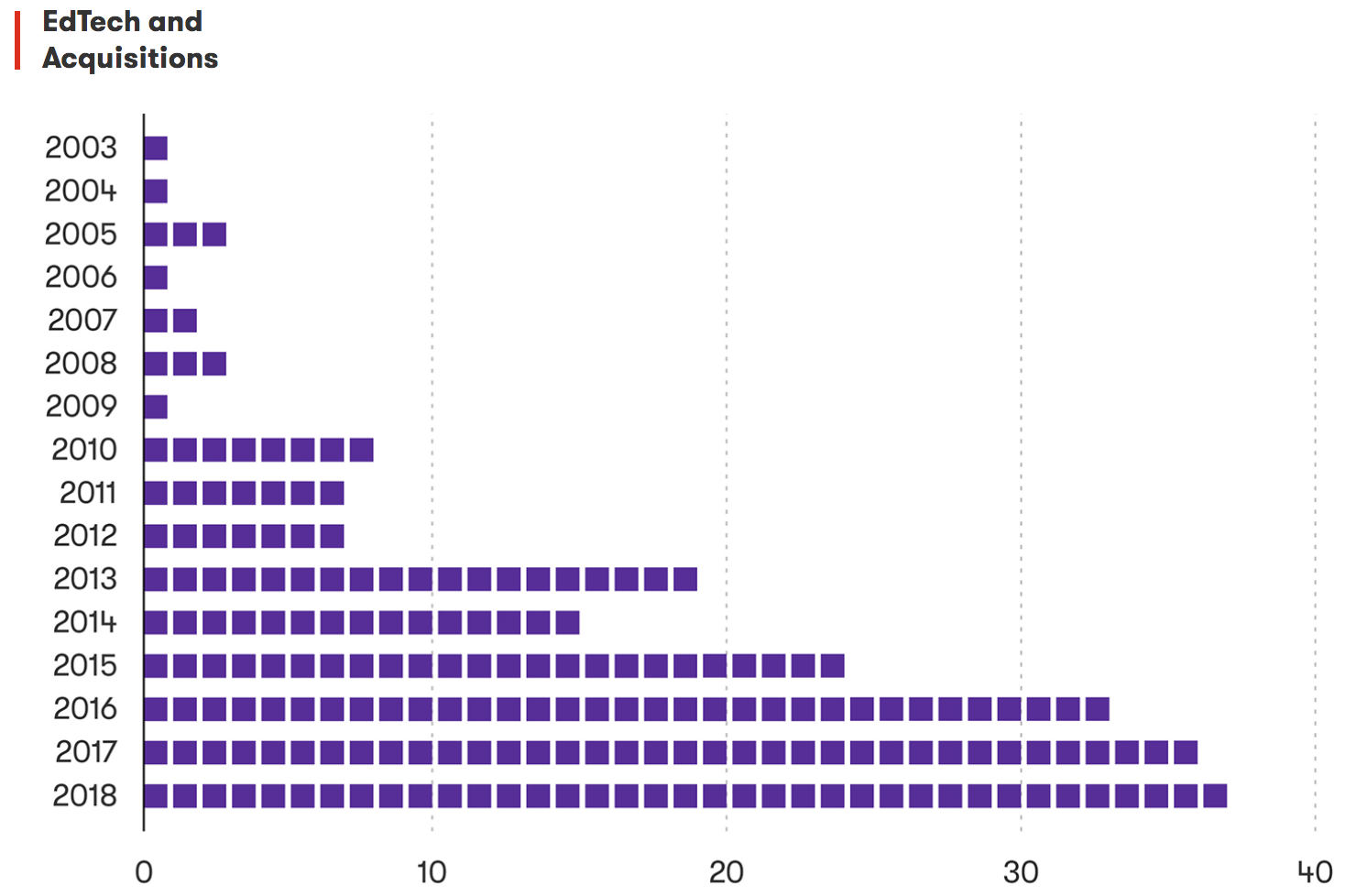

Boot the growth

Boot the growthThere have been approximately 225 acquisitions in edtech between 2003 and 2018, according to Crunchbase data. RS Components sent me a graph in March to contextualize this timeframe a bit more:

Edtech deals over time. Graph credit: RS Components.

Powered by WPeMatico

As more universities turn to offering online degrees to expand their student bodies by way of cyberspace, one of the pioneers in enabling that trend has made an acquisition to expand into new territory around skills training and continuing education. 2U, which helps build online degree programs for a number of top universities, is paying $750 million to acquire Trilogy Education, which creates online and in-person “boot camps” — continuing education programs — in collaboration with universities to train those already in the workforce with tech skills in areas like coding, data analytics, UX/UI and cybersecurity.

The deal, which is expected to close in the next 60 days, is coming in a combination of cash and shares — $400 million in cash and $350 million in newly issued shares of 2U common stock — the company said. It’s a decent exit for Trilogy, which was valued at $545 million (according to PitchBook) when it raised $50 million in June 2018. Its investors include Highland Capital, Macquarie and Exceed, among others.

2U, meanwhile, has a market cap of $3.85 billion and is publicly traded on Nasdaq.

The acquisition helps 2U consolidate its university footprint, which will get bumped up to 68 from its previous 36. And it presents an obvious opportunity to up-sell and cross-sell: those who are already jumping into building degree programs can diversify into more skills training, while those who have yet to build full degree services but have created skills training programs now might consider how to parlay that experience into degrees — all from one provider, 2U. This also opens more generally a bigger window for 2U to expand into the continuing education market, which it estimates is worth some $366 billion.

It also helps it better compete with other companies that have already built a dual-track approach to online education, building degrees as well as short courses, like Coursera (Udacity and Udemy are among those that have focused on further education).

“[Trilogy Education] is a natural strategic fit and growth driver for 2U that will extend our reach across the career curriculum continuum, deepen our relationships with new and existing partners, drive marketing efficiencies, and open a more direct corporate training and enterprise sales channel for the company. We expect the addition of Trilogy to accelerate our path to $1 billion in revenue by one year from 2022 to 2021,” 2U co-founder and CEO Christopher “Chip” Paucek said in a statement. “Increasingly, universities are attempting to add practical, technical skills to their degrees. We simply future-proof the degree by adding this type of technical competency.”

The presence of commercial companies building educational courses for nonprofit universities, and taking a cut in the process, has seen more than a little controversy. The business spin that is put on education through these programs not only calls into question how and what schools (and their partners) prioritise in the curriculum, but they raise issues around how higher education is priced, and who profits from these degrees — which sometimes can still cost more than $60,000, despite no physical time in classrooms. (There is an excellent dive into the issue here in the Huffington Post, featuring an interview with the co-founder of 2U, John Katzman, who also founded the Princeton Review.)

To be fair, some of the issues around higher education — such as the exorbitantly high cost in some countries, and the fact that it still feels like a largely elitist endeavor with the odds of students gaining acceptance and achieving in top universities still in favor of too-small a privileged subset of families — cannot be completely tied to the development of online learning courses powered by for-profit companies.

And you could also argue that this was bound to be the next step, given how technology has evolved across all of education, and the fact that edtech is not a core competency for many institutions.

One of the potential positives that comes out of online degree programs is that it gives opportunities to a much wider group of would-be students, and mass market is something that Trilogy knows: it has to date already provided courses for 20,000 people and 1,200 instructors across 120 programs, it says, with an emphasis on practical skills to bring up local workforces, and working with universities to build these courses and connecting with big companies — customers include Google, Microsoft and Bank of America — to deliver them.

“By joining forces with 2U, Trilogy Education can empower universities to reach more students, in more places, throughout more of their lives, while driving positive economic impact in their local regions,” Trilogy Education CEO and founder Dan Sommer said in a statement. “Trilogy and 2U share a belief that universities are critical to lifelong learning and to meeting the workforce development needs of local economies both domestically and internationally, and we’re proud to further our mission and continue this important work as part of the 2U family.

Powered by WPeMatico